Amendment No. 1 to the BankUnited Single Family Shared-Loss Agreement (the “SFLSA”) with the FDIC

Exhibit 2.1c

EXECUTION COPY

Amendment No. 1 to the BankUnited

Single Family Shared-Loss Agreement

(the “SFLSA”) with the FDIC

This Amendment No. 1 (the “Amendment”) is made and effective as of November 2, 2010 (the “Effective Date”), and amends the SFLSA between BankUnited and the FDIC as follows:

WHEREAS, on May 21, 2009 BankUnited entered into the SFLSA with the FDIC as Receiver of BankUnited, FSB, Coral Gables, Florida; and

WHEREAS, under the terms of the above referenced SFLSA the FDIC pays BankUnited a specified percent of the Loss Amount on Short-Sale Losses; and

WHEREAS, the FDIC and BankUnited wish to provide loss coverage for Short Refinance Losses (as hereinafter defined).

NOW THEREFORE, in consideration of the mutual covenants and undertakings set forth herein, and other good and valuable consideration, the receipt and sufficiency of which are hereby acknowledged, the parties hereby agree to amend the SFLSA as follows:

1. Amendments to Article I - Definitions.

(a). The following definitions are hereby inserted in Article I of the SFLSA:

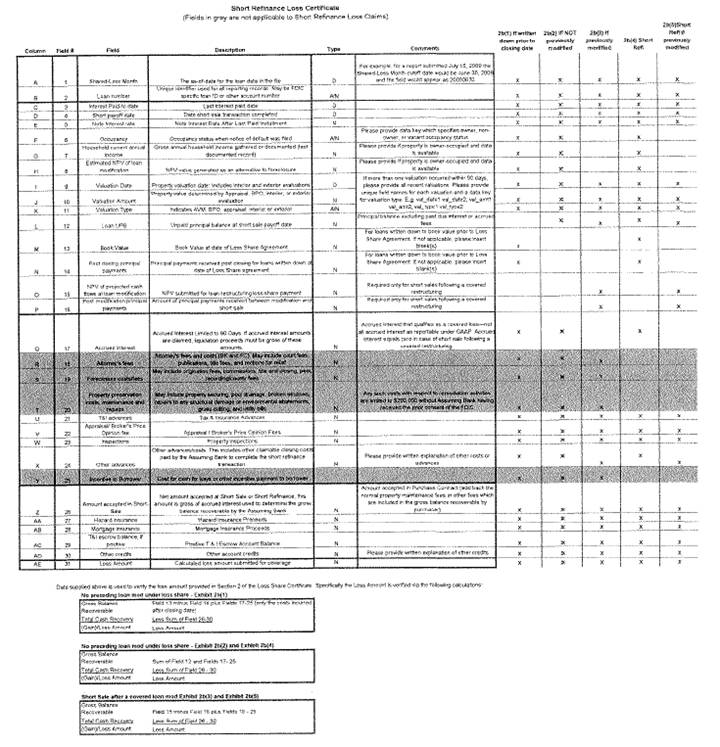

“Short Refinance Loss” means the loss realized on a Short Refinance measured by the difference between the outstanding principal balance, including advances to pay taxes and insurance or homeowner’s association dues to protect the property pending such refinance, of the Single Family Shared-Loss Loan at the date of Short Refinance less any and all funds received by the Assuming Bank with respect to any Loan or Collateral liquidated through the Short Refinance program; provided that such loss shall be calculated in accordance with the form and methodology specified on Exhibit 2(b)(4) attached hereto.

“Qualifying Borrower” means a borrower with respect to a Single Family Shared-Loss Loan meeting the criteria described under “Eligibility — Qualifying Borrower Characteristics” on Exhibit A attached hereto.

“Short Refinance” means a transaction where (a) a Qualifying Borrower with respect to a Single Family Shared-Loss Loan refinances such loan through an unaffiliated third-party originator, resulting in a satisfaction of the existing loan, (b) the

proceeds to the Assuming Bank are less than the balance due on the loan and (c) the standards set forth on Exhibit A and Exhibit B (attached hereto) are met.

“Collateral” means any and all real or personal property, whether tangible or intangible, securing or pledged to secure a Single Family Shared-Loss Loan, including any account, equipment, guarantee or contract right, or other interest that is the subject of any collateral document.

