Pricing Agreement

Exhibit 1.2

EXECUTION VERSION

March 9, 2015

Barclays Capital Inc.

As representative of the several Underwriters

named in Schedule I (the “Representative”)

Ladies and Gentlemen:

Barclays PLC (the “Company”) proposes to issue US$1,000,000,000 aggregate principal amount of 2.00% Fixed Rate Senior Notes due 2018 (the “2018 Notes”) and US$2,000,000,000 aggregate principal amount of 3.65% Fixed Rate Senior Notes due 2025 (the “2025 Notes” and, together with the 2018 Notes, the “Notes”). Each of the Underwriters hereby undertakes to purchase at the subscription price set forth in Schedule II hereto, the amount of Notes set forth opposite the name of such Underwriter in Schedule I hereto, such payment to be made at the Time of Delivery set forth in Schedule II hereto. The obligations of the Underwriters hereunder are several but not joint.

Each of the provisions of the Underwriting Agreement—Standard Provisions, dated September 4, 2014 (the “Underwriting Agreement”), is incorporated herein by reference in its entirety, and shall be deemed to be a part of this Agreement to the same extent as if such provisions had been set forth in full herein; and each of the representations and warranties set forth therein shall be deemed to have been made at and as of the date of this Agreement, except that each representation and warranty with respect to the Prospectus in Section 2 of the Underwriting Agreement shall be deemed to be a representation and warranty as of the date of the Prospectus and also a representation and warranty as of the date of this Agreement in relation to the Prospectus as amended or supplemented relating to the Notes. Each reference to the Representatives herein and in the provisions of the Underwriting Agreement so incorporated by reference shall be deemed to refer to you. Unless otherwise defined herein, terms defined in the Underwriting Agreement are used herein as therein defined. The Representative designated to act on behalf of each of the Underwriters of Designated Securities pursuant to Section 14 of the Underwriting Agreement and the address referred to in such Section 14 is set forth in Schedule II hereto.

An amendment to the Registration Statement, or a supplement to the Prospectus, as the case may be, relating to the Designated Securities, in the form heretofore delivered to you, is now proposed to be filed with the Commission.

The Applicable Time for purposes of this Pricing Agreement is 5:15 PM New York time on March 9, 2015. Each “free writing prospectus” as defined in Rule 405 under the Securities Act for which each party hereto has received consent to use in accordance with Section 7 of the Underwriting Agreement is listed in Schedule III hereto and is attached as Exhibit A and Exhibit B hereto.

If the foregoing is in accordance with your understanding, please sign and return to us the counterpart hereof, and upon acceptance hereof by you, on behalf of each of the Underwriters, this letter and such acceptance hereof, including the provisions of the Underwriting Agreement incorporated herein by reference, shall constitute a binding agreement between each of the Underwriters on the one hand and the Company on the other.

| Very truly yours, | ||

| BARCLAYS PLC | ||

| /s/ Xxx Xxxxx | ||

| Name: | Xxx Xxxxx | |

| Title: | Director, Capital Markets Execution | |

| Accepted as of the date hereof at New York, New York | ||

| On behalf of itself and each of the other Underwriters | ||

| BARCLAYS CAPITAL INC. | ||

| /s/ Xxxxx Xxxxx | ||

| Name: | Xxxxx Xxxxx | |

| Title: | Managing Director | |

[Signature Page to Pricing Agreement]

SCHEDULE I

| Principal Amount of the 2018 Notes |

Principal Amount of the 2025 Notes |

|||||||

| Underwriter |

||||||||

| Barclays Capital Inc. |

$ | 820,000,000 | $ | 1,640,000,000 | ||||

| Academy Securities, Inc. |

$ | 10,000,000 | $ | 20,000,000 | ||||

| ANZ Securities, Inc. |

$ | 10,000,000 | $ | 20,000,000 | ||||

| BMO Capital Markets Corp. |

$ | 10,000,000 | $ | 20,000,000 | ||||

| Capital One Securities, Inc. |

$ | 10,000,000 | $ | 20,000,000 | ||||

| CastleOak Securities, L.P. |

$ | 10,000,000 | $ | 20,000,000 | ||||

| CIBC World Markets Corp. |

$ | 10,000,000 | $ | 20,000,000 | ||||

| Xxxxxx Xxxxxxxx, LLC |

$ | 10,000,000 | $ | 20,000,000 | ||||

| Fifth Third Securities, Inc. |

$ | 10,000,000 | $ | 20,000,000 | ||||

| Lebenthal & Co, LLC |

$ | 10,000,000 | $ | 20,000,000 | ||||

| Mizuho Securities USA Inc. |

$ | 10,000,000 | $ | 20,000,000 | ||||

| National Bank of Abu Dhabi P.J.S.C. |

$ | 10,000,000 | $ | 20,000,000 | ||||

| PNC Capital Markets LLC |

$ | 10,000,000 | $ | 20,000,000 | ||||

| Scotia Capital (USA) Inc. |

$ | 10,000,000 | $ | 20,000,000 | ||||

| SMBC Nikko Securities America, Inc. |

$ | 10,000,000 | $ | 20,000,000 | ||||

| TD Securities (USA) LLC |

$ | 10,000,000 | $ | 20,000,000 | ||||

| The Xxxxxxxx Capital Group, L.P. |

$ | 10,000,000 | $ | 20,000,000 | ||||

| U.S. Bancorp Investments, Inc. |

$ | 10,000,000 | $ | 20,000,000 | ||||

| Xxxxx Fargo Securities, LLC |

$ | 10,000,000 | $ | 20,000,000 | ||||

|

|

|

|

|

|||||

| Total |

$ | 1,000,000,000 | $ | 2,000,000,000 | ||||

SCHEDULE II

Title of Designated Securities:

US$ 1,000,000,000 2.00% Fixed Rate Senior Notes due 2018

US$ 2,000,000,000 3.65% Fixed Rate Senior Notes due 2025

Price to Public:

99.991% of principal amount (for the 2018 Notes)

99.685% of principal amount (for the 2025 Notes)

Subscription Price by Underwriters:

99.766% of principal amount (for the 2018 Notes)

99.235% of principal amount (for the 2025 Notes)

Form of Designated Securities:

Each of the 2018 Notes and the 2025 Notes will be represented by one or more global notes registered in the name of Cede & Co., as nominee of The Depository Trust Company issued pursuant to the Senior Debt Securities Indenture dated November 10, 2014 between the Company and The Bank of New York Mellon acting through its London Branch, as trustee (the “Trustee”)

Securities Exchange, if any:

The New York Stock Exchange

Maturity Date:

The stated maturity of the principal of the 2018 Notes will be March 16, 2018.

The stated maturity of the principal of the 2025 Notes will be March 16, 2025.

Interest Rate:

Interest will accrue on the 2018 Notes from the date of their issuance. Interest will accrue on the 2018 Notes at a rate of 2.00% per year from and including the date of issuance.

Interest will accrue on the 2025 Notes from the date of their issuance. Interest will accrue on the 2025 Notes at a rate of 3.65% per year from and including the date of issuance.

Interest Payment Dates:

Interest will be payable on the Notes semi-annually in arrear on March 16 and September 16 of each year, commencing on September 16, 2015 and ending on the relevant Maturity Date.

Record Dates:

The Business Day immediately preceding each Interest Payment Date (or, if the Notes are held in definitive form, the 15th Business Day preceding each Interest Payment Date).

Sinking Fund Provisions:

No sinking fund provisions.

Redemption Provisions for Notes:

The 2018 Notes and the 2025 Notes are redeemable, at the option of the Company, in the event of various tax law changes that have specified consequences, as described further in, and subject to the conditions specified in, the prospectus supplement dated March 9, 2015 relating to the Notes.

Time of Delivery:

March 16, 2015 by 9:30 AM New York time.

Specified Funds for Payment of Subscription Price of Designated Securities:

By wire transfer to a bank account specified by the Company in same day funds.

Value Added Tax:

(a) If the Company is obliged to pay any sum to the Underwriters under this Agreement and any value added tax (“VAT”) is properly charged on such amount, the Company shall pay to the Underwriters an amount equal to such VAT on receipt of a valid VAT invoice;

(b) If the Company is obliged to pay a sum to the Underwriters under this Agreement for any fee, cost, charge or expense properly incurred under or in connection with this Agreement (the “Relevant Cost”) and no VAT is payable by the Company in respect of the Relevant Cost under paragraph (a) above, the Company shall pay to the Underwriters an amount which:

(i) if for VAT purposes the Relevant Cost is consideration for a supply of goods or services made to the Underwriters, is equal to any input VAT incurred by the Underwriters on that supply of goods and services, but only if and to the extent that the Underwriters are unable to recover such input VAT from HM Revenue & Customs (whether by repayment or credit) provided, however, that the Underwriters shall reimburse the Company for any amount paid by the Company in respect of irrecoverable input VAT pursuant to this paragraph (i) if and to the extent such input VAT is subsequently recovered from HM Revenue & Customs (whether by repayment or credit);

(ii) if for VAT purposes the Relevant Cost is a disbursement properly incurred by the Underwriters under or in connection with this Agreement as agent on behalf of the Company, is equal to any VAT paid on the Relevant Cost by the Underwriters provided, however, that the Underwriters shall use best endeavors to procure that the actual supplier of the goods or services which the Underwriters received as agent issues a valid VAT invoice to the Company.

