ASSET PURCHASE AGREEMENT By and Among RadioLoyalty, Inc. (“Seller”) and Lux Digital Pictures, Inc. (“Buyer”) StreamTrack Media, Inc. (“Buyer’s Subsidiary”) Dated August 31, 2012

EXHIBIT 10.1

By and Among

RadioLoyalty, Inc. (“Seller”)

and

Lux Digital Pictures, Inc. (“Buyer”)

StreamTrack Media, Inc. (“Buyer’s Subsidiary”)

Dated August 31, 2012

TABLE OF CONTENTS

| Page No. | |||

| Recitals | 1 | ||

| 1. | Purchase and Sale of Assets | 1 | |

| 1.1 |

Sale of Acquired Assets

|

1 | |

| 1.2 |

Purchase Price

|

1 | |

| 1.3 |

Risk of Loss

|

2 | |

| 1.4 |

Valuation of Assets

|

2 | |

| 2. | Obligations and Liabilities | 2 | |

| 3. | Piggyback Registration Rights | 2 | |

| 4. | Closing and Further Acts | 3 | |

| 4.1 |

Time and Place of Closing

|

3 | |

| 4.2 |

Actions at Closing

|

3 | |

| 4.3 |

Conduct of Business Prior to Closing

|

3 | |

| 4.4 |

No Solicitation and Due Diligence

|

4 | |

| 5. | Representations and Warranties of Seller | 5 | |

| 5.1 |

Power and Authority; Binding Nature of Agreement

|

5 | |

| 5.2 |

Subsidiaries

|

5 | |

| 5.3 |

Good Standing

|

5 | |

| 5.4 |

Charter Documents and Corporate Records

|

5 | |

| 5.5 |

Absence of Changes

|

5 | |

| 5.6 |

Financial Statements

|

7 | |

| 5.7 |

Approvals

|

7 | |

| 5.8 |

Brokers

|

7 | |

| 5.9 |

Representations True on Closing Date

|

7 | |

| 6. | Representations and Warranties of Buyer | 8 | |

| 6.1 |

Power and Authority; Binding Nature of Agreement

|

8 | |

| 6.2 |

Good Standing

|

8 | |

| 6.3 |

Approvals

|

8 | |

| 6.4 |

Brokers

|

8 | |

| 6.5 |

Representations True on Closing Date

|

8 | |

i

TABLE OF CONTENTS

| Page No. | |||

| 7. | Conditions to Closing | 8 | |

| 7.1 |

Conditions Precedent to Buyer’s Obligation to Close

|

8 | |

| 7.2 |

Conditions Precedent to Seller’s Obligation to Close

|

9 | |

| 7.3 |

Notice Requirement

|

9 | |

| 8. | Further Assurances and Post Closing Covenants | 10 | |

| 8.1 |

Books and Records

|

10 | |

| 8.2 |

Employee Plans and Employment

|

10 | |

| 9. | Survival of Representations and Warranties | 10 | |

| 10. | Indemnification | 10 | |

| 10.1 |

Indemnification by Seller

|

10 | |

| 10.2 |

Indemnification by Buyer

|

11 | |

| 10.3 |

Procedure for Indemnification Claims

|

11 | |

| 11. | Injunctive Relief | 12 | |

| 11.1 |

Damages Inadequate

|

12 | |

| 11.2 |

Injunctive Relief

|

12 | |

| 12. | Arbitration | 12 | |

| 13. | Waivers | 13 | |

| 14. | Successors and Assigns | 13 | |

| 15. | Entire and Sole Agreement | 13 | |

| 16. | Governing Law | 13 | |

| 17. | Counterparts | 13 | |

| 18. | Attorney’s Fees and Costs | 14 | |

| 19. | Assignment | 14 | |

| 20. | Remedies | 14 | |

| 21. | Section Headings | 14 | |

| 22. | Severability | 14 | |

| 23. | Notices | 14 | |

| 24. | Publicity | 15 | |

| 25. | Confidentially | 15 | |

ii

TABLE OF CONTENTS

| Exhibit A: |

Xxxx of Sale of Assets

|

|

| Exhibit B: |

Certificate of Obligation to Issue Shares

|

|

| Exhibit C: |

List of Assets

|

|

| Exhibit D: |

List of Assumed Liabilities

|

|

| Exhibit E: |

Valuation of Assets

|

|

| Exhibit F: |

Financial Statements of Seller as of May 31, 2012 (Unaudited)

