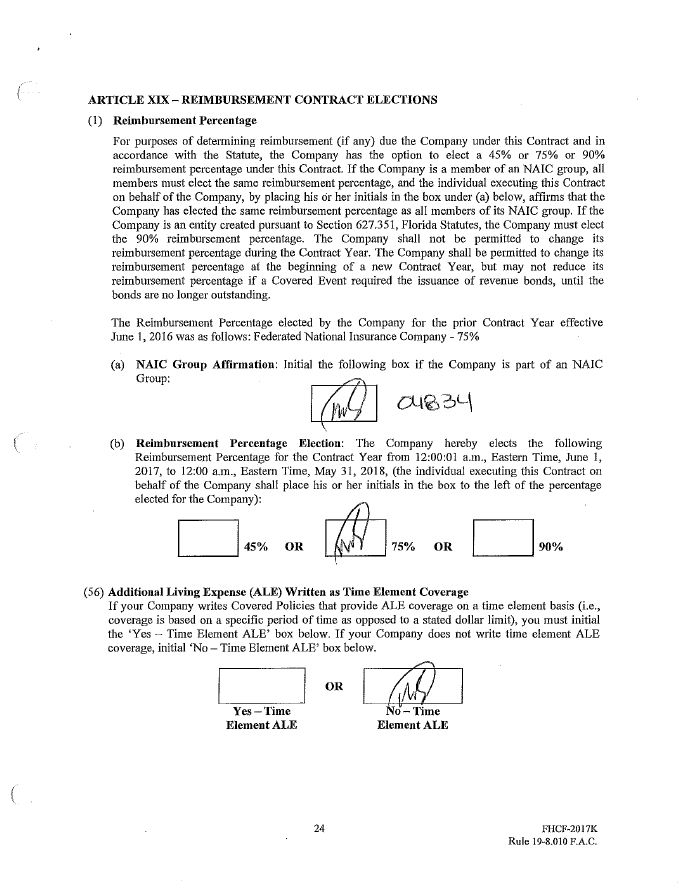

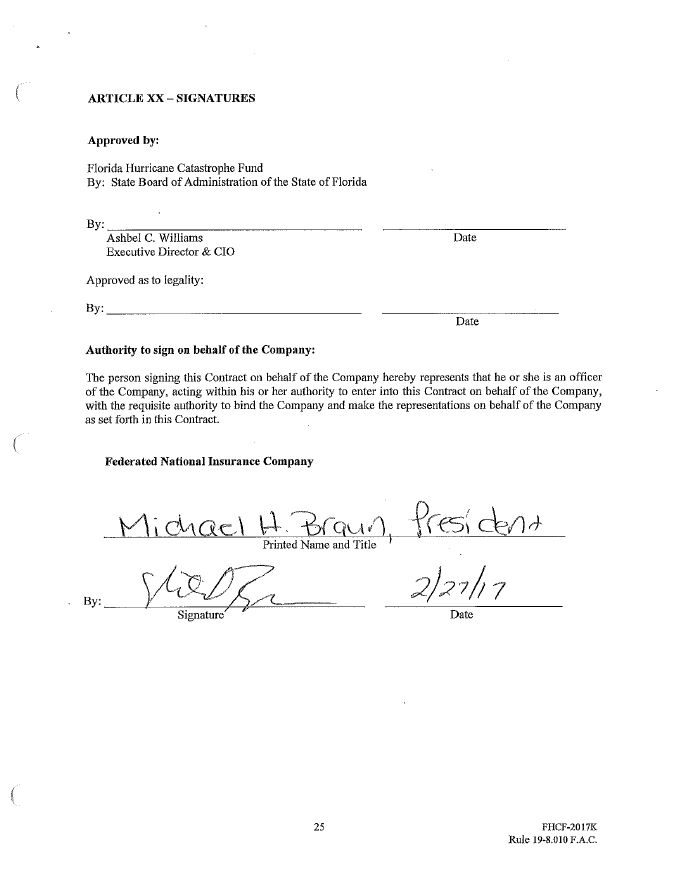

Contract

Exhibit 10.1

STATE BOARD OF ADMINISTRATION OF FLORIDA 1801 HERMITAGE XXXXXXXXXXXXXXXXXXXX, XXXXXXX 00000 (850) 488-4406 POST OFFICE BOX 13300 32317-3300 reimbursement contract Effective: June 1,2017 (Contract) between xxx xxxxx GOVERNOR CHAIR XXXX XXXXXXX CHIEF FINANCIAL OFFICER XXX XXXXX ATTORNEY GENERAL ASH WILLIAMSexecutive DIRECTOR & CIO FEDERATED NATIONAL INSURANCE COMPANY (Company) XXXX # 00000 and THE STATE BOARD OF ADMINISTRATION OF THE STATE OF FLORIDA (SBA)WHICH ADMINISTERS THE FLORIDA HURRICANE CATASTROPHE FUND (FHCF) PREAMBLE The Legislature of the State of Florida has enacted Section 215.555, Florida Statutes (Statute), whichdirects the SBA to administer the FHCF. This Contract, consisting of the principal document entitledReimbursement Contract, addressing the mandatory FHCF coverage, and Addenda, is subject to theStatute and to any administrative rale adopted pursuant thereto, and is not intended to be in conflicttherewith. All provisions in the principal document are equally applicable to each Addendum unlessspecifically superseded by one of the Addenda. In consideration of the promises set forth in this Contract, the parties agree as follows: ARTICLE I - SCOPE OF AGREEMENT As a condition precedent to the SBA’s obligations under this Contract, the Company, an AuthorizedInsurer or an entity writing Covered Policies under Section 627.351, Florida Statutes, in the State ofFlorida, shall report to the SBA in a specified format the business it writes which is described in thisContract as Covered Policies. The terms of this Contract shall determine the rights and obligations of the parties. This Contract providesreimbursement to the Company under certain circumstances, as described herein, and does not provide orextend insurance or reinsurance coverage to any person, firm, corporation or other entity. The SBA shallreimburse the Company for its Ultimate Net Loss on Covered Policies, which were in force and in effectat the time of the Covered Event(s) causing the Loss, in excess of the Company’s Retention as a result ofeach Covered Event commencing during the Contract Vear, to the extent funds are available, all ashereinafter defined. 1 FHCF-20I7K Rule 19-S.OIO F.A.C.

ARTICLE II - PARTIES TO THE CONTRACT This Contract is solely between the Company and the SBA which administers the FHCF. In no instanceshall any insured of the Company or any claimant against an insured of the Company, or any other thirdparty, have any rights under this Contract, except as provided in Article XV. The SBA will only disbursefunds to die Company, except as provided for in Article XV, The Company shall not, without the priorapproval of the Office of Insurance Regulation, sell, assign, or transfer to any third party, in return for afee or other consideration any sums the FHCF pays under diis Contract or the right to receive such sums. ARTICLE III-TERM (1) The term of this Contract shall apply to Losses from Covered Events which commence during the period from 12:00:01 a.m., Eastern Time, June 1, 2017, to12:00 midnight. Eastern Time, May 31, 2018 (Contract Year). Pursuant to the terms of this Contract, the SBA shall not be liable for Losses from Covered Events which commence after the effective time and date of expiration or termination. Should this Contract expire or terminate while a Covered Event is in progress, the SBA shall be responsible for such Covered Event in progress in the same manner and to the same extent it would have been responsible had die Contract expired the day following die conclusion of the Covered Event in progress. (2) The Company is required to designate a coverage level, make die required selections, and return this fully executed Contract to the FHCF Administrator so that the Contract is received by the FHCF Administrator no later than 5 p.m,, Central Time, March 1, 2017. Failure to do so shall result in the Company’s coverage level under this Contract being deemed as follows; (a) For Companies that are a member of a National Association of Insurance Commissioners (NAIC) group, die same coverage level selected by the other Companies of the same NAIC group shall be deemed. If executed Contracts for none of the members of an NAIC group have been received by the FHCF Administrator, the coverage level from the prior Contract Year shall be deemed. (b) For Companies that are not a member of an NAIC group under which other Companies are active participants in the FHCF, the coverage level from the prior Contract Year shall be deemed, (c) For New Participants, as that term is defined in Article V(21), that are a member of an NAIC group, the same coverage level selected by the other Companies of the same NAIC group shall be deemed. (d) For New Participants that are not a member of an NAIC group under which odier Companies are active participants in the FHCF, the 45%, 75% or 90% coverage levels may be selected providing that the FHCF Administrator receives executed Contracts within 30 calendar days of the effective date of the first Covered Policy, otherwise, the 45% coverage level shall be deemed. (3) Failure by the Company to meet the requirements of this Article may result in referral to the Office of Insurance Regulation. ARTICLE IV - LIABILITY OF THE FHCF (1) The SBA shall reimburse the Company, with respect to each Covered Event commencing during the Contract Year for the “Reimbursement Percentage” elected, this percentage times the amount of Ultimate Net Loss paid by the Company in excess of the Company’s Retention, as adjusted pursuant to Article V(28), plus 5% of the reimbursed Losses for Loss Adjustment Expense Reimbursement, (2) The Reimbursement Percentage will be 45% or 75% or 90%, at the Company’s option as elected under Article XIX. FHCF-2017K 2 Rule 19-8.010 F.A.C.

