Pricing Agreement

Exhibit 1.2

August 3, 2016

Barclays Capital Inc.

As representative of the several Underwriters

named in Schedule I (the “Representative”)

Ladies and Gentlemen:

Barclays PLC (the “Company”) proposes to issue an additional US$800,000,000 aggregate principal amount of 5.20% Subordinated Notes due 2026 (the “Notes”) to be consolidated and form a single series with the Notes issued on May 12, 2016. Each of the Underwriters hereby undertakes to purchase at the subscription price set forth in Schedule II hereto, the amount of Notes set forth opposite the name of such Underwriter in Schedule I hereto, such payment to be made at the Time of Delivery set forth in Schedule II hereto. The obligations of the Underwriters hereunder are several but not joint.

Each of the provisions of the Underwriting Agreement—Standard Provisions, dated September 4, 2014 (the “Underwriting Agreement”), is incorporated herein by reference in its entirety, and shall be deemed to be a part of this Agreement to the same extent as if such provisions had been set forth in full herein; and each of the representations and warranties set forth therein shall be deemed to have been made at and as of the date of this Agreement, except that each representation and warranty with respect to the Prospectus in Section 2 of the Underwriting Agreement shall be deemed to be a representation and warranty as of the date of the Prospectus and also a representation and warranty as of the date of this Agreement in relation to the Prospectus as amended or supplemented relating to the Notes. Each reference to the Representatives herein and in the provisions of the Underwriting Agreement so incorporated by reference shall be deemed to refer to you. Unless otherwise defined herein, terms defined in the Underwriting Agreement are used herein as therein defined. The Representative designated to act on behalf of each of the Underwriters of Designated Securities pursuant to Section 14 of the Underwriting Agreement and the address referred to in such Section 14 is set forth in Schedule II hereto.

An amendment to the Registration Statement, or a supplement to the Prospectus, as the case may be, relating to the Designated Securities, in the form heretofore delivered to you, is now proposed to be filed with the Commission.

The Applicable Time for purposes of this Pricing Agreement is 5:30 p.m. New York time on August 3, 2016. Each “free writing prospectus” as defined in Rule 405 under the Securities Act for which each party hereto has received consent to use in accordance with Section 7 of the Underwriting Agreement is listed in Schedule III hereto and is attached as Exhibit A hereto.

Where a resolution measure is taken in relation to any BRRD undertaking or any member of the same group as that BRRD undertaking and that BRRD undertaking or any member of the same group as that BRRD undertaking is a party to this Agreement (any such party to this Agreement being an “Affected Party”), each other party to this Agreement agrees that it shall only be entitled to exercise any termination right under this Agreement against the Affected Party to the extent that it would be entitled to do so under the Special Resolution Regime if this Agreement were governed by the laws of any part of the United Kingdom. For the purpose of this clause, “resolution measure” means a ‘crisis prevention measure,’ ‘crisis management measure’ or ‘recognised third-country resolution action,’ each with the meaning given in the “PRA Rulebook: CRR Firms and Non-Authorised Persons: Stay in Resolution Instrument 2015,” as may be amended from time to time (the “PRA Contractual Stay Rules”), provided, however, that ‘crisis prevention measure’ shall be interpreted in the manner outlined in Rule 2.3 of the PRA Contractual Stay Rules; “BRRD undertaking,” “group,” “Special Resolution Regime” and “termination right” have the respective meanings given in the PRA Contractual Stay Rules.

Notwithstanding and to the exclusion of any other term of this Agreement or any other agreements, arrangements, or understanding between the parties, each party acknowledges and accepts that a BRRD Liability arising under this Agreement may be subject to the exercise of Bail-in Powers by the Relevant Resolution Authority, and acknowledges, accepts, and agrees to be bound by:

(a) the effect of the exercise of Bail-in Powers by the Relevant Resolution Authority in relation to any BRRD Liability of each Covered Party to it under this Agreement, that (without limitation) may include and result in any of the following, or some combination thereof;

(i) the reduction of all, or a portion, of the BRRD Liability or outstanding amounts due thereon;

(ii) the conversion of all, or a portion, of the BRRD Liability into shares, other securities or other obligations of the relevant Covered Party or another person, and the issue to or conferral on the other party of such shares, securities or obligations;

(iii) the cancellation of the BRRD Liability; or

(iv) the amendment or alteration of any interest, if applicable, thereon, the maturity or the dates on which any payments are due, including by suspending payment for a temporary period;

(b) the variation of the terms of this Agreement, as deemed necessary by the Relevant Resolution Authority, to give effect to the exercise of Bail-in Powers by the Relevant Resolution Authority.

For these purposes:

“Bail-in Legislation” means in relation to a member state of the European Economic Area which has implemented, or which at any time implements, the BRRD, the relevant implementing law, regulation, rule or requirement as described in the EU Bail-in Legislation Schedule from time to time.

“Bail-in Powers” means any Write-down and Conversion Powers as defined in the EU Bail-in Legislation Schedule, in relation to the relevant Bail-in Legislation.

“BRRD” means Directive 2014/59/EU establishing a framework for the recovery and resolution of credit institutions and investment firms.

“Covered Party” means any party subject to the Bail-in Legislation.

“EU Bail-in Legislation Schedule” means the document described as such, then in effect, and published by the Loan Market Association (or any successor person) from time to time at xxxx://xxx.xxx.xx.xxx/xxxxx.xxxx?xx000.

“BRRD Liability” means a liability in respect of which the relevant Write Down and Conversion Powers in the applicable Bail-in Legislation may be exercised.

“Relevant Resolution Authority” means the resolution authority with the ability to exercise any Bail-in Powers in relation to the relevant Covered Party.

If the foregoing is in accordance with your understanding, please sign and return to us the counterpart hereof, and upon acceptance hereof by you, on behalf of each of the Underwriters, this letter and such acceptance hereof, including the provisions of the Underwriting Agreement incorporated herein by reference, shall constitute a binding agreement between each of the Underwriters on the one hand and the Company on the other.

| Very truly yours, |

| BARCLAYS PLC |

| /s/ Miray Muminoglu |

| Name: Miray Muminoglu |

| Title: Co-Head of Capital Markets Execution |

| Accepted as of the date hereof at New York, New York |

| On behalf of itself and each of the other Underwriters

BARCLAYS CAPITAL INC. |

| /s/ Xxxx Xxxxx-Xxxxxx |

| Name: Xxxx Xxxxx-Xxxxxx |

| Title: Managing Director |

SCHEDULE I

| Underwriter |

Principal Amount of Notes | |||

| Barclays Capital Inc |

US$ | 664,000,000 | ||

| Academy Securities, Inc. |

8,000,000 | |||

| BMO Capital Markets Corp. |

8,000,000 | |||

| Danske Markets Inc |

8,000,000 | |||

| ING Financial Markets LLC |

8,000,000 | |||

| Lebenthal & Co, LLC. |

8,000,000 | |||

| Loop Capital Markets LLC |

8,000,000 | |||

| Mizuho Securities USA Inc. |

8,000,000 | |||

| PNC Capital Markets LLC |

8,000,000 | |||

| Rabo Securities USA, Inc. |

8,000,000 | |||

| Regions Securities LLC |

8,000,000 | |||

| Santander Investment Securities Inc. |

8,000,000 | |||

| Scotia Capital (USA) Inc. |

8,000,000 | |||

| Xxxxxxx Xxxxxxxxx Xxxxx & Co., L.L.C. |

8,000,000 | |||

| SMBC Nikko Securities America, Inc. |

8,000,000 | |||

| TD Securities (USA) LLC |

8,000,000 | |||

| The Xxxxxxxx Capital Group, L.P. |

8,000,000 | |||

| Xxxxx Fargo Securities, LLC |

8,000,000 | |||

|

|

|

|||

| Total |

US$ | 800,000,000 | ||

SCHEDULE II

Title of Designated Securities:

US$800,000,000 5.20% Fixed Rate Subordinated Notes due 2026

The Notes offered under this Pricing Agreement will have the same terms (other than the price to public and date of delivery), form part of the same series and trade freely with the Notes issued on May 12, 2016.

Price to Public:

102.789% of principal amount plus accrued interest from and including May 12, 2016 up to but excluding the date of delivery, which is expected to be August 10, 2016, in the amount of $10,168,888.89

Subscription Price by Underwriters:

102.339% of principal amount plus accrued interest from and including May 12, 2016 up to but excluding the date of delivery, which is expected to be August 10, 2016, in the amount of $10,168,888.89

Form of Designated Securities:

The Notes will be represented by one or more global notes registered in the name of Cede & Co., as nominee of The Depository Trust Company issued pursuant to the Dated Subordinated Debt Indenture, dated September 11, 2014, between the Company and The Bank of New York Mellon acting through its London Branch, as trustee (the “Trustee”), as supplemented by the Second Supplemental Indenture between the Company and the Trustee entered into on May 12, 2016 (as amended on the date of delivery)

Securities Exchange, if any:

The New York Stock Exchange

Maturity Date:

The stated maturity of the principal of the Notes will be May 12, 2026.

Interest Rate:

Interest will accrue on the Notes at a rate of 5.20% per year from and including May 12, 2016.

Interest Payment Dates:

Interest will be payable semi-annually in arrear on May 12 and November 12 of each year, commencing on November 12, 2016 and ending on the Maturity Date.

Record Dates:

The Business Day immediately preceding each Interest Payment Date (or, if the Notes are held in definitive form, the 15th Business Day preceding each Interest Payment Date).

Sinking Fund Provisions:

No sinking fund provisions.

Redemption Provisions for Notes:

The Notes are redeemable, at the option of the Company, (i) in the event of various tax law changes and other limited circumstances that have specified consequences, and (ii) in the event of certain regulatory changes or events, each as described further in, and subject to the conditions specified in, the prospectus supplement dated May 5, 2016 relating to the Notes.

Time of Delivery:

August 10, 2016 by 9:30 a.m. New York time.

Specified Funds for Payment of Subscription Price of Designated Securities:

By wire transfer to a bank account specified by the Company in same day funds.

Value Added Tax:

(a) If the Company is obliged to pay any sum to the Underwriters under this Agreement and any value added tax (“VAT”) is properly charged on such amount, the Company shall pay to the Underwriters an amount equal to such VAT on receipt of a valid VAT invoice;

(b) If the Company is obliged to pay a sum to the Underwriters under this Agreement for any fee, cost, charge or expense properly incurred under or in connection with this Agreement (the “Relevant Cost”) and no VAT is payable by the Company in respect of the Relevant Cost under paragraph (a) above, the Company shall pay to the Underwriters an amount which:

(i) if for VAT purposes the Relevant Cost is consideration for a supply of goods or services made to the Underwriters, is equal to any input VAT incurred by the Underwriters on that supply of goods and services, but only if and to the extent that the Underwriters are unable to recover such input VAT from HM Revenue & Customs (whether by repayment or credit) provided, however, that the Underwriters shall reimburse the Company for any amount paid by the Company in respect of irrecoverable input VAT pursuant to this paragraph (i) if and to the extent such input VAT is subsequently recovered from HM Revenue & Customs (whether by repayment or credit);

(ii) if for VAT purposes the Relevant Cost is a disbursement properly incurred by the Underwriters under or in connection with this Agreement as agent on behalf of the Company, is equal to any VAT paid on the Relevant Cost by the Underwriters provided, however, that the Underwriters shall use best endeavors to procure that the actual supplier of the goods or services which the Underwriters received as agent issues a valid VAT invoice to the Company.

Closing Location: Linklaters LLP, Xxx Xxxx Xxxxxx, Xxxxxx XX0X 0XX, Xxxxxx Xxxxxxx.

Name and address of Representative:

Designated Representative: Barclays Capital Inc.

Address for Notices:

Barclays Capital Inc.

000 Xxxxxxx Xxxxxx

Xxx Xxxx, XX 00000

Attn: Syndicate Registration

Selling Restrictions:

Each Underwriter of Designated Securities has represented, warranted and agreed that:

| a) | it has only communicated or caused to be communicated, and will only communicate or cause to be communicated, any invitation or inducement to engage in investment activity (within the meaning of Section 21 of the Financial Services and Markets Xxx 0000, as amended (the “FSMA”)) received by it in connection with the issue or sale of any Designated Securities in circumstances in which Section 21(1) of the FSMA does not apply to the Company; and |

| b) | it has complied and will comply with all applicable provisions of the FSMA with respect to anything done by it in relation to the Designated Securities in, from or otherwise involving the United Kingdom. |

With respect to sales of the Designated Securities in Canada, each Underwriter of Designated Securities represents to and agrees with the Company that, directly or indirectly, it shall sell the Designated Securities only to purchasers purchasing as principal that are both “accredited investors” as defined in National Instrument 45-106 Prospectus and Registration Exemptions and “permitted clients” as defined in National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations.

Other Terms and Conditions:

As set forth in the prospectus supplement dated May 5, 2016 relating to the Notes, incorporating the Prospectus dated May 2, 2014 relating to the Notes.

SCHEDULE III

Issuer Free Writing Prospectus:

Final Term Sheet, dated August 3, 2016, attached hereto as Exhibit A

Barclays PLC Fixed Income Investor Presentation: H1 2016 Results Announcement, dated July 2016, attached hereto as Exhibit B

Exhibit A

USD 800m Reopening of 5.20% Fixed Rate Subordinated

Notes due 2026

Pricing Term Sheet

| Issuer: |

Barclays PLC | |

| Notes: |

5.20% Fixed Rate Subordinated Notes due 2026 | |

| Expected Issue Ratings:1 |

Baa3 (Xxxxx’x) / BB+ (S&P) / A– (Fitch) | |

| Status: |

Dated Subordinated Debt / Unsecured / Tier 2 | |

| Legal Format: |

SEC registered | |

| Original Principal Amount: |

USD 1,250,000,000 | |

| Reopening Amount: |

USD 800,000,000 | |

| Principal Amount after Reopening: |

USD 2,050,000,000 | |

| Fungibility |

Yes | |

| Original Issue Date: |

May 12, 2016 | |

| Reopening Trade Date: |

August 3, 2016 | |

| Reopening Issue Date: |

August 10, 2016 (T+5) | |

| Maturity Date: |

May 12, 2026 | |

| Coupon: |

5.20% | |

| Interest Payment Dates: |

Semi-annually in arrear on May 12 and November 12 in each year, commencing on November 12, 2016 and ending on the Maturity Date | |

| Coupon Calculation: |

30/360, following, unadjusted | |

| Business Days: |

New York, London | |

| U.K. Bail-in Power Acknowledgement: |

Yes. See section entitled “Description of Subordinated Notes—Agreement with Respect to the Exercise of U.K. Bail-in Power” in the Prospectus Supplement dated May 5, 2016 (the “Original Prospectus Supplement”). | |

| Regulatory Event Redemption |

If there is a change in the regulatory classification of the Notes that occurs on or after the original issue date of the Notes and that does, or would be likely to, result in the whole or any part of the outstanding aggregate principal amount of the notes at any time being excluded from or ceasing to count towards, the Group’s Tier 2 Capital (a “Regulatory Event”), the Issuer may, at its option, at any time, redeem the Notes, in whole but not in part, at a redemption price equal to 100% of their principal amount, together with any accrued but unpaid interest to (but excluding) the date fixed for redemption. Any redemption upon the occurrence of a Regulatory Event will be subject to the provisions described in the Original Prospectus Supplement. | |

| 1 | Note: A securities rating is not a recommendation to buy, sell or hold securities and may be subject to revision or withdrawal at any time. |

| Tax Redemption |

If there is a Tax Event (as defined in the Original Prospectus Supplement), the Issuer may, at its option, at any time, redeem the Notes, in whole but not in part, at a redemption price equal to 100% of their principal amount, together with any accrued but unpaid interest to (but excluding) the date fixed for redemption, as further described and subject to the conditions specified in the Original Prospectus Supplement. | |

| Benchmark Treasury: |

T 1.625 05/15/26 | |

| Spread to Benchmark on the Reopended Notes: |

330bps | |

| Reoffer Yield on the Reopended Notes: |

4.837% | |

| Issue Price on the Reopended Notes: |

102.789% plus accrued interest from and including May 12, 2016 to (but excluding) August 10, 2016 | |

| Aggregate Accrued Interest on the Reopended Notes: |

USD 10,168,888.89 | |

| Underwriting Discount on the Reopended Notes: |

0.45% | |

| Net Proceeds from the Reopening including accrued interest: |

USD 828,880,888.89 | |

| Sole Bookrunner: |

Barclays Capital Inc. | |

| Co-managers: |

Academy Securities, Inc.; BMO Capital Markets Corp.; Danske Markets Inc; ING Financial Markets LLC; Lebenthal & Co, LLC.; Loop Capital Markets LLC; Mizuho Securities USA Inc.; PNC Capital Markets LLC; Rabo Securities USA, Inc.; Regions Securities LLC; Santander Investment Securities Inc.; Scotia Capital (USA) Inc.; Xxxxxxx Xxxxxxxxx Xxxxx & Co., L.L.C.; SMBC Nikko Securities America, Inc.; TD Securities (USA) LLC; The Xxxxxxxx Capital Group, L.P.; Xxxxx Fargo Securities, LLC | |

| Risk Factors: |

An investment in the Notes involves risks. See “Risk Factors” section beginning on page S-16 of the Original Prospectus Supplement. | |

| U.S. Federal Income Tax Considerations: |

The following supplements a discussion under “Tax Considerations—U.S. Taxation of Debt Securities” in the prospectus dated May 2, 2014 (the “Prospectus”) and is subject to the limitations and exceptions set forth therein. Interest on the Notes should generally be taxed as ordinary income at the time interest is received or when it accrues, depending on the method of accounting for tax purposes. However, the portion of the first interest payment on the Notes that represents a return of the accrued interest paid upon the purchase of the Notes will not be treated as an interest payment for U.S. federal income tax purposes, but will instead be excluded from income and will reduce the basis in the Notes by such amount. | |

| Denominations: |

USD 200,000 and integral multiples of USD 1,000 in excess thereof | |

| ISIN/CUSIP: |

US06738EAP07 / 06738E AP0 | |

| Settlement: |

DTC; Book-entry; Transferable | |

| Documentation: |

To be documented under the Issuer’s shelf registration statement on Form F-3 (No. 333-195645) and to be issued pursuant to the Dated Subordinated Debt Indenture, dated September 11, 2014, between the Issuer and The Bank of New York Mellon acting through its London Branch, as trustee (the “Trustee”), as supplemented by the Second Supplemental Indenture between the Issuer and the Trustee entered into on May 12, 2016 (as amended) | |

| Listing: |

We will apply to list the reopened Notes on the New York Stock Exchange | |

| Governing Law: |

New York law, except for subordination provisions and waiver of set-off provisions which will be governed by English law | |

-2-

| Definitions: |

Unless otherwise defined herein, all capitalized terms have the meaning set forth in the Original Prospectus Supplement | |

The Issuer has filed a registration statement (including the Prospectus and the Original Prospectus Supplement) with the U.S. Securities and Exchange Commission (“SEC”) for this offering. Before you invest, you should read the Prospectus and the Original Prospectus Supplement for this offering in that registration statement, and other documents the Issuer has filed with the SEC for more complete information about the issuer and this offering. You may get these documents for free by searching the SEC online database (XXXXX®) at xxx.xxx.xxx. Alternatively, you may obtain a copy of the Prospectus and the Original Prospectus Supplement from Barclays Capital Inc. by calling 0-000-000-0000.