Closing Location: Linklaters LLP, Xxx Xxxx Xxxxxx, Xxxxxx XX0X 0XX, Xxxxxx Xxxxxxx.

Name and address of Representative:

Designated Representative: Barclays Capital Inc.

Address for Notices:

Barclays Capital Inc.

000 Xxxxxxx Xxxxxx

Xxx Xxxx, XX 00000

Attn: Syndicate Registration

Selling Restrictions:

Each Underwriter of Designated Securities has represented, warranted and agreed that:

| a) | it has only communicated or caused to be communicated, and will only communicate or cause to be communicated, any invitation or inducement to engage in investment activity (within the meaning of Section 21 of the Financial Services and Markets Xxx 0000 (the “FSMA”)) received by it in connection with the issue or sale of any Designated Securities in circumstances in which Section 21(1) of the FSMA does not apply to the Company; and |

| b) | it has complied and will comply with all applicable provisions of the FSMA with respect to anything done by it in relation to the Designated Securities in, from or otherwise involving the United Kingdom. |

With respect to sales of the Designated Securities in Canada, each Underwriter of Designated Securities represents to and agrees with the Company that, directly or indirectly, it shall sell the Designated Securities only to purchasers purchasing as principal that are both “accredited investors” as defined in National Instrument 45-106 Prospectus and Registration Exemptions and “permitted clients” as defined in National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations.

Other Terms and Conditions:

As set forth in the prospectus supplement dated March 9, 2015 relating to the Notes, incorporating the Prospectus dated May 2, 2014 relating to the Notes.

SCHEDULE III

Issuer Free Writing Prospectus:

Final Term Sheet for the 2018 Notes, dated March 9, 2015, attached hereto as Exhibit A.

Final Term Sheet for the 2025 Notes, dated March 9, 2015, attached hereto as Exhibit B.

Barclays PLC Fixed Income Investor Presentation: 2014 Full Year Results, dated March 3, 2015, attached hereto as Exhibit C.

Exhibit A

Final Term Sheet for the 2018 Notes, dated March 9, 2015

Free Writing Prospectus

Filed Pursuant to Rule 433

Reg. Statement No. 333-195645

USD 1bn 2.00% Fixed Rate Senior Notes due 2018

Pricing Term Sheet

| Issuer: | Barclays PLC | |

| Notes: | USD 1bn 2.00% Fixed Rate Senior Notes due 2018 | |

| Expected Issue Ratings1: | A3 (Xxxxx’x) / BBB (S&P) / A (Fitch) | |

| Status: | Senior Debt / Unsecured | |

| Legal Format: | SEC registered | |

| Principal Amount: | USD 1,000,000,000 | |

| Trade Date: | Xxxxx 0, 0000 | |

| Xxxxxxxxxx Date: | March 16, 2015 (T+5) | |

| Maturity Date: | Xxxxx 00, 0000 | |

| Xxxxxx: | 2.00% | |

| Interest Payment Dates: | Semi-annually in arrear on March 16 and September 16 in each year, commencing on September 16, 2015 and ending on the Maturity Date | |

| Coupon Calculation: | 30/360, following, unadjusted | |

| Business Days: | New York, London | |

| U.K. Bail-in Power Acknowledgement: | Yes. See section entitled “Description of Senior Notes—Agreement with Respect to the Exercise of U.K. Bail-in Power” in the Preliminary Prospectus Supplement dated March 9, 2015 (the “Preliminary Prospectus Supplement”) | |

| Tax Redemption | If there is a Tax Event (as defined in the Preliminary Prospectus Supplement), the Issuer may, at its option, at any time, redeem the Notes, in whole but not in part, at a redemption price equal to 100% of their principal amount, together with any accrued but unpaid interest to (but excluding) the date fixed for redemption, as further described and subject to the conditions specified in the Preliminary Prospectus Supplement | |

| Benchmark Treasury: | T 1 02/15/18 | |

| Spread to Benchmark: | 90bps | |

| Reoffer Yield: | 2.003% | |

| Issue Price: | 99.991% | |

| Underwriting Discount: | 0.225% | |

| Net Proceeds: | USD 997,660,000 | |

| 1 | Note: A securities rating is not a recommendation to buy, sell or hold securities and may be subject to revision or withdrawal at any time. |

| Sole Bookrunner: | Barclays Capital Inc. | |

| Co-managers: | Academy Securities, Inc., ANZ Securities, Inc., BMO Capital Markets Corp., Capital One Securities, Inc., CastleOak Securities, L.P., CIBC World Markets Corp., Xxxxxx Xxxxxxxx, LLC, Fifth Third Securities, Inc., Lebenthal & Co, LLC, Mizuho Securities USA Inc., National Bank of Abu Dhabi P.J.S.C., PNC Capital Markets LLC, Scotia Capital (USA) Inc., SMBC Nikko Securities America, Inc., TD Securities (USA) LLC, The Xxxxxxxx Capital Group, L.P., U.S. Bancorp Investments, Inc., Xxxxx Fargo Securities, LLC | |

| Risk Factors: | An investment in the Notes involves risks. See “Risk Factors” section beginning on page S-8 of the Preliminary Prospectus Supplement | |

| Denominations: | USD 200,000 and integral multiples of USD 1,000 in excess thereof | |

| ISIN/CUSIP: | US06738EAF25 / 06738E AF2 | |

| Settlement: | DTC; Book-entry; Transferable | |

| Documentation: | To be documented under the Issuer’s shelf registration statement on Form F-3 (No. 333-195645) and to be issued pursuant to the Senior Debt Indenture dated November 10, 2014 between the Issuer and The Bank of New York Mellon acting through its London Branch, as trustee | |

| Listing: | We will apply to list the Notes on the New York Stock Exchange | |

| Governing Law: | New York law | |

| Definitions: | Unless otherwise defined herein, all capitalized terms have the meaning set forth in the Preliminary Prospectus Supplement | |

The Issuer has filed a registration statement (including a prospectus dated May 2, 2014 (the “Prospectus”) and the Preliminary Prospectus Supplement) with the U.S. Securities and Exchange Commission (“SEC”) for this offering. Before you invest, you should read the Prospectus and the Preliminary Prospectus Supplement for this offering in that registration statement, and other documents the Issuer has filed with the SEC for more complete information about the issuer and this offering. You may get these documents for free by searching the SEC online database (XXXXX®) at xxx.xxx.xxx. Alternatively, you may obtain a copy of the Prospectus and the Preliminary Prospectus Supplement from Barclays Capital Inc. by calling 0-000-000-0000.

-2-

Exhibit B

Final Term Sheet for the 2025 Notes, dated March 9, 2015

Free Writing Prospectus

Filed Pursuant to Rule 433

Reg. Statement No. 333-195645

USD 2bn 3.65% Fixed Rate Senior Notes due 2025

Pricing Term Sheet

| Issuer: | Barclays PLC | |

| Notes: | USD 2bn 3.65% Fixed Rate Senior Notes due 2025 | |

| Expected Issue Ratings1: | A3 (Xxxxx’x) / BBB (S&P) / A (Fitch) | |

| Status: | Senior Debt / Unsecured | |

| Legal Format: | SEC registered | |

| Principal Amount: | USD 2,000,000,000 | |

| Trade Date: | Xxxxx 0, 0000 | |

| Xxxxxxxxxx Date: | March 16, 2015 (T+5) | |

| Maturity Date: | Xxxxx 00, 0000 | |

| Xxxxxx: | 3.65% | |

| Interest Payment Dates: | Semi-annually in arrear on March 16 and September 16 in each year, commencing on September 16, 2015 and ending on the Maturity Date | |

| Coupon Calculation: | 30/360, following, unadjusted | |

| Business Days: | New York, London | |

| U.K. Bail-in Power Acknowledgement: | Yes. See section entitled “Description of Senior Notes—Agreement with Respect to the Exercise of U.K. Bail-in Power” in the Preliminary Prospectus Supplement dated March 9, 2015 (the “Preliminary Prospectus Supplement”) | |

| Tax Redemption | If there is a Tax Event (as defined in the Preliminary Prospectus Supplement), the Issuer may, at its option, at any time, redeem the Notes, in whole but not in part, at a redemption price equal to 100% of their principal amount, together with any accrued but unpaid interest to (but excluding) the date fixed for redemption, as further described and subject to the conditions specified in the Preliminary Prospectus Supplement | |

| Benchmark Treasury: | T 2 02/15/25 | |

| Spread to Benchmark: | 150bps | |

| Reoffer Yield: | 3.688% | |

| Issue Price: | 99.685% | |

| Underwriting Discount: | 0.45% | |

| Net Proceeds: | USD 1,984,700,000 | |

| 1 | Note: A securities rating is not a recommendation to buy, sell or hold securities and may be subject to revision or withdrawal at any time. |