(3) The aggregate liability of the FHCF with respect to all Reimbursement Contracts covering this Contract Year shall not exceed die limit set forth under Section 215.555(4)(c)L, Florida Statutes. Forspecifics regarding reimbursement calculations, see section (3)(c) of Article X. (4) Upon the occurrence of a Covered Event, the SB A shall evaluate the potential Losses to the FHCF and the FHCF’s capacity at the time of the event. The initial Projected Payout Multiple used toreimburse the Company for its Losses shall not exceed the Projected Payout Multiple as calculatedbased on the capacity needed to provide the FHCF’s coverage. If it appears that the EstimatedClaims-Paying Capacity may be exceeded, the SB A shall reduce the projected payout factors ormultiples for determining each participating insurer’s projected payout uniformly among all insurersto reflect the Estimated Claims-Paying Capacity. (5) Reimbursement amounts shall not be reduced by reinsurance paid or payable to the Company from other sources. Once die Company’s limit of coverage has been exhausted, the Company will not beentitled to further reimbursements. (6) After the end of the calendar year, the SB A shall notify insurers of die estimated Borrowing Capacity and the Balance of the Fund as of December 31. In May and October of each year, the SBAshall publish in die Florida Administrative Register a statement of the FHCF’s estimated BorrowingCapacity, Estimated Claims-Paying Capacity, and die projected Balance of the Fund as ofDecember 31. (7) The obligation of the SBA with respect to all Contracts covering a particular Contract Year shall not exceed the Balance of the Fund as of December 31 of that Contract Year, together witii themaximum amount the SBA is able to raise through the issuance of revenue bonds or through othermeans available to the SBA under Section 215,555, Florida Statutes, up to the limit in accordancewith Section 23 5.555(4)(c)l. and (6), Florida Statutes. The obligations and the liability of the SBAare more fully described in Rule 19-8,013, Florida Administrative Code (F.A.C.). ARTICLE V - DEFINITIONS (1) Actual Claims-Paying Capacity of the FHCF This term means the sum of the Balance of the Fund as of December 31 of a Contract Year, plus anyreinsurance purchased by the FHCF, plus the amount the SBA is able to raise through the issuance ofrevenue bonds, or through other means available by law to the SBA, up to the limit in accordancewith Section 215.555(4)(c)l. and (6), Florida Statutes. (2) Aetna daily Indicated This term means, with respect to Premiums paid by Companies for reimbursement provided by theFHCF, an amount determined in accordance with the definition provided in Section 215.555(2)(a),Florida Statutes. (3) Additional Living Expense (ALE) ALE Losses covered by the FHCF are not to exceed 40 percent of the insured value of a ResidentialStructure or its contents based on the coverage provided in the policy. Fair rental value, loss of rents,or business interruption losses are not covered by the FHCF. (4) Administrator This term means the entity with which the SBA contracts to perform administrative tasks associatedwith the operations of the FHCF. The Administrator is Paragon Strategic Solutions Inc,,8200Tower, 0000 Xxxx 00xx Xxxxxx, Xxxxx 0000, Xxxxxxxxxxx, Xxxxxxxxx 00000, The telephone number is(800) 000-0000, and the facsimile number is (000) 000-0000. FHCF-2017K 3 Rule 19-8.010 F.A.C.

(5) Authorized Insurer This term is defined in Section 624.09(1), Florida Statutes, (6) Borrowing Capacity This term means the amount of funds which are able to be raised by the issuance of revenue bonds orthrough other financing mechanisms, less bond issuance expenses and reserves. (7) Citizens Property Insurance Corporation (Citizens) This term means Citizens Property Insurance Corporation as created under Section 627.351(6),Florida Statutes, For tire purposes of(he FHCF, Citizens Property Insurance Corporationincorporates two accounts, (a) the coastal account and (b) the personal lines and commercial lines accounts. Each account is treated by the FHCF as if it were a separate participating insurer with itsown reportable exposures, Reimbursement Premium, Retention, and Ultimate Net Loss. (8) Contract This term means this Reimbursement Contract for the current Contract Year. (9) Covered Event This term means any one storm declared to be a hurricane by the National Hurricane Center whichcauses insured losses in Florida. A Covered Event begins when a hurricane causes damage in Floridawhile it is a hurricane and continues throughout any subsequent downgrades in storm status by dieNational Hurricane Center regardless of whether the hurricane makes landfall. Any storm, includinga tropical storm, which does not become a hurricane is not a Covered Event. (10)Covered Policy or Covered Policies (a) Covered Policy, as defined in Section 215.555(2)(c), Florida Statutes, is further clarified to mean only that portion of a binder, policy or contract of insurance that insures real or personal property located in the State of Florida to the extent such policy insures a Residential Structure or the contents of a Residential Structure, located in the State of Florida. (b) Due to the specialized nature of the definition of Covered Policies, Covered Policies are not limited to only one line of business in the Company’s annual statement required to he filed by Section624.424, Florida Statutes. Instead, Covered Policies are found in several lines of business on the Company’s annual statement. Covered Policies will at a minimum be reported in the Company’s statutory annual statement as: 1. Fire 2. Allied Lines 3. Farmowners Multiple Peril 4. Homeowners Multiple Peril 5. Commercial Multiple Peril (non liability portion, covering condominiums and apartments) 6. Inland Marine Note that where particular insurance exposures, e.g., mobile homes, are reported on an annualstatement is not dispositive of whether or not the exposure is a Covered Policy. (c) This definition applies only to the first-party property section of a policy pertaining strictly to the structure, its contents, appurtenant structures, or ALE coverage. (d) Covered Policy also includes any collateral protection insurance policy covering personal residences which protects both the borrower’s and the lender’s financial interest, in an amount at least equal to the coverage for the dwelling in place under the lapsed homeowner’s policy, if such policy can be accurately reported as required in Section 215.555(5), Florida Statutes. A Company will be deemed to be able to accurately report data if the required data, as specified in the Premium Formula adopted in Section 215,555(5), Florida Statutes, is available, (e) See Article VI for specific exclusions. FHCF-2017K 4 Rule 19-8.010 F.A.C.

(11) Deductible Buy-Back Policy This term means a specific policy that provides coverage to a policyholder for some portion of thepolicyholder’s deductible under a policy issued by another insurer. (12) Estimated Claims-Paying Capacity of the FHCF This term means the sum of the projected Balance of the Fund as of December 31 of a ContractYear, plus any reinsurance purchased by the FHCF, plus the most recent estimate of the BorrowingCapacity of the FHCF, determined pursuant to Section 215.555(4)(c), Florida Statutes. (13) Excess Policy This term, for the purposes of this Contract, means a policy that provides insurance protection forlarge commercial property risks and that provides a layer of coverage above a primary layer (whichis insured by a different insurer) that acts much the same as a very large deductible. (14) Florid a Department of Financial Services This term means the Florida regulatory agency, created pursuant to Section 20.121, FloridaStatutes, which is charged with regulating the Florida insurance market and administering theFlorida Insurance Code. (15) Florida Insurance Code This term means those chapters identified in Section 624.01, Florida Statutes, which are designatedas the Florida Insurance Code. (16) Formula or the Premium Formula This term means tire Formula approved by the SB A for the purpose of determining the ActuariallyIndicated Premium to be paid to the FHCF. The Premium Formula is defined as an approach ormethodology which leads to the creation of premium rates. The Formula shall, pursuant to Section215.555(5)(b), Florida Statutes, include a cash build-up factor in the amount specified therein. (17) Fund Balance or Balance of the Fund as of December 31 These terms mean the amount of assets available to pay claims, not including any bondingproceeds, resulting from Covered Events which occurred during the Contract Year. (18) Insurer Group For purposes of the coverage option election in Section 2I5.555(4)(b), Florida Statutes, InsurerGroup means the group designation assigned by the National Association of InsuranceCommissioners (NA1C) for purposes of filing consolidated financial statements. A Company is amember of a group as designated by the NAIC until such Company is assigned another groupdesignation or is no longer a member of a group recognized by the NAIC. (19) Loss “Loss” or “Losses” means incurred losses under a Covered Policy from a Covered Event, includingAdditional Living Expenses not to exceed 40 percent of the insured value of a Residential Structureor its contents and amounts paid as fees on behalf of or inuring to the benefit of a policyholder. “Loss” excludes allocated or unallocated loss adjustment expenses and also excludes any item forwhich this Contract does not provide reimbursement pursuant to the exclusions in Article VI, (20) Loss Adjustment Expense Reimbursement (a) Loss Adjustment Expense Reimbursement shall be 5% of the reimbursed Losses under this Contract as provided in Article TV, pursuant to Section 215.555(4)(b)l., Florida Statutes. (b) The 5% Loss Adjustment Expense Reimbursement is included in the total Payout Multiple applied to each Company. (21) New Participants) This term means all Companies which begin writing Covered Policies on or after the beginning ofthe Contract Year. A Company that removes exposure from Citizens pursuant to an assumptionagreement effective on or after June 1 and had written no other Covered Policies before June 1 isalso considered a New Participant, FHCF-20I7K 5 Rule 19-8.010 F.A.C.