-3-

Exhibit B

|

Barclays PLC

Fixed Income Investor Presentation

H1 2016 Results Announcement July 2016

|

STRATEGY & HOLDCO

CAPITAL STRUCTURAL LIQUIDITY

PERFORMANCE TRANSITION ASSET QUALITY CREDIT RATING APPENDIX

& LEVERAGE REFORM & FUNDING

OVERVIEW & MREL/TLAC

Strategy & Performance

Overview

|

STRATEGY & HOLDCO

CAPITAL STRUCTURAL LIQUIDITY

PERFORMANCE TRANSITION ASSET QUALITY CREDIT RATING APPENDIX

& LEVERAGE REFORM & FUNDING

OVERVIEW & MREL/TLAC

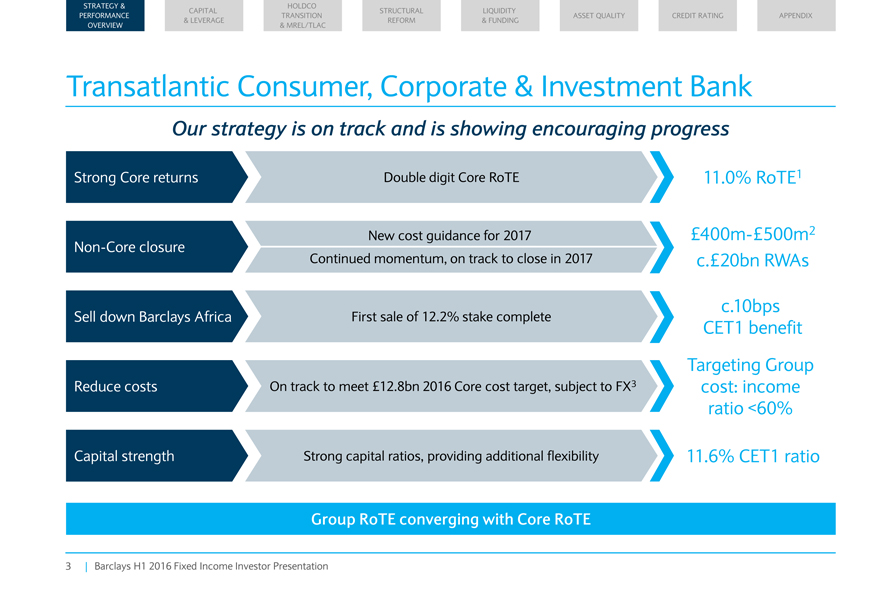

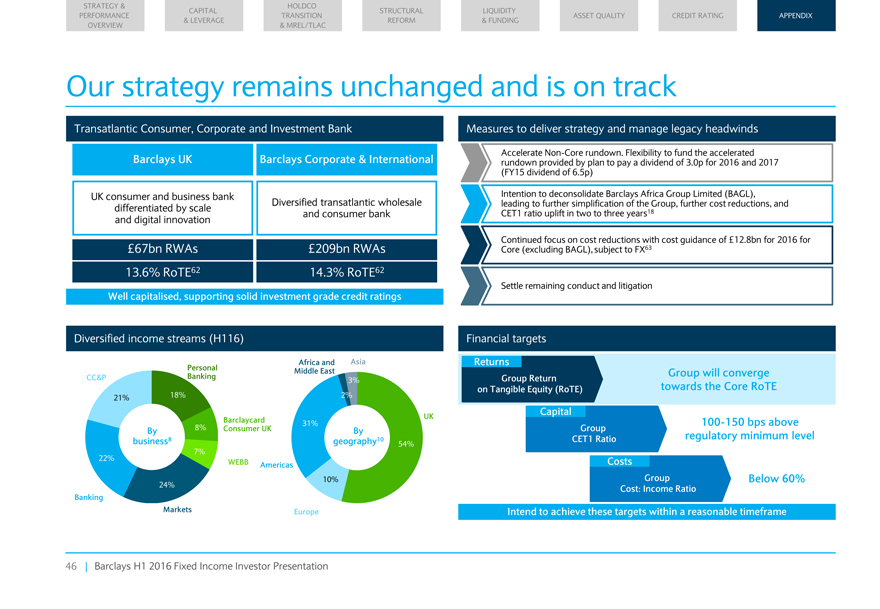

Transatlantic Consumer, Corporate & Investment Bank

Our strategy is

on track and is showing encouraging progress

Strong Core returns Double digit Core RoTE 11.0% RoTE1

New cost guidance for 2017 £400m-£500m2

Non-Core closure

Continued momentum, on track to close in 2017 c.£20bn RWAs

c.10bps

Sell down Barclays Africa First sale of 12.2% stake complete

CET1 benefit Targeting Group

Reduce costs On track to meet £12.8bn 2016 Core cost target, subject to FX3 cost: income

ratio <60%

Capital strength Strong capital ratios, providing additional flexibility 11.6%

CET1 ratio

Group RoTE converging with Core RoTE

Barclays H1 2016 Fixed Income

Investor Presentation

| 3 |

|

STRATEGY & HOLDCO

CAPITAL STRUCTURAL LIQUIDITY

PERFORMANCE TRANSITION ASSET QUALITY CREDIT RATING APPENDIX

& LEVERAGE REFORM & FUNDING

OVERVIEW & MREL/TLAC

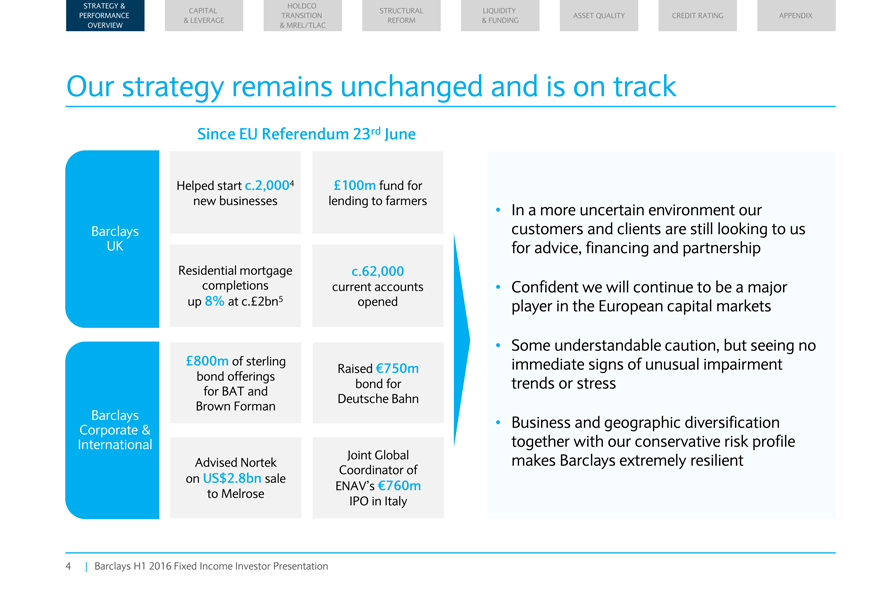

Our strategy remains unchanged and is on track

Since EU Referendum

23rd June

Helped start c.2,0004 £100m fund for new businesses lending to farmers

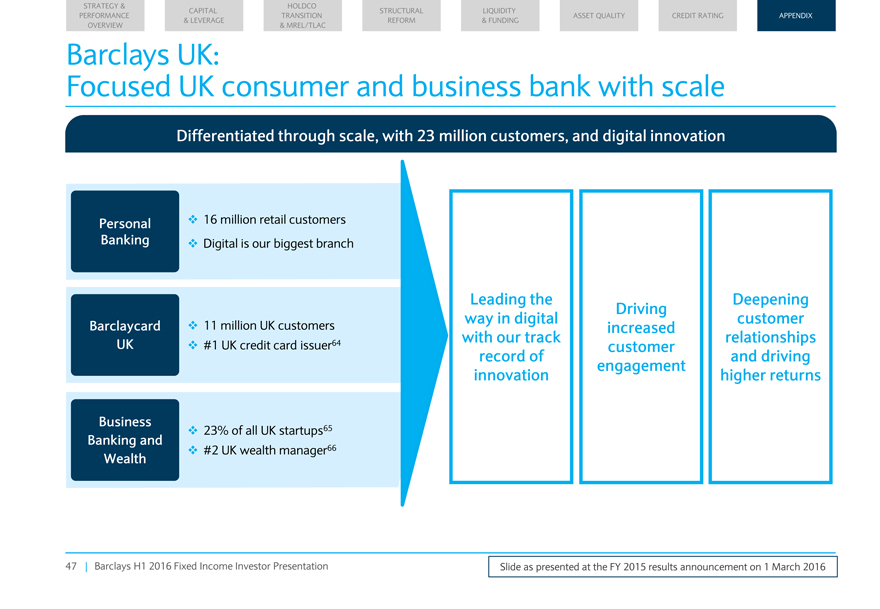

Barclays UK

Residential mortgage c.62,000 completions current accounts up 8% at c.£2bn5

opened

£800m of sterling

Raised €750m bond offerings bond for for

BAT and Deutsche Bahn Xxxxx Xxxxxx

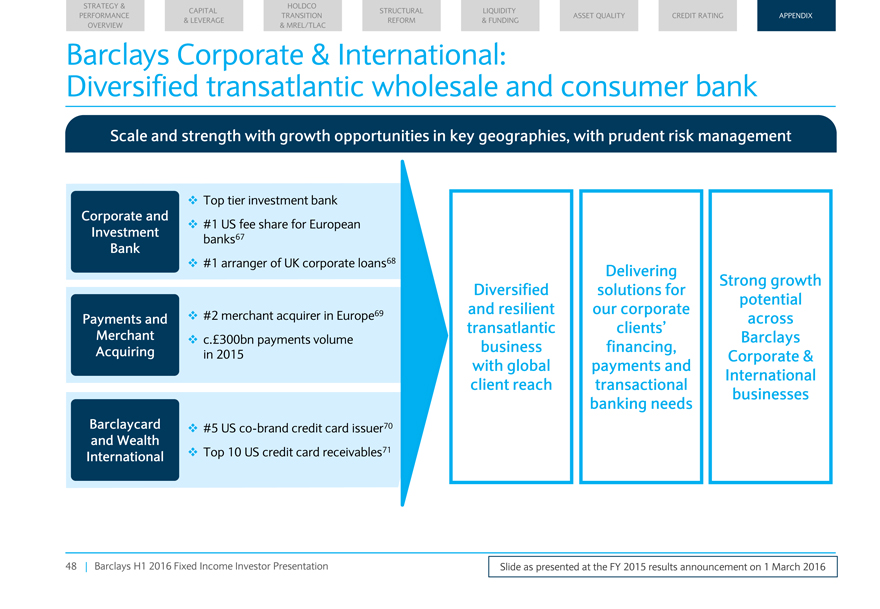

Barclays Corporate & International

Joint Global Advised Nortek Coordinator of on US$2.8bn sale

ENAV?s €760m

to Melrose IPO in Italy

In a more uncertain environment our customers and clients are still looking to us for advice, financing and partnership

Confident we will continue to be a major player in the European capital markets

Some

understandable caution, but seeing no immediate signs of unusual impairment trends or stress

Business and geographic diversification together with our conservative

risk profile makes Barclays extremely resilient

Barclays H1 2016 Fixed Income Investor Presentation

| 4 |

|

STRATEGY & HOLDCO

CAPITAL STRUCTURAL LIQUIDITY

PERFORMANCE TRANSITION ASSET QUALITY CREDIT RATING APPENDIX

& LEVERAGE REFORM & FUNDING

OVERVIEW & MREL/TLAC

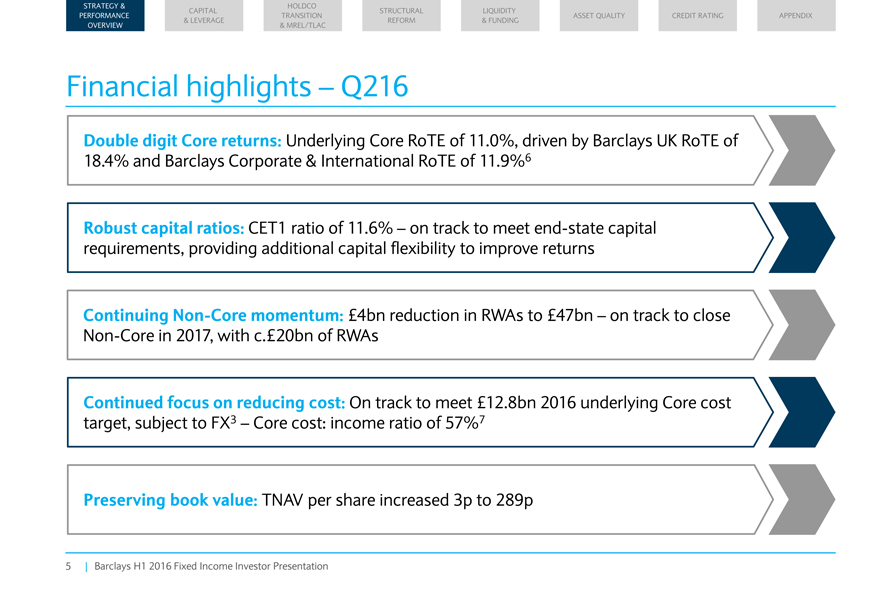

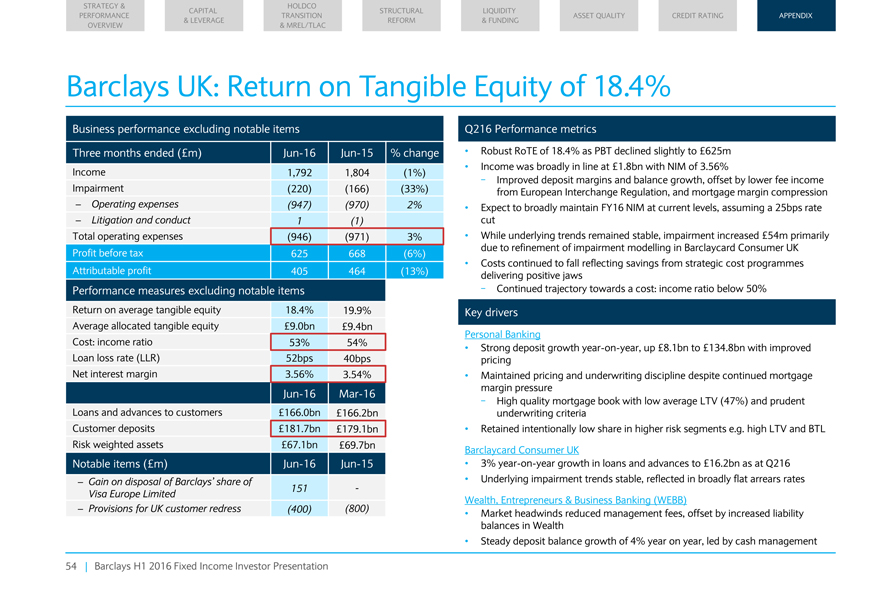

Financial highlights – Q216

Double digit Core returns: Underlying Core

RoTE of 11.0%, driven by Barclays UK RoTE of 18.4% and Barclays Corporate & International RoTE of 11.9%6

Robust capital ratios: CET1 ratio of 11.6% –

on track to meet end-state capital requirements, providing additional capital flexibility to improve returns

Continuing Non-Core momentum: £4bn reduction in

RWAs to £47bn – on track to close Non-Core in 2017, with c.£20bn of RWAs

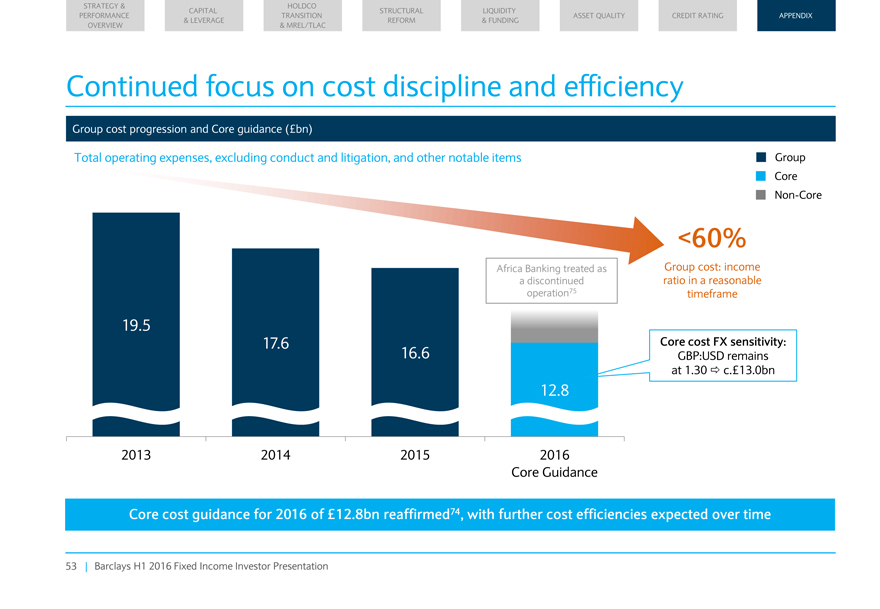

Continued focus on reducing cost: On track to meet £12.8bn 2016

underlying Core cost target, subject to FX3 – Core cost: income ratio of 57%7

Preserving book value: TNAV per share increased 3p to 289p

Barclays H1 2016 Fixed Income Investor Presentation

| 5 |

|

STRATEGY & HOLDCO

CAPITAL STRUCTURAL LIQUIDITY

PERFORMANCE TRANSITION ASSET QUALITY CREDIT RATING APPENDIX

& LEVERAGE REFORM & FUNDING

OVERVIEW & MREL/TLAC

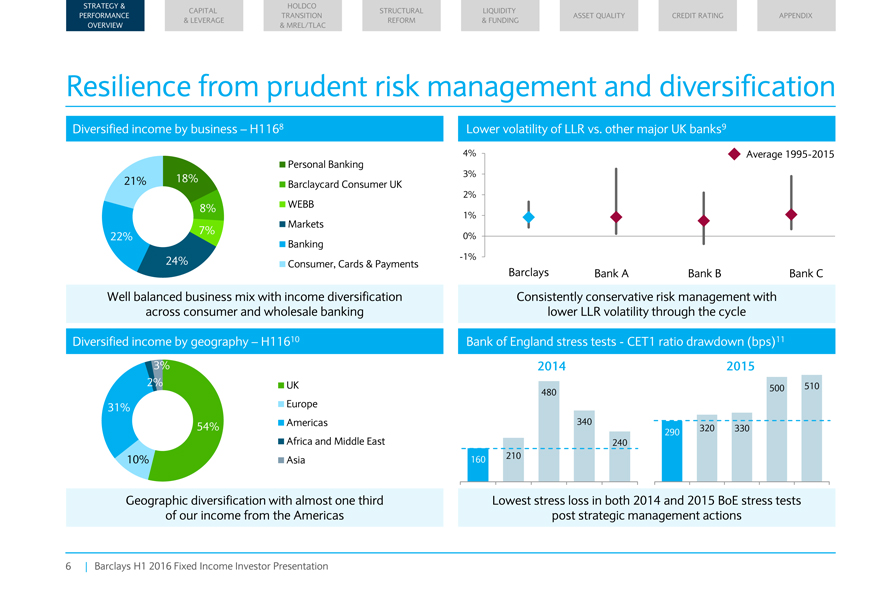

Resilience from prudent risk management and diversification

Diversified

income by business – H1168 Lower volatility of LLR vs. other major UK banks9

4% Average 1995-2015 Personal Banking 3%

21% 18%

Barclaycard Consumer UK

XXXX 2%

8%

1%

Markets

7%

22% 0%

Banking

24% -1%

Consumer, Cards & Payments

Barclays Bank A Bank B Bank C

Well balanced business mix with income diversification Consistently conservative risk management with across consumer and wholesale banking lower LLR volatility through the cycle