| Sole Bookrunner: | Barclays Capital Inc. | |

| Co-managers: | Academy Securities, Inc., ANZ Securities, Inc., BMO Capital Markets Corp., Capital One Securities, Inc., CastleOak Securities, L.P., CIBC World Markets Corp., Xxxxxx Xxxxxxxx, LLC, Fifth Third Securities, Inc., Lebenthal & Co, LLC, Mizuho Securities USA Inc., National Bank of Abu Dhabi P.J.S.C., PNC Capital Markets LLC, Scotia Capital (USA) Inc., SMBC Nikko Securities America, Inc., TD Securities (USA) LLC, The Xxxxxxxx Capital Group, L.P., U.S. Bancorp Investments, Inc., Xxxxx Fargo Securities, LLC | |

| Risk Factors: | An investment in the Notes involves risks. See “Risk Factors” section beginning on page S-8 of the Preliminary Prospectus Supplement | |

| Denominations: | USD 200,000 and integral multiples of USD 1,000 in excess thereof | |

| ISIN/CUSIP: | US06738EAE59 / 06738E AE5 | |

| Settlement: | DTC; Book-entry; Transferable | |

| Documentation: | To be documented under the Issuer’s shelf registration statement on Form F-3 (No. 333-195645) and to be issued pursuant to the Senior Debt Indenture dated November 10, 2014 between the Issuer and The Bank of New York Mellon acting through its London Branch, as trustee | |

| Listing: | We will apply to list the Notes on the New York Stock Exchange | |

| Governing Law: | New York law | |

| Definitions: | Unless otherwise defined herein, all capitalized terms have the meaning set forth in the Preliminary Prospectus Supplement | |

The Issuer has filed a registration statement (including a prospectus dated May 2, 2014 (the “Prospectus”) and the Preliminary Prospectus Supplement) with the U.S. Securities and Exchange Commission (“SEC”) for this offering. Before you invest, you should read the Prospectus and the Preliminary Prospectus Supplement for this offering in that registration statement, and other documents the Issuer has filed with the SEC for more complete information about the issuer and this offering. You may get these documents for free by searching the SEC online database (XXXXX®) at xxx.xxx.xxx. Alternatively, you may obtain a copy of the Prospectus and the Preliminary Prospectus Supplement from Barclays Capital Inc. by calling 0-000-000-0000.

-2-

Fixed Income Investor Presentation

2014 Full Year Results

3 March 2015

Free Writing Prospectus

Filed Pursuant to Rule 433

Reg. Statement No. 333-195645

Exhibit C |

Financial highlights

1

Including Spain disposal |

Barclays Full Year 2014 Fixed Income Investor Presentation

2

Increased

adjusted

pre-tax

profits

by

12%

–

Core

up

3%,

Non-Core

losses

down 24%

Costs excluding CTA £16.9bn, ahead of £17bn guidance

Building

capital:

CET1

ratio

10.5%

and

BCBS

leverage

ratio

3.8%

1

Core business performed well with PBT of £6.7bn and XxX of 9.2% (10.9%

ex-CTA)

Strong progress on shrinking Non-Core and releasing capital

|

Performance Overview

ASSET QUALITY

CREDIT RATING

APPENDIX

PERFORMANCE

OVERVIEW

LIQUIDITY &

FUNDING

CAPITAL &

LEVERAGE |

Financial performance

•

Adjusted profit before tax increased by 12% to £5.5bn as PCB

and Barclaycard continued to grow profits. This was partly

offset by reduced income in the Investment Bank, which made

progress on its origination-led strategy whilst driving cost

savings and RWA efficiencies

•

Adjusted income decreased 8% while impairment reduced by

29% due to a £732m reduction in Non-Core to £168m and 8%

reduction in the Core business

•

Total adjusted operating expenses decreased 9% to £18.1bn

driven by savings from Transform programmes and favourable

currency movements. Operating expenses excluding CTA

were £16.9bn, down from £18.7bn in 2013 and ahead of the

£17bn 2014 target

•

Adjusted attributable profit was £2.8bn, resulting in EPS of

17.3p

•

Core

XxX

was

9.2%

(or

10.9%

excluding

CTA)

–

Group XxX

was 5.1%

•

Barclays Non-Core attributable loss reduced by 43% to

£1.1bn, and XxX drag fell to 4.1%

Summary Group financials: Adjusted profits up 12%

1

EPS and XxX calculations are based on adjusted attributable profit, also taking into

account tax credits on AT1 coupons | PERFORMANCE

OVERVIEW

Barclays Full Year 2014 Fixed Income Investor Presentation

4

ASSET QUALITY

CREDIT RATING

APPENDIX

LIQUIDITY &

FUNDING

CAPITAL &

LEVERAGE

Year ended

–

December (£m)

2013

2014

Income

27,896

25,728

Impairment

(3,071)

(2,168)

Total operating expenses

(19,893)

(18,069)

–

Costs to achieve Transform (CTA)

(1,209)

(1,165)

Adjusted profit before tax

4,908

5,502

Tax

(1,963)

(1,704)

NCI and other equity interests

(757)

(1,019)

Adjusted attributable profit

2,188

2,779

–

Provisions for PPI and IRH redress

(2,000)

(1,110)

–

Gain on US Xxxxxx acquisition

assets

259

461

–

Provision for ongoing investigations

and litigation relating to Foreign

Exchange

–

(1,250)

–

Loss on announced sale of the

Spanish business

–

(446)

–

ESHLA valuation revision

–

(935)

–

Own credit and goodwill impairment

(299)

34

Statutory profit before tax

2,868

2,256

Statutory attributable profit/(loss)

540

(174)

Basic EPS

1

15.3p

17.3p

Return

on average equity

1

4.1%

5.1% |

|

(£bn)

Dec-13

Sep-14

Dec-14

Balance

Sheet

Total assets

1,344

1,366

1,358

Leverage exposure

1

n/a

1,324

1,233

Leverage ratio

1

n/a

3.5%

3.7%

Capital

2

Fully loaded CET1 ratio

9.1%

10.2%

10.3%

Fully loaded CET1

capital

40.4

42.0

41.5

Risk-weighted assets

442

413

402

Liquidity

Liquidity coverage

ratio

3

96%

115%

124%

Liquidity pool

127

146

149

Funding

Loan to Deposit Ratio

4

91%

90%

89%

Wholesale funding

5

186

178

171

NSFR

3

94%

n/a

102%

•

Continued strengthening of all key balance sheet metrics

•

Good progress on capital position with fully loaded CRD

IV CET1 ratio of 10.3% and BCBS leverage ratio of

3.7%, both well on track towards 2016 Transform targets

•

Liquidity pool increased to £149bn, 82% of which in cash

and deposits with central banks and high quality

government bonds

•

Solid LCR with a £30bn surplus above 100% future

requirement

•

Funding profile remained conservative with Loan to

Deposit Ratio of 89% in retail and corporate businesses

•

Wholesale funding outstanding was £171bn, of which

£75bn matures in <1 year

•

NSFR exceeded 100% well ahead of implementation

date

Strengthening key financial metrics

Highlights

PERFORMANCE

OVERVIEW

Barclays Full Year 2014 Fixed Income Investor Presentation

5

ASSET QUALITY

CREDIT RATING

APPENDIX

LIQUIDITY &

FUNDING

CAPITAL &

LEVERAGE

1

Estimates

based

on

current

understanding

of

the

BCBS

270

standards

and

the

requirements

contained

in

the

European

Commission

delegated

act

|

2

Based

on

Barclays

interpretation

of

the

final

CRD

IV

text

and

latest

EBA

technical

standards

|

3

LCR

based

on

CRD

IV

rules

as

per

the

EU

Delegated

Act

and

the

NSFR

based

on

the

final

guidelines

published

by

the

BCBS

in

October

2014.

NSFR

disclosed

semi-annually

|

4

LDR

calculated

for

PCB,

Africa

Banking,

Barclaycard

and

Non-Core

retail

|

5

Excludes

repurchase

agreements

| |

|

Highlights

Financial performance

•

PBT up 3% at £6.7bn:

–

PCB and Barclaycard profits up 29% and 13%

respectively

–

Africa Banking profits down 6%, but up 13% on a

constant currency basis

–

Investment Bank profits down 32% in a year of

transition

•

Income fell 4% to £24.7bn

•

Impairment improved by 8% to £2.0bn, reflecting the

improving UK economic environment benefitting PCB

and reduced impairment in Africa Banking South Africa

mortgages portfolio

•

Operating expenses down 6% to £16.1bn reflecting

Transform savings across the businesses, partially offset

by an increase in CTA spend, including restructuring of

the branch network and technology improvements to

increase automation in PCB

•

Core attributable profit was £3.9bn with Core EPS of 24p

•

Core XxX was 9.2% (10.9% excluding CTA) on average

allocated equity of £42bn, up £6bn from 2013

Core business performing well

Year

ended

–

December

(£m)

2013

2014

Income

25,603

24,678

Impairment

(2,171)

(2,000)

Total operating expenses

(17,048)

(16,058)

–

Costs to achieve Transform (CTA)

(671)

(953)

Adjusted profit before tax

6,470

6,682

Tax

(1,754)

(1,976)

NCI and other equity interests

(638)

(842)

Adjusted attributable profit

4,078

3,864

Adjusted financial performance

measures

Average allocated equity

£36bn

£42bn

Return on average tangible equity

14.4%

11.3%

Return on average equity

11.3%

9.2%

Cost: income ratio

67%

65%

Basic EPS contribution

28.5p

24.0p

Dec-13

Dec-14

CRD IV RWAs

£333bn

£327bn

Leverage exposure

1

n/a

£956bn

1

BCBS

270

leverage

exposure.