|

iii

This Asset Purchase Agreement (the “Agreement”) is made and entered into as of the 31st day of August 2012 by and among RadioLoyalty, Inc., a California corporation (the “Seller”), Lux Digital Pictures, Inc., a Wyoming corporation (the “Buyer” or “Company”), and StreamTrack Media, Inc., a California corporation (“Buyer’s Subsidiary”), with respect to the following facts:

R E C I T A L S

A. Seller is engaged in the business of providing key support services for both mobile and online content, using proprietary platforms developed by Seller over the last five years (the “Business”).

B. Seller wishes to sell to Buyer, and Buyer wishes to purchase from Seller, the Business and substantially all of the assets (collectively, the “Acquired Assets”) of Seller on the terms and subject to the conditions set forth in this Agreement.

C. The purchase of the Acquired Assets under this Agreement is intended to qualify as a tax free purchase and sale under Section 368 of the Internal Revenue Code of 1986, as amended.

NOW, THEREFORE, for good and valuable consideration the receipt and sufficiency of which are hereby acknowledged by the parties to this Agreement, and in light of the above recitals to this Agreement, the parties to this Agreement hereby agree as follows:

Purchase and Sale of Assets.

1.1 Sale of Acquired Assets. Upon the terms, and subject to the conditions set forth in this Agreement being satisfied or waived as provided herein, at the Closing (as defined in Section 4.1 of this Agreement), Seller will sell, transfer, and assign to Buyer’s Subsidiary and Buyer will purchase and accept from Seller substantially all of the tangible and intangible assets of the Seller, presently owned or leased by the Seller, wherever located, including, but not limited to all contractual rights, accounts

receivable, all other receivables, cash, deposits, prepaid expenses, inventory, machinery, equipment, engineering data, databases, systems, designs, computer hardware and software, records, works in process, backlog, intellectual property (including but not limited to patents and licensing agreements), know-how, trade secrets, inventions, technology, company name, operating and equipment leases, licenses, permits, franchises, websites, customers, suppliers, contracts, sales and marketing literature and processes, techniques, goodwill, web sites, and pricing information related to the Business, as more particularly described in Exhibit C to this Agreement (the “Acquired Assets”), free and clear of all claims, liens, security interests, pledges and encumbrances other than those assumed by Buyer’s Subsidiary pursuant to this Agreement.

- 1 -

1.2 Purchase Price. Upon the terms and conditions set forth in this Agreement, in consideration for the sale, assignment, and transfer of the Acquired Assets to the Buyer’s Subsidiary, the Buyer will, after the Closing and within five (5) business days after the recording of Amended and Restated Articles of Incorporation by the Buyer with the Wyoming Secretary of State that effect a reverse split of the Buyer’s issued and outstanding common stock, issue to Seller a number of shares of Buyer’s common

stock (the “Shares”) such that on the date of the issuance of the Shares, the Seller and its affiliates will own a number of shares of the Buyer’s common stock equal to approximately 90% of the total issued and outstanding shares of Buyer’s common stock, (i) assuming the conversion of all outstanding Series A Convertible Preferred Stock of the Buyer into Buyer’s common stock on the Share issuance date, and (ii) including and taking into account all other shares of the Buyer’s common stock already owned by the Seller and its affiliates on the Share issuance date (the “Purchase Price”); provided, that the calculation of the number of Shares issuable to Seller under this Agreement will reflect that the dilution caused by outstanding shares of Buyer’s common stock in the public float on the Share issuance date will be borne 90% by the

Seller and 10% by the holders of the Buyer’s outstanding Series A Convertible Preferred Stock, (i.e. on the Share issuance date and assuming the conversion of all outstanding Series A Convertible Preferred Stock of the Buyer on such date, the Seller will own 90% of the Buyer’s outstanding common stock that is not in the Buyer’s public float, and the holders of such Series A Convertible Preferred Stock will collectively own 10% of the Buyer’s outstanding common stock that is not in the Buyer’s public float). Reference to the Buyer’s “public float” in this Agreement means outstanding shares of Buyer’s common stock that are not owned by Buyer, Seller, or any of their affiliates.