(22) Office of Insurance Regulation This term means that office within the Department of Financial Seivices and which was created inSection 20.121(3), Florida Statutes. (23) Payout Multiple This term means the multiple as calculated in accordance with Section 215.555(4) (c), FloridaStatutes, which is derived by dividing the single season Claims-Paying Capacity of the FHCF bythe total aggregate industry Reimbursement Premium for the FHCF for the Contract Year billed asof December 31 of the Contact Year, Die final Payout Multiple is determined onceReimbursement Premiums have been billed as of December 31 and the amount of bond proceedshas been determined. (24) Premium This term means the same as Reimbursement Premium. (25) Projected Payout Multiple The Projected Payout Multiple is used to calculate a Company’s projected payout pursuant toSection 215,555(4)(d)2., Florida Statutes. The Projected Payout Multiple is derived by dividing theestimated single season Claims-Paying Capacity of the FHCF by the estimated total aggregateindustry Reimbursement Premium for the FHCF for the Contract Year. The Company’sReimbursement Premium as paid to the SB A for the Contract Year is multiplied by the ProjectedPayout Multiple to estimate the Company’s coverage from the FHCF for the Contract Year. (26) Reimbursement Premium This term means the Premium determined by multiplying each $1,000 of insured value reported bythe Company in accordance with Section 215.555(5)(b), Florida Statutes, by the rate as derivedfrom the Premium Formula, as described in Rule 19-8.028, F.A.C. (27) Residential Structures This term means units or buildings used exclusively or predominantly for dwelling or habitationaloccupancies, including the primary structure and appurtenant structures insured under the samepolicy and any other structures covered under endorsements associated with a policy covering aresidential structure. For the purpose of this Contract, a single structure which includes a mix ofcommercial habitational and commercial non-habitational occupancies, and which is insured undera commercial policy, is considered a Residential Structure if 50% or more of the total insured valueof the structure is used for habitational occupancies. Covered Residential Structures do not includeany structures listed under Article VI. (28) Retention This term means the amount of Losses from a Covered Event which must be incurred by theCompany before it is eligible for reimbursement from the FHCF. (a) When the Company incurs Losses from one or two Covered Events during the Contract Year, the Company’s full Retention shall be applied to each of the Covered Events. (b) When the Company incurs Losses from more than two Covered Events during tire Contract Year-, the Company’s full Retention shall be applied to each of the two Covered Events causing the largest Losses for the Company. For each other Covered Event resulting in Losses, the Company’s Retention shall be reduced to one-third of its full Retention. 1. All reimbursement of Losses for each Covered Event shall be based on the Company’s full Retention until December 31 of the Contract Year. Adjustments to reflect a reduction to one-third of die full Retention shall be made on or after January1 of the Contract Year provided the Company reports its Losses as specified in this Contract. 2. Adjustments to the Company’s Retention shall be based upon its paid and outstanding Losses as reported on the Company’s Proof of Loss Reports, but shall not include incurred but not reported Losses. The Company’s Proof of Loss Reports shall be used to determine FHCF-2017K 6 Rule 19-8.010 F.A.C.

which Covered Events constitute die Company’s two largest Covered Events. After thisinitial determination, any subsequent adjustments shall be made quarterly by the SB A onlyif the Proof of Loss Reports reveal that loss development patterns have resulted in a change in the order of Covered Events entitled to the reduction to one-third of the full Retention, (c)The Company’s full Retention is established in accordance with the provisions of Section 215.555(2)(e), Florida Statutes, and shall be determined by multiplying the Retention Multiple by the Company’s Reimbursement Premium for the Contract Year, (29) Retention Multiple (a) The Retention Multiple is applied to the Company’s Reimbursement Premium to determine the Company’s Retention. The Retention Multiple for the 2017/2018 Contract Year shall be equal to $4.5 billion, adjusted based upon the reported exposure for the 2015/203 6 Contract Year to reflect the percentage growth in exposure to the FF1CF since 2004, divided by the estimated total industry Reimbursement Premium at the 90% reimbursement percentage level for the Contract Year as determined by the SB A. (b) The Retention Multiple shall be adjusted to reflect the reimbursement percentage elected by the Company under this Contract as follows: 1. If the Company elects a 90% reimbursement percentage, the adjusted Retention Multiple is 100% of the amount determined under (29) (a) above; 2. If the Company elects a 75% reimbursement percentage, the adjusted Retention Multiple is 120% of the amount determined under (29) (a) above; or 3. If the Company elects a 45% reimbursement percentage, the adjusted Retention Multiple is 200% of the amount determined under (29) (a) above. (30) Ultimate Net Loss (a) This term means all Losses under Covered Policies in force at the time of a Covered Event prior to the application of the Company’s Retention and reimbursement percentage, and excluding loss adjustment expense and any exclusions under Article VI. (b) The Company’s Ultimate Net Loss shall be determined in accordance with the deductible level as specified under the policy sustaining the Loss without talcing into consideration any deductible discounts or deductible waivers. (c) Salvages and all other recoveries, excluding reinsurance recoveries, shall be first deducted from such Loss to arrive at the amount of liability attaching hereunder, (d) All salvages, recoveries or payments recovered or received subsequent to a Loss settlement under this Contract shall be applied as if recovered or received prior to the aforesaid settlement and all necessary adjustments shall be made by the parties hereto. (e) Nothing in this clause shall be construed to mean that Losses under this Contract are not recoverable until the Company’s Ultimate Net Loss has been ascertained. (f) The SBA shall be subrogated to the rights of the Company to the extent of its reimbursement of the Company. The Company agrees to assist and cooperate with the SBA in all respects as regards such subrogation. The Company further agrees to undertake such actions as may be necessary to enforce its rights of salvage and subrogation, and its rights, if any, against other insurers as respects any claim, loss, or payment arising out of a Covered Event. ARTICLE VI - EXCLUSIONS This Contract does not provide reimbursement for: (1) Any losses not defined as being within the scope of a Covered Policy. (2) Any policy which excludes wind or hurricane coverage. FHCF-2017K 7 Rule 19-8.010 F.A.C.