Diversified income by geography – H11610 Bank of England stress tests—CET1 ratio drawdown (bps)11

3% 2014 2015

2% UK 510 480 500

31% Europe

54% Americas 340

290 320 330

Africa and Middle East 240

10% Asia 160 210

Geographic diversification with almost one third Lowest stress loss in both

2014 and 2015 BoE stress tests of our income from the Americas post strategic management actions

Barclays H1 2016 Fixed Income Investor Presentation

| 6 |

|

STRATEGY & HOLDCO

CAPITAL STRUCTURAL LIQUIDITY

PERFORMANCE TRANSITION ASSET QUALITY CREDIT RATING APPENDIX

& LEVERAGE REFORM & FUNDING

OVERVIEW & MREL/TLAC

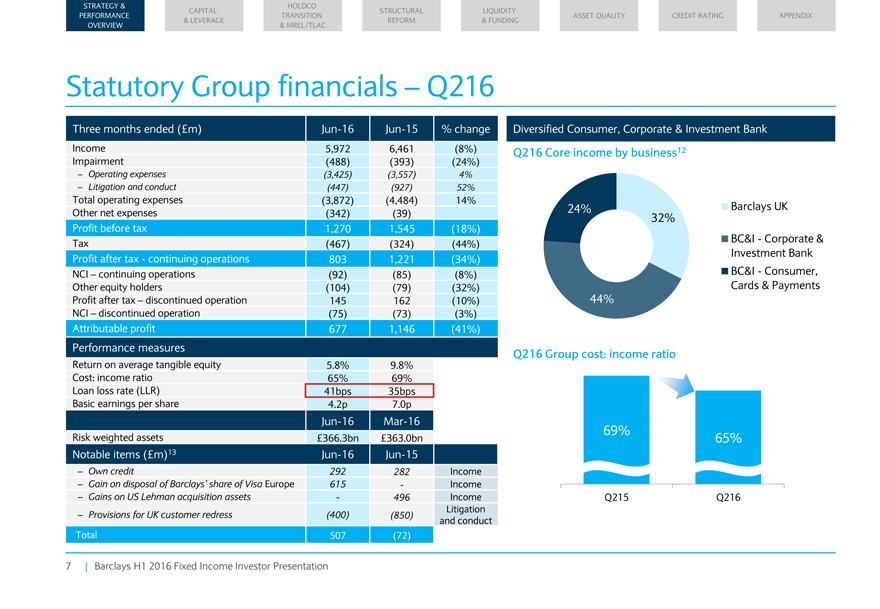

Statutory Group financials – Q216

Three months ended

(£m) Jun-16 Jun-15% change Diversified Consumer, Corporate & Investment Bank

Income 5,972 6,461(8%) Q216 Core income by business12

Impairment(488)(393)(24%)

– Operating expenses(3,425)(3,557) 4%

– Litigation and conduct(447)(927) 52%

Total operating expenses(3,872)(4,484) 14%

Other net expenses(342)(39) 24% 32% Barclays UK

Profit before tax 1,270

1,545(18%)

Tax(467)(324)(44%) BC&I—Corporate &

Profit after

tax—continuing operations 803 1,221(34%) Investment Bank

NCI – continuing operations(92)(85)(8%) BC&I—Consumer,

Other equity holders(104)(79)(32%) Cards & Payments

Profit after tax –

discontinued operation 145 162(10%) 44%

NCI – discontinued operation(75)(73)(3%)

Attributable profit 677 1,146(41%)

Performance measures Q216 Group cost: income ratio

Return on average tangible equity 5.8% 9.8%

Cost: income ratio 65% 69%

Loan loss rate (LLR) 41bps 35bps

Basic earnings per share 4.2p 7.0p

Jun-16 Mar-16 69%

Risk weighted assets £366.3bn £363.0bn 65%

Notable items (£m)13 Jun-16 Jun-15

– Own credit 292 282 Income

– Gain on disposal of Barclays’ share of Visa Europe 615—Income

– Gains on US Xxxxxx acquisition assets—496 Income Q215 Q216

Litigation

– Provisions for UK customer redress(400)(850) and conduct

Total 507(72)

Barclays H1 2016 Fixed Income Investor Presentation

| 7 |

|

STRATEGY & HOLDCO

CAPITAL STRUCTURAL LIQUIDITY

PERFORMANCE TRANSITION ASSET QUALITY CREDIT RATING APPENDIX

& LEVERAGE REFORM & FUNDING

OVERVIEW & MREL/TLAC

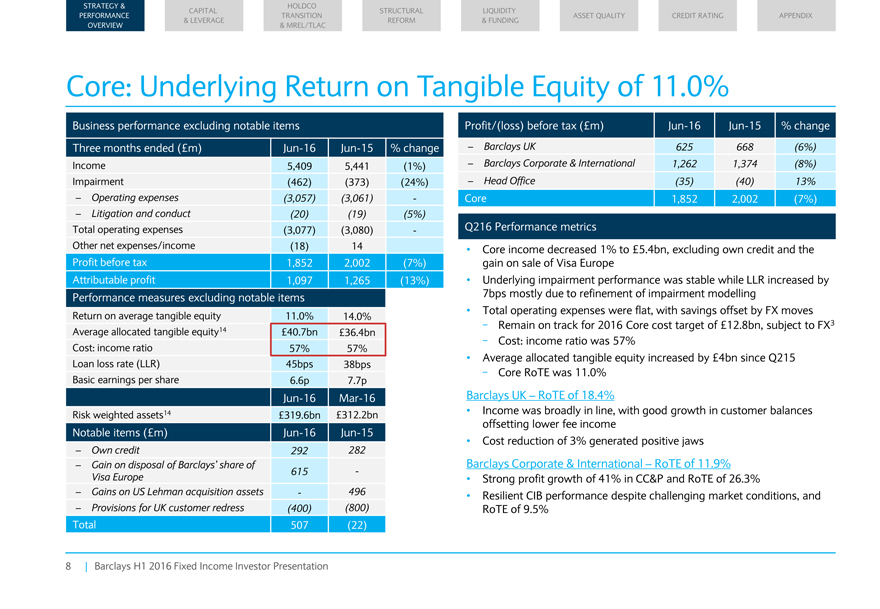

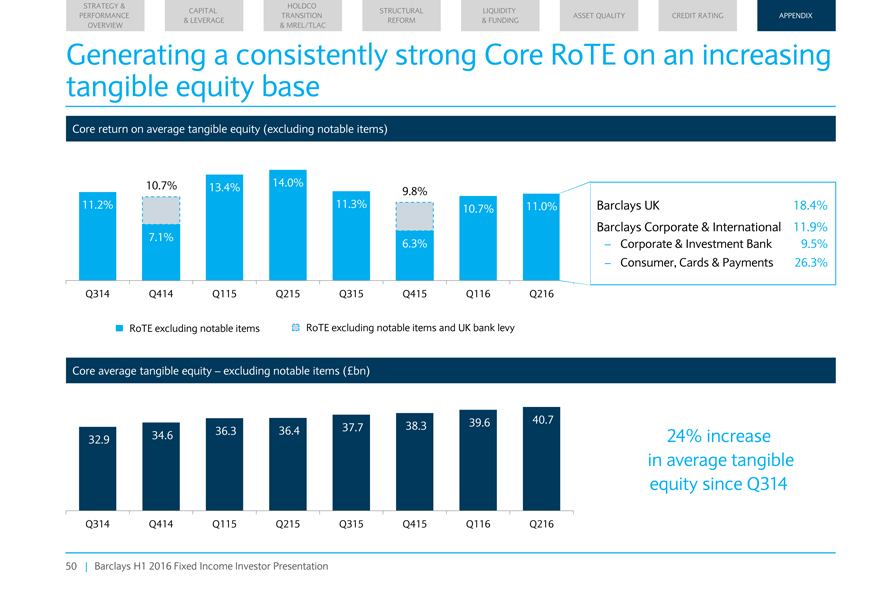

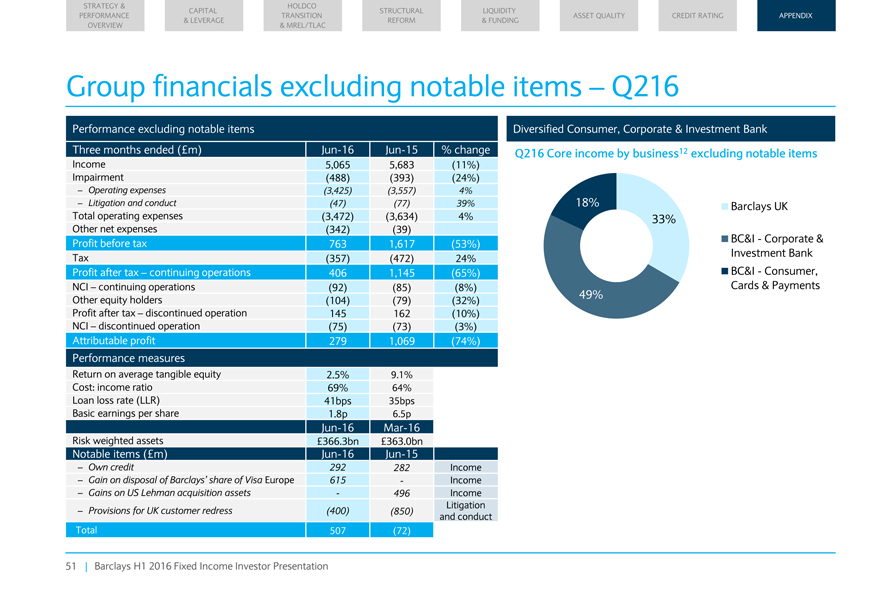

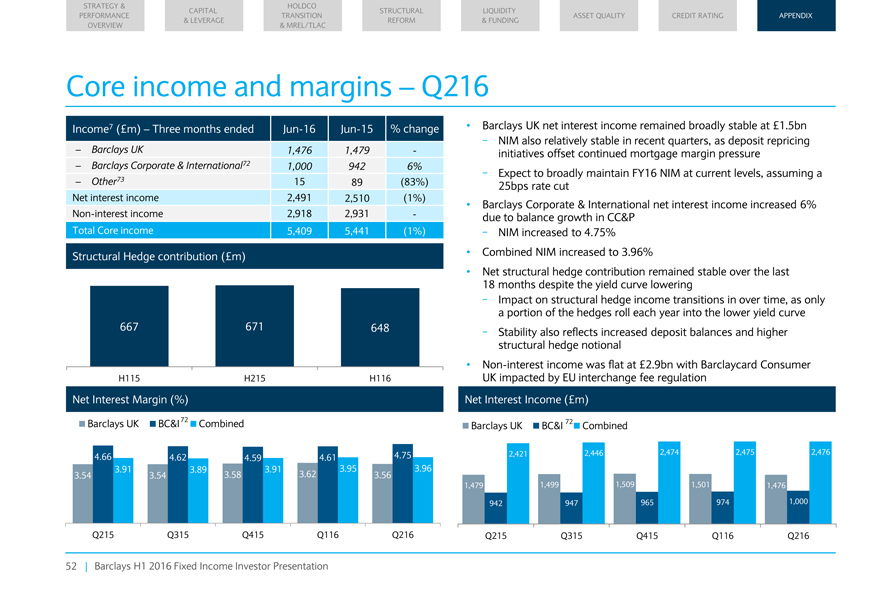

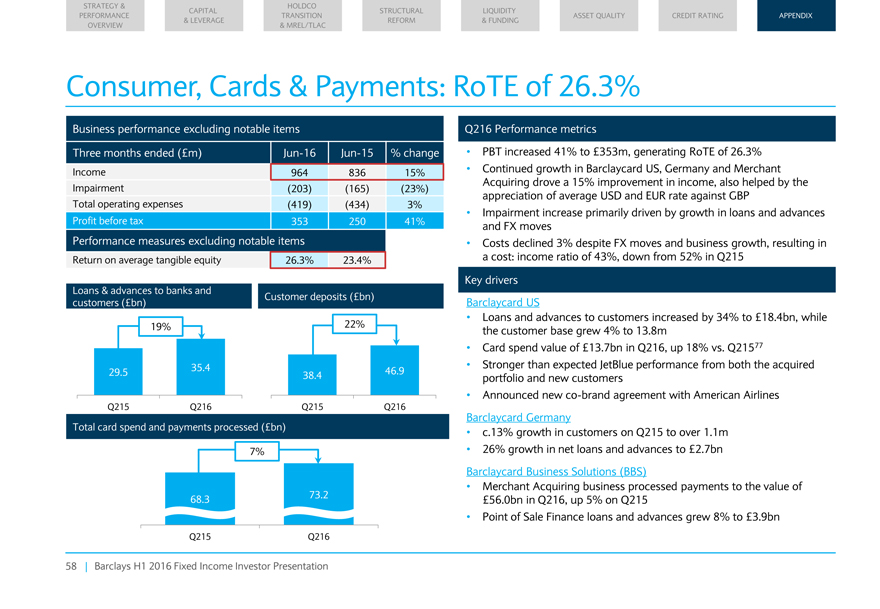

Core: Underlying Return on Tangible Equity of 11.0%

Business performance

excluding notable items Profit/(loss) before tax (£m) Jun-16 Jun-15% change

Three months ended (£m) Jun-16 Jun-15% change – Barclays UK

625 668(6%)

Income 5,409 5,441(1%) – Barclays Corporate & International 1,262 1,374(8%)

Impairment(462)(373)(24%) – Head Office(35)(40) 13%

– Operating

expenses(3,057)(3,061)—Core 1,852 2,002(7%)

– Litigation and conduct(20)(19)(5%)

Total operating expenses(3,077)(3,080)—Q216 Performance metrics

Other net

expenses/income(18) 14 Core income decreased 1% to £5.4bn, excluding own credit and the

Profit before tax 1,852 2,002(7%) gain on sale of Visa Europe

Attributable profit 1,097 1,265(13%) Underlying impairment performance was stable while LLR increased by

Performance measures excluding notable items 7bps mostly due to refinement of impairment modelling

Return on average tangible equity 11.0% 14.0% Total operating expenses were flat, with savings offset by FX moves

Average allocated tangible equity14 £40.7bn £36.4bn—Remain on track for 2016 Core cost target of £12.8bn, subject to FX3

Cost: income ratio 57% 57%—Cost: income ratio was 57%

Loan loss rate (LLR) 45bps 38bps

Average allocated tangible equity increased by £4bn since Q215

Basic earnings per share 6.6p 7.7p—Core RoTE was 11.0%

Jun-16 Mar-16 Barclays UK – RoTE of 18.4%

Risk weighted assets14 £319.6bn

£312.2bn Income was broadly in line, with good growth in customer balances

offsetting lower fee income

Notable items (£m) Jun-16 Jun-15 Cost reduction of 3% generated positive jaws

– Own credit 292 282

– Gain on disposal of Barclays’ share of

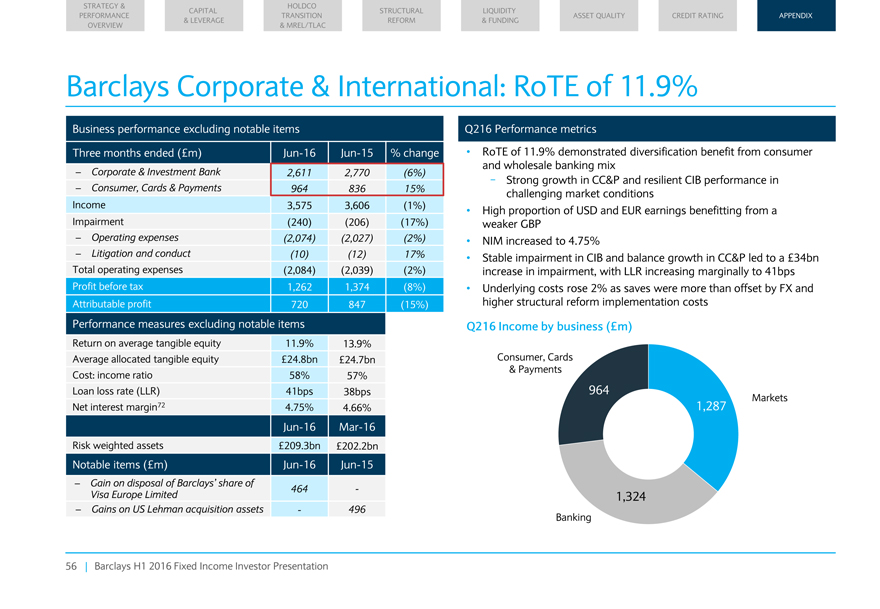

Barclays Corporate & International – RoTE of 11.9%

615 -

Visa

Europe Strong profit growth of 41% in CC&P and RoTE of 26.3%

– Gains on US Xxxxxx acquisition assets—496 Resilient CIB performance despite

challenging market conditions, and

– Provisions for UK customer redress(400)(800) RoTE of 9.5%

Total 507(22)