1.3 Risk of Loss. Pending the Closing, all risk of loss, damage or destruction to the Acquired Assets will be borne by Seller and the Purchase Price being paid to Seller by Buyer will, in the case of any such loss, damage, or destruction, be adjusted accordingly. In the event of a significant adjustment, either party will have the option to terminate the purchase contemplated under this Agreement.

1.4 Valuation of Assets. Buyer and Seller agree that the total value of the Acquired Assets is the amount set forth on Exhibit E to this Agreement. Buyer and Seller covenant to determine in good faith the value of each of the Acquired Assets after the Closing.

Obligations and Liabilities.

On the Closing Date, neither Buyer nor Buyer’s Subsidiary will assume or be obligated to satisfy or perform any liabilities, obligations or payables of Seller, other than those listed on Exhibit D to this Agreement.

Piggyback Registration Rights.

With respect to shares of Buyer’s common stock owned by Buyer or its affiliates (the “Registerable Securities”), if Buyer determines to register any of its securities for its own account, other than a registration relating to (a) any employee benefit plans, (b) a corporate reorganization or Rule 145 transaction or (c) any registration form which does not permit secondary sales, Buyer and its affiliates shall have to right to include in such registration up to the number of shares of Registerable Securities equal to 15% of the total number of shares that Seller determines to register (the “Piggyback Registration Right”).

- 2 -

Closing and Further Acts.

4.1 Time and Place of Closing. Upon satisfaction or waiver of the conditions set forth in Section 7 of this Agreement, the closing of the transactions contemplated by this Agreement (the “Closing”) will take place at the law offices of Xxxxxxxxxx & Associates at 0000 Xxxxx Xxxxxx Xxxxxxxxx, Xxxxx 000, Xxxxx Xxxxxx, Xxxxxxxxxx 00000 at 1:00 p.m. (local time) on the date that the parties may mutually agree in writing, but in no event later than August 31, 2012 (the “Closing

Date”). In the event that the Closing does not occur by August 31, 2012 through no fault or breach of this Agreement by either party, and the Closing Date is not extended by mutual written agreement of the Seller and the Buyer, then either party may terminate this Agreement without further obligation to the other party, except as provided in Section 25 of this Agreement.

4.2 Actions at Closing. At the Closing, the following actions will take place:

(a) Buyer will deliver to Seller a certificate evidencing Buyer’s obligation to issue the Shares to Seller in the form attached to this Agreement as Exhibit B (the “Certificate”).

(b) Seller will execute and deliver to Buyer a xxxx of sale in the form attached to this Agreement as Exhibit A (the “Xxxx of Sale”), transferring to Buyer’s Subsidiary title to the Acquired Assets free and clear of all encumbrances, liens or claims.

(c) Seller will deliver to Buyer copies of necessary resolutions of the Board of Directors and majority shareholders of Seller authorizing the execution, delivery and performance of this Agreement and the other agreements contemplated by this Agreement (including the Xxxx of Sale) for Seller’s execution, and consummation of the transactions contemplated by this Agreement, which resolutions have been certified by an officer of Seller as being valid and in full force and effect.

(d) Buyer will deliver to Seller copies of resolutions of the directors of Buyer authorizing the execution, delivery and performance of this Agreement and the other agreements contemplated by this Agreement for Buyer’s execution, if any, and consummation of the transactions contemplated by this Agreement, which resolutions have been certified by an officer of Buyer as being valid and in full force and effect.

(e) Any additional documents or instruments as a party may reasonably request or as may be necessary to evidence and affect the sale, assignment, transfer and delivery of the Acquired Assets to the Buyer’s Subsidiary.