(' (3) Any Excess Policy or Deductible Buy-Back Policy that requires individual ratemaking, as determined by the FHCF. (4) (a) Any policy for Residential Structures that provides a layer of coverage underneath an Excess Policy issued by a different insurer; (b) Any policy providing a layer of windstorm or hurricane coverage for a particular structure above or below a layer of windstorm or hurricane coverage under a separate policy issued by a different insurer, or any other circumstance in which two or more insurers provide primarywindstorm or hurricane coverage for a single structure using separate policy forms; (c) Any other policy providing a layer of windstorm or hurricane coverage for a particular- structure below a layer of self-insured windstorm or hurricane coverage for the same structure; or (d) The exclusions in this subsection do not apply to primary quota share policies written by Citizens Property Insurance Corporation under Section 627.35 l(6)(c)2,, Florida Statutes. (5) Any liability of the Company attributable to losses for fair rental value, loss of rent or rental income, or business interruption. (6) Any collateral protection policy that does not meet the definition of Covered Policy as defined in Article V(10)(d). (7) Any reinsurance assumed by the Company. (8) Any exposure for hotels, motels, timeshares, shelters, camps, retreats, and any other rental properly used solely for commercial purposes. (9) Any exposure for homeowner associations if no habitational structures are insured under the policy. (10)Any exposure for homes and condominium structures or units that are non-owner occupied and rented for 6 or more rental periods by different parties during the course of a 12-month period. (11)Commercial healthcare facilities and nursing homes; however, a nursing home which is an integral part of a retirement community consisting primarily of habitational structures that are not nursinghomes will not be subject to this exclusion. (12)Any exposure under commercial policies covering only appurtenant structures or structures that do not function as a habitational structure (e.g., a policy covering only the pool of an apartment complex). (13)Policies covering only Additional Living Expense. (14)Any exposure for barns or barns with apartments or living quarters. (15)Any exposure for builders risk coverage or new Residential Structures still under construction. (16)Any exposure for recreational vehicles, golf carts, or boats (including boat related equipment) requiring licensing and written on a separate policy or endorsement. (17)Any liability of the Company for extra contractual obligations or liabilities in excess of original policy limits. This exclusion includes, but is not limited to, amounts paid as bad faith awards, punitive damages awards, or other court-imposed fines, sanctions, or penalties; or other amounts inexcess of the coverage limits under the Covered Policy. (18) Any losses paid in excess of a policy’s hurricane limit in force at the time of each Covered Event, including individual coverage limits (i.e., building, appurtenant structures, contents, and additional living expense), or other amounts paid as the result of a voluntary expansion of coverage by theinsurer, including, but not limited to, a discount on or waiver of an applicable deductible. Thisexclusion includes overpayments of a specific individual coverage limit even if total payments undertire policy are within the aggregate policy limit. (19) Any losses paid under a policy for Additional Living Expense, written as a time element coverage, in excess of the Additional Living Expense exposure reported for that policy under the Data Call for the applicable Contract Year (unless policy limits have changed effective after June 30 of theContract Year). FHCF-2017K 8 Rule 19-8.010 F.A.C.

(20) Any losses which the Company’s claims files do not adequately support. Claim file support shall be deemed adequate if in compliance with the Records Retention Requirements outlined on the Form FHCF-L1B (Proof of Loss Report) applicable to the Contract Year. (21) Any exposure for, or amounts paid to reimburse a policyholder for, condominium association loss assessments or under similar coverages for contractual liabilities, (22) Losses in excess of the sum of the Balance of the Fund as of December 31 of the Contract Year and the amount the SB A is able to raise through the issuance of revenue bonds or by the use of other financing mechanisms, up to the limit pursuant to Section 215,555(4)(c), Florida Statutes. (23) Any liability assumed by the Company from Pools, Associations, and Syndicates. Exception; Covered Policies assumed from Citizens under the terms and conditions of an executed assumption agreement between the Authorized Insurer and Citizens are covered by this Contract. (24) All liability of the Company arising by contract, operation of law, or otherwise, from its participation or membership, whether voluntary or involuntary, in any insolvency fund.“Insolvency fund” includes any guaranty fund, insolvency fund, plan, pool, association, fund or other arrangement, howsoever denominated, established or governed, which provides for any assessment of or payment or assumption by the Company of part or all of any claim, debt, charge, fee, or other obligation of an insurer, or its successors or assigns, which has been declared by any competent authority to be insolvent, or which is otherwise deemed unable to meet any claim, debt, charge, fee or other obligation in whole or in part, (25) Property losses that are proximately caused by any peril other than a Covered Event, including, but not limited to, fire, theft, flood or rising water, or windstorm that does not constitute a Covered Event, or any liability of the Company for loss or damage caused by or resulting from nuclear reaction, nuclear radiation, or radioactive contamination from any cause, whether direct or indirect, proximate or remote, and regardless of any other cause or event contributing concurrently or in any other sequence to the loss. (26) The FHCF does not provide coverage for water damage which is generally excluded under property insurance contracts and has been defined to mean flood, surface water, waves, tidal water, overflow of a body of water, storm surge, or spray from any of these, whether or not driven by wind, (27) Policies and endorsements predominantly covering Specialized Fine Arts Risks or collectible types of property meeting the following requirements: (a) A policy or endorsement predominantly covering Specialized Fine Arts Risks and not covering any Residential Structure if it meets the description in subparagraph1 and if the conditions in subparagraph 2 are met. 1. For purposes of this exemption, a Specialized Fine Arts Risk policy or endorsement is a policy or endorsement that: a. Insures works of art, of rarity, or of historic value, such as paintings, works on paper, etchings, art glass windows, pictures, statuary, sculptures, tapestries, antique furniture, antique silver, antique rugs, rare books or manuscripts, jewelry, or other similar items; b. Charges a minimum premium of $500; and c. Insures scheduled items valued, in the aggregate, at no less than $100,000. 2. The insurer offers specialized loss prevention services or other collector services designed to prevent or minimize loss, or, to value or inventory the Specialized Fine Arts for insurance purposes, such as: a. Collection risk assessments; b. Fire and security loss prevention; c. Warehouse inspections to protect items stored off-site; d. Assistance with collection inventory management; or FHCF-2017K 9 Rule 19-8.010 F.A.C.

e. Collection valuation reviews. (b) A policy form or endorsement generally used by the Company to cover personal property which could include property of a collectible nature, including fine arts, as further described in this paragraph, either on a scheduled basis or written under a blanket limit, and not covering anything other than personal property. All such policy forms or endorsements are subject to the exclusion provided in this paragraph when the policy or endorsement limit equals or exceeds $500,000. Generally such collectible property has unusually high values due to its investible, artistic, or unique intrinsic nature. The class of property covered under such a policy or endorsement represents an unusually high exposure value and such policy is intended to provide coverage for a class or classes of property that is not typical for the contents coverage under residential property insurance policies. In many cases property may be located at various locations either in or outside the state of Florida or the location of the property may change from time to time. The investment nature of such property distinguishes this type of exposure from the typical contents associated with a Covered Policy. (28) Any losses under liability coverages, (29) Any exposure for a condominium structure insured on a commercial policy in which more than 50% of the individual units are non-owner occupied and rented for 6 or more rental periods by different parties during tire course of a 12-month period. (30) Any structure used exclusively or predominantly for non-dwelling or non-habitational occupancies, ARTICLE VII - MANAGEMENT OF CLAIMS AND LOSSES The Company shall investigate and settle or defend ail claims and Losses. All payments of claims orLosses by the Company within the terms and limits of tire appropriate coverage parts of Covered Policiesshall be binding on the SBA, subject to tire terms of this Contract, including tire provisions in Article XIIIrelating to inspection of records and examinations. ARTICLE VIII -REIMBURSEMENT ADJUSTMENTS Section 215.555(4)(d) and (e), Florida Statutes, provides the SBA with tire right to seek the return ofexcess reimbursements which have been paid to the Company along with interest thereon. Excessreimbursements are those payments made to the Company by the SBA that are in excess of tireCompany’s coverage under the Contract Year. Excess reimbursements may result from adjustments to theProjected Payout Multiple or the Payout Multiple, incorrect exposure(Data Call) submissions orresubmissions, incorrect calculations of Reimbursement Premiums or Retentions, incorrect Proof of LossReports, incorrect calculation of reinsurance recoveries, or subsequent readjustment of policyholderclaims, including subrogation and salvage, or any combination of the foregoing. The Company will besent an invoice showing the due date for adjustments along with the interest due thereon through the duedate. The applicable interest rate for interest credits, and for interest charges for adjustments beyond theCompany’s control, will be the average rate earned by the SBA for the FHCF for the first four months ofthe Contract Year. The applicable interest rate for interest charges on excess reimbursements due toadjustments resulting from incorrect exposure submissions or Proof of Loss Reports will accrue at thisrate plus 5%. All interest will continue to accrue if not paid by the due date. ARTICLE IX - REIMBURSEMENT PREMIUM (1) The Company shall, in a timely manner, pay the SBA its Reimbursement Premium for the Contract Year. The Reimbursement Premium for the Contract Year shall be calculated in accordance with Section 215.555, Florida Statutes, with any rules promulgated thereunder, and with Article X(2). (2) The Company’s Reimbursement Premium is based on its June 30 exposure in accordance with Article X, except as provided for New Participants under Article X, and is not adjusted to reflect an FHCF-2017K 10 Rule 19-8.01 OF. A.C.