Barclays H1 2016 Fixed Income Investor Presentation

| 8 |

|

STRATEGY & HOLDCO

CAPITAL STRUCTURAL LIQUIDITY

PERFORMANCE TRANSITION ASSET QUALITY CREDIT RATING APPENDIX

& LEVERAGE REFORM & FUNDING

OVERVIEW & MREL/TLAC

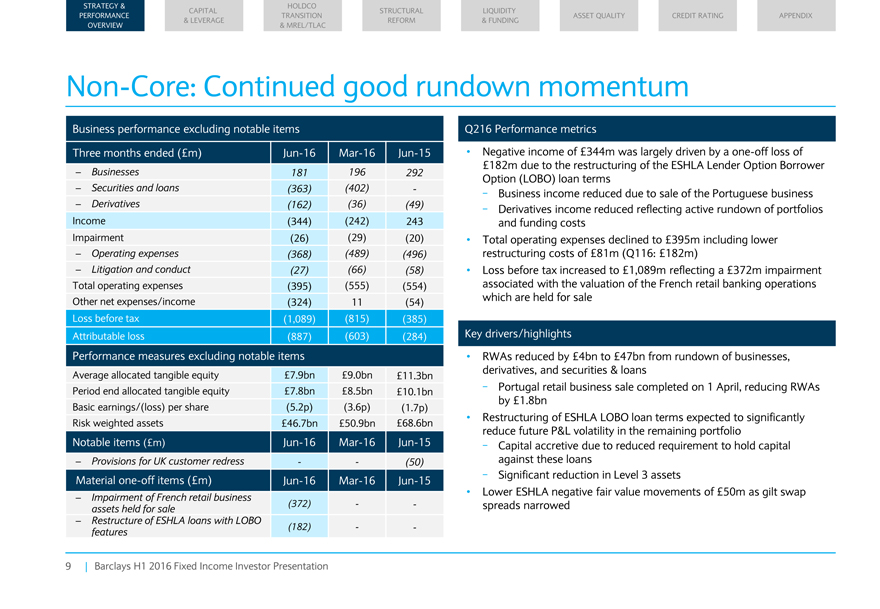

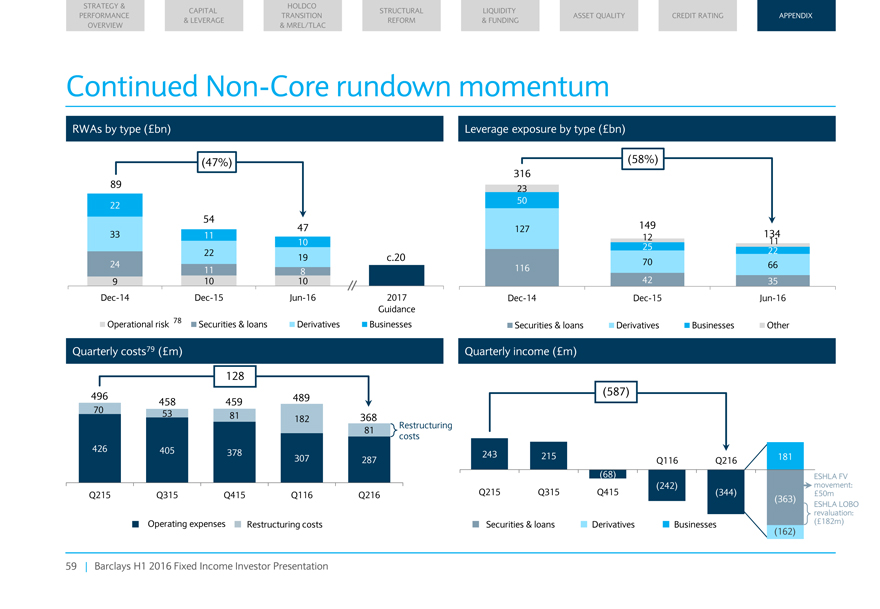

Non-Core: Continued good rundown momentum

Business performance excluding

notable items

Three months ended (£m) Jun-16 Mar-16 Jun-15

–

Businesses 181 196 292

– Securities and loans(363)(402) -

–

Derivatives(162)(36)(49)

Income(344)(242) 243

Impairment(26)(29)(20)

– Operating expenses(368)(489)(496)

– Litigation and

conduct(27)(66)(58)

Total operating expenses(395)(555)(554)

Other net

expenses/income(324) 11(54)

Loss before tax(1,089)(815)(385)

Attributable

loss(887)(603)(284)

Performance measures excluding notable items

Average

allocated tangible equity £7.9bn £9.0bn £11.3bn

Period end allocated tangible equity £7.8bn £8.5bn £10.1bn

Basic earnings/(loss) per share(5.2p)(3.6p)(1.7p)

Risk weighted assets £46.7bn

£50.9bn £68.6bn

Notable items (£m) Jun-16 Mar-16 Jun-15

– Provisions for UK customer redress —(50)

Material one-off items

(£m) Jun-16 Mar-16 Jun-15

– Impairment of French retail business

assets held for sale(372) —

– Restructure of ESHLA loans with LOBO

features(182) —

Q216 Performance metrics

Negative income of £344m was largely driven by a one-off loss of £182m due to the restructuring of the ESHLA Lender Option Borrower Option (LOBO) loan terms

- Business income reduced due to sale of the Portuguese business

- Derivatives income reduced

reflecting active rundown of portfolios and funding costs Total operating expenses declined to £395m including lower restructuring costs of £81m (Q116: £182m) Loss before tax increased to £1,089m reflecting a £372m

impairment associated with the valuation of the French retail banking operations which are held for sale

Key drivers/highlights

RWAs reduced by £4bn to £47bn from rundown of businesses, derivatives, and securities & loans

- Portugal retail business sale completed on 1 April, reducing RWAs by £1.8bn Restructuring of XXXXX XXXX loan terms expected to significantly reduce future P&L

volatility in the remaining portfolio

- Capital accretive due to reduced requirement to hold capital against these loans

- Significant reduction in Level 3 assets

Lower ESHLA negative fair value movements of

£50m as gilt swap spreads narrowed

Barclays H1 2016 Fixed Income Investor Presentation

9

|

STRATEGY & HOLDCO

CAPITAL STRUCTURAL LIQUIDITY

PERFORMANCE TRANSITION ASSET QUALITY CREDIT RATING APPENDIX

& LEVERAGE REFORM & FUNDING

OVERVIEW & MREL/TLAC

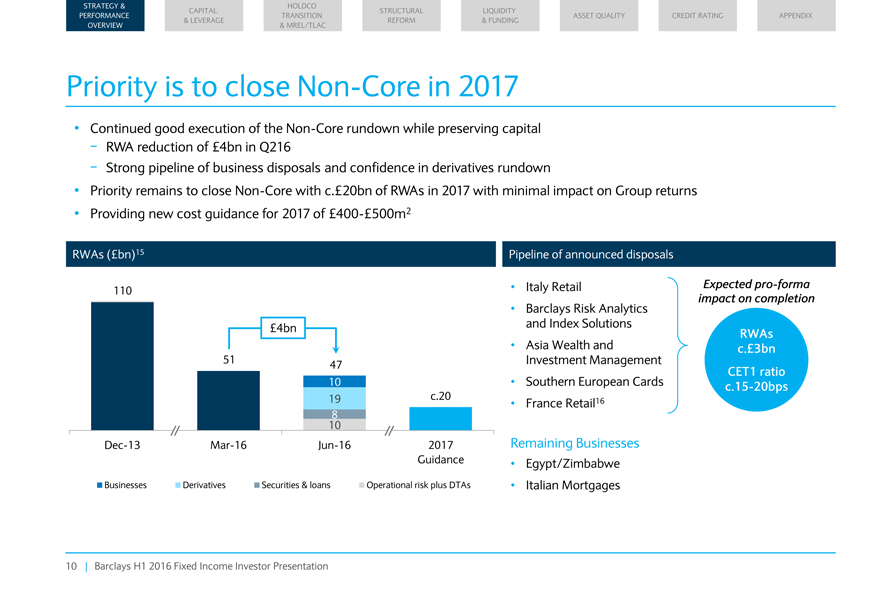

Priority is to close Non-Core in 2017

Continued good execution of the

Non-Core rundown while preserving capital

- RWA reduction of £4bn in Q216

- Strong pipeline of business disposals and confidence in derivatives rundown

Priority remains to close Non-Core with c.£20bn of RWAs in 2017 with minimal impact on Group returns Providing new cost guidance for 2017 of

£400-£500m2

RWAs (£bn)15 Pipeline of announced disposals

110

£4bn

51 47 10

19 c.20 8 10 Dec-13 Mar-16 Jun-16 2017 Guidance

Businesses Derivatives Securities & loans Operational risk plus DTAs

Italy Retail

Barclays Risk Analytics and Index Solutions Asia Wealth and Investment Management Southern European Cards France Retail16

Remaining Businesses

Egypt/Zimbabwe Italian Mortgages

Expected pro-forma impact on completion

RWAs c.£3bn CET1 ratio c.15-20bps

Barclays H1 2016 Fixed Income Investor Presentation

10

|

STRATEGY & HOLDCO

CAPITAL STRUCTURAL LIQUIDITY

PERFORMANCE TRANSITION ASSET QUALITY CREDIT RATING APPENDIX

& LEVERAGE REFORM & FUNDING

OVERVIEW & MREL/TLAC

Capital & Leverage

|

STRATEGY & HOLDCO

CAPITAL STRUCTURAL LIQUIDITY

PERFORMANCE TRANSITION ASSET QUALITY CREDIT RATING APPENDIX

& LEVERAGE REFORM & FUNDING

OVERVIEW & MREL/TLAC

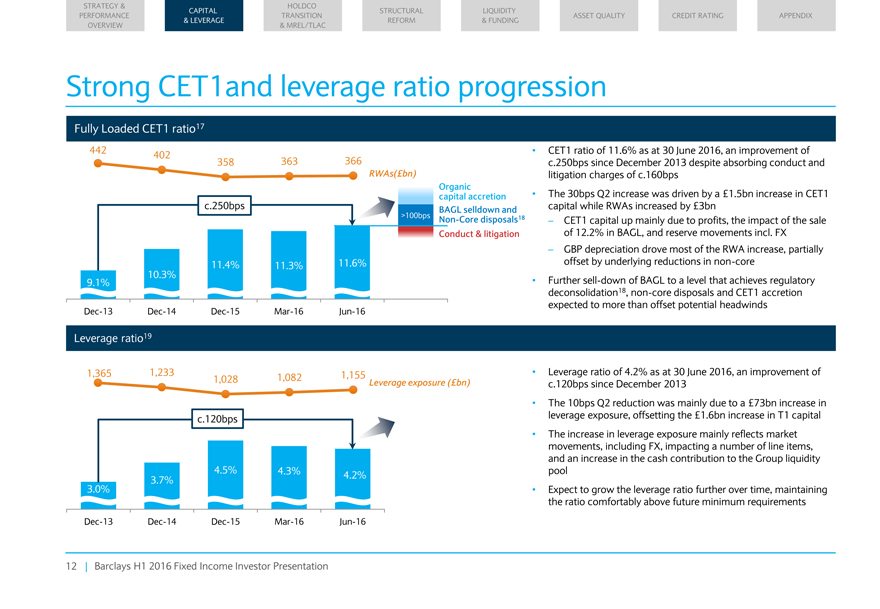

Strong CET1and leverage ratio progression

Fully Loaded CET1 ratio17

442 402 366 358 363

RWAs(£bn)

Organic capital accretion c.250bps BAGL selldown and >100bps Non-Core disposals18 Conduct & litigation

11.4% 11.3% 11.6% 11.3%

10.3%

9.1%

Dec-13 Dec-14 Dec-15 Mar-16 Jun-16

Leverage ratio19

1,365 1,233 1,082 1,155

1,028 Leverage exposure (£bn)

c.120bps

3.7% 4.5% 4.3% 4.2%

3.0%

Dec-13 Dec-14 Dec-15 Mar-16 Jun-16

CET1 ratio of 11.6% as at 30 June 2016, an improvement

of c.250bps since December 2013 despite absorbing conduct and litigation charges of c.160bps

The 30bps Q2 increase was driven by a £1.5bn increase in CET1

capital while RWAs increased by £3bn

– CET1 capital up mainly due to profits, the impact of the sale of 12.2% in BAGL, and reserve movements incl. FX

– GBP depreciation drove most of the RWA increase, partially offset by underlying reductions in non-core Further sell-down of BAGL to a level that achieves

regulatory deconsolidation18, non-core disposals and CET1 accretion expected to more than offset potential headwinds

Leverage ratio of 4.2% as at 30 June

2016, an improvement of c.120bps since December 2013 The 10bps Q2 reduction was mainly due to a £73bn increase in leverage exposure, offsetting the £1.6bn increase in T1 capital

The increase in leverage exposure mainly reflects market movements, including FX, impacting a number of line items, and an increase in the cash contribution to the Group liquidity

pool Expect to grow the leverage ratio further over time, maintaining the ratio comfortably above future minimum requirements

Barclays H1 2016 Fixed Income

Investor Presentation

12

|

STRATEGY & HOLDCO

CAPITAL STRUCTURAL LIQUIDITY

PERFORMANCE TRANSITION ASSET QUALITY CREDIT RATING APPENDIX

& LEVERAGE REFORM & FUNDING

OVERVIEW & MREL/TLAC

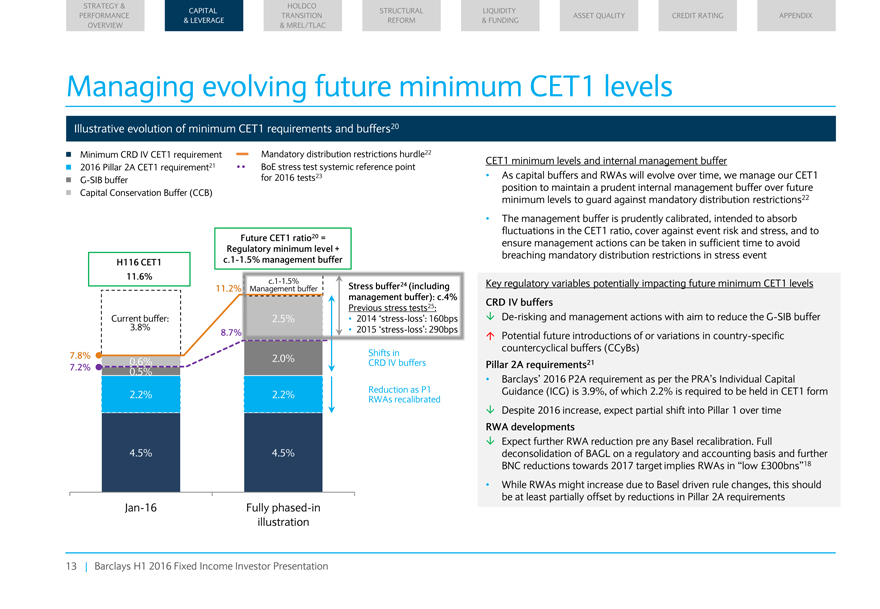

Managing evolving future minimum CET1 levels

Illustrative evolution of

minimum CET1 requirements and buffers20

Minimum CRD IV CET1 requirement Mandatory distribution restrictions hurdle22 2016 Pillar 2A CET1 requirement21 BoE stress

test systemic reference point G-SIB buffer for 2016 tests23 Capital Conservation Buffer (CCB)

Future CET1 ratio20 = Regulatory minimum level + H116 CET1 c.1-1.5%

management buffer 11.6%

11.2% Stress buffer24 (including management buffer): c.4%

Previous stress tests25:

Current buffer: • 2014 „stress-loss?: 160bps 3.8% •

2015 „stress-loss?: 290bps

8.7%

7.8% Shifts in 0.6% 2.0% CRD IV buffers

7.2% 0.5%

2.2% 2.2% Reduction RWAs recalibrated as P1

4.5% 4.5%

Jan-16 Fully phased-in illustration

CET1 minimum levels and internal management buffer

As capital buffers and RWAs will evolve

over time, we manage our CET1 position to maintain a prudent internal management buffer over future minimum levels to guard against mandatory distribution restrictions22

The management buffer is prudently calibrated, intended to absorb fluctuations in the CET1 ratio, cover against event risk and stress, and to ensure management actions can be taken

in sufficient time to avoid breaching mandatory distribution restrictions in stress event

Key regulatory variables potentially impacting future minimum CET1 levels

CRD IV buffers

De-risking and management actions with aim to reduce the G-SIB

buffer ? Potential future introductions of or variations in country-specific countercyclical buffers (CCyBs)

Pillar 2A requirements21

Barclays? 2016 P2A requirement as per the PRA?s Individual Capital

Guidance (ICG) is 3.9%, of

which 2.2% is required to be held in CET1 form ? Despite 2016 increase, expect partial shift into Pillar 1 over time

RWA developments

Expect further RWA reduction pre any Basel recalibration. Full deconsolidation of BAGL on a regulatory and accounting basis and further BNC reductions towards 2017 target implies

RWAs in “low £300bns“18

While RWAs might increase due to Basel driven rule changes, this should be at least partially offset by reductions in

Pillar 2A requirements

Barclays H1 2016 Fixed Income Investor Presentation

13

STRATEGY & HOLDCO

CAPITAL STRUCTURAL LIQUIDITY

PERFORMANCE TRANSITION ASSET QUALITY CREDIT

RATING APPENDIX

& LEVERAGE REFORM & FUNDING

OVERVIEW &

MREL/TLAC

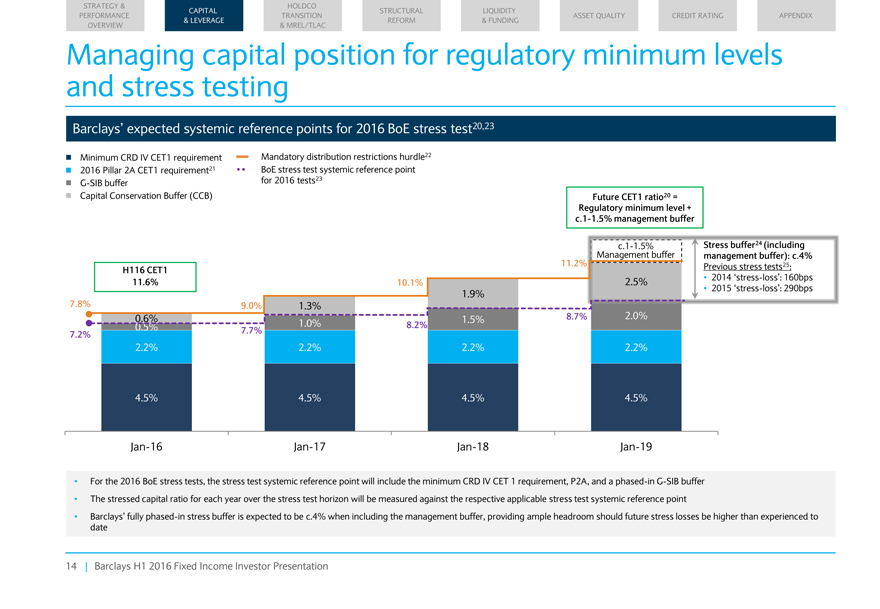

Managing capital position for regulatory minimum levels and stress testing

Barclays? expected systemic reference points for 2016 BoE stress test20,23

Minimum CRD IV CET1

requirement Mandatory distribution restrictions hurdle22

2016 Pillar 2A CET1 requirement21 BoE stress test systemic reference point

G-SIB buffer for 2016 tests23

Capital Conservation Buffer (CCB) Future CET1 ratio20 =

Regulatory minimum level +

c.1-1.5% management buffer

Stress buffer24 (including

management buffer): c.4%

H116 CET1 11.2% Previous stress tests25:

11.6% 10.1% • 2014 „stress-loss?: 160bps

1.9% • 2015 „stress-loss?: 290bps

7.8% 9.0% 1.3%

0.6% 1.5% 8.7% 2.0%

0.5% 7.7% 1.0% 8.2%

7.2%

2.2% 2.2% 2.2% 2.2%

4.5% 4.5% 4.5% 4.5%

Jan-16 Jan-17 Jan-18 Jan-19

For the 2016 BoE stress tests, the stress test systemic reference point will include the minimum CRD IV CET 1 requirement, P2A, and a phased-in G-SIB buffer

The stressed capital ratio for each year over the stress test horizon will be measured against the respective applicable stress test systemic reference point