4.3 Conduct of Business Prior to Closing. Except for transactions contemplated by this Agreement, after the execution of this Agreement by the Buyer and until the Closing, Seller will:

(a) Consistent with the ordinary course of business, maintain the operations and goodwill of the Business and the Seller, and continue its relationships with persons having business dealings with Seller; and

- 3 -

(b) Consistent with the ordinary course of business, maintain all of the assets of the Seller in their current condition, ordinary wear and tear excepted, and insurance on all of said assets in such amounts and of such kinds comparable to that in effect on the date of this Agreement; and

(c) Maintain the books, accounts and records of Seller consistent with its customary accounting policies consistently applied, including recognition of revenues and expenses, continue to collect accounts receivable and pay accounts payable utilizing normal procedures and without discontinuing or accelerating payment of such accounts and comply with all contractual and other obligations applicable to the Seller; and

(d) Not make any change to, or otherwise amend in any way, the contracts with, salaries, wages or other compensation of, any officer, director, agent or other similar representative of Seller (including any increase in any benefits or benefit plan costs or any change in any bonus, insurance, pension, compensation or other benefit plan); and

(e) Not hire any officer, director, employee, agent or other similar representative of Seller except employees hired in the ordinary course of business; and

(f) Not incur any indebtedness for borrowed money except in the ordinary course of business, and not pledge or grant liens or security interests in any of the Acquired Assets; and

(g) Not sell, transfer or dispose of any Acquired Assets except for sales in the ordinary course of business; and

(h) Not distribute any assets of Seller to any of its shareholders or other affiliates of the Seller, or to any other party; and

(i) Begin the year end financial process consistent with prior year practices.

4.4 No Solicitation and Due Diligence. Seller will not, nor will the Seller encourage, facilitate, solicit, or authorize any of its shareholders, directors, officers, employees, agents or representatives to solicit or enter into any discussion (or continue any discussion) with any third party (including the provision of any information to a third party), or enter into any agreement or understanding of any kind regarding the purchase, sale, lease,

assignment, conveyance or other disposition or acquisition of all or any portion of the Acquired Assets, the Business or any capital stock of the Seller, for the period commencing on the date first above written and extending until August 31, 2012. During this period and until the Closing or termination of this Agreement, Seller will fully cooperate with the Buyer and its representatives to enable them to conduct complete due diligence of the Seller, the Business, the Acquired Assets, and the books, records and documents relating to the Seller, the Business and the Acquired Assets.

Representations and Warranties of Seller.

Seller represents and warrants to Buyer as follows:

- 4 -

5.1 Power and Authority; Binding Nature of Agreement. Seller has full power and authority to enter into this Agreement and to perform its obligations hereunder. The execution, delivery, and performance of this Agreement by it have been duly authorized by all necessary action on its part. Assuming that this Agreement is a valid and binding obligation of each of the other parties hereto, this Agreement is a valid and binding obligation of Seller.

5.2 Subsidiaries. There is no corporation, general partnership, limited partnership, joint venture, association, trust or other entity or organization which Seller directly or indirectly controls or in which Seller directly or indirectly owns any equity or other interest.

5.3 Good Standing. Seller (i) is duly organized, validly existing and in good standing under the laws of the jurisdiction in which it is incorporated, (ii) has all necessary power and authority to own its assets and to conduct its business as it is currently being conducted, and (iii) is duly qualified or licensed to do business and are in good standing in every jurisdiction (both domestic and foreign) where such qualification or licensing is required.

5.4 Charter Documents and Corporate Records. Seller has delivered to Buyer complete and correct copies of (i) the articles of incorporation, bylaws and other charter or organizational documents of the Seller, including all amendments thereto, (ii) the stock records of the Seller, and (iii) the minutes and other records of the meetings and other proceedings of the shareholders and directors of the Seller. Seller is not in violation or breach of (i) any of the provisions of its articles of

incorporation, bylaws or other charter or organizational documents, or (ii) any resolution adopted by its shareholders or directors. There have been no meetings or other proceedings of the shareholders or directors of Seller that are not fully reflected in the appropriate minute books or other written records of Seller.