(b). The following definition is hereby amended and restated as follows:

“Short-Sale Loss” means the loss resulting from the Assuming Bank’s agreement with the mortgagor to accept a payoff in an amount less than the balance due on the loan (including the costs of any cash incentives to borrower to agree to such sale or to maintain the property pending such sale); provided that the term Short-Sale Loss includes a Short Refinance Loss. Short-Sale Losses shall be calculated in accordance with the form and methodology specified in Exhibits 2(b)(1)-(4) as applicable.

2. Amendments to Section 2.1. Section 2.1 is amended by adding the following at the end thereof:

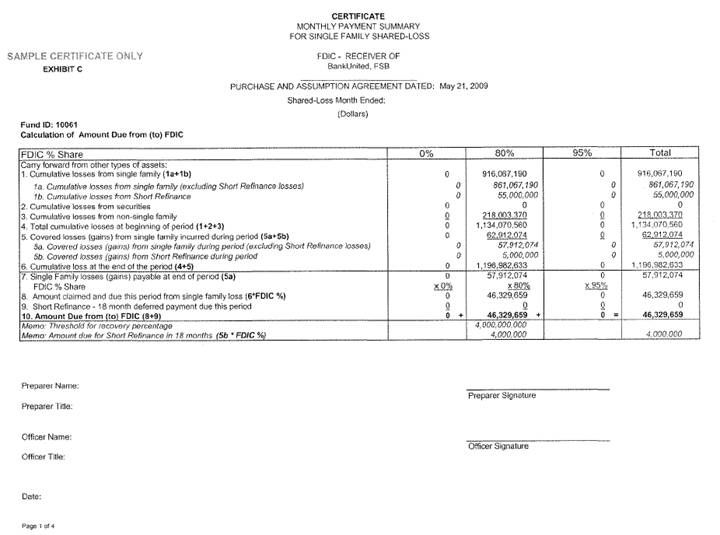

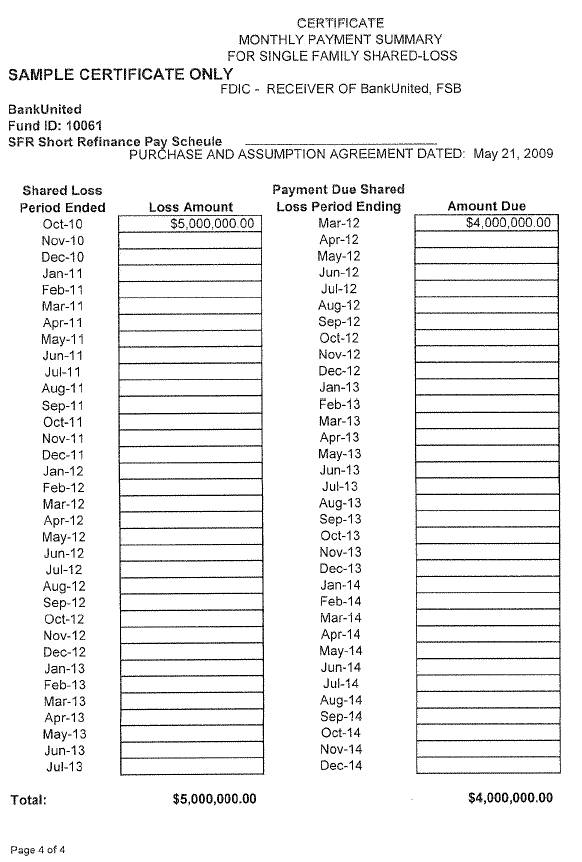

(g)(i) Notwithstanding anything to the contrary set forth in the SFSLA, the Assuming Bank may include a claim for a Short-Sale Loss that is a Short Refinance Loss on the Monthly Certificate with respect to the Shared-Loss Month in which such Short Refinance Loss occurs (which Monthly Certificate shall be in the form attached as Exhibit C hereto). The Assuming Bank agrees that it is not entitled to receive payment on such claim until the earlier of (a) 18 months after the closing of the Short Refinance transaction and (b) the date loss sharing payments are due for the Monthly Certificate delivered in connection with the final Shared-Loss Month. Claim amounts will be determined using the methodology specified on the Short Refinance Loss Certificate attached as Exhibit 2(b)(4); provided, however, that the “Total Cash Recovery” shall in no event be less than 90% of the value of the Collateral. For the avoidance of doubt, a Short Refinance Loss shall be included in the determination of the Stated Threshold for the Monthly Certificate which includes such Short Refinance Loss.