Barclays? fully phased-in stress buffer is expected to be c.4% when including the management buffer, providing ample headroom should future stress losses be higher than experienced

to date

Barclays H1 2016 Fixed Income Investor Presentation

14

STRATEGY & HOLDCO

CAPITAL STRUCTURAL LIQUIDITY

PERFORMANCE TRANSITION ASSET QUALITY CREDIT

RATING APPENDIX

& LEVERAGE REFORM & FUNDING

OVERVIEW &

MREL/TLAC

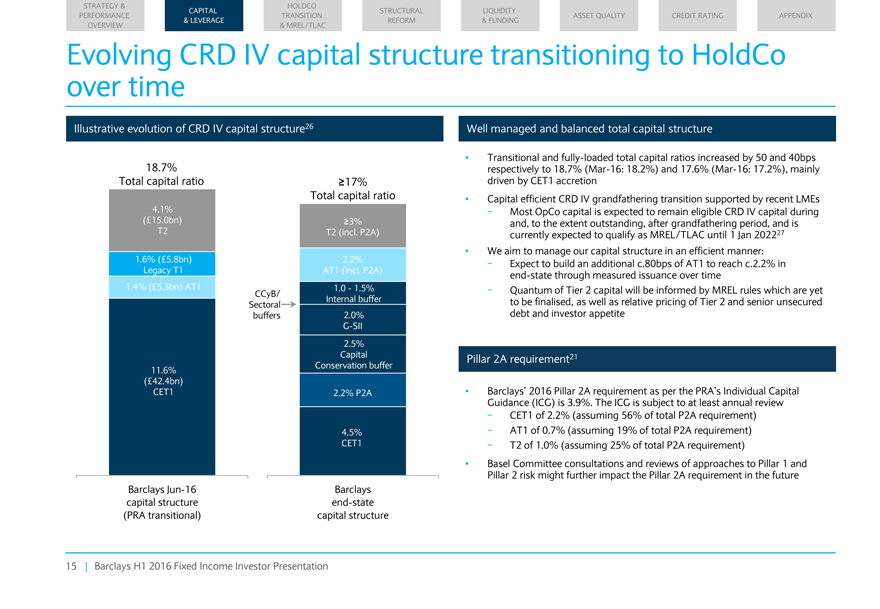

Evolving CRD IV capital structure transitioning to HoldCo

over time

Illustrative evolution of CRD IV capital structure26 Well managed and balanced total capital structure

Transitional and fully-loaded total capital ratios increased by 50 and 40bps

18.7%

respectively to 18.7% (Mar-16: 18.2%) and 17.6% (Mar-16: 17.2%), mainly

Total capital ratio ?17% driven by CET1 accretion

Total capital ratio Capital efficient CRD IV grandfathering transition supported by recent LMEs

4.1%—Most OpCo capital is expected to remain eligible CRD IV capital during

(£15.0bn) ?3% and, to the extent outstanding, after grandfathering period, and is

T2 T2

(incl. P2A) currently expected to qualify as MREL/TLAC until 1 Jan 202227

We aim to manage our capital structure in an efficient manner:

1.6% (£5.8bn) 2.2%—Expect to build an additional c.80bps of AT1 to reach c.2.2% in

Legacy T1 AT1 (incl. P2A) end-state through measured issuance over time

1.4%

(£5.3bn) AT1 CCyB/ 1.0—1.5%—Quantum of Tier 2 capital will be informed by MREL rules which are yet

Sectoral Internal buffer to be finalised,

as well as relative pricing of Tier 2 and senior unsecured

buffers 2.0% debt and investor appetite

G-SII

2.5%

Capital Pillar 2A requirement21

11.6% Conservation buffer

(£42.4bn)

CET1 2.2% P2A Barclays? 2016 Pillar 2A requirement as per the PRA?s Individual

Capital

Guidance (ICG) is 3.9%. The ICG is subject to at least annual review

—CET1 of 2.2% (assuming 56% of total P2A requirement)

4.5%—AT1 of

0.7% (assuming 19% of total P2A requirement)

CET1—T2 of 1.0% (assuming 25% of total P2A requirement)

Basel Committee consultations and reviews of approaches to Pillar 1 and

Pillar 2 risk might

further impact the Pillar 2A requirement in the future

Barclays Jun-16 Barclays

capital structure end-state

(PRA transitional) capital structure

Barclays H1 2016 Fixed Income Investor Presentation

15

|

STRATEGY & HOLDCO

CAPITAL STRUCTURAL LIQUIDITY

PERFORMANCE TRANSITION ASSET QUALITY CREDIT RATING APPENDIX

& LEVERAGE REFORM & FUNDING

OVERVIEW & MREL/TLAC

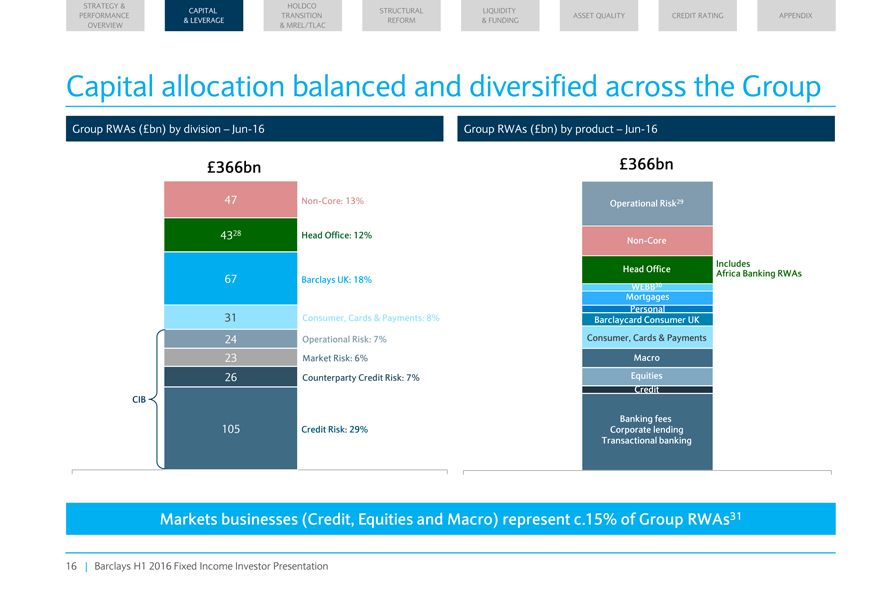

Capital allocation balanced and diversified across the Group

Group RWAs

(£bn) by division – Jun-16 Group RWAs (£bn) by product – Jun-16

£366bn £366bn

47 Non-Core: 13% Operational Risk29

4328 Head Office: 12%

Non-Core

Includes

Head Office Africa Banking RWAs

67 Barclays UK: 18%

WEBB30 Mortgages Consumer, Cards & Payments: 8% Personal

31 Barclaycard Consumer UK

24 Operational Risk: 7% Consumer, Cards & Payments

23 Market Risk:

6% Macro

26 Counterparty Credit Risk: 7% Equities Credit CIB

Banking fees 105

Credit Risk: 29% Corporate lending Transactional banking

Markets businesses (Credit, Equities and Macro) represent c.15% of Group RWAs31

Barclays H1 2016 Fixed Income Investor Presentation

16

|

STRATEGY & HOLDCO

CAPITAL STRUCTURAL LIQUIDITY

PERFORMANCE TRANSITION ASSET QUALITY CREDIT RATING APPENDIX

& LEVERAGE REFORM & FUNDING

OVERVIEW & MREL/TLAC

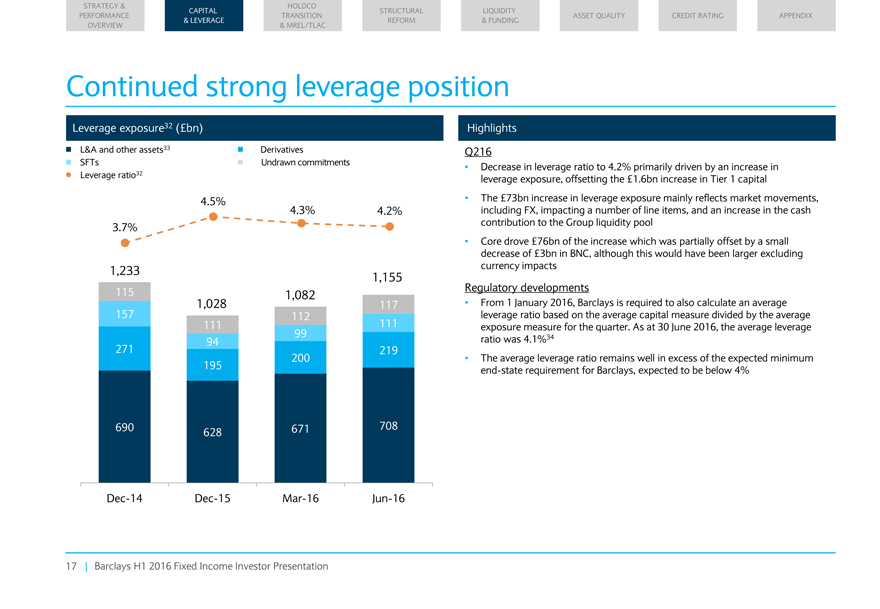

Continued strong leverage position

Leverage exposure32 (£bn)

L&A and other assets33 Derivatives

SFTs Undrawn commitments Leverage

ratio32

4.5%

4.3% 4.2%

3.7%

1,233

1,155 115 1,028 1,082

117 157 112 111 111 99 94 271 219 200 195

690 671 708 628

Dec-14 Dec-15 Mar-16 Jun-16

Highlights Q216

Decrease in leverage ratio to 4.2% primarily driven by an increase in leverage

exposure, offsetting the £1.6bn increase in Tier 1 capital

The £73bn increase in leverage exposure mainly reflects market movements, including FX,

impacting a number of line items, and an increase in the cash contribution to the Group liquidity pool

Core drove £76bn of the increase which was partially

offset by a small decrease of £3bn in BNC, although this would have been larger excluding currency impacts

Regulatory developments

From 1 January 2016, Barclays is required to also calculate an average leverage ratio based on the average capital measure divided by the average exposure measure for the

quarter. As at 30 June 2016, the average leverage ratio was 4.1%34

The average leverage ratio remains well in excess of the expected minimum end-state

requirement for Barclays, expected to be below 4%

Barclays H1 2016 Fixed Income Investor Presentation

17

|

STRATEGY & HOLDCO

CAPITAL STRUCTURAL LIQUIDITY

PERFORMANCE TRANSITION ASSET QUALITY CREDIT RATING APPENDIX

& LEVERAGE REFORM & FUNDING

OVERVIEW & MREL/TLAC

Holding company transition and MREL/TLAC

|

STRATEGY & HOLDCO

CAPITAL STRUCTURAL LIQUIDITY

PERFORMANCE TRANSITION ASSET QUALITY CREDIT RATING APPENDIX

& LEVERAGE REFORM & FUNDING

OVERVIEW & MREL/TLAC

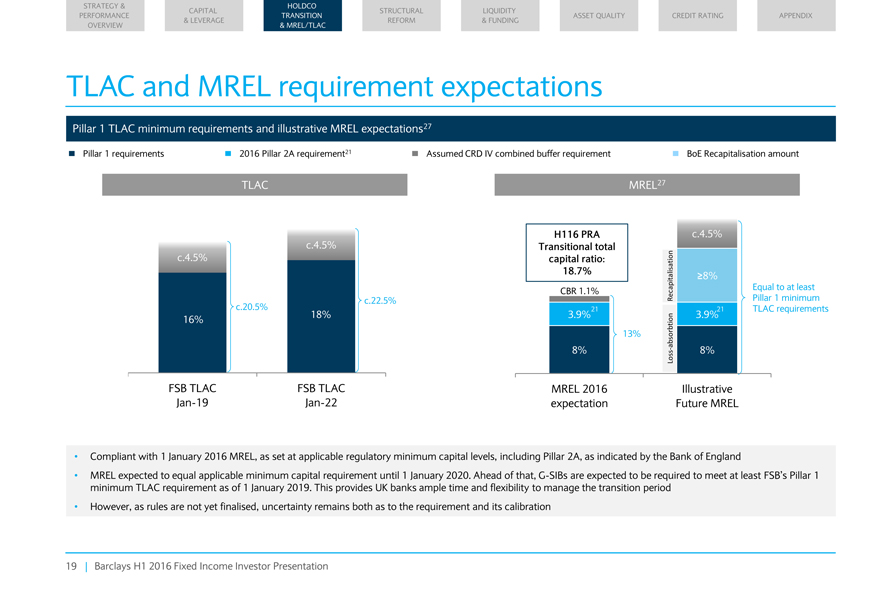

TLAC and MREL requirement expectations

Pillar 1 TLAC minimum requirements and

illustrative MREL expectations27

Pillar 1 requirements 2016 Pillar 2A requirement21 Assumed CRD IV combined buffer requirement BoE Recapitalisation amount

TLAC MREL27

H116 PRA c.4.5% c.4.5% Transitional total c.4.5% capital ratio:

18.7% ?8%

CBR 1.1% Equal to at least c.20.5% c.22.5% Recapitalisation Pillar 1 minimum 18% 3.9%21 3.9%21 TLAC requirements

16%

13% absorbtion

8% Loss—8%

FSB TLAC FSB TLAC MREL 2016 Illustrative Jan-19 Jan-22 expectation Future MREL

Compliant with 1 January 2016 MREL, as set at applicable regulatory minimum capital levels, including Pillar 2A, as indicated by the Bank of England

MREL expected to equal applicable minimum capital requirement until 1 January 2020. Ahead of that, G-SIBs are expected to be required to meet at least FSB?s

Pillar 1 minimum TLAC requirement as of 1 January 2019. This provides UK banks ample time and flexibility to manage the transition period

However, as rules

are not yet finalised, uncertainty remains both as to the requirement and its calibration

Barclays H1 2016 Fixed Income Investor Presentation

19

|

STRATEGY & HOLDCO

CAPITAL STRUCTURAL LIQUIDITY

PERFORMANCE TRANSITION ASSET QUALITY CREDIT RATING APPENDIX

& LEVERAGE REFORM & FUNDING

OVERVIEW & MREL/TLAC

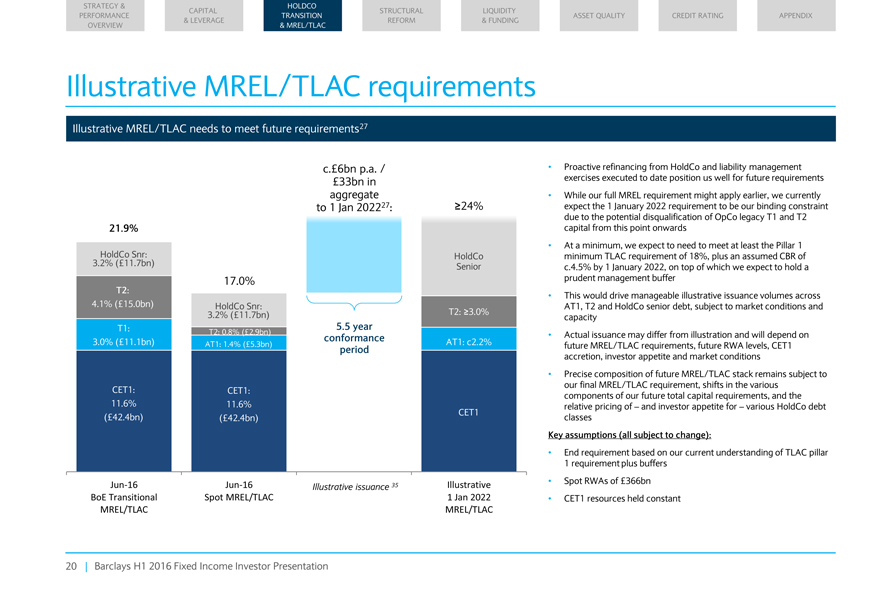

Illustrative MREL/TLAC requirements

Illustrative MREL/TLAC needs to meet

future requirements27

c.£6bn p.a. / Proactive refinancing from HoldCo and liability management £33bn in exercises executed to date position us well for

future requirements aggregate While our full MREL requirement might apply earlier, we currently to 1 Jan 202227: ?24% expect the 1 January 2022 requirement to be our binding constraint due to the potential disqualification of OpCo legacy T1 and

T2 21.9% capital from this point onwards HoldCo Snr: At a minimum, we expect to need to meet at least the Pillar 1 HoldCo minimum TLAC requirement of 18%, plus an assumed CBR of 3.2% (£11.7bn) Senior c.4.5% by 1 January 2022, on top

of which we expect to hold a 17.0% prudent management buffer

T2:

This would

drive manageable illustrative issuance volumes across 4.1% (£15.0bn) HoldCo Snr: AT1, T2 and HoldCo senior debt, subject to market conditions and 3.2% (£11.7bn) T2: ?3.0% capacity

T1: 5.5 year

T2: 0.8% (£2.9bn) Actual issuance may differ from illustration and

will depend on 3.0% (£11.1bn) conformance AT1: c2.2% AT1: 1.4% (£5.3bn) period future XXXX/XXXX xxxxxxxxxxxx, xxxxxx XXX xxxxxx, XXX0 accretion, investor appetite and market conditions

Precise composition of future MREL/TLAC stack remains subject to our final MREL/TLAC requirement, shifts in the various CET1: CET1: components of our future total capital

requirements, and the 11.6% 11.6% CET1 relative pricing of – and investor appetite for – various HoldCo debt

(£42.4bn) (£42.4bn) classes

Key assumptions (all subject to change):

End requirement based on our current

understanding of TLAC pillar 1 requirement plus buffers

Spot RWAs of £366bn

Jun-16 Jun-16 Illustrative issuance 35 Illustrative

BoE Transitional Spot MREL/TLAC 1 Jan 2022

• CET1 resources held constant MREL/TLAC MREL/TLAC

Barclays H1 2016 Fixed Income Investor Presentation

20

|

STRATEGY & HOLDCO

CAPITAL STRUCTURAL LIQUIDITY

PERFORMANCE TRANSITION ASSET QUALITY CREDIT RATING APPENDIX

& LEVERAGE REFORM & FUNDING

OVERVIEW & MREL/TLAC

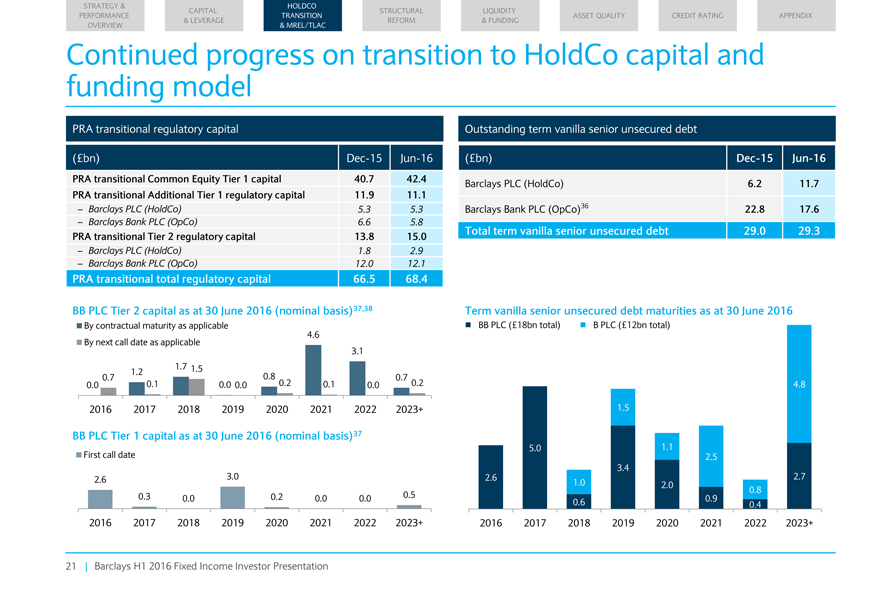

Continued progress on transition to HoldCo capital and funding model

PRA

transitional regulatory capital Outstanding term vanilla senior unsecured debt

(£bn) Dec-15 Jun-16 (£bn) Dec-15 Jun-16

PRA transitional Common Equity Tier 1 capital 40.7 42.4 Barclays PLC (HoldCo) 6.2 11.7 PRA transitional Additional Tier 1 regulatory capital 11.9 11.1