5.5 Absence of Changes. Except as otherwise set forth on Schedule 5.5 hereto or otherwise disclosed to Buyer in writing prior to the Closing, since May 31, 2012:

(a) There has not been any material adverse change in the business, condition, assets, operations or prospects of Seller and no event has occurred that might have an adverse effect on the business, condition, assets, operations or prospects of Seller.

(b) Seller has not (i) declared, set aside or paid any dividend or made any other contribution in respect of any shares of capital stock, nor (ii) repurchased, redeemed or otherwise reacquired any shares of capital stock or other securities.

(c) Seller has not sold or otherwise issued any shares of capital stock or any other securities.

(d) Seller has not amended its articles of incorporation, bylaws or other charter or organizational documents, nor has it effected or been a party to any merger, recapitalization, reclassification of shares, stock split, reverse stock split, reorganization or similar transaction.

(e) Seller has not formed any subsidiary or contributed any funds or other assets to any subsidiary.

- 5 -

(f) Seller has not purchased or otherwise acquired any assets, nor has it leased any assets from any other person, except in the ordinary course of business consistent with past practice.

(g) Seller has not made any capital expenditure outside the ordinary course of business or inconsistent with past practice, or in an amount exceeding ten thousand dollars ($10,000) singly or in excess of fifty thousand dollars ($50,000) in the aggregate, without Buyer’s prior written consent.

(h) Seller has not sold or otherwise transferred any assets to any other person, except in the ordinary course of business consistent with past practice and at a price equal to the fair market value of the assets transferred.

(i) There has not been any material loss, damage or destruction to any of the properties or assets of Seller (whether or not covered by insurance).

(j) Seller not written off as uncollectible any indebtedness or accounts receivable, except for write-offs that were made in the ordinary course of business consistent with past practice and that involved less than one thousand dollars ($1,000) singly and less than ten thousand dollars ($10,000) in the aggregate.

(k) Seller has not leased any assets to any other person except in the ordinary course of business consistent with past practice and at a rental rate equal to the fair rental value of the leased assets.

(l) Seller has not mortgaged, pledged, hypothecated or otherwise encumbered any assets, except in the ordinary course of business consistent with past practice.

(m) Seller has not entered into any contract or incurred any debt, liability or other obligation (whether absolute, accrued, contingent or otherwise), except for (i) contracts that were entered into in the ordinary course of business consistent with past practice and that have terms of less than six months and do not contemplate payments by or to Seller which will exceed, over the term of the contract, ten thousand dollars ($10,000) in the aggregate, (ii) current liabilities incurred in the ordinary course of business consistent with the past practice, and (iii) transactions related to customer and supply activities incurred in the ordinary course of

business consistent with past practice.

(n) Seller has not made any loan or advance to any other person, except for advances that have been made to customers in the ordinary course of business consistent with past practice and that have been properly reflected as “accounts receivables.”

(o) Seller has not paid any bonus to, or increased the amount of the salary, fringe benefits or other compensation or remuneration payable to, any of the directors, officers or employees of Seller.

- 6 -

(p) No contract or other instrument to which Seller is or was a party or by which Seller or any of its assets are or were bound has been amended or terminated, except in the ordinary course of business consistent with past practice.

(q) Seller has not forgiven any debt or otherwise released or waived any right or claim, except in the ordinary course of business consistent with past practice.

(r) Seller has not changed its methods of accounting or its accounting practices in any respect.

(s) Seller has not entered into any transaction outside the ordinary course of business or inconsistent with past practice, other than those listed on Schedule 5.5 of this Agreement.

(t) Seller has not agreed or committed (orally or in writing) to do any of the things described in clauses (b) through (s) of this Section 5.5.

5.6 Financial Statements. The unaudited financial statements of Seller attached hereto as Exhibit F as of and for the period ending May 31, 2012, are prepared in accordance with generally accepted accounting principles consistently applied and accurately and fairly represent the financial condition and operating results of the Seller as of the dates and for the periods indicated.