increase or decrease in exposure for Covered Policies effective after June 30 nor is theReimbursement Premium adjusted when the Company cancels policies or is liquidated or otherwisechanges its business status(merger, acquisition, or termination) or stops writing new business(continues in business with its policies in a runoff mode). Similarly, new business written after June 30 will not increase or decrease the Company’s FHCF Reimbursement Premium or impact its FHCFcoverage. FHCF Reimbursement Premiums are required of all Companies based on their writingCovered Policies in Florida as of June 30, and each Company’s FHCF coverage as based on thedefinition in Section 215.555(2)(m), Florida Statutes, shall exist for the entirety of the Contract Yearregardless of exposure changes, except as provided for New Participants under Article X. (3) Since the calculation of the Actuarially Indicated Premium assumes that the Companies will pay their Reimbursement Premiums timely, interest charges will accrue under the following circumstances. A Company may choose to estimate its own Premium installments. However, if the Company’s estimation is less than the provisional Premium billed, an interest charge will accrue on the difference between the estimated Premium and the final Premium. If a Company estimates its first installment, the Administrator shall xxxx that estimated Premium as the second installment as well, which will be considered as an estimate by the Company. No interest will accrue regarding any provisional Premium if paid as billed by the FHCF’s Administrator, except in the case of an estimated second installment as set forth in this Article. Also, if a Company makes an estimation that is higher than the provisional Premium billed but is less than the final Premium, interest will not accrue. If the Premium payment is not received from a Company when it is due, an interest charge will accrue on a daily basis until the payment is received. Interest will also accrue on Premiums resulting from submissions or resubmissions finalized after December I of the Contract Year. An interest credit will be applied for any Premium which is overpaid as either an estimate or as a provisional Premium. Interest shall not be credited past December1 of the Contract Year. The applicable interest rate for interest credits will be the average rate earned by the SBA for the FHCF for the first four months of the Contract Year, The applicable interest rate for interest charges will accrue at this rate plus 5%. ARTICLE X - REPORTS AND REMITTANCES (1) Exposures (a) If the Company writes Covered Policies before June 1 of the Contract Year, the Company shall report to the SBA, unless otherwise provided in Rule19-8.029, F.A.C., no later than the statutorily required date of September1 of the Contract Year, by ZIP Code or other limited geographical area as specified by the SBA, its insured values under Covered Policies as of June 30 of the Contract Year as outlined in the annual reporting of insured values form, FHCF- D1A (Data Call) adopted for the Contract Year under Rule 19-8.029, F.A.C., and other data or information in the format specified by the SBA. (b) If the Company first begins writing Covered Policies on or after June 1 but prior to December 1 of the Contract Year, the Company shall report to the SBA, no later than February 1 of the Contract Year, by ZIP Code or oilier limited geographical area as specified by the SBA, its insured values under Covered Policies as of November 30 of the Contract Year as outlined in the Supplemental Instructions for New Participants section of the Data Call adopted for the Contact Year under Rule19-8.029, F.A.C., and other data or information in the format specified by the SBA. (c) If the Company first begins writing Covered Policies on December 1 through and including May 31 of the Contact Year, the Company shall not report its exposure data for the Contact Year to the SBA. (d) The requirement that a report is due on a certain date means that the report shall be received by the SBA no later than 4 p.m. Eastern Time on the due date. If the applicable due date is a FHCF-2017K 11 Rule 19-8.010 F.A.C.

Saturday, Sunday or legal holiday, then the actual due date will he the day immediatelyfollowing the applicable due date which is not a Saturday, Sunday or legal holiday. Forpurposes of tire timeliness of the submission, neither the United States Postal Service postmarknor a postage meter date is in any way determinative. Reports sent to tire FHCF Administrator-in Minneapolis, Minnesota, will be returned to the sender. Reports not in the physicalpossession of the SBA by 4 p.m.. Eastern Time, on the applicable due date are late. (2) Reimbursement Premium (a) If the Company writes Covered Policies before June 1 of the Contract Year, the Company shall pay the FHCF its Reimbursement Premium in installments due on or before August1, October 1, and December 1 of the Contract Year- in amounts to be determined by the FHCF. However, if the Company’s Reimbursement Premium for the prior Contract Year was less than $5,000, the Company’s full provisional Reimbursement Premium, in an amount equal to the Reimbursement Premium paid in the prior year, shall be due in full on or before August 1 of the Contract Year. The Company will be invoiced for amounts due, if any, beyond the provisional Reimbursement Premium payment, on or before December 1 of the Contract Year. (b) If the Company is under administrative supervision, or if any control or oversight of the Company has been transferred through any legal or regulatory action to a state regulator or court appointed receiver or rehabilitator (referred to in the aggregate as “state action”): 1. The full annual provisional Reimbursement Premium as billed and any outstanding balances will be due and payable on August1, or the date that such State action occurs after- August I of the Contract Y ear. 2. Failure by such Company to pay the full annual provisional Reimbursement Premium as specified in1. above by the applicable due date(s) shall r esult in the 45% coverage level being deemed for the complete Contract Year regardless of the level selected for the Company through the execution of this Contract and regardless of whether a hurr icane event occurred or triggered coverage. 3. The provisions required in 1. and 2, above will not apply when the state regulator, receiver, or rehabilitator provides a letter of assurance to the FHCF that tire Company will have the resources and will pay the full Reimbursement Premium for the coverage level selected through the execution of this Contract. 4. When control or oversight has been transferred, in whole or in part, through a legal or regulatory action, tire controlling management of the Company shall specify by August I or as soon thereafter as possible (but not to exceed two weeks after any regulatory or legal action) in a letter to the FHCF as to the Company’s intentions to either pay the full FHCF Reimbursement Premium as specified in 1. above, to default to the 45% coverage being deemed as specified in 2. above, or to provide the assurances as specified in 3. above. (c) . A New Participant that first begins writing Covered Policies on or after June 1 but prior to December 1 of the Contr act Year shall pay the FHCF a provisional Reimbursement Premium of $1,000 upon execution of this Contract. The Administrator shall calculate the Company's actual Reimbursement Premium for the period based on its actual exposure as of November 30 of the Contract Year-, as reported on or before February 1 of the Contract Year. To recognize that New Participants have limited exposure during this period, the actual Premium as determined by processing the Company's exposure data shall then be divided in half, the provisional Premium shall be credited, and the resulting amount shall be the total Premium due for the Company for the remainder of the Contract Year. However, if that amount is less than $1,000, then the Company shall pay $1,000. The Premium payment is due no later than April 1 of the Contract Year, Tire Company’s Retention and coverage will be determined based on the total Premium due as calculated above. FHCF-20I7K 12 Rule 19-8.010 F.A.C.

(d) A New Participant that first begins writing Covered Policies on or after December 1 through and including May 31 of the Contract Year shall pay the FHCF a Reimbursement Premium of $1,000 upon execution of this Contract. (e) The requirement that the Reimbursement Premium is due on a certain date means that the Premium shall be remitted by wire transfer or ACH and shall have been credited to the I 'HCPs account at its bank in Tampa, Florida, as set out on the invoice sent to the Company, on the due date applicable to the particular installment. If the applicable due date is a Saturday, Sunday or legal holiday, then the actual due date will be the day immediately following the applicable due date which is not a Saturday, Sunday or legal holiday. Reimbursement Premiums not credited to the FHCF’s account on the applicable due date are late. (f) Except as required by Section 215.555(7)(c), Florida Statutes, or as described in the following sentence. Reimbursement Premiums, together with earnings thereon, received in a given Contract Year- will be used only to pay for Losses attributable to Covered Events occurring in drat Contract Year or for Losses attributable to Covered Events in subsequent Contract Years and will not be used to pay for past Losses or for debt service on post-event revenue bonds issued pursuant to Section2I5.555(6)(a)L, Florida Statutes. Reimbursement Premiums and earnings thereon may be used for payments relating to such revenue bonds in the event emergency assessments are insufficient. If Reimbursement Premiums or earnings thereon are used for debt service on post-event revenue bonds, then the amount of tire Reimbursement Premiums or earnings thereon so used shall be returned, without interest, to the Fund when emergency assessments or other legally available funds remain available after making payment relating to the post-event revenue bonds and any other purposes for which emergency assessments were levied. (3) Losses (a) In General Losses resulting from a Covered Event commencing during the Contract Year shall be reportedby the Company and reimbursed by the FHCF as provided herein and in accordance with theStatute, this Contract, and any rules adopted pursuant to the Statute. For a Companyparticipating in a quota share primary insurance agreements) with Citizens Property InsuranceCorporation Coastal Account, Citizens and the Company shall report only their respectiveportion of Losses under the quota share primary insurance agreements). Pursuant to Section215.555(4)(c), Florida Statutes, the SBA is obligated to pay for Losses not to exceed the ActualClaims-Paying Capacity of the FHCF, up to the limit in accordance with Section215.555(4)(c)l., Florida Statutes, for any one Contract Year. (b) Loss Reports 1. At the direction of the SBA, the Company shall report its projected Ultimate Net Loss from each Covered Event to provide information to the SBA in determining any potential liability for possible reimbursable Losses under the Contract on the Interim Loss Report, Form FHCF-L1A, adopted for the Contract Year under Rule 19-8.029, F.A.C. Interim Loss Reports {including subsequent Interim Loss Reports if required by the SBA) will be due in no less than fourteen days from the date of the notice from the SBA that such a report is required. 2. FHCF reimbursements will be issued based on Ultimate Net Loss information reported by the Company on the Proof of Loss Report, Form FHCF-L1B, adopted for the Contract Year under Rule 19-8,029, F.A.C. a. To qualify for reimbursement, the Proof of Loss Report must have the electronic signatures of two executive officers authorized by the Company to sign or submit the report, FHCF-2017K 13 Rule 19-8.010 F.A.C.