– Barclays PLC (HoldCo) 5.3 5.3 Barclays Bank PLC (OpCo)36 22.8 17.6

– Barclays Bank

PLC (OpCo) 6.6 5.8

Total term vanilla senior unsecured debt 29.0 29.3

PRA

transitional Tier 2 regulatory capital 13.8 15.0

– Barclays PLC (HoldCo) 1.8 2.9

– Barclays Bank PLC (OpCo) 12.0 12.1

PRA transitional total regulatory capital 66.5 68.4

BB PLC Tier 2 capital as at 30 June 2016 (nominal basis)37,38 Term vanilla senior unsecured debt maturities as at 30 June 2016

By contractual maturity as applicable 4.6 BB PLC (£18bn total) B PLC (£12bn total) By next call date as applicable 3.1 1.7 1.5 1.2 0.8 0.7 0.7

0.0 0.1 0.0 0.0 0.2 0.1 0.0 0.2 4.8

2016 2017 2018 2019 2020 2021 2022 2023+ 1.5

BB PLC Tier 1 capital as at 30 June 2016 (nominal basis)37

5.0 1.1

First call date 2.5 3.4

2.6 3.0 2.6 2.7 1.0 2.0 0.8 0.3 0.0 0.2 0.0 0.0 0.5 0.9 0.6 0.4

2016 2017 2018 2019 2020 2021 2022 2023+ 2016 2017 2018 2019 2020 2021 2022 2023+

Barclays H1 2016 Fixed Income Investor Presentation

21

STRATEGY & HOLDCO

CAPITAL STRUCTURAL LIQUIDITY

PERFORMANCE TRANSITION ASSET QUALITY CREDIT

RATING APPENDIX

& LEVERAGE REFORM & FUNDING

OVERVIEW &

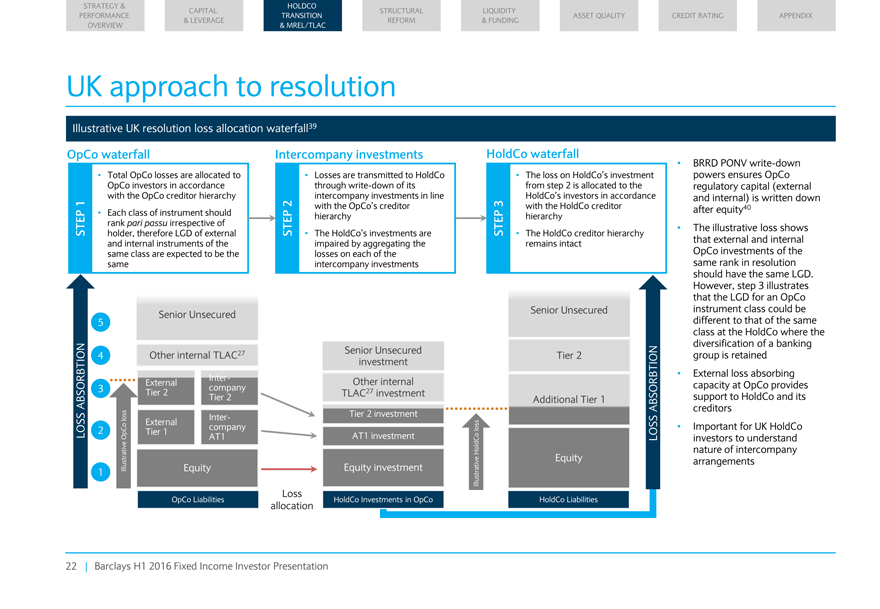

MREL/TLAC UK approach to resolution

Illustrative UK resolution loss allocation waterfall39 OpCo waterfall Intercompany investments HoldCo waterfall BRRD PONV

write-down Total OpCo losses are allocated to Losses are transmitted to HoldCo • The loss on HoldCo?s investment powers ensures OpCo OpCo investors in accordance through write-down of its from step 2 is allocated to the regulatory capital

(external with the OpCo creditor hierarchy intercompany investments in line HoldCo?s investors in accordance and internal) is written down

| 1 | 2 with the OpCo?s creditor 3 with the HoldCo creditor after equity40 |

Each class of instrument should hierarchy hierarchy rank pari passu irrespective of The illustrative loss shows

STEP holder, therefore LGD of external STEP The HoldCo?s investments are STEP The HoldCo creditor hierarchy and internal instruments of the impaired by aggregating the remains

intact that external and internal same class are expected to be the losses on each of the OpCo investments of the same intercompany investments same rank in resolution should have the same LGD.

However, step 3 illustrates that the LGD for an OpCo Senior Unsecured instrument class could be Senior Unsecured 5 different to that of the same class at the HoldCo where the

Senior Unsecured diversification of a banking

4 Other internal TLAC27 Tier 2

group is retained investment Inter- External loss absorbing External Other internal capacity at OpCo provides 3 company 27 Tier 2 TLAC investment support to HoldCo and its ABSORBTION Tier 2 Additional Tier 1

ABSORBTION creditors Tier 2 investment loss Inter-

External company loss • Important for

UK HoldCo LOSS 2 OpCo Tier 1 AT1 AT1 investment LOSS investors to understand HoldCo nature of intercompany Equity arrangements Illustrative Equity Equity investment 1 Illustrative

Loss OpCo Liabilities HoldCo Investments in OpCo HoldCo Liabilities

allocation Barclays H1

2016 Fixed Income Investor Presentation

22

|

STRATEGY & HOLDCO

CAPITAL STRUCTURAL LIQUIDITY

PERFORMANCE TRANSITION ASSET QUALITY CREDIT RATING APPENDIX

& LEVERAGE REFORM & FUNDING

OVERVIEW & MREL/TLAC

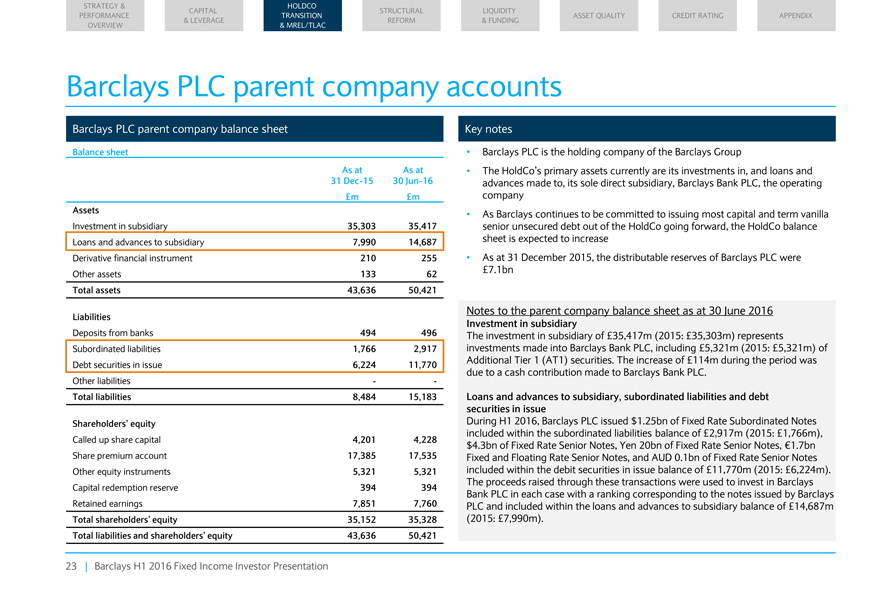

Barclays PLC parent company accounts

Barclays PLC parent company balance

sheet Key notes

Balance sheet Barclays PLC is the holding company of the Barclays Group

As at As at The HoldCo?s primary assets currently are its investments in, and loans and

| 31 | Dec-15 30 Jun-16 advances made to, its sole direct subsidiary, Barclays Bank PLC, the operating |

£m £m company

Assets As Barclays continues to be committed to issuing most capital and term vanilla

Investment in subsidiary 35,303 35,417 senior unsecured debt out of the HoldCo going forward, the HoldCo balance

Loans and advances to subsidiary 7,990 14,687 sheet is expected to increase

Derivative

financial instrument 210 255 As at 31 December 2015, the distributable reserves of Barclays PLC were

Other assets 133 62 £7.1bn

Total assets 43,636 50,421

Liabilities Notes to the parent company balance sheet as at

30 June 2016

Investment in subsidiary

Deposits from banks 494 496 The

investment in subsidiary of £35,417m (2015: £35,303m) represents

Subordinated liabilities 1,766 2,917 investments made into Barclays Bank PLC,

including £5,321m (2015: £5,321m) of

Debt securities in issue 6,224 11,770 Additional Tier 1 (AT1) securities. The increase of £114m during the

period was

due to a cash contribution made to Barclays Bank PLC.

Other

liabilities —

Total liabilities 8,484 15,183 Loans and advances to subsidiary, subordinated liabilities and debt

securities in issue

Shareholders’ equity During H1 2016, Barclays PLC issued $1.25bn of

Fixed Rate Subordinated Notes

included within the subordinated liabilities balance of £2,917m (2015: £1,766m),

Called up share capital 4,201 4,228 $4.3bn of Fixed Rate Senior Notes, Yen 20bn of Fixed Rate Senior Notes, €1.7bn

Share premium account 17,385 17,535 Fixed and Floating Rate Senior Notes, and AUD 0.1bn of Fixed Rate Senior Notes

Other equity instruments 5,321 5,321 included within the debit securities in issue balance of £11,770m (2015: £6,224m).

Capital redemption reserve 394 394 The proceeds raised through these transactions were used to invest in Barclays

Bank PLC in each case with a ranking corresponding to the notes issued by Barclays

Retained

earnings 7,851 7,760 PLC and included within the loans and advances to subsidiary balance of £14,687m

Total shareholders’ equity 35,152 35,328(2015:

£7,990m).

Total liabilities and shareholders’ equity 43,636 50,421

Barclays H1 2016 Fixed Income Investor Presentation

23

|

STRATEGY & HOLDCO

CAPITAL STRUCTURAL LIQUIDITY

PERFORMANCE TRANSITION ASSET QUALITY CREDIT RATING APPENDIX

& LEVERAGE REFORM & FUNDING

OVERVIEW & MREL/TLAC

Structural Reform

|

STRATEGY & HOLDCO

CAPITAL STRUCTURAL LIQUIDITY

PERFORMANCE TRANSITION ASSET QUALITY CREDIT RATING APPENDIX

& LEVERAGE REFORM & FUNDING

OVERVIEW & MREL/TLAC

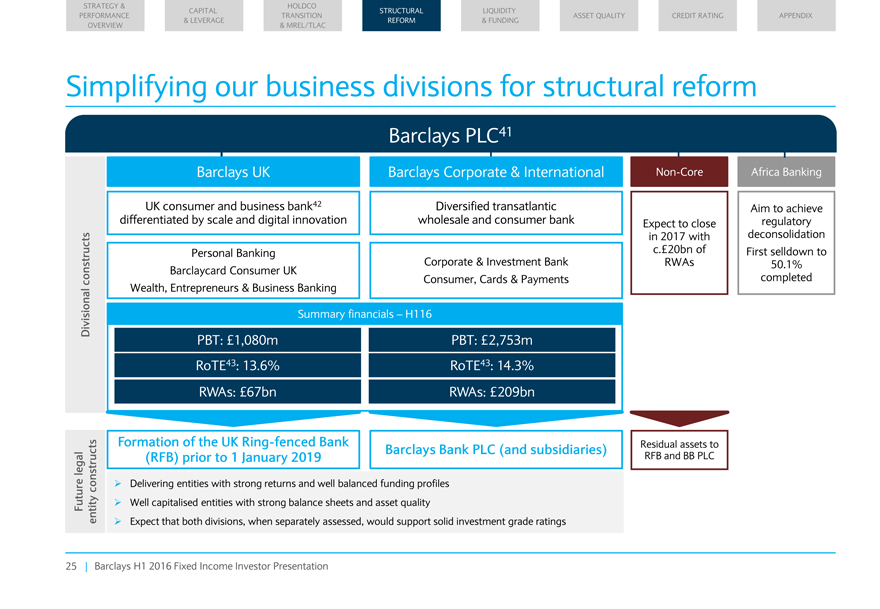

Simplifying our business divisions for structural reform

Barclays a PLC L 41

Barclays UK Barclays Corporate & International Non-Core Africa Banking

UK consumer and business bank42 Diversified transatlantic Aim to achieve differentiated by scale and digital innovation wholesale and consumer bank Expect to close

regulatory in 2017 with deconsolidation Personal Banking c.£20bn of First selldown to Corporate & Investment Bank RWAs 50.1% Barclaycard Consumer UK constructs Consumer, Cards & Payments completed Wealth,

Entrepreneurs & Business Banking Divisional Summary financials – H116

PBT: £1,080m PBT: £2,753m RoTE43: 13.6% RoTE43: 14.3% RWAs:

£67bn RWAs: £209bn

Formation of the UK Ring-fenced Bank Residual assets to legal (RFB) prior to 1 January 2019 Barclays Bank PLC (and

subsidiaries) RFB and BB PLC

returns and well constructs? Delivering entities with strong balanced funding profiles entities with strong and asset Future entity?

Well capitalised balance sheets quality

? Expect that both divisions, when separately assessed, would support solid investment grade ratings

Barclays H1 2016 Fixed Income Investor Presentation

25

|

STRATEGY & HOLDCO

CAPITAL STRUCTURAL LIQUIDITY

PERFORMANCE TRANSITION ASSET QUALITY CREDIT RATING APPENDIX

& LEVERAGE REFORM & FUNDING

OVERVIEW & MREL/TLAC

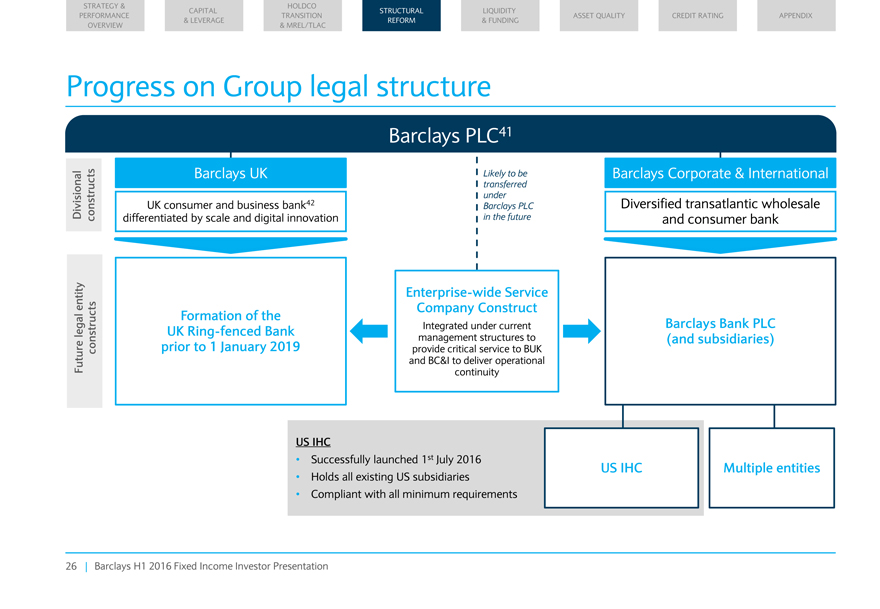

Progress on Group legal structure

Barclays PLC41

Barclays UK Likely to be Barclays Corporate & International

transferred 42 under

Divisional UK consumer and business bank Barclays PLC Diversified transatlantic wholesale

constructs differentiated by scale and digital innovation in the future and consumer bank

Enterprise-wide Service entity Company Construct Formation of the

Integrated

under current Barclays Bank PLC

legal UK Ring-fenced Bank prior to 1 January 2019 management structures to (and subsidiaries)

constructs provide critical service to BUK Future and BC&I to deliver operational continuity

US IHC

Successfully launched 1st July 2016

US IHC Multiple entities

Holds all existing US subsidiaries

Compliant with all minimum requirements

Barclays H1 2016 Fixed Income Investor Presentation

26

|

STRATEGY & HOLDCO

CAPITAL STRUCTURAL LIQUIDITY

PERFORMANCE TRANSITION ASSET QUALITY CREDIT RATING APPENDIX

& LEVERAGE REFORM & FUNDING

OVERVIEW & MREL/TLAC

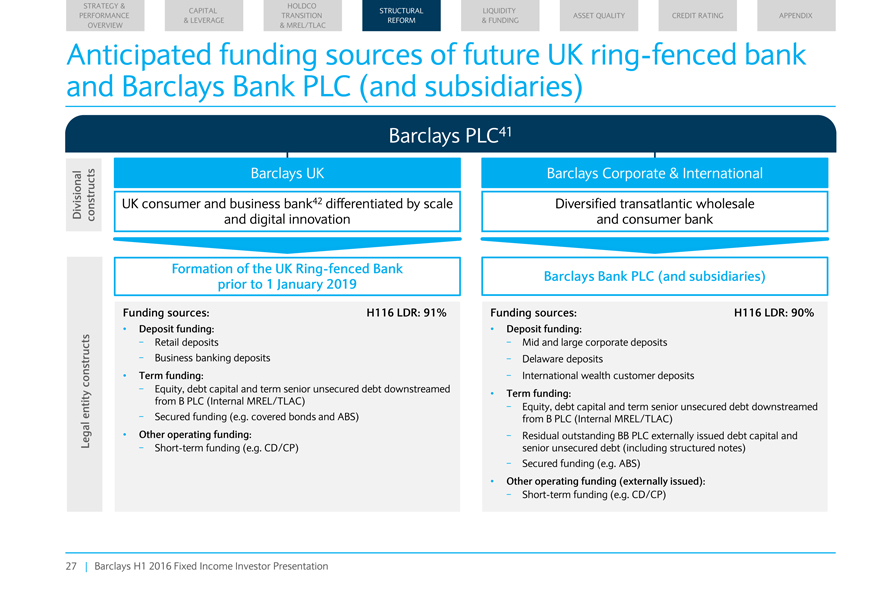

Anticipated funding sources of future UK ring-fenced bank

and Barclays Bank

PLC (and subsidiaries)

Barclays PLC41

Barclays UK Barclays

Corporate & International

Divisional constructs UK consumer and business bank42 differentiated by scale Diversified transatlantic wholesale

and digital innovation and consumer bank

Formation of the UK Ring-fenced Bank Barclays Bank

PLC (and subsidiaries)

prior to 1 January 2019

Funding sources: H116

LDR: 91% Funding sources: H116 LDR: 90%

Deposit funding: Deposit funding:

—Retail deposits—Mid and large corporate deposits

—Business

banking deposits—Delaware deposits

constructs Term funding:—International wealth customer deposits

—Equity, debt capital and term senior unsecured debt downstreamed Term funding:

entity

from B PLC (Internal MREL/TLAC)—Equity, debt capital and term senior unsecured debt downstreamed

—Secured funding (e.g. covered bonds and ABS) from B PLC

(Internal MREL/TLAC)

Legal Other operating funding:—Residual outstanding BB PLC externally issued debt capital and

—Short-term funding (e.g. CD/CP) senior unsecured debt (including structured notes)

—Secured funding (e.g. ABS)

Other operating funding (externally issued):

—Short-term funding (e.g. CD/CP)

Barclays H1 2016 Fixed Income Investor

Presentation

27

|

STRATEGY & HOLDCO

CAPITAL STRUCTURAL LIQUIDITY

PERFORMANCE TRANSITION ASSET QUALITY CREDIT RATING APPENDIX

& LEVERAGE REFORM & FUNDING

OVERVIEW & MREL/TLAC

Liquidity & Funding

STRATEGY & HOLDCO

CAPITAL STRUCTURAL LIQUIDITY

PERFORMANCE TRANSITION ASSET QUALITY CREDIT

RATING APPENDIX

& LEVERAGE REFORM & FUNDING

OVERVIEW &

MREL/TLAC

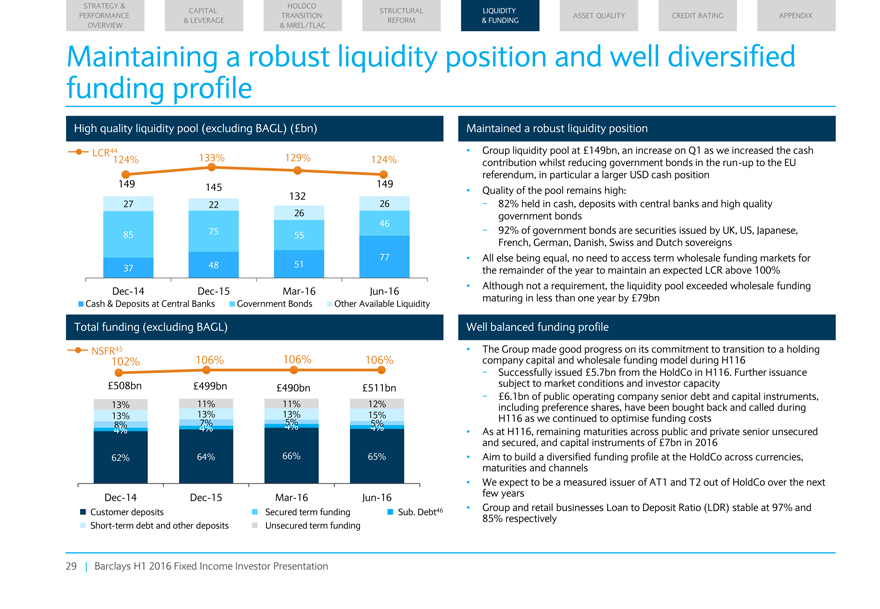

Maintaining a robust liquidity position and well diversified

funding profile

High quality liquidity pool (excluding BAGL) (£bn)

Maintained a robust liquidity position

LCR44 Group liquidity pool at £149bn, an increase on Q1 as we increased the cash

124% 133% 129% 124% contribution whilst reducing government bonds in the run-up to the EU

referendum, in particular a larger USD cash position

149 145 149 Quality of

the pool remains high:

132

| 27 | 22 26—82% held in cash, deposits with central banks and high quality |

| 26 | government bonds |

| 46 |

| 85 | 75 55—92% of government bonds are securities issued by UK, US, Japanese, |

French, German, Danish, Swiss and Dutch sovereigns

| 77 | All else being equal, no need to access term wholesale funding markets for |

| 37 | 48 51 the remainder of the year to maintain an expected LCR above 100% |

Dec-14 Dec-15 Mar-16 Jun-16 Although not a requirement, the liquidity pool exceeded wholesale funding

Cash & Deposits at Central Banks Government Bonds Other Available Liquidity maturing in less than one year by £79bn

Total funding (excluding BAGL) Well balanced funding profile

NSFR45 The Group made good

progress on its commitment to transition to a holding

102% 106% 106% 106% company capital and wholesale funding model during H116

—Successfully issued £5.7bn from the HoldCo in H116. Further issuance

£508bn

£499bn £490bn £511bn subject to market conditions and investor capacity

—£6.1bn of public operating company senior debt and capital

instruments,

13% 11% 11% 12% including preference shares, have been bought back and called during

13% 13% 13% 15% H116 as we continued to optimise funding costs

4% 8% 4% 7% 4% 5% 4% 5% As at

H116, remaining maturities across public and private senior unsecured

and secured, and capital instruments of £7bn in 2016

62% 64% 66% 65% Aim to build a diversified funding profile at the HoldCo across currencies,

maturities and channels

We expect to be a measured issuer of AT1 and T2 out

of HoldCo over the next

Dec-14 Dec-15 Mar-16 Jun-16 few years

Customer

deposits Secured term funding Sub. Debt46 Group and retail businesses Loan to Deposit Ratio (LDR) stable at 97% and

Short-term debt and other deposits Unsecured

term funding 85% respectively

Barclays H1 2016 Fixed Income Investor Presentation

29

|

STRATEGY & HOLDCO

CAPITAL STRUCTURAL LIQUIDITY

PERFORMANCE TRANSITION ASSET QUALITY CREDIT RATING APPENDIX

& LEVERAGE REFORM & FUNDING

OVERVIEW & MREL/TLAC

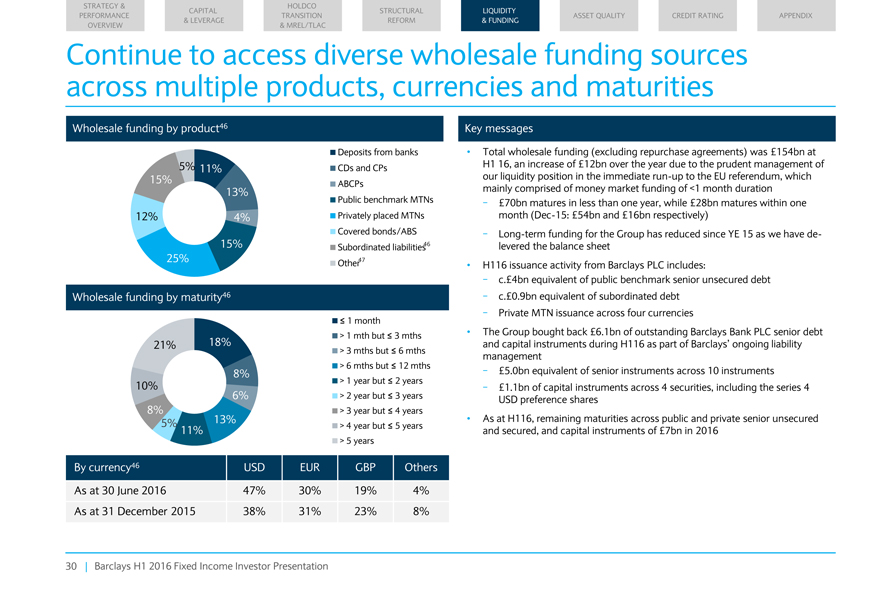

Continue to access diverse wholesale funding sources across multiple products, currencies and maturities

Wholesale funding by product46

Deposits from banks

5% 11% CDs and CPs 15% ABCPs

13%

Public benchmark MTNs 12% 4% Privately placed MTNs Covered bonds/ABS

15% Subordinated

liabilities 46 25% Other47

Wholesale funding by maturity46

? 1 month

> 1 mth but ? 3 mths

21% 18%

> 3 mths but ? 6 mths

> 6 mths but ? 12 mths

8%

10% > 1 year but ? 2 years

6% > 2 year but ? 3 years

8% > 3 year but ? 4 years

5% 13%

11% > 4 year but ? 5 years

> 5 years

By currency46 USD EUR GBP Others As at 30 June 2016 47% 30% 19% 4% As at

31 December 2015 38% 31% 23% 8%

Key messages

Total wholesale funding

(excluding repurchase agreements) was £154bn at H1 16, an increase of £12bn over the year due to the prudent management of our liquidity position in the immediate run-up to the EU referendum, which mainly comprised of money market

funding of <1 month duration

- £70bn matures in less than one year, while £28bn matures within one month (Dec-15: £54bn and £16bn

respectively)

- Long-term funding for the Group has reduced since YE 15 as we have de-levered the balance sheet H116 issuance activity from Barclays PLC

includes:—c.£4bn equivalent of public benchmark senior unsecured debt—c.£0.9bn equivalent of subordinated debt

- Private MTN issuance across

four currencies

The Group bought back £6.1bn of outstanding Barclays Bank PLC senior debt and capital instruments during H116 as part of Barclays? ongoing

liability management

- £5.0bn equivalent of senior instruments across 10 instruments

- £1.1bn of capital instruments across 4 securities, including the series 4 USD preference shares As at H116, remaining maturities across public and private senior unsecured

and secured, and capital instruments of £7bn in 2016

Barclays H1 2016 Fixed Income Investor Presentation

30

|

STRATEGY & HOLDCO

CAPITAL STRUCTURAL LIQUIDITY

PERFORMANCE TRANSITION ASSET QUALITY CREDIT RATING APPENDIX

& LEVERAGE REFORM & FUNDING

OVERVIEW & MREL/TLAC

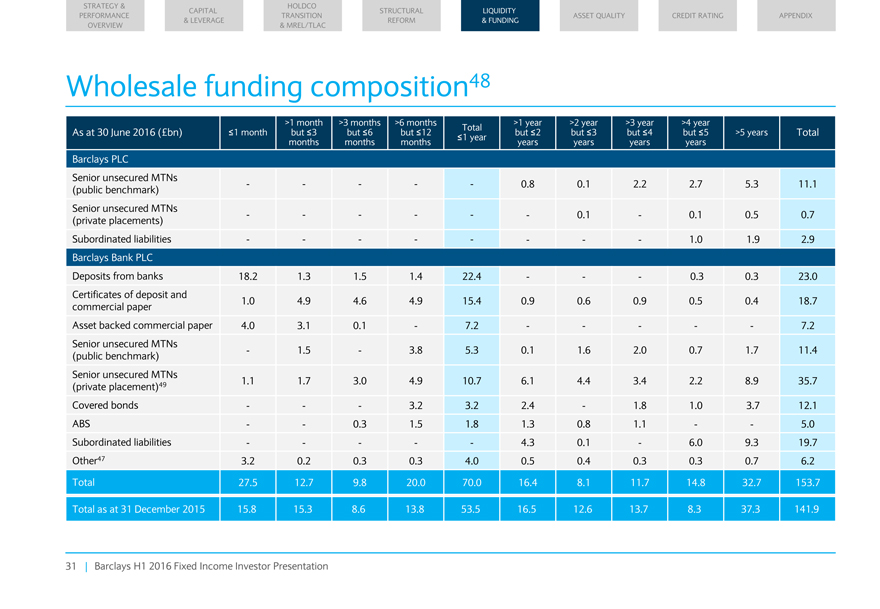

Wholesale funding composition48

>1 month >3 months >6 months >1

year >2 year >3 year >4 year

As at 30 June 2016 (£bn) ?1 month but ?3 but ?6 but ?12 Total but ?2 but ?3 but ?4 but ?5 >5 years Total

?1 year

months months months years years years years

Barclays PLC

Senior unsecured MTNs

(public benchmark) — ——0.8 0.1 2.2 2.7 5.3 11.1

Senior unsecured MTNs

(private placements) — — — 0.1—0.1 0.5 0.7

Subordinated

liabilities — — — — 1.0 1.9 2.9

Barclays Bank PLC

Deposits from banks 18.2 1.3 1.5 1.4 22.4 ——0.3 0.3 23.0

Certificates of deposit and

commercial paper 1.0 4.9 4.6 4.9 15.4 0.9 0.6 0.9

0.5 0.4 18.7

Asset backed commercial paper 4.0 3.1 0.1—7.2 — ——7.2

Senior unsecured MTNs

(public benchmark)—1.5—3.8 5.3 0.1 1.6 2.0 0.7 1.7 11.4

Senior unsecured MTNs

(private placement)49 1.1 1.7 3.0 4.9 10.7 6.1 4.4 3.4

2.2 8.9 35.7

Covered bonds ——3.2 3.2 2.4—1.8 1.0 3.7 12.1

ABS

— 0.3 1.5 1.8 1.3 0.8 1.1 — 5.0

Subordinated liabilities — ——4.3 0.1—6.0 9.3 19.7

Other47 3.2 0.2 0.3 0.3 4.0 0.5 0.4 0.3 0.3 0.7 6.2

Total 27.5 12.7 9.8 20.0 70.0 16.4 8.1

11.7 14.8 32.7 153.7

Total as at 31 December 2015 15.8 15.3 8.6 13.8 53.5 16.5 12.6 13.7 8.3 37.3 141.9

Barclays H1 2016 Fixed Income Investor Presentation

31

|

STRATEGY & HOLDCO

CAPITAL STRUCTURAL LIQUIDITY

PERFORMANCE TRANSITION ASSET QUALITY CREDIT RATING APPENDIX

& LEVERAGE REFORM & FUNDING

OVERVIEW & MREL/TLAC

Asset quality

STRATEGY & HOLDCO

CAPITAL STRUCTURAL LIQUIDITY

PERFORMANCE TRANSITION ASSET QUALITY CREDIT

RATING APPENDIX

& LEVERAGE REFORM & FUNDING

OVERVIEW &

MREL/TLAC

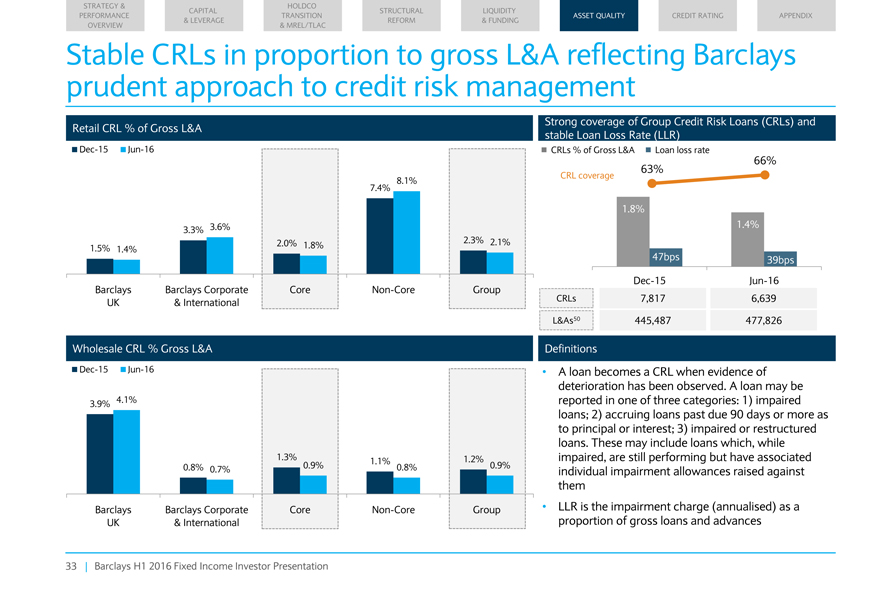

Stable CRLs in proportion to gross L&A reflecting Barclays prudent approach to credit risk management

Retail CRL % of Gross L&A Strong coverage of Group Credit Risk Loans (CRLs) and

stable

Loan Loss Rate (LLR)

Dec-15 Jun-16 CRLs % of Gross L&A Loan loss rate

66%

8.1% CRL coverage 63% 7.4% 1.8% 3.3% 3.6% 1.4% 1.5% 1.4% 2.0% 1.8% 2.3% 2.1% 47bps 39bps

Dec-15 Jun-16 Barclays Barclays Corporate Core Non-Core Group

UK & International CRLs 7,817 6,639 L&As50 445,487 477,826

Wholesale CRL % Gross L&A Definitions Dec-15 Jun-16 A loan becomes a CRL when evidence

of

deterioration has been observed. A loan may be 3.9% 4.1% reported in one of three categories: 1) impaired loans; 2) accruing loans past due 90 days or more as

to principal or interest; 3) impaired or restructured loans. These may include loans which, while

| 1.3% | 1.1% 1.2% impaired, are still performing but have associated |

| 0.8% | 0.7% 0.9% 0.8% 0.9% individual impairment allowances raised against them Barclays Barclays Corporate Core Non-Core Group LLR is the impairment charge (annualised) as a |

UK & International proportion of

gross loans and advances

Barclays H1 2016 Fixed Income Investor Presentation

33

|

STRATEGY & HOLDCO

CAPITAL STRUCTURAL LIQUIDITY

PERFORMANCE TRANSITION ASSET QUALITY CREDIT RATING APPENDIX

& LEVERAGE REFORM & FUNDING

OVERVIEW & MREL/TLAC

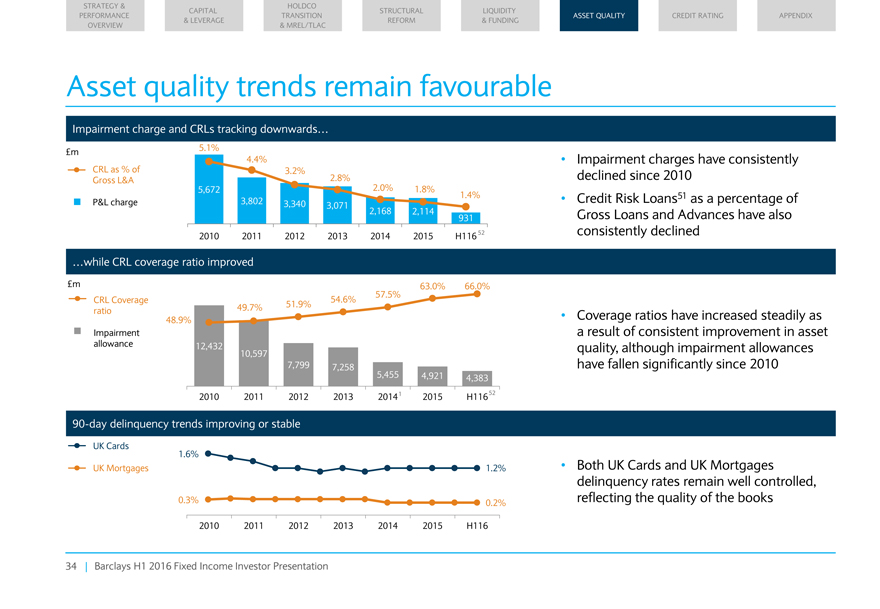

Asset quality trends remain favourable

Impairment charge and CRLs tracking

downwards…

£m 5.1%

4.4%

CRL as % of 3.2%

Gross L&A 2.8%

5,672 2.0% 1.8%

1.4% P&L charge 3,802 3,340 3,071 2,168 2,114 931 2010 2011 2012 2013 2014

2015 H116 52

…while CRL coverage ratio improved

£m 63.0% 66.0%

57.5% CRL Coverage 54.6% 49.7% 51.9% ratio 48.9% Impairment allowance 12,432 10,597 7,799 7,258 5,455 4,921 4,383 2010 2011 2012 2013 20141 2015 H11652