5.7 Approvals. No authorization, consent or approval of, or registration or filing with, any governmental authority is required to be obtained or made by Seller in connection with the execution, delivery or performance of this Agreement, and the conveyance by Seller to Buyer of the Business and the Acquired Assets.

5.8 Brokers. Seller has not agreed to pay any brokerage fees, finder’s fees or other fees or commissions with respect to the transactions contemplated by this Agreement, and, to Seller’s knowledge, no person is entitled, or intends to claim that it is entitled, to receive any such fees or commissions in connection with such transaction.

5.9 Representations True on Closing Date. The representations and warranties of Seller set forth in this Agreement are true and correct on the date hereof, and will be true and correct on the Closing Date as though such representations and warranties were made as of the Closing Date.

Representations and Warranties of Buyer.

Buyer represents and warrants to Seller as follows:

6.1 Power and Authority; Binding Nature of Agreement. Buyer has full power and authority to enter into this Agreement and to perform its obligations hereunder. The execution, delivery and performance of this Agreement by Buyer have been duly authorized by all necessary action on its part. Assuming that this Agreement is a valid and binding obligation of the Seller, this Agreement is a valid and binding obligation of Buyer.

- 7 -

6.2 Good Standing. Buyer (i) is duly organized, validly existing and in good standing under the laws of the jurisdiction in which it is organized, (ii) has all necessary power and authority to own its assets and to conduct its business as it is currently being conducted, and (iii) is duly qualified or licensed to do business and is in good standing in every jurisdiction (both domestic and foreign) where such qualification or licensing is required, including mortgage banking licenses.

6.3 Approvals. No authorization, consent or approval of, or registration or filing with, any governmental authority or any other person is required to be obtained or made by Buyer in connection with the execution, delivery or performance of this Agreement.

6.4 Brokers. Buyer has not agreed to pay any brokerage fees, finder’s fees or other fees or commissions with respect to the transactions contemplated by this Agreement, and, to Buyer’s knowledge, no person is entitled, or intends to claim that it is entitled, to receive any such fees or commissions in connection with such transactions.

6.5 Representations True on Closing Date. The representations and warranties of Buyer set forth in this Agreement are true and correct on the date hereof, and will be true and correct on the Closing Date as though such representations and warranties were made as of the Closing Date.

Conditions to Closing.

7.1 Conditions Precedent to Buyer’s Obligation To Close. Buyer’s obligation to close the asset purchase as contemplated in this Agreement is conditioned upon the occurrence or waiver by Buyer of the following:

(a) All state, local and other governmental approvals and all other consents or approvals of any third parties necessary to consummate the transactions contemplated by this Agreement must have been received.

(b) Seller must have delivered to Buyer a certificate executed by the Secretary of the Seller certifying (i) the names of the officers of Seller authorized to sign this Agreement to which it is a party and all other documents and instruments executed by Seller pursuant hereto, together with the true signatures of such officers; (ii) copies of corporate resolutions adopted by the Board of Directors of Seller authorizing the appropriate officers of Seller to execute and deliver this Agreement and all other agreements, documents and instruments executed by the Seller pursuant hereto and to consummate the transactions contemplated herein; and (iii)

copies of corporate resolutions adopted by the shareholders of Seller authorizing the directors and appropriate officers of Seller to execute and deliver this Agreement and all other agreements, documents and instruments executed by the Seller pursuant hereto and to consummate the transactions contemplated herein.

- 8 -

(c) Buyer must in its sole discretion be satisfied with its full and complete due diligence of Seller, the Acquired Assets, and all other aspects of the transactions contemplated by this Agreement, including but not limited to financial, legal and business affairs of Seller.

(e) The conveyance of the Acquired Assets to Buyer’s Subsidiary free and clear of any encumbrance other than those assumed by Buyer under this Agreement, and the effective assignment and acceptance of assignment of all of Seller’s material contracts to Buyer.

(d) All representations and warranties of Seller made in this Agreement or in any exhibit or schedule hereto delivered by Seller must be true and correct as of the Closing Date with the same force and effect as if made on and as of that date.