(ii) If the Stated Threshold is crossed for the Single Family Shared-Loss reporting period during which a Short Refinance Loss is claimed, the Short Refinance Loss for the reporting period shall be allocated by applying the following formula:

A = Stated Threshold

B = Total cumulative losses at beginning of period (Certificate page 1 item 4)

C = Covered losses (gains) from Short Refinance during period (Certificate page 1 item 5b)

D = Covered losses (gains) from single family incurred during the period (Certificate page 1 item 5)

E = Cumulative loss at end of month (Certificate page 1 item 7)

![]()

(iii) Either party may terminate the Pilot Short Refinance program described on Exhibit A upon 30-days prior written notice to the other party, provided that no party may submit any such written notice prior to the nine-month anniversary of the Effective Date hereof; provided, however, that any party may provide such a termination notice if the parties agree in writing that the LPS Applied Analytics model utilized for the Pilot Short Refinance program does not adequately predict loss frequency rates. If either party terminates the program, the FDIC will honor all loss share claims for Short Refinances in process, whether or not a Short Refinance Loss claim has been submitted prior to such termination.

(iv) The Assuming Bank shall provide, on a monthly basis, information on the number of borrowers considered for a Short Refinance and the number of borrowers with a Short Refinance transaction in process.

3. Counterparts. This amendment may be executed in any number of counterparts, each of which shall be deemed an original, but all of which shall constitute one and the same amendment.

4. No Further Amendment. Except as expressly amended hereby, the SFLSA is in all respects ratified and confirmed and all the terms, conditions and provisions thereof shall remain in full force and effect. This Amendment is limited precisely as written and shall not be deemed to be an amendment to any other term or condition of the SFLSA or any of the documents referred to therein.

[Signature Page Follows]

IN WITNESS WHEREOF, the parties hereto have executed this Amendment as of the Effective Date.

|

|

|

FEDERAL DEPOSIT INSURANCE CORPORATION, RECEIVER OF BANKUNITED, FSB, CORAL GABLES, FLORIDA | |

|

|

|

|

|

|

|

|

|

|

|

|

|

By: |

/s/ Xxxxx Malami |

|

|

|

|

Name: Xxxxx Malami |

|

|

|

|

Title: Assistant Director |

|

|

|

|

|

|

Attest: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

FEDERAL DEPOSIT INSURANCE CORPORATION | |

|

|

|

|

|

|

|

|

|

|

|

|

|

By: |

/s/ Xxxxx Malami |

|

|

|

|

Name: Ralpha Malami |

|

|

|

|

Title: Assistant Director |

|

|

|

|

|

|

Attest: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

BANKUNITED | |

|

|

|

|

|

|

|

|

|

|

|

|

|

By: |

/s/ Xxxxxxxx Xxxxx |

|

|

|

|

Name: Xxxxxxxx Xxxxx |

|

|

|

|

Title: COO |

|

|

|

|

|

|

Attest: |

|

|

|

|

|

|

|

|

|

|

|

|

|

[Signature Page to Amendment No. 1]

Exhibit A

Pilot Short Refinance Program Terms

Premise

The BankUnited Option ARM (OARM) portfolio is deteriorating quickly with loans rolling current to delinquent at rates as high as 5.4% monthly. The majority of these loans are set to recast in 2011 with the pace accelerating through 2010. BankUnited has proposed including short refinance as a permitted Loss under the Single-Family Shared Loss Agreement (SFSLA), given it is the least costly loss mitigation solution for OARM loans.

BankUnited will enter a joint marketing agreement with an unaffiliated third party originator to solicit borrowers for refinance opportunities. The unaffiliated third party originator will provide financing and will be the originator of the new loans. BankUnited will not receive any compensation and will not retain an interest in the new loan from the unaffiliated third party originator under this arrangement. The unaffiliated third party originator will act independently, and shall not act as BankUnited’s agent. Borrowers will not be precluded from seeking refinance opportunities with other lenders, as long as the new lender is not an affiliate of BankUnited and BankUnited is not receiving compensation or retaining an interest in the loan (any such other lender, an “Alternative Lender”). For the avoidance of doubt, a loss may still qualify as a Short Refinance Loss if the refinance is originated by an Alternative Lender.