b. The Company must also submit a Detailed Claims Listing, Form FHCF-DCL, adopted for the Contract Year under Rule 19-8.029, F.A.C., at the same time it submits its first Proof of Loss Report for a specific Covered Event that qualifies the Company for reimbursement under that Covered Event, and should be prepared to supply a Detailed Claims Listing for any subsequent Proof of Loss Report upon request. c. While the Company may submit a Proof of Loss Report requesting reimbursement at any time following a Covered Event, hie Company shall submit a mandatory Proof of Loss Report for each Covered Event no earlier than December 1 and no later than December 31 of the Contract Year during which the Covered Event occurs using the most current data available, regardless of the amount of Ultimate Net Loss or the amount of reimbursements or advances already received. d. For the Proof of Loss Reports due by December 31 of hie Contract Year, and hie required subsequent quarterly and annual reports required under subparagraphs 3. and 4. below, the Company shall submit its Proof of Loss Reports by each quarter-end oryear-end using the most current data available. However, the date of such data shall notbe more than sixty days prior to the applicable quarter-end or year-end date. 3. Updated Proof of Loss Reports for each Covered Event are due quarterly thereafter until all Losses resulting from a Covered Event are fully discharged including any adjustments to such Losses due to salvage or other recoveries, or the Company has received its full coverage under the Contract Year in which the Covered Event occurred. Guidelines follow: a. Quarterly Proof of Loss Reports are due by March 31 from a Company whose Losses exceed, or are expected to exceed, 50% of its FHCF Retention for a specific Covered Event. b. Quarterly Proof of Loss Reports are due by June 30 from a Company whose Losses exceed, or are expected to exceed, 75% of its FHCF Retention for a specific Covered Event, c. Quarterly Proof of Loss Reports are due xxx September 30 and quar terly thereafter from a Company whose Losses exceed, or are expected to exceed, its FHCF Retention for a specific Covered Event. If the Company’s Retention must be recalculated as the result of an exposure resubmission,and if the recalculated Retention changes the FHCF’s reimbursement obligations, then theCompany shall submit additional Proof of Loss Reports for recalculation of the FHCF’sobligations. 4. Annually after December 31 of the Contract Year’, all Companies shall submit a mandatory year-end Proof of Loss Report for each Covered Event, as applicable, using the most current data available, accompanied by a Detailed Claims Listing, This Proof of Loss Report shall be filed no earlier than December 1 and no later than December 31 of each year and shall continue until the earlier of tire commutation process described in(3)(d) below or until all Losses resulting from the Covered Event are fully discharged including any adjustments to such Losses due to salvage or other recoveries. 5. The SB A, except as noted below, will determine and pay, within 30 days or as soon as practicable after receiving Proof of Loss Reports, the reimbursement amount due based on Losses paid by the Company to date and adjustments to this amount based on subsequent quarterly information. The adjustments to reimbursement amounts shall require the SB A to pay, or the Company to return, amounts reflecting the most recent determination of Losses, a. The SB A shall have tire right to consult with all relevant regulatory agencies to seek all relevant information, and shall consider any other factors deemed relevant, prior to the issuance of reimbursements. FHCF-20I7K 14 Rule 19-8.010 F.A.C.

b. The SBA shall require commercial self-insurance funds established under Section 624.462, Florida Statutes, to submit contractor receipts to support paid Losses reported on a Proof of Loss Report, and the SBA may hire an independent consultant to confirm Losses, prior to the issuance of reimbursements. c. The SBA shall have the right to conduct a loss examination prior to the issuance of any advances or reimbursements requested by Companies that have been placed under regulatory supervision by a State or where control has been transferred through any legal or regulatory proceeding to a state regulator or court appointed receiver or rehabilitates 6. All Proof of Loss Reports received will be compared with the FHCF’s exposure data to establish the facial reasonableness of the reports. The SBA may also review the results of current and prior Contract Year exposure and loss examinations to determine the reasonableness of the reported Losses. Except as noted in paragraph 4, above, Companies meeting these tests for reasonableness will be scheduled for reimbursement. Companies not meeting these tests for reasonableness will be handled on a case-by-case basis and will be contacted to provide specific information regarding their individual book of business. The discovery of errors in a Company’s reported exposure under tire Data Call may require a resubmission of the current Contract Year Data Call which, as the Data Call impacts the Company’s Premium, Retention, and coverage for the Contract Year, will be required before the Company’s request for reimbursement or an advance will be fully processed by the Administrator. (c) Loss Reimbursement Calculations 1. in general, the Company’s paid Ultimate Net Losses must exceed its full FFICF Retention for a specific Covered Event before any reimbursement is payable from the FHCF for that Covered Event. As described in Article V(28)(b), Retention adjustments will be made on or after January 1 of the Contract Year, No interest is payable on additional payments to the Company due to this type of Retention adjustment. Each Company, including entities created pursuant to Section 627.351(6), Florida Statutes, incurring reimbursable Losses will receive the amount of reimbursement due under the individual Company’s Contract up to the amount of the Company’s payout. If more than one Covered Event occurs in any one Contract Year, any reimbursements due from the FHCF shall take into account the Company’s Retention for each Covered Event, However, the Company’s reimbursements from tire FHCF for all Covered Events occurring during the Contract Year shall not exceed, in aggregate, the Projected Payout Multiple or Payout Multiple, as applicable, times the individual Company’s Reimbursement Premium for the Contract Year. 2. Reserve established. When a Covered Event occurs in a subsequent Contract Year when reimbursable Losses are still being paid for a Covered Event in a previous Contract Year, the SBA will establish a reserve for the outstanding reimbursable Losses for the previous Contract Year, based on the length of time the Losses have been outstanding, the amount of Losses already paid, the percentage of incurred Losses still unpaid, and any other factors specific to the loss development of the Covered Events involved. (d) Commutation 1. Not less than 36 months or more than 60 months after the end of the Contract Year, the Company shall file a final Proof of Loss Report(s), with the exception of Companies havingno reportable Losses as described in paragraph (3)(d)l.a. below. Otherwise, the final Proofof Loss Report(s) is required as specified in paragraph (3)(d)l.b. below. The Company andSBA may mutually agree to initiate commutation after 36 months and prior to 60 monthsafter the end of the Contract Year, The commutation negotiations shall begin at the later of 60 months after the end of the Contract Year or upon completion of the FHCF lossexamination for the Company and the resolution of all outstanding examination issues. FHCF-20I7K 15 Rule 19-8.010 F.A.C.