All

references

to

leverage

exposure

in

this

document

is

on

this

basis

|

PERFORMANCE

OVERVIEW

Barclays Full Year 2014 Fixed Income Investor Presentation

6

ASSET QUALITY

CREDIT RATING

APPENDIX

LIQUIDITY &

FUNDING

CAPITAL &

LEVERAGE |

|

ASSET QUALITY

CREDIT RATING

APPENDIX

LIQUIDITY &

FUNDING

CAPITAL &

LEVERAGE

Year

ended

–

December

(£m)

2013

2014

–

Businesses

1,498

1,101

–

Securities and Loans

642

117

–

Derivatives

153

(168)

Income

2,293

1,050

Impairment

(900)

(168)

Total operating expenses

(2,845)

(2,011)

–

Costs to achieve Transform (CTA)

(538)

(212)

Loss before tax

(1,562)

(1,180)

Tax

(209)

272

NCI and other equity interests

(119)

(177)

Attributable profit/(loss)

(1,890)

(1,085)

Financial performance measures

Average

allocated

equity

1

£17bn

£13bn

Period end allocated equity

£15bn

£11bn

Return on average tangible equity drag

(9.6%)

(5.4%)

Return on average equity drag

(7.2%)

(4.1%)

Basic EPS contribution

(13.2p)

(6.7p)

Highlights

•

Loss before tax reduced by 24% to £1,180m as

improvements in impairments and costs were partially

offset by significant declines in income due to sales and

rundown of businesses, securities and loans and the

non-recurrence of favourable fair value movements on

derivatives

•

2013 CTA spend primarily reflects restructuring in

Europe, with the subsequent savings flowing through

2014 operating expenses

•

The income and costs relating to Spain will exit on

completion, with a c.£280m reduction in annualised

income, offset by c.£240m saving in gross costs

•

Period end equity reduced by £4.1bn to £11.0bn

•

Reduced loss and lower allocated equity reduced drag

on Group XxX to 4.1%, well within the 6% to 3% drag

guidance

Continued shrinkage and capital return in Non-Core

PERFORMANCE

OVERVIEW

Barclays Full Year 2014 Fixed Income Investor Presentation

7 |

ASSET QUALITY

CREDIT RATING

APPENDIX

PERFORMANCE

OVERVIEW

LIQUIDITY &

FUNDING

Capital & Leverage

CAPITAL &

LEVERAGE |

|

Fully

loaded

(FL)

CRD

IV

CET1

ratio

progression

1

RWA reduction (£bn)

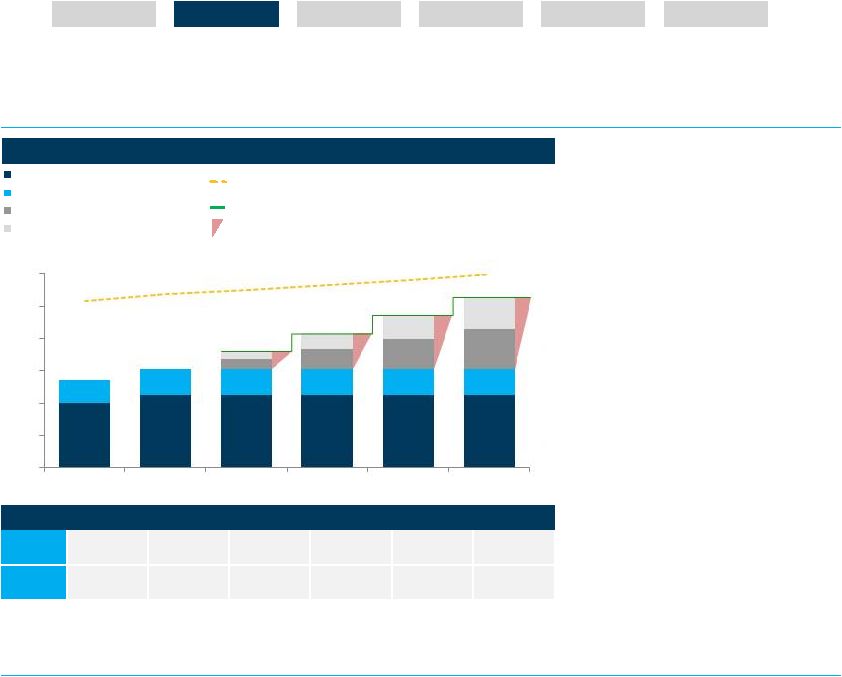

Good progress on CET1 ratio towards 2016 Transform

target

•

FL CRD IV CET1 ratio up 120bps, or c.140bps if including the

sale of the Spanish businesses, demonstrating good progress

towards 2016 Transform target of greater than 11%

•

Continued capital build as FL CRDIV CET1 capital grew by

£1.1bn to £41.5bn, after absorbing £3.3bn of adjusting items

•

Confident that our planned trajectory positions us well to meet

future regulatory requirements

•

RWAs reduced by £41bn, or £46bn including the sale of

the Spanish businesses, reflecting excellent progress on

the run-down of Non-Core to £75bn

•

Increases due to model updates largely offset by

methodology and policy driven decreases

Spain

c.16bps

2

40

42

41

CET1

Capital

(9%)

o/w

Spain

(£5bn)

2

1

Based

on

Barclays

interpretation

of

the

final

CRD

IV

text

and

latest

EBA

technical

standards.

Following

the

full

implementation

of

CRD

IV

reporting

in

2014,

the

previously

reported

31

December

2013

RWAs

were

revised

by

£6.9bn

to

£442bn

and

fully

loaded

CET1

ratio

by

(0.2%)

to

9.1%

|

2

As

announced

on

2

January

2015

|

CAPITAL &

LEVERAGE

Barclays Full Year 2014 Fixed Income Investor Presentation

9

ASSET QUALITY

CREDIT RATING

APPENDIX

PERFORMANCE

OVERVIEW

LIQUIDITY &

FUNDING

9.1%

10.2%

10.3%

>11%

Dec-13

Sep-14

Dec-14

2016

442

413

402

c.400

Dec-13

Sep-13

Dec-14

2016

Target

Guidance

+120bps |

ASSET QUALITY

CREDIT RATING

APPENDIX

PERFORMANCE

OVERVIEW

LIQUIDITY &

FUNDING

RWAs (£bn)

Highlights

•

RWAs reduced by £40.6bn, or £46bn including the sale

of the Spanish businesses, reflecting excellent progress

on the rundown of Non-Core, allowing for growth in Core

businesses

•

Non-Core RWAs reduced £35bn to £75bn reflecting the

disposal of businesses, rundown and exit of securities

and loans, and derivative risk reductions

•

If excluding the impact of methodology and model

changes, Investment Bank RWAs reduced by £11bn

driven principally by trading book risk reductions

•

Increases due to model updates largely offset by

methodology and policy driven decreases

RWAs: Well managed to support business growth and

returns

1

Excludes

model

and

methodology

driven

movements

|

2

Includes

foreign

exchange

movements

of

£(1.5)bn.