BankUnited will not make any representations regarding eligibility or the quality of the new loan.

Eligibility

Qualifying Borrower Characteristics:

· Pre-recast OARM borrowers with an expected recast within one year and an expected payment increase at recast of more than 10%.

· Single Family Shared-Loss Loan is prepaid or due for current month

· Owner-Occupied property, primary residence.

Transaction Requirements:

· After calculation in accordance with the applicable guidelines, the Short Refinance Loss will result in a lesser monetary loss than a Foreclosure Loss.

· BankUnited will not be required to offer borrowers the Short Refinance program where the amount of principal reduced would exceed the lesser of (a) 35 percent of the outstanding unpaid principal balance and (b) $250,000.

· New loan must adhere to FHA, Xxxxxx Xxx, or Xxxxxxx Mac underwriting standards and balance requirements.

· BankUnited will be required to consider the borrower’s ability to make cash contributions towards closing costs and shortfall. The criteria for consideration are outlined in the Borrower Contribution Guidelines document, attached hereto as Exhibit B.

· The borrower will have the option to make additional cash contributions towards the outstanding principal balance in order to qualify for the transaction.

· After the close of a Short Refinance transaction, BankUnited agrees that it will not have any servicing rights on behalf of the unaffiliated third party originator.

· BankUnited will have the option to exclude loans with mortgage insurance from this program since the Short Refinance transaction may jeopardize the mortgage insurance.

Evaluation Analysis and Least Cost Parameters

· The unaffiliated third party originator will provide BankUnited with data used for the borrower’s underwriting evaluation in connection with BankUnited’s determination of the borrower’s eligibility for this program.

· Subject to meeting other guidelines specified herein, a Short Refinance will be approved if the value of Short Refinance exceeds the estimated value of a foreclosure.

Additional Considerations

· The FDIC will not make any representations or warranties in connection with the refinanced loan nor will it have any liability for breaches of representation or warranties made to the originator and/or buyer of any refinanced loan.

· BankUnited will not make any representations or warranties for the eligibility or quality of the new loan.

· BankUnited shall not charge the borrower any prepayment penalty or late fees.

· The third party originator will be entitled to receive reasonable and customary fees for originating and funding each Short Refinance transaction, which may be included on the settlement statement; however, reasonable and customary fees must adhere to Fannie, Freddie, or FHA guidelines.

· If the borrower contributes any cash at closing, regardless of whether this is applied to closing costs, MI premium or other, that amount shall be applied to reduce the amount of the Short Refinance Loss.

· If any future investor incentives apply to Short Refinance transactions, the Short Refinance Loss amount will be reduced by the amount of such investor incentive.

Exhibit B

Short Refinance Pilot Program

Borrower Contribution Guidelines

Required Contribution

Borrowers shall be evaluated for their ability to contribute to short refinance losses. The contribution required from the borrower (“Required Contribution”) will be the lesser of (1) the available funds for contribution, or (2) the baseline contribution as defined below.

Available Funds for Contribution

The amount of funds the borrower has available to contribute toward a short refinance; determined as follows

Available Funds for Contribution = Total liquid assets – Exclusions

(Available funds for contribution will be determined using the signed 1003 and 1008 provided for the third party lender’s underwriting determination.)

Total liquid assets are assets available in cash, savings, checking, money market funds, certificates of deposit, marketable stocks and bonds. This does not include qualified retirement funds (401K and XXX) and annuities.

Exclusions include:

1. The equivalent of 12 months payments of principal, interest, taxes and insurance (“PITI”) for the new loan

2. 50% of any remaining liquid assets in excess of the equivalent 12 months PITI

Baseline Contribution

Baseline contribution = Closing Costs + 50% of Gross loss (as defined below)

Gross loss = Total Debt (UPB & Advances) – New Loan Proceeds (excluding closing costs)

Net Loss

Net Loss = Gross Loss – Required Contribution

Net Loss limit: In no case shall Net Loss recognized by BankUnited exceed 35% of UPB or $250,000

Should the Required Contribution not reduce Net Loss to 35% of Total Debt or $250,000, then borrower is permitted to contribute additional funds to reduce the Net Loss to the limit.

Exhibit C

(See Attached)

Exhibit 2(b)(4)

(See Attached)