a. If the Company’s most recently submitted Proof of Loss Report(s) indicates that it has no Losses resulting horn Covered Events during the Contract Year, the SB A shall after 36 months request that the Company execute a final commutation agreement. The finalcommutation agreement shall constitute a complete and final release of all obligations ofthe SBA with respect to Losses. If the Company chooses not to execute a finalcommutation agreement, the SBA shall be released from all obligations60 monthsfollowing the end of the Contract Year if no Proof of Loss Report indicatingreimbursable Losses had been filed and the commutation shall be deemed concluded.However during this time, if the Company determines that it does have Losses to reportfor FHCF reimbursement, the Company must submit an updated Proof of Loss Reportprior to the end of 60 months after the Contract Year and the Company shall be requiredto follow the commutation provisions and time frames otherwise specified in thissection. b. If the Company has submitted a Proof of Loss Report indicating that it does have Losses resulting from a Covered Event during the Contract Year, the SBA may require theCompany to submit within 30 days an updated, current Proof of Loss Report for eachCovered Event during the Contract Year. The Proof of Loss Report must include all paid Losses as well as all outstanding Losses and incurred but not reported Losses, which arenot finally settled and which may be reimbursable Losses under this Contract, and mustbe accompanied by supporting documentation (at a minimum an adjuster’s summary report or equivalent details) and a copy of a written opinion on the present value of theoutstanding Losses and incurred but not reported Losses by the Company’s certifyingactuary. Failure of the Company to provide an updated current Proof of Loss Report, supporting documentation, and an opinion by the date requested by the SBA may resultin referral to the Office of Insurance Regulation for a violation of the Contract. Increasesin reported paid, outstanding, or incurred but not reported Losses on original or corrected Proof of Loss Report filings received later than 60 months after the end of theContract Year shall not be eligible for reimbursement or commutation. 2. Determining the present value of outstanding Losses. a If the Company exceeds or expects to exceed its Retention, the Company and the SBA . or their respective representatives shall attempt, by mutual agreement, to agree upon the present value of all outstanding Losses, both reported and incurred but not reported, resulting from Covered Events during the Contract Year. Payment by the SBA of its portion of any amount or amounts so mutually’ agreed and certified by the Company’s certifying actuary shall constitute a complete and final release of the SBA in respect of all Losses, both reported and unreported, under this Contract. b. If agreement on present value cannot be reached within 90 days of the FHCF’s receipt of the final Proof of Loss Report and supporting documentation, the Company and the SBA may mutually appoint an actuary, adjuster, or appraiser to investigate and determine such Losses. If both parties then agree, the SBA shall pay its portion of the amount so determined to be the present value of such Losses. c. If tlie parties fail to agree, then any difference shall be settled by a panel of three actuaries, as provided in this paragraph. i. One actuary shall be chosen by each party, and the third actuary shall be chosen by those two actuaries. If either party does not appoint an actuary within 30 days, the other party may appoint two actuaries. If the two actuaries fail to agree on the selection of an independent third actuary within 30 days of their appointment, each of them shall name two, of whom the other shall decline one and the decision shall be made by drawing lots. FHCF-2037K 16 Rule 19-8.010 F.A.C.

ii. All of the actuaries shall be regularly engaged in the valuation of property claims and losses and shall be members of the Casualty Actuarial Society and of the American Academy of Actuaries. iii. None of the actuaries shall be under the control of either party to this Contract. iv. Each party shall submit its case to the panel in writing on the 30th day after the appointment of the third actuary. Following the submission of the case to the panel,the parties are prohibited from providing any further information or othercommunication except at the request of the panel. Such responses to requests fromthe panel must be in writing and simultaneously provided to die other party and allmembers of the panel, except that the panel may require the response to be providedhi a meeting or teleconference attended by both parties and all members of thepanel. v. The decision in writing of any two actuaries, when filed with the parties hereto, shall, be final and binding on both parties. d. The reasonable and customary expense of the actuaries and of the commutation (as a result of b. and c. above) shall be equally divided between the two parties. Said commutation shall take place in Tallahassee, Florida, unless some other place is mutually agreed upon by the Company and the SB A. (4) Advances (a) The SB A may make advances for loss reimbursements as defined herein, at market interest rates, to the Company in accordance with Section 215,555(4)(e), Florida Statutes. An advance is an early reimbursement which allows the Company to continue to pay claims in a timely manner. Advances will be made based on the Company’s paid and reported outstanding Losses for Covered Policies (excluding all incurred but not reported Losses) as reported on a Proof of Loss Report, and shall include Loss Adjustment Expense Reimbursement as calculated by the FHCF. In order to be eligible for an advance, the Company must submit its exposure data for the Contract Year as required under paragraph(1) of this Article. Except as noted below, advances, if approved, will be made as soon as practicable after the SBA receives a written request, signed by two officers of the Company, for an advance of a specific amount and any other information required for the specific type of advance under subparagraphs (c) and (e) below. All reimbursements due to the Company shall be offset against any amount of outstanding advances plus the interest due thereon, (b) For advances or excess advances, which are advances that are in excess of the amount to which the Company is entitled, the market interest rate shall be the prime rate as published in the Wall Street Journal on the first business day of the Contract Year. This rate will be adjusted annually on the first business day of each subsequent Contract Year, regardless of whether the Company executes subsequent Contracts. In addition to the prime rate, an additional 5% interest charge will apply on excess advances. All interest charged will commence on the date the SBA issues a check for an advance and will cease on the date upon which the FHCF has received the Company’s Proof of Loss Report for the Covered Event for which the Company qualifies for reimbursement. If such reimbursement is less than the amount of outstanding advances issued to the Company, interest will continue to accrue on the outstanding balance of the advances until subsequent Proof of Loss Reports quality the Company for reimbursement under any Covered Event equal to or exceeding the amount of any outstanding advances. Interest shall be billed on a periodic basis. If it is determined that the Company received funds in excess of those to which it was entitled, the interest as to those sums will not cease on the date of the receipt of the Proof of Loss Report but will continue until the Company reimburses the FHCF for the overpayment. FHCF-20I7K 17 Rule 19-8.01 OF. A.C.

(c) If the Company lias an outstanding advance balance as of December 3] of this or any other Contract Year, the Company is required to have an actuary certify outstanding and incurred but not reported Losses as reported on the applicable December Proof of Loss Report. (d) The specific type of advances enumerated in Section 215.555, Florida Statutes, follow. I.Advances to Companies to prevent insolvency, as defined under Article XIV, a. Section 215.555(4)(e)3., Florida Statutes, provides that the SBA shall advance to the Company amounts necessary to maintain the solvency of the Company, up to50 percent of the SBA’s estimate of the reimbursement due to tire Company, b. In addition to the requirements outlined in subparagraph (4)(a) above, the requirements for an advance to a Company to prevent insolvency are that the Company demonstrates it is likely to qualify for reimbursement and that the immediate receipt of moneys from tire SBA is likely to prevent the Company fr om becoming insolvent, and the Company provides the following information: i. Current assets; ii. Current liabilities other than liabilities due to the Covered Event;iii. Current surplus as to policyholders; iv. Estimate of other expected liabilities not due to the Covered Event; and v. Amount of reinsurance available to pay claims for the Covered Event under other reinsurance treaties. c. The SBA’s final decision regarding air application for an advance to prevent insolvency shall be based on whether or not, considering tire totality of the circumstances, including the SBA’s obligations to provide reimbursement for all Covered Events occurring during tire Contract Year, granting an advance is essential to allowing the entity to continue to pay additional claims for a Covered Event in a timely manner. 2, Advances to entities created pursuant to Section 627.351 (6), Florida Statutes. a. Section 215.555(4) (e)2., Florida Statutes, provides that the SBA may advance to an entity created pursuant to Section 627.351(6), Florida Statutes, up to 90% of the lesserof tire SBA’s estimate of the reimbursement due or the entity’s share of the actualaggregate Reimbursement Premium for that Contract Year, multiplied by the currentavailable liquid assets of the FHCF. . b. hr addition to tire requirements outlined in subparagraph (4)(a) above, the requirements for an advance to entities created pursuant to Section 627.351(6), Florida Statutes, are that the entity must demonstrate to the SBA that the advance is essential to allow the entity to pay claims for a Covered Event. 3. Advances to limited apportionment companies. Section 215.555(4)(e)3., Florida Statutes, provides that the SBA may advance the amountof estimated reimbursement payable to limited apportionment companies. (e) In determining whether or not to grant air advance and the amount of an advance, the SBA: 1. Shall determine whether its assets available for the payment of obligations are sufficient and sufficiently liquid to fulfill its obligations to other Companies prior to granting anadvance; 2. Shall review and consider all the information submitted by such Companies; 3. Shall review such Companies’ compliance with all requirements of Section 215.555, Florida Statutes; 4. Shall consult with all relevant regulatory agencies to seek all relevant information; FHCF-2017K 18 Rule 19-8.010 F.A.C,