This

does

not

include

movements

for

modelled

counterparty

risk

or

modelled

market

risk

|

1

402

1

Spain

1

1

442

2

CAPITAL &

CAPITAL &

LEVERAGE

LEVERAGE

Barclays Full Year 2014 Fixed Income Investor Presentation

10

2013

Core

business

growth

(ex. IB)

BNC

run-down

IB

reduction

Net model

and

methodology

updates

Other

2014

9

5

34

11

1

3 |

Barclays Non-Core:

Outperforming on RWA Spain

2

1

Derivatives

figure

for

Sep-14

has

been

adjusted

following

reclassification

of

assets

previously

reported

in

securities

and

loans

|

2

Portion

of

Spain

within

Barclays

Non-Core

|

3

2016

target

amended

to

reflect

the

impact

of

Spain

|

Target = 80

Barclays Full Year 2014 Fixed Income Investor Presentation

11

Dec-13

Disposals

Efficiencies

Maturities

and other

Dec-14

110

75

19

11

5

Xxx-00

Xxx-00

Xxx-00

0000

Xxxxxxx

Operational risk and DTA

Securities and loans

Xxxxxxxxxxx

0

Xxxxxxxxxx

000

00

9

9

22

16

31

31

19

13

5

Revised

Target

75

ASSET QUALITY

CREDIT RATING

APPENDIX

PERFORMANCE

OVERVIEW

LIQUIDITY &

FUNDING

CAPITAL &

LEVERAGE

RWA reduction bridge (£bn)

RWA by type (£bn)

81 |

Continued progress on the transition towards our

‘target’

end-state capital structure

Evolution of capital structure

Fully loaded CRD IV capital position

•

Fully loaded CRD IV CET1 ratio at 10.3% (10.2% on PRA transitional

basis) on track to meet our target of > 11% in 2016. The ratio was

well in excess of the 7% PRA regulatory target

•

Robust buffers to contingent capital triggers

–

AT1 contingent capital: c.330bps or £13.3bn

–

T2

contingent

capital:

c.530bps

or

£21.5bn

•

As

we

build

CET1

capital

over

the

transitional

period,

we

expect

to

reach a range of 11.5-12% in end-state reflecting our intention to

hold an internal management buffer of up to 150bps over

future

minimum

requirements

•

Transitional total capital ratio increased to 16.5% (2013: 15.0%), and

fully loaded total capital ratio increased to 15.4% (2013: 13.9%)

•

Further clarity required on Total Loss Absorbing Capacity (TLAC)

quantum and composition. In the interim, we continue to build

towards our ‘target’

end-state capital structure which assumes at

least 17% of total capital; final requirements subject to PRA

discretion

•

Barclays 2015 Pillar 2A requirement as per the PRA’s Individual Capital

Guidance (ICG) is 2.8%. The ICG is subject to at least annual review

–

CET1 of 1.6% (assuming 56%)

–

AT1 of 0.5% (assuming 19%)

–

T2 of 0.7% (assuming 25%)

•

The PRA consultation on the Pillar 2 framework (CP1/15), and Basel

Committee consultations and reviews of approaches to Pillar 1 and Pillar 2

risk might further impact the Pillar 2A requirement in the future

1.8% (£7.4bn)

Legacy T1

3.5%

(£14.3bn)

T2

17%

Total capital ratio

CCCB/

Sectoral

buffers

16.5%

Total capital ratio

1.6% P2A

Pillar

2A

requirement

6

4.5%

CET1

1.7% (£6.9bn)

Legacy T1

1

Difference

to

fully

loaded

ratio

of

10.3%

arises

from

a

regulatory

adjustment

relating

to

unrealised

gains

|

2

Being

the

higher

of

7%

PRA

expectation

and

CRD

IV

capital

requirements

|

3

CRD

IV

rules

on

mandatory

distribution

restrictions

apply

from

1

January 2016

onwards

based

on

transitional

CET1

requirements

|

4

Based

on

the

CRD

IV

CET1

transitional

(FSA

October

2012

statement)

the

ratio

was

12.3%

as

at

31

December

2014

|

5

Barclays

current

regulatory

target

is

to

meet

a

FL

CRD

IV

CET1

ratio

of

9%

by 2019,

plus

a

Pillar

2A

add-on.

Pillar

2A

requirements

for

2015

held

constant

out

to

end-state

for

illustrative

purposes.

The

PRA

buffer

is

assumed

to

be

below

the

combined

buffer

requirement

of

4.5%

in

end-

state

albeit

this

might

not

be

the

case.

CCCB,

other

systemic

and

sectoral

buffer

assumed

to

be

zero

|

6

Point

in

time

assessment

made

at

least

annually,

by

the

PRA,

to

reflect

idiosyncratic

risks

not

fully

captured

under

Pillar

1

|

2.5%

Capital

Conservation buffer

Max 1.5%

Internal buffer

2.0%

AT1 (incl. P2A)

2.9%

T2 (incl. P2A)

2.0%

G-SII

Barclays Full Year 2014 Fixed Income Investor Presentation

12

ASSET QUALITY

CREDIT RATING

APPENDIX

PERFORMANCE

OVERVIEW

LIQUIDITY &

FUNDING

CAPITAL &

LEVERAGE

10.2%

1

(£40.9bn)

CET1

1.1% (£4.3bn) AT1

Barclays FY 14

capital structure

(PRA Transitional)

Barclays'

'target' end-state

capital structure

2

3

5

4 |

ASSET QUALITY

CREDIT RATING

APPENDIX

PERFORMANCE

OVERVIEW

LIQUIDITY &

FUNDING

CAPITAL &

LEVERAGE

13

We intend to manage our CET1 capital ratio to mitigate

against the risk of mandatory distribution restrictions

•

Mandatory restrictions to discretionary

distributions

2

will apply to all European

banks, under CRD IV, from 1 January 2016

(Art. 162.2 of CRD)

•

As outlined in Art. 141 of CRD, mandatory

distribution restrictions apply if an

institution fails to meet the combined buffer

requirement (CBR)

3

at which point a

Maximum Distributable Amount (MDA) is

calculated on a reducing scale

•

CBR is phased in from 2016. In end state,

we intend to hold an internal management

buffer of up to 150bps above CBR

providing prudent headroom to the

mandatory distribution restriction point

•

As at 1 January 2016, mandatory

distribution restrictions on interest payment

would apply at 7.2%, stepping up to 10.6%

by 2019 when the CRD IV transitional rules

are fully phased in

1

•

Barclays expects to have full discretion in

the allocation of permitted distributions

within the MDA

To AT1

7% trigger

c.£13bn

c.£15bn

>16bn

c.£17bn

c.£18bn

To MDA

restriction

n/a

n/a

>15bn

c.£12bn

c.£9bn

c.£4-6bn

CET1 requirements

1

(as at 1 January except FY14)

Capital conservation buffer (CET1)

G-SII buffer (CET1)

Trajectory of fully loaded CET1 ratio, assuming >11% target

is met

after

which

we

build

towards

11.5-12%

in

end

state

3

Distributions subject to mandatory distribution restrictions

Minimum CET1 ratio

Estimated

buffers

1

(fully

loaded

CET1

ratio

vs.

AT1

7%

trigger

and

vs.

MDA

restrictions)

Sliding scale of restrictions

Pillar 2A

1

This

analysis

is

presented

for

illustrative

purposes

only

and

is

not

a

forecast

of

Barclays’

results

of

operations

or

capital

position

or

otherwise.

The

analysis

is

based

on

certain

assumptions

(including

a

straight

line

progress

towards

meeting

the

>11%

CET1

ratio

target

in

2016,

and

11.5-12%

in

end-state,

and

that

the

P2A

requirement

for

2015

is

constant

out

to

2019

which

may

not

be

the

case

as

the

requirement

is

subject

to

at

least

annual

review)

which

cannot

be

assured

and

are

subject

to

change.

This

illustration

does

not

consider

proposals

in

the

FSB

Consultative

Document

on

the

adequacy

of

loss-absorbing

capacity

of

global

systemically

important

banks

in

resolution

|

2

Dividends

on

ordinary

shares,

interest

payments

in

respect

of

AT1

securities

and

variable

compensation

|

3

As

per

Art.

128(6)

of

CRD:

total

CET1

capital

required

to

meet

the

requirement

for

the

capital

conservation

buffer,

as

well

as

an

institution

specific

countercyclical

buffer

(CCCB),

G-SII

buffer,

O-SII

buffer

and

systemic

risk

buffer

as

applicable.

For

Barclays

this

is

currently

the

2.5%

Capital

Conservation

Buffer

and

2%

G-SII

buffer

while

the

CCCB

and

other

systemic

risk

and

sectoral

buffers

are

assumed

to

be

zero

|

CAPITAL &

LEVERAGE

Barclays Full Year 2014 Fixed Income Investor Presentation

|

10.6%

8.4%

7.2%

9.5%

4.0%

4.5%

4.5%

4.5%

4.5%

4.5%

1.4%

1.6%

1.6%

1.6%

1.6%

1.6%

0.6%

1.3%

1.9%

2.5%

0.5%

1.0%

1.5%

2.0%

10.3%

>11.0%

11.5-12%

0%

2%

4%

6%

8%

10%

12%

FY 14

2015

2016

2017

2018

2019

c.£18-20bn |

|

ASSET QUALITY

CREDIT RATING

APPENDIX

PERFORMANCE

OVERVIEW

LIQUIDITY &

FUNDING

Leverage

ratio

progression

1

Leverage

exposure

reduction

(£trn)

1

•

Significant reduction in leverage exposure, driven

principally by reductions in Non-Core and in the Core

Investment Bank

•

Leverage exposure decreased by £91bn in Q4 2014

driven mainly by a £35bn reduction in SFT exposure,

£16bn reduction in PFE, and a seasonal £28bn

reduction in settlement balances

+30bps

41

45

46

T1

Capital

1

(9%)

BCBS 270

impact

1

Dec-13 not comparable to the estimates as of Jun-14 onwards due to different

basis of preparation. Dec-13 estimated ratio and T1 capital based on PRA leverage ratio calculated as fully loaded CRD IV T1 capital adjusted for certain

PRA defined deductions, and a PRA adjusted leverage exposure measure. From

Jun-14 onwards, estimated ratios based on current understanding of the BCBS 270 standards and the requirements contained in the European

Commission

delegated

act.