(e) Seller must have performed and complied with all agreements, covenants and conditions required by this Agreement to be performed or complied with by Seller prior to or at the Closing Date.

7.2 Conditions Precedent to Seller’s Obligation To Close. Seller’s obligation to close the asset purchase as contemplated in this Agreement is conditioned upon the occurrence or waiver by Seller of the following:

Buyer has delivered to Seller a Certificate evidencing Buyer’s obligation to issue the Shares to Seller.

(b) All representations and warranties of Buyer made in this Agreement or in any exhibit hereto delivered by Buyer must be true and correct on and as of the Closing Date with the same force and effect as if made on and as of that date.

(b) Buyer must have performed and complied with all agreements and conditions required by this Agreement to be performed or complied with by Buyer prior to or at the Closing Date.

7.3 Notice Requirement. Seller will give prompt written notice to Buyer of any development occurring after the date of this Agreement, or any item about which Seller did not have actual knowledge on the date of this Agreement, which causes or reasonably could be expected to cause a breach of any of the representations and warranties in Section 5 of this Agreement. Buyer will give prompt written notice to Seller of any development

occurring after the date of this Agreement, or any item about which Buyer did not have actual knowledge on the date of this Agreement, which causes or reasonably could be expected to cause a breach of any of the representations and warranties in Section 6 of this Agreement. No disclosure by any party pursuant to this Section 7.3 will be deemed to amend or supplement the Exhibits or to prevent or cure any misrepresentation or breach of any representation, warranty, or covenant in this Agreement.

Further Assurances and Post Closing Covenants.

Following the Closing, Seller agrees to take such actions and execute, acknowledge and deliver to Buyer such further instruments of assignment, assumptions, conveyance and transfer and take any other action as Buyer may reasonably request in order to more effectively convey, sell, transfer and assign to Buyer’s Subsidiary all of the Acquired Assets, to confirm the title of Buyer’s Subsidiary thereto, and to assist Buyer’s Subsidiary in exercising its rights with respect to the Acquired Assets. In addition, the Seller shall do the following:

- 9 -

8.1 Books and Records. Seller and Buyer agree that so long as any books, records, and files pertaining to the Business or the Acquired Assets, to the extent they pertain to the operations of Seller prior to the Closing Date, remain in existence and available, each party (at its expense) will have the right, for any reasonable and proper purpose, to inspect and make copies of the same at any time during normal business hours and on reasonable notice.

8.2 Employee Plans and Employment.

(a) Nothing contained herein will be deemed to create any third party benefits for any employee or former employee of the Seller. Nothing contained herein will be deemed to create any right of employment for any employee of the Seller, either before or after the Closing Date.

(b) Seller acknowledges that neither Buyer nor Buyer’s Subsidiary shall have any obligation to implement any employee stock option plan.

Survival of Representations and Warranties.

All representations and warranties made by each of the parties hereto will survive the Closing for a period of two years after the Closing Date.

Indemnification.

10.1 Indemnification by Seller. Seller agrees to indemnify, defend and hold harmless Buyer against any and all claims, demands, losses, costs, expenses, obligations, liabilities and damages, including interest, penalties and attorneys’ and experts’ fees and costs, incurred by Buyer or any of its affiliates arising, resulting from, or relating to any and all liabilities of Seller or relating to any Acquired Assets, other than those liabilities specifically assumed by the Buyer as expressly provided in Section 2 of

this Agreement, any misrepresentation of a material fact or omission to disclose a material fact made by Seller in this Agreement, any exhibits to this Agreement or in any other document furnished or to be furnished by Seller under this Agreement, or any breach of, or failure by Seller to perform, any of its representations, warranties, covenants or agreements in this Agreement or in any exhibit or other document furnished or to be furnished by Seller under this Agreement.