5. Shall review the damage caused by the Covered Event and when that Covered Event occurred; 6. Shall consider whether the Company has substantially exhausted amounts previously advanced; 7. Shall consider any other factors deemed relevant; and 8. Shall require commercial self-insurance funds established under section 624.462, Florida Statutes, to submit a copy of written estimates of expenses in support of the amount of advance requested. (f) Any amount advanced by the SBA shall be used by the Company only to pay claims of its policyholders for the Covered Event which has precipitated the immediate need to continue to pay additional claims as they become due. (5) Inadequate Data Submissions If exposure data or other information required to be reported by the Company under the terms of thisContract is not received by the FHCF in the format specified by the FHCF or is inadequate to theextent that the FHCF requires resubmission of data, the Company will be required to pay the FHCF aresubmission fee of $1,000 for resubmissions that are not a result of an examination by the SBA, If aresubmission is necessary as a result of an examination report issued by the SBA, the firstresubmission fee will be $2,000, If the Company’s examination-required resubmission is inadequateand the SBA requires an additional resubmission(s), the resubmission fee for each subsequentresubmission shall be$2,000. A resubmission of exposure data may delay the processing of theCompany’s request for reimbursement or an advance. (6) Confidential Information/Trade Secret Information Pursuant to the provisions of Section 215.557, Florida Statutes, the reports of insured values underCovered Policies by ZIP Code submitted to the SBA pursuant to Section 215,555, Florida Statutes,are confidential and exempt from the provisions of Section 319.07(1), Florida Statutes, and Section24(a), Art. I of the State Constitution. If other information submitted by the Company to the FHCFcould reasonably be ruled a “trade secret” as defined in Section812.081, Florida Statutes, suchinformation must be clearly marked “Trade Secret Information.” ARTICLE XI - TAXES In consideration of the terms under which this Contract is issued, the Company agrees to make nodeduction in respect of the Premium herein when making premium tax returns to the appropriateauthorities. Should any taxes be levied on the Company in respect of the Premium herein, the Companyagrees to make no claim upon the SBA for reimbursement in respect of such taxes. ARTICLE XII - ERRORS AND OMISSIONS Any inadvertent delay, omission, or error on the part of the SBA shall not be held to relieve the Companyfrom any liability which would attach to it hereunder if such delay, omission, or error had not been made. ARTICLE XIII - INSPECTION OF RECORDS The Company shall allow the SBA to inspect, examine, and verify, at reasonable times, all records of theCompany relating to the Covered Policies under this Contract, including Company files concerningclaims, Losses, or legal proceedings regarding subrogation or claims recoveries which involve thisContract, including premium, loss records and reports involving exposure data or Losses under CoveredPolicies. This right by the SBA to inspect, examine, and verify shall survive the completion and closureof an exposure examination or loss examination file and the termination of the Contract. The Companyshall have no right to re-open an exposure or loss examination once closed and the findings have been FHCF-2017K 19 Rule 19-8.010 F.A.C.

,, accepted by the Company; any re-opening shall be at the sole discretion of the SBA. If the State Board of i Administration Finance Corporation has issued revenue bonds and relied upon the exposure and Loss data submitted and certified by the Company as accurate to determine the amount of bonding needed, theSBA may choose not to require, or accept, a resubmission if the resubmission will result in additionalreimbursements to the Company. The SBA may require any discovered errors, inadvertent omissions,and typographical errors associated with the data reporting of insured values, discovered prior to theclosing of the file and acceptance of the examination findings by the Company, to be corrected to reflectthe proper values. The Company shall retain its records in accordance with die requirements for recordsretention regarding exposure reports and claims reports outlined herein, and in any administrative rulesadopted pursuant to Section 215.555, Florida Statutes, Companies writing covered collateral protectionpolicies, as defined in definition(10)(d) of Article V, must be able to provide documentation that thepolicy covers personal residences, protects both the borrower’s and lender’s interest, and tiiat thecoverage is in an amount at least equal to the coverage for the dwelling in place under the lapsedhomeowner’s policy. (1) Purpose of FHCF Examination The purpose of the examinations conducted by the SBA is to evaluate the accuracy of the FHCFexposure or Loss data reported by the Company. However, due to the limited nature of theexamination, it cannot be relied upon as an assurance that a Company’s data is reported accurately xxxx its entirety. The Company should not rely on the FHCF to identify every type of reporting error inits data. In addition, the reporting requirements are subject to change each Contract Year so it is theCompany’s responsibility to be familiar with the applicable Contract Year requirements and toincorporate any changes into its data for that Contract Year. It is also the Company’s responsibilityto ensure that its data is reported accurately and to comply with Florida Statutes and any applicablerules when reporting exposure data. The examination report is not intended to provide a legaldetermination of the Company’s compliance. (2) Examination Requirements for Exposure Verification The Company shall retain complete and accurate records, in policy level detail, of all exposure datasubmitted to the SBA in any Contract Year until the SBA has completed its examination of tireCompany’s exposure submissions. The Company shall also retain complete and accurate records ofany completed exposure examination for any Contract Year in which the Company incurred Lossesuntil the completion of the loss reimbursement examination and commutation for that Contract Year.The records to be retained are outlined in the Data Call adopted for the Contract Year under Rule 19- 8.029, F.A.C. A complete list of records to be retained for the exposure examination is set forth inForm FHCF-EAP1, adopted for the Contract Year- under Rule 19-8.030, F.A.C. (3) Examination Requirements for Loss Reports The Company shall retain complete and accurate records of all reported Losses and/or advancessubmitted to the SBA until the SBA has completed its examination of the Company’s reimbursableLosses and commutation for the Contract Year (if applicable) has been concluded. Tire records to beretained are set forth as part of tire Proof of Loss Report, Form FHCF-L1B, adopted for the ContractYear under Rule 19-8.029, F.A.C., and Form FHCF-LAP1, adopted for the Contract Year underRule 19-8.030, F.A.C. (4) Examination Procedures (a) The FHCF will send an examination notice to the Company providing the commencement date of the examination, the site of the examination, any accommodation requirements of the examiner, and the reports and data which must be assembled by the Company and forwarded to the FHCF upon request. The Company shall be prepared to choose one location in which to be examined, unless otherwise specified by the SBA, t FHCF-2017K 20 Rule 19-8.01 OF. A.C.

(b) The reports and data are required to be forwarded to the FHCF as set forth in an examination notice letter. The information is then forwarded to the examiner. If the FHCF receives accurate and complete records as requested, the examiner will contact the Company to inform the Company as to what policies or other documentation will be required once the examiner is on site. Any records not required to be provided to the examiner in advance shall be made available at tire time the examiner arrives on site. Any records to support reported exposure or Losses which are provided after the examiner has left the work-site will, at the SBA’s discretion, result in an additional examination of exposure and/or Loss records or an extension or expansion of the examination already in progress. All costs associated with such additional examination or with the extension or expansion of the original examination shall be borne by the Company. (c) At the conclusion of the examiner’s work and the management review of the examiner’s report, findings, recommendations, and work papers, the FHCF will forward an examination report to the Company and require a response from the Company by a date certain as to the examination findings and recommendations, if any. (d) If the Company accepts the examination findings and recommendations, and there is no recommendation for additional information, the examination report will be finalized and the exam file closed. (e) If the Company disputes the examiner’s findings, the areas in dispute will be resolved by a meeting or a conference call between the Company and FHCF management (f) 1. If the recommendation of the examiner is to resubmit the Company’s exposure data for the Contract Year in question, then the FHCF will send the Company a letter outlining theprocess for resubmission and including a deadline to resubmit. Once the resubmission isreceived, the FHCF’s Administrator calculates a revised Reimbursement Premium for theContract Year which has been examined. The SBA shall then review the resubmission withrespect to the examiner’s findings, and accept the resubmission or contact the Company withany questions regarding the resubmission. Once the SBA has accepted the resubmission as asufficient response to the examiner’s findings, the exam is closed. 2. If the recommendation of the examiner is to give the Company the option to either resubmit the exposure data or to pay the estimated Premium difference, then the FHCF will send the Company a letter outlining the process for resubmission or for paying the estimated Premium difference and including a deadline for the resubmission or the payment to be received by the FHCF’s Administrator. If the Company chooses to resubmit, the same procedures outlined in Article X1II(4) apply. (g) If the recommendation of the examiner is to update the Company’s Proof of Loss Report(s) for the Contract Year under review, the FHCF will send the Company a letter outlining the process for submitting the Proof of Loss Report(s) and including a deadline to file. Once the Proof of Loss Report(s) is received by the FHCF Administrator, the FHCF’s Administrator will calculate a revised reimbursement. The SBA shall then review the submitted Proof of Loss Report(s) with respect to the examiner’s findings, and accept the Proof of Loss Report(s) as filed or contact the Company with any questions. Once the SBA has accepted the corrected Proof of Loss Report(s) as a sufficient response to the examiner’s findings, the exam is closed. (h) The examiner’s list of errors is made available in the examination report sent to the Company. Given that the examination was based on a sample of the Company’s policies or claims rather than the whole universe of the Company’s Covered Policies or reported claims, the error list is not intended to provide a complete list of errors but is intended to indicate what information needs to be reviewed and corrected throughout the Company’s book of Covered Policy business or claims information to ensure more complete and accurate reporting to the FHCF. FHCF-20I7K 21 Rule 19-8.010 F.A.C.