|

2

As

announced

on

2

January

2015

Barclays Full Year 2014 Fixed Income Investor Presentation

14

Leverage ratio progression ahead of plan

Dec-00

Xxx-00

Xxx-00

0000

Xxxxxx

0.0%

3.4%

3.7%

>4%

Dec-13

Jun-14

Sep-14

Dec-14

1.36

1.35

1.32

1.23

CAPITAL &

LEVERAGE

•

Leverage ratio up significantly to 3.7%, or 3.8% if

reflecting

the

sale

of

the

Spanish

businesses

2

,

well

on track

to meet 2016 Transform target of in excess of 4%

•

Improvement over the year driven by T1 capital growth,

including £2.3bn of AT1 issuance, and leverage exposure

reduction

•

Leverage ratio already in line with expected minimum end-

state requirement of 3.7% as outlined by the Financial Policy

Committee |

|

ASSET QUALITY

CREDIT RATING

APPENDIX

PERFORMANCE

OVERVIEW

LIQUIDITY &

FUNDING

BCBS

leverage

exposure

1

(£bn)

Highlights

•

Leverage exposures during Q4 14 decreased by £91bn to

£1,233bn

•

Loans and advances and other assets decreased by £52bn to

£713bn primarily due to a seasonal reduction in settlement

balances of £28bn and a £13bn reduction in cash balances

•

SFTs decreased £35bn to £157bn driven by a £26bn reduction

in IFRS reverse repurchase agreements and £9bn in SFT

adjustments, reflecting deleveraging in BNC and a seasonal

reduction in trading volumes

•

Total derivative exposures decreased £8bn due to a £16bn

reduction in the potential future exposure (PFE), partially offset

by an increase in IFRS derivatives and cash collateral

PFE on derivatives decreased £16bn to £179bn mainly

due to reductions in business activity and optimisations,

including trade compressions and tear-ups. This was

partially offset by an increase relating to sold options

driven by a change to the basis of calculation

Other derivatives exposures (excluding PFE) increased

£8bn to £92bn driven by an increase in IFRS derivatives

of £57bn to £440bn and cash collateral £13bn to £73bn.

This was broadly offset by increases in allowable

derivatives netting

Steady progression on leverage ratio

1,353

1,324

L&A and other assets

SFTs

Undrawn commitments

Derivatives

BCBS leverage

ratio

1

1

Current

understanding

of

the

BCBS

270

standards

and

the

requirements

contained

in

the

European

Commission

delegated

act

|

2

Loans

and

advances

and

other

assets

net

of

regulatory

deductions

and

other

adjustments

|

1,233

CAPITAL &

LEVERAGE

Barclays Full Year 2014 Fixed Income Investor Presentation

15

3.4%

3.5%

3.7%

732

743

690

288

279

271

228

192

157

105

110

115

Jun-14

Sep-14

Dec-14

–

–

2 |

ASSET QUALITY

CREDIT RATING

APPENDIX

PERFORMANCE

OVERVIEW

CAPITAL &

LEVERAGE

Liquidity & Funding

LIQUIDITY &

FUNDING |

|

17

•

Losses arise at OpCo, and are transmitted to HoldCo through write-

down of intercompany instruments

•

Losses at HoldCo are limited to its investment in the OpCo

•

Losses should be allocated in accordance with the insolvency

hierarchy, meaning pari passu treatment of equal-ranked internal and

external claims

•

‘No creditor worse off’

than in insolvency safeguard expected to apply

for senior unsecured debt

Expected

creditor

hierarchy

during

transition

1

Barclays position

•

Barclays has started to issue capital and term senior unsecured debt

out of Barclays PLC, the Holding Company

•

To better align the credit proposition between investors in HoldCo and

OpCo securities during the transition period, proceeds raised by

Barclays PLC have been used to subscribe for capital and senior

unsecured term debt in Barclays Bank PLC with corresponding ranking

•

As the HoldCo is a creditor of the OpCo alongside OpCo external

creditors, respecting the creditor hierarchy should require pari passu

treatment between internally and externally OpCo issued capital and

debt of the same rank

1

•

Maturing

capital

and

term

senior

unsecured

debt

to

be

refinanced

out of HoldCo during the transition period, making the external creditor

hierarchy simpler post transition

Transition towards a holding company capital and

funding model

Barclays Bank

PLC (OpCo)

External capital

External equity

External senior

Subscription of internal OpCo

issued equity, capital and

debt

2

1

st

OpCo Equity

2

nd

OpCo external

& intercompany

AT1

3

rd

OpCo external

& intercompany

T2

4

th

OpCo external

& intercompany

senior

unsecured debt

External OpCo

senior

External OpCo

capital

1

Based

on

Barclays

expectations

of

the

creditor

hierarchy

in

a

resolution

scenario;

assumes

internal

subordination

not

imposed

during

transition

|

2

Internal

issuance

in

each

case

currently

with

ranking

corresponding

to

external

HoldCo

issuance.

Detailed

disclosure

can

be

found

in

the

Barclays

PLC

and

Barclays

Bank

PLC

2014

annual

reports

|

3

Total

loss

absorbing

capacity

(TLAC)

as

proposed

in

the

FSB

Consultative

Document

on

the

adequacy

of

loss-absorbing

capacity

of

global

systemically

important

banks

in

resolution

I

Barclays Full Year 2014 Fixed Income Investor Presentation

LIQUIDITY &

FUNDING

ASSET QUALITY

CREDIT RATING

APPENDIX

PERFORMANCE

OVERVIEW

CAPITAL &

LEVERAGE

(HoldCo)

When required to qualify as TLAC

3

in a material subsidiary,

senior obligations with >1 year residual maturity would need

to be downstreamed in subordinated form to its “excluded

liabilities”

Investment at HoldCo gives exposure to diversified businesses

post ring-fencing, comparable to the position of OpCo investors

today

–

–

•

Evolving regulation, including the implementation of MREL beginning

1 Jan 2016 and any subsequent regulatory policy interpretations,

may require a change to the current approach. Any change would be

communicated to the market |

|

ASSET QUALITY

CREDIT RATING

APPENDIX

PERFORMANCE

OVERVIEW

LIQUIDITY &

FUNDING

CAPITAL &

LEVERAGE

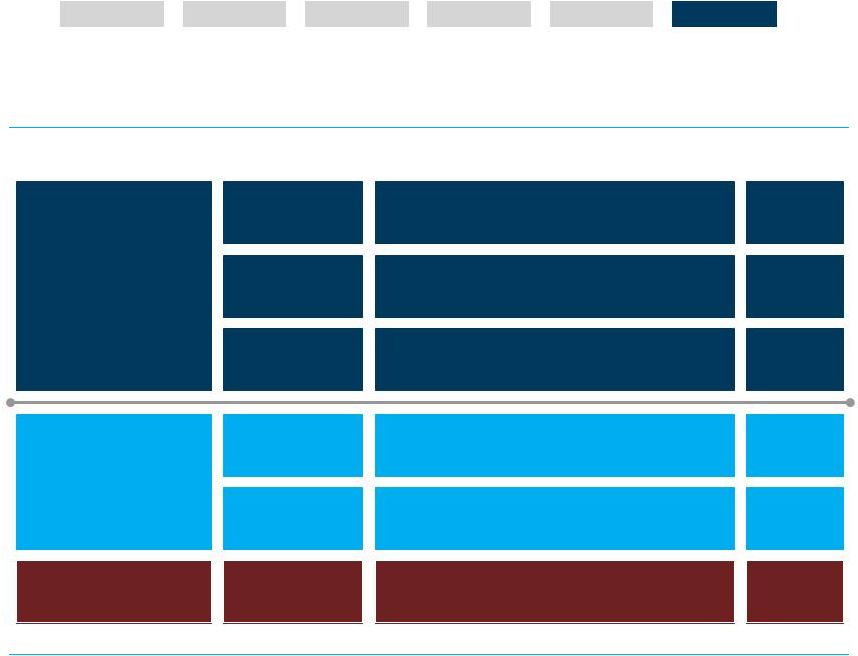

Balance sheet

2014

2013

As at 31 December

Notes

£m

£m

Assets

Investment in subsidiary

46

33,743

30,059

Loans and advances to subsidiary

46

2,866

-

Derivative financial instrument

46

313

271

Other assets

174

812

Total assets

37,096

31,142

Liabilities

Deposits from banks

528

400

Subordinated liabilities

46

810

-

Debt securities in issue

46

2,056

-

Other liabilities

10

-

Total liabilities

3,404

400

Called up share capital

31

4,125

4,028

Share premium account

31

16,684

15,859

Other equity instruments

31

4,326

2,063

Capital redemption reserve

394

394

Retained earnings

8,163

8,398

33,692

30,742

37,096

31,142

Barclays PLC Parent Company Balance Sheet

Extract from notes to Parent Company Balance Sheet

46 Barclays PLC (the Parent Company)

Investment in subsidiary

The investment in subsidiary of £33,743m (2013: £30,059m) represents

investments made into Barclays Bank PLC, including £4,326m (2013:

£2,063m) of Additional Tier 1 (AT1) securities. The increase of

£3,684m during the year was due to a £2,263m increased holding in

Barclays Bank PLC issued securities and a further cash contribution of

£1,421m. Loans and advances to subsidiary and debt securities in

issue During the period, Barclays PLC issued £810m equivalent of Fixed

Rate Subordinated Notes (Tier 2) and £2,056m equivalent of Fixed Rate

Senior Notes accounted for as subordinated liabilities and debt securities

in issue respectively. The proceeds raised through these transactions were

used, respectively, to subscribe for £810m equivalent of Fixed Rate

Subordinated Notes (Tier 2) issued by Barclays Bank PLC, and to make

£2,056m equivalent of Fixed Rate Senior Loans to Barclays Bank PLC, in

each case with a ranking corresponding to the notes issued by Barclays

PLC.