90-day

delinquency trends improving or stable

UK Cards

1.6%

UK Mortgages 1.2%

0.3%

0.2% 2010 2011 2012 2013 2014 2015 H116

Impairment charges have consistently declined since

2010 Credit Risk Loans51 as a percentage of Gross Loans and Advances have also consistently declined

Coverage ratios have increased steadily as a result of

consistent improvement in asset quality, although impairment allowances have fallen significantly since 2010

Both UK Cards and UK Mortgages delinquency rates

remain well controlled, reflecting the quality of the books

Barclays H1 2016 Fixed Income Investor Presentation

34

|

STRATEGY & HOLDCO

CAPITAL STRUCTURAL LIQUIDITY

PERFORMANCE TRANSITION ASSET QUALITY CREDIT RATING APPENDIX

& LEVERAGE REFORM & FUNDING

OVERVIEW & MREL/TLAC

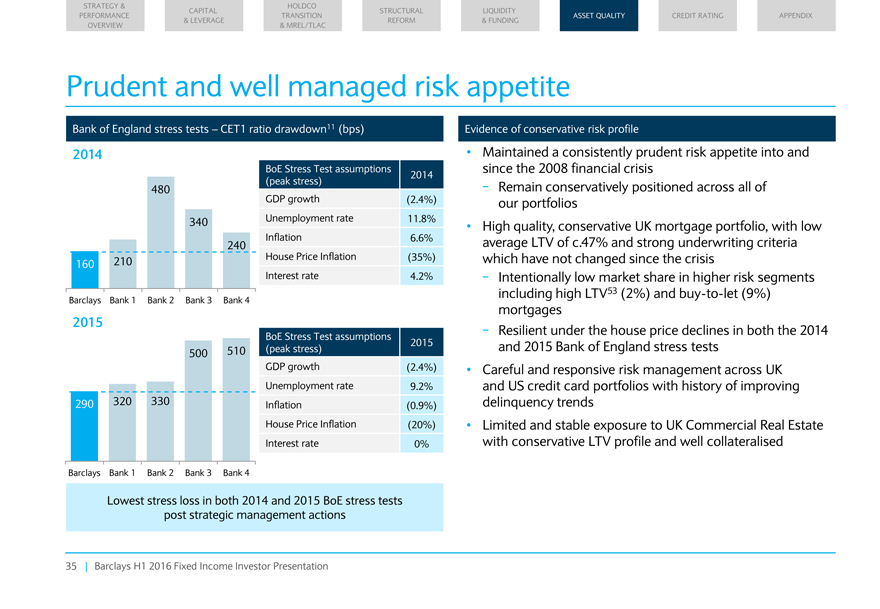

Prudent and well managed risk appetite

Bank of England stress tests –

CET1 ratio drawdown11 (bps)

0000

XxX Xxxxxx Test assumptions

2014

(peak stress)

480

GDP growth (2.4%)

340 Unemployment rate 11.8% Inflation 6.6% 240 House Price Inflation 210 (35%)

160

Interest rate 4.2%

Barclays Bank 1 Bank 2 Bank 3 Bank 4

0000

XxX Xxxxxx Test assumptions

2015 500 510 (peak stress) GDP growth (2.4%)

Unemployment rate 9.2% 290 320 330 Inflation

(0.9%) House Price Inflation (20%) Interest rate 0%

Barclays Bank 1 Bank 2 Bank 3 Bank 4

Lowest stress loss in both 2014 and 2015 BoE stress tests post strategic management actions

Evidence of conservative risk profile

Maintained a consistently prudent risk

appetite into and since the 2008 financial crisis

- Remain conservatively positioned across all of our portfolios

High quality, conservative UK mortgage portfolio, with low average LTV of c.47% and strong underwriting criteria which have not changed since the crisis

- Intentionally low market share in higher risk segments including high LTV53 (2%) and buy-to-let (9%) mortgages

- Resilient under the house price declines in both the 2014 and 2015 Bank of England stress tests Careful and responsive risk management across UK and US credit card portfolios

with history of improving delinquency trends Limited and stable exposure to UK Commercial Real Estate with conservative LTV profile and well collateralised

Barclays H1 2016 Fixed Income Investor Presentation

35

|

STRATEGY & HOLDCO

CAPITAL STRUCTURAL LIQUIDITY

PERFORMANCE TRANSITION ASSET QUALITY CREDIT RATING APPENDIX

& LEVERAGE REFORM & FUNDING

OVERVIEW & MREL/TLAC

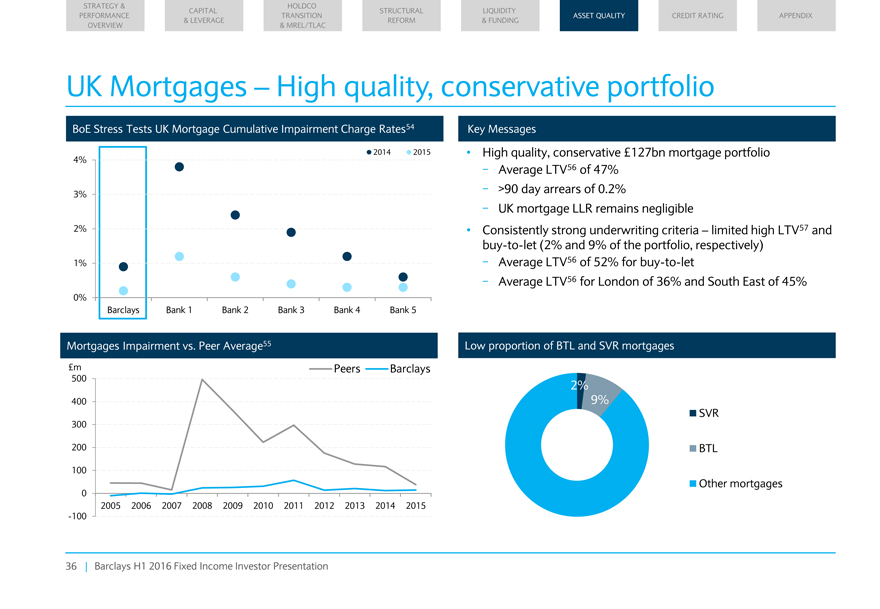

UK Mortgages – High quality, conservative portfolio

BoE Stress Tests UK

Mortgage Cumulative Impairment Charge Rates54

2014 2015

4% 3% 2% 1%

0%

Barclays Bank 1 Bank 2 Bank 3 Bank 4 Bank 5

Mortgages Impairment vs. Peer Average55

£m Peers Barclays

500 400 300 200 100

0

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 -100

Key Messages

High quality, conservative £127bn mortgage portfolio

- Average LTV56 of 47%

- >90 day arrears of 0.2%

- UK mortgage LLR remains negligible

Consistently strong underwriting criteria – limited high LTV57 and buy-to-let (2% and 9% of the portfolio, respectively)

- Average LTV56 of 52% for buy-to-let

- Average LTV56 for London of 36% and South East of 45%

Low proportion of BTL and SVR mortgages

2% 9%

SVR

BTL

Other mortgages

Barclays H1 2016 Fixed Income Investor Presentation

36

|

STRATEGY & HOLDCO

CAPITAL STRUCTURAL LIQUIDITY

PERFORMANCE TRANSITION ASSET QUALITY CREDIT RATING APPENDIX

& LEVERAGE REFORM & FUNDING

OVERVIEW & MREL/TLAC

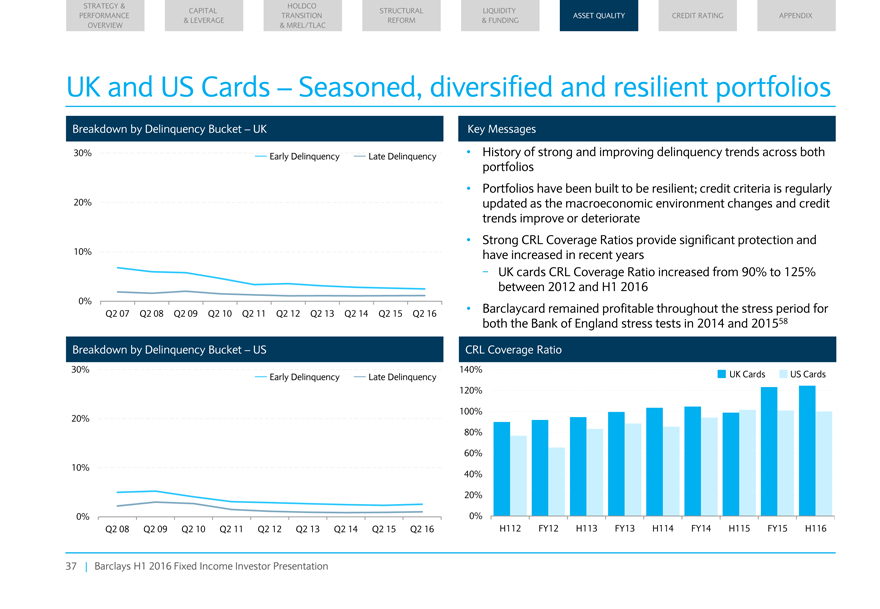

UK and US Cards – Seasoned, diversified and resilient portfolios

Breakdown by Delinquency Bucket – UK

30% Early Delinquency Late

Delinquency

20%

10%

0%

Q2 07 Q2 08 Q2 09 Q2 10 Q2 11 Q2 12 Q2 13 Q2 14 Q2 15 Q2 16

Breakdown by Delinquency Bucket – US

30%

Early Delinquency Late Delinquency

20%

10%

0%

Q2 08 Q2 09 Q2 10 Q2 11 Q2 12 Q2 13 Q2 14 Q2 15 Q2 16

Key Messages

History of strong and improving delinquency trends across both portfolios Portfolios have been built to be resilient; credit criteria is regularly updated as the

macroeconomic environment changes and credit trends improve or deteriorate Strong CRL Coverage Ratios provide significant protection and have increased in recent years

- UK cards CRL Coverage Ratio increased from 90% to 125% between 2012 and H1 2016 Barclaycard remained profitable throughout the stress period for both the Bank of England stress

tests in 2014 and 201558

CRL Coverage Ratio

140%

UK Cards US Cards 120%

100% 80% 60% 40% 20%

0%

H112 FY12 H113 FY13 H114 FY14 H115 FY15 H116

Barclays H1 2016 Fixed Income Investor Presentation

37

|

STRATEGY & HOLDCO

CAPITAL STRUCTURAL LIQUIDITY

PERFORMANCE TRANSITION ASSET QUALITY CREDIT RATING APPENDIX

& LEVERAGE REFORM & FUNDING

OVERVIEW & MREL/TLAC

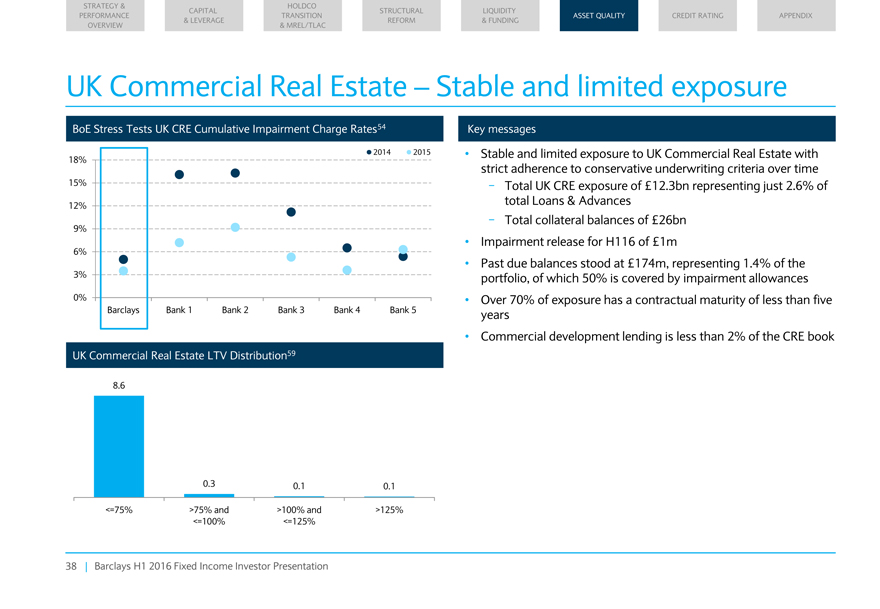

UK Commercial Real Estate – Stable and limited exposure

BoE Stress Tests

UK CRE Cumulative Impairment Charge Rates54

2014 2015

18% 15% 12% 9% 6% 3%

0%

Barclays Bank 1 Bank 2 Bank 3 Bank 4 Bank 5

UK Commercial Real Estate LTV Distribution59

8.6

0.3 0.1 0.1 <=75% >75% and >100% and >125% <=100% <=125%

Key messages

Stable and limited exposure to UK Commercial Real Estate with strict adherence to conservative underwriting criteria over time

- Total UK CRE exposure of £12.3bn representing just 2.6% of total Loans & Advances

- Total collateral balances of £26bn Impairment release for H116 of £1m

Past due

balances stood at £174m, representing 1.4% of the portfolio, of which 50% is covered by impairment allowances Over 70% of exposure has a contractual maturity of less than five years Commercial development lending is less than 2% of the CRE

book

Barclays H1 2016 Fixed Income Investor Presentation

38

|

STRATEGY & HOLDCO

CAPITAL STRUCTURAL LIQUIDITY

PERFORMANCE TRANSITION ASSET QUALITY CREDIT RATING APPENDIX

& LEVERAGE REFORM & FUNDING

OVERVIEW & MREL/TLAC

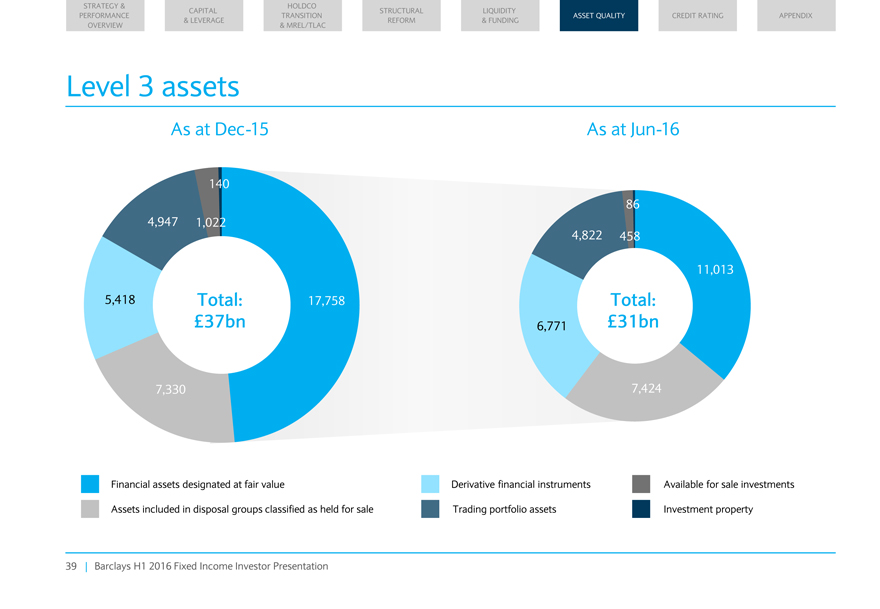

Level 3 assets

As at Dec-15 As at Jun-16

140

86 4,947 1,022 4,822 458

11,013 5,418 Total: 17,758 Total:

£37bn 6,771 £31bn

7,330 7,424

Financial assets designated at fair value Derivative financial instruments

Available for sale investments

Assets included in disposal groups classified as held for sale Trading portfolio assets Investment property

Barclays H1 2016 Fixed Income Investor Presentation

39

|

STRATEGY & HOLDCO

CAPITAL STRUCTURAL LIQUIDITY

PERFORMANCE TRANSITION ASSET QUALITY CREDIT RATING APPENDIX

& LEVERAGE REFORM & FUNDING

OVERVIEW & MREL/TLAC

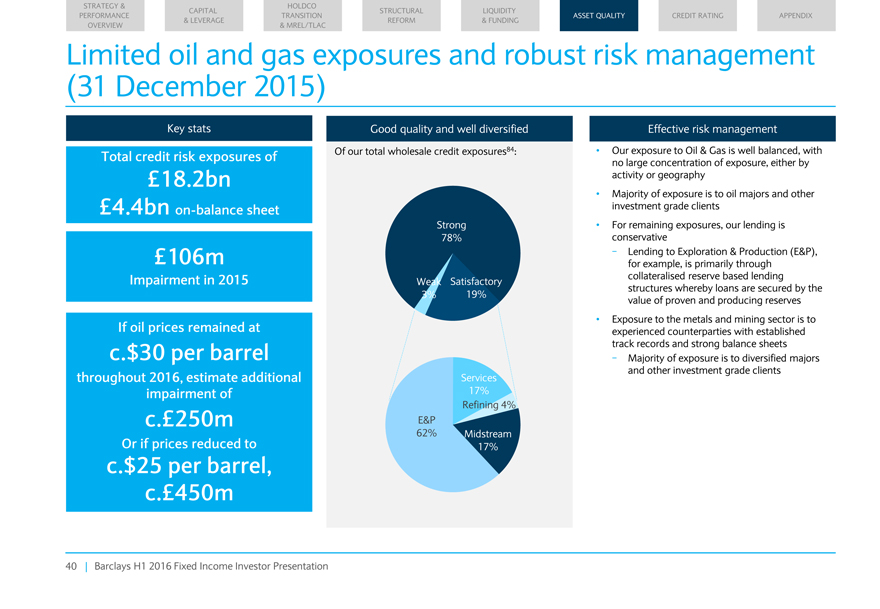

Limited oil and gas exposures and robust risk management (31 December 2015)

Key stats Good quality and well diversified Effective risk management

Total

credit risk exposures of Of our total wholesale credit exposures84: Our exposure to Oil & Gas is well balanced, with no large concentration of exposure, either by £18.2bn activity or geography

Majority of exposure is to oil majors and other £4.4bn on-balance sheet investment grade clients Strong For remaining exposures, our lending is 78% conservative £106m

—Lending to Exploration & Production (E&P), for example, is primarily through Impairment in 2015 collateralised reserve based lending Weak Satisfactory structures whereby loans are secured by the

3% 19% value of proven and producing reserves

Exposure to the metals and mining sector is to

If oil prices remained at experienced counterparties with established c.$30 per barrel track records and strong balance sheets

- Majority of exposure is to diversified majors and other investment grade clients

throughout

2016, estimate additional Services impairment of 17%

Refining 4%

c.£250m E&P

62% Midstream

Or if prices reduced to 17%

c.$25 per barrel, c.£450m

Barclays H1 2016 Fixed Income Investor Presentation

40

|

STRATEGY & HOLDCO

CAPITAL STRUCTURAL LIQUIDITY

PERFORMANCE TRANSITION ASSET QUALITY CREDIT RATING APPENDIX