Barclays PLC Parent company accounts

LIQUIDITY &

FUNDING

Barclays Full Year 2014 Fixed Income Investor Presentation

18

Total liabilities and shareholders’ equity

Total shareholders’ equity

Shareholders’ equity

|

|

ASSET QUALITY

CREDIT RATING

APPENDIX

PERFORMANCE

OVERVIEW

CAPITAL &

LEVERAGE

19

•

Proactive transition towards a HoldCo funding and

capital model positions us well to meet potential future

TLAC requirements

•

While requirements remain to be set, Barclays current

expectation is a multi-year conformance period

•

Good portion of OpCo term senior unsecured debt

maturing before 2019 which can be refinanced from

HoldCo

•

Based on Barclays current interpretation of TLAC

requirements,

proxy

TLAC

ratio

at

24%

4

on

the

assumption that Barclays Bank PLC term non-

structured senior unsecured debt is refinanced from

HoldCo and subordinated to OpCo excluded liabilities

•

Currently do not intend to use HoldCo senior

unsecured debt proceeds to subscribe for OpCo

liabilities on a subordinated basis until required to do

so

•

The future TLAC-ratio will further benefit from CET1

capital growth and AT1 issuance towards end-state

expectations

•

As TLAC rules are finalised and as we approach

implementation date, we will assess the appropriate

composition and quantum of our future TLAC stack

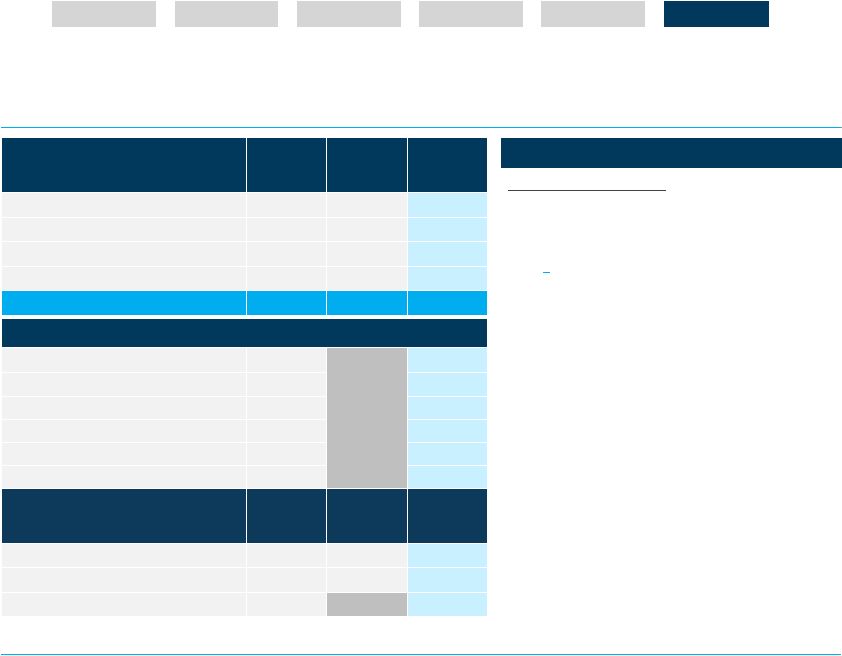

Proxy

Total

Loss

Absorbing

Capacity

(TLAC)

1

(£bn)

Dec-14

PRA transitional Common Equity Tier 1 capital

41

PRA transitional Additional Tier 1 regulatory capital

11

Barclays PLC (HoldCo)

4

Barclays Bank PLC (OpCo)

7

PRA transitional Tier 2 regulatory capital

14

Barclays PLC (HoldCo)

1

Barclays Bank PLC (OpCo)

13

PRA transitional total regulatory capital

66

HoldCo

term

non-structured

senior

unsecured

debt

2

2

OpCo

term

non-structured

senior

unsecured

debt

3

29

Total term non-structured senior unsecured debt

97

CRD IV RWAs

402

BCBS leverage exposure

1,233

Proxy risk-weighted TLAC ratio

~ 24%

Proxy leverage based TLAC ratio

~ 8%

1

For

illustrative

purposes

only

reflecting

Barclays

interpretation

of

the

FSB

Consultative

Document

on

“Adequacy

of

loss-absorbing

capacity

of

global

systemically

important

banks

in

resolution”,

including

certain

assumptions

on

the

inclusion

or

exclusion

of

certain

liabilities

where

further

regulatory

guidance

is

necessary.

Evolving

regulation,

including

the

implementation

of

MREL

beginning

1

Jan

2016

and

any

subsequent

regulatory

policy

interpretations,

may

require

a

change

to

the

current

approach

|

2

Barclays

PLC

issued

senior

unsecured

term

debt

assumed

to

qualify

for

consolidated

TLAC

purposes

I

3

Comprise

all

outstanding

Barclays

Bank

PLC

issued

public

and

private

term

senior

unsecured

debt,

regardless

of

residual

maturity.

This

excludes

£35bn

of

notes

issued

under

the

structured

notes

programmes

|

4

Including

the

4.5%

combined

buffer

requirement

which

needs

to

be

met

in

CET1.

The

combined

buffer

requirement

comprises

a

2%

G-SII

buffer

and

2.5%

capital

conservation

buffer

a

fully

phased

in

basis.

Barclays Full Year 2014 Fixed Income Investor Presentation

LIQUIDITY &

FUNDING |

|

ASSET QUALITY

CREDIT RATING

APPENDIX

PERFORMANCE

OVERVIEW

LIQUIDITY &

FUNDING

CAPITAL &

LEVERAGE

Balance sheet is conservatively funded

20

Trading portfolio assets and reverse repurchase

agreements are largely funded in wholesale markets by

repurchase agreements and trading portfolio liabilities

Customer loans and advances largely funded by

customer deposits

Decreasing reliance on wholesale funding (£171bn as at

31 December 2014, down £15bn since 31 December

2013)

Liquidity pool predominantly funded through wholesale

markets, and well in excess of short-term wholesale

funds

Derivative assets and liabilities matched

1

Matched

cash

collateral

and

settlement

balances

|

2

The

Group

Loan

to

Deposit

Ratio

(LDR)

includes

BAGL,

cash

collateral

and

settlement

balances

|

3

Including

L&A

to

banks,

financial

assets

at

fair

value,

AFS

securities

(excluding

liquidity

pool),

unencumbered

trading

portfolio

assets,

and

excess

derivative

assets

|

4

Including

excess

cash

collateral

and

settlement

balances

|

LIQUIDITY &

FUNDING

Barclays Full Year 2014 Fixed Income Investor Presentation

Derivatives, 438

Reverse repo, 132

Matched

funding

£709bn

Trading portfolio assets, 37

Other

matched

assets¹,

102

Other

assets³,

135

Customer loans & advances, 311

Liquidity pool, 149

100%

Group

LDR

2

Customer deposits, 332

Other

liabilities,

31

4

>1 year wholesale funds, 96

<1 year wholesale funds, 75

Other

matched

liabilities¹,

102

Trading portfolio liabilities, 45

Repo, 124

Derivatives, 438

Total assets

Total Liabilities and Equity

Balance sheet structure -

£1.3tn (excluding BAGL), 31 Dec 14

Equity, 61 |

|

High quality liquidity pool (£bn)

Key messages

•

Further strengthened liquidity position with the Group

liquidity pool up by £22bn to £149bn, building a larger

surplus to the internal Liquidity Risk Appetite

•

Quality of the pool remains high:

82% held in cash, deposits with central banks and high

quality government bonds

Over 95% of government bonds are securities issued by

UK, US, Japanese, French, German, Danish, Swiss and

Dutch sovereigns

•

Even though not a regulatory requirement, the size of

our liquidity pool is almost double that of wholesale debt

maturing in less than a year

•

Additional significant sources of contingent funding in

the form of high quality assets pre-positioned with

central banks globally

•

Continued strengthening of estimated CRD IV/Basel 3

liquidity ratios:

Estimated LCR increased to 124%, mainly due to the

increase in the size of the liquidity pool, resulting in a

£30bn surplus above the future 100% requirement

Estimated NSFR strengthened to 102%, primarily driven

by the progress on run-down of Non-Core

Maintaining a robust liquidity position, with pool well in

excess of internal and external minimum requirements

Estimated

CRD IV/Basel 3 liquidity ratios

Metric

2013

2014

Expected 100%

requirement date

LCR

2

96%

124%

1 January 2018

Surplus

-

£30bn

NSFR

3

94%

102%

1 January 2018

Surplus to 30-day Barcxxxx-xxxxxxxx XXX

0000

0000

XXX

000%

124%

Surplus

£5bn

£29bn

127

150

1

Barclays

interpretation

of

current

rules

and

guidance

|

2

LCR

estimated

based

on

the

EU

delegated

act

|

3

Estimated

based

on

the

final

BCBS

rules

published

in

October

2014

|

Barclays Full Year 2014 Fixed Income Investor Presentation

21

85

43

37

46

62

85

19

22

27

2012

2013

2014

Cash & Deposits at Central Banks

Government Bonds

Other Available Liquidity

149

PERFORMANCE

ASSET QUALITY

CREDIT RATING

APPENDIX

LEVERAGE

OVERVIEW

FUNDING

CAPITAL &

LIQUIDITY &

1 |

|

ASSET QUALITY

CREDIT RATING

APPENDIX

PERFORMANCE

OVERVIEW

LIQUIDITY &

FUNDING

CAPITAL &

LEVERAGE

22

Continue to access diverse wholesale funding sources

across multiple products, currencies and maturities

Key Messages

By

currency

1

USD

EUR

GBP

Others

As at 31 December 2014

35%

32%

25%

8%

As at 31 December 2013

35%

36%

19%

10%

Wholesale funding by product (as at 31 December 2014)

By

remaining

maturity

1

:

WAM

net

of

liquidity

pool

105

months

1

Given

different

accounting

treatments,

AT1

capital

is

not

included

in

outstanding

subordinated

liabilities,

while

T2

contingent

capital

notes

are

included

|

2

Primarily

comprised

of

fair

valued

deposits

(£5bn)

and

secured

financing of

physical

gold

(£5bn)

|

2

1

2

LIQUIDITY &

FUNDING

Barclays Full Year 2014 Fixed Income Investor Presentation

10%

16%

3%

13%

26%

13%

12%

7%

Depostis from banks

CDs and CPs

ABCPs

Public benchmark MTNs

Privateley place MTNs

Covered bonds / ABS

Suborindated liabilities

Other

10%

14%

8%

8%

4%

8%

21%

27%

1 month

> 1 mth but <

3 mths

> 3 mths but

6 mths

> 6 mths but

9 mths

> 9 mths but

12 mths

> 1 year but

2 years

> 2 years but

> 5 years

•

Overall stock of wholesale funding continues to fall as we

de-lever the balance sheet, with total wholesale funding

(excluding repurchase agreements) of £171bn as at

31 December 2014, a reduction of £69bn since 2012

(31 December 2013: £186bn)

£75bn matures in less than one year, while £17bn

matures within one month (31 December 2013: £82bn

and £20bn respectively)

•

£15bn of term funding (net of early redemptions) issued in

2014. Activity includes:

£8bn public benchmark senior unsecured debt, £2bn

of which issued by Barclays PLC

£0.8bn Tier 2 deal issued by Barclays PLC

£1.5bn of Covered bonds, as well as £3bn US and UK

credit card backed securities, issued by Barclays

Bank PLC

<

<

<

<

>

<

1

5 years

1

•

We have £23bn of term funding maturing 2015 and £13bn

maturing in 2016

•

We expect to issue a gross amount of £10-15bn in 2015

across public and private senior unsecured, secured and

subordinated debt and to maintain a stable and diverse

funding base by type, currency and distribution channel

<

–

–

–

– |

Asset quality

PERFORMANCE

LIQUIDITY &

ASSET QUALITY

CREDIT RATING

APPENDIX

LEVERAGE

CAPITAL &

OVERVIEW

FUNDING |

|

Continued strong asset quality

1

Africa Banking impairment was down 14% on a constant currency basis | •

Credit impairment charges improved 8% to £2bn, reflecting

lower impairments in PCB and Africa Banking

•

PCB benefitted from the improving economic environment in

the UK, particularly for Corporate which benefited from one-off

releases and lower defaults from large UK Corporate clients

•

Africa Banking saw improvements in the South Africa

mortgages portfolio and business banking

•

Barclaycard increased 8% due to asset growth and enhanced

coverage for forbearance. Delinquency rates remained broadly

stable and the loan loss rate reduced 24bps to 308bps

Barclays Full Year 2014 Fixed Income Investor Presentation

24

2,171

2,000

FY13

FY14

8%

Impairment charge (£m)

Highlights

Personal and Corporate Banking

Barclaycard

Africa Banking

1

Impairment (£m)

22%

621

482

FY13

FY14

(8%)

27%

1,096

1,183

FY13

FY14

479

349

FY13

FY14

PERFORMANCE

LIQUIDITY &

ASSET QUALITY

CREDIT RATING

APPENDIX

CAPITAL &

OVERVIEW

LEVERAGE

FUNDING |

|

CREDIT RATING

APPENDIX

PERFORMANCE

OVERVIEW

LIQUIDITY &

FUNDING

CAPITAL &

LEVERAGE

•

Declining Loan Loss Rate (LLR) trend

across the Group reflecting Barclays’

well-managed and conservative risk

profile

•

The Group LLR of 46bps remains

significantly below the longer term

average of 88bps

•

Group impairment charges improved

29% year-on-year to £2.2bn

(31 December 2013: £3.1bn), principally

reflecting lower charges in Personal &

Corporate Banking, Africa Banking and

Non-Core

•

Group LLRs declining in both retail and

wholesale in line with improving macro

economic conditions

Retail loan loss rate (bps)

Group impairment improved 29%, with positive trends

across businesses

LLR

Annualised impairment charge

Gross loans and advances

Wholesale loan loss rate (bps)

Highlights

25

ASSET QUALITY

Barclays Full Year 2014 Fixed Income Investor Presentation

25

180

332

94

78

91

18

138

308

85

75

84

Personal &

Corporate

Banking

Africa

Banking

Barclaycard

Core

Barclays

Non-Core

Group

Dec-13

Dec-14

(3)

34

56

16

133

37

(0)

00

00

00

00

00

Investment

Bank

Personal &

Corporate

Banking

Africa Banking

Core

Barclays

Non-Core

Group

Dec-13

Dec-14 |

|

ASSET QUALITY

CREDIT RATING

APPENDIX

PERFORMANCE

OVERVIEW

LIQUIDITY &

FUNDING

CAPITAL &

LEVERAGE

•

The vast majority of the exposures to Spain have been

disposed of as of 2 January 2015

•

Exposure to Spain, Italy, Portugal and Ireland reduced

further, down 18% to £43.2bn in December 2014 in line

with Non-Core strategy

•

£1bn of outstanding ECB LTRO as at 31 December 2014

•

Local net funding mismatches decreased

Portugal: €1.9bn funding gap (2013: €3bn)

Italy: €9.9bn funding gap (2013: €11.6bn)

•

We continue to explore options to exit our other

European retail and corporate exposures or materially

reduce the capital they consume

Reduced exposure to Eurozone periphery

Exposures by geography (£bn)¹

Exposures by asset class (£bn)

59.2

53.1

43.2

59.0

52.8

Key Messages

43.2

26

1

Net on balance sheet|

Barclays Full Year 2014 Fixed Income Investor Presentation

5.4

2.2

2.0

5.7

6.5

17.7

9.3

7.1

4.3

32.5

31.4

16.6

6.3

5.9

2.6

2012

2013

2014

Sovereign

Financial institutions

Corporate

Residential mortgages

Other retail lending

23.5

19.2

15.6

22.7

20.6

18.0

7.9

6.3

4.8

4.9

6.7

4.8

2012

2013

2014

Spain

Italy

Portugal

Ireland

ASSET QUALITY |

|

CREDIT RATING

APPENDIX

PERFORMANCE

OVERVIEW

LIQUIDITY &

FUNDING

CAPITAL &

LEVERAGE

Managing country exposures

Passing stress tests –

stressed CET1 ratios

Risk –

Minimising potential headwinds

Managing sector exposures (£bn)

•

No material operations in Russia,

with <£2bn exposure in relation to

financing and trading counterparties

•

Barclays has always maintained internal stress tests

•

Barclays passed both the PRA and EBA stress tests in 2014,

with stressed CET1 ratios ahead of UK peers

•

Under the PRA test, the 7.0% represents pre-management

actions, and significantly above the 4.5% minimum threshold

•

Total net exposure of £27m in Greece

•

Investment grade makes up c.90%

of limits in oil and gas

1

Total on and off balance sheet |

1

1

Barclays Full Year 2014 Fixed Income Investor Presentation

27

ASSET QUALITY

All other

exposure

Oil majors

Exploration

and

production

Midstream

(pipelines)

Refining

Oilfield

services

PRA stress test

EBA stress test

Barclays CET1

stressed ratio

UK Peers CET1

stressed ratio

Oil and gas |

|