10.2 Indemnification by Buyer. Buyer agrees to indemnify, defend and hold harmless Seller against any and all claims, demands, losses, costs, expenses, obligations, liabilities and damages, including interest, penalties and attorneys’ and experts’ fees and costs incurred by Seller arising, resulting from or relating to any breach of, or failure by Buyer to perform, any of its representations, warranties, covenants or agreements in this Agreement or in any exhibit or other document furnished or to be furnished by

Buyer under this Agreement, including but not limited to indemnifying Seller for all liabilities specifically assumed by the Buyer under Section 2 of this Agreement, or arising from the Buyer’s operation of the Business after the Closing, unless caused by the Seller.

- 10 -

10.3 Procedure for Indemnification Claims.

(a) Whenever any parties become aware that a claim (an “Underlying Claim”) has arisen entitling them to seek indemnification under this Section 10 of the Agreement, such parties (the “Indemnified Parties”) shall promptly send a notice (“Notice”) to the parties liable for such indemnification (the “Indemnifying Parties”) of the right to indemnification (the “Indemnity Claim”); provided, however, that the failure to so notify the Indemnifying Parties will relieve the Indemnifying Parties from liability under this Agreement with respect to such Indemnity Claim only if, and only to the

extent that, such failure to notify the Indemnifying Parties results in material prejudice to the Indemnifying Parties of rights and defenses otherwise available to the Indemnifying Parties with respect to the Underlying Claim. Any Notice pursuant to this Section 10.3(a) shall set forth in reasonable detail, to the extent then available, the basis for such Indemnity Claim and an estimate of the amount of damages arising therefrom.

(b) If an Indemnity Claim does not result from or arise in connection with any Underlying Claim or legal proceedings by a third party, the Indemnifying Parties will have fifteen (15) calendar days following receipt of the Notice to issue a written response to the Indemnified Parties, indicating the Indemnifying Parties’ intention to either (i) contest the Indemnity Claim or (ii) accept the Indemnity Claim as valid. The Indemnifying Parties’ failure to provide such a written response within such fifteen (15) day period shall be deemed to be an acceptance of

the Indemnity Claim as valid. In the event that an Indemnity Claim is accepted as valid, the Indemnifying Parties shall, within fifteen (15) Business Days thereafter, pay the damages incurred by the Indemnified Parties in respect of the Underlying Claim in cash by wire transfer of immediately available funds to the account or accounts specified by the Indemnified Parties. To the extent appropriate, payments for indemnifiable damages made pursuant to Section 10 of the Agreement will be treated as adjustments to the Purchase Price.

(c) In the event an Indemnity Claim results from or arises in connection with any Underlying Claim or legal proceedings by a third party, the Indemnifying Parties shall have fifteen (15) calendar days following receipt of the Notice to send a Notice to the Indemnified Parties of their election to, at their sole cost and expense, assume the defense of any such Underlying Claim or legal proceeding; provided that such Notice of election shall contain a confirmation by the Indemnifying Parties of their obligation to hold harmless the Indemnified Parties with respect to damages arising from such Underlying Claim. The failure by the

Indemnifying Parties to elect to assume the defense of any such Underlying Claim within such fifteen (15) day period shall entitle the Indemnified Parties to undertake control of the defense of the Underlying Claim on behalf of and for the account and risk of the Indemnifying Parties in such manner as the Indemnified Parties may deem appropriate, including, but not limited to, settling the Underlying Claim. However, the parties controlling the defense of the Underlying Claim shall not settle or compromise such Underlying Claim without the prior written consent of the other parties, which consent shall not be unreasonably withheld or delayed. The non-controlling parties shall be entitled to participate in (but not control) the defense of any such action, with their own counsel and at their own expense.

- 11 -

(d) The Indemnifying Parties and the Indemnified Parties will cooperate reasonably, fully and in good faith with each other, at the sole expense of the Indemnifying Parties, in connection with the defense, compromise or settlement of any Underlying Claim including, without limitation, by making available to the other parties all pertinent information and witnesses within their reasonable control.

Injunctive Relief.

11.1 Damages Inadequate. Each party acknowledges that it would be impossible to measure in money the damages to the other party if there is a failure to comply with any covenants and provisions of this Agreement, and agrees that in the event of any breach of any covenant or provision, the other party to this Agreement will not have an adequate remedy at law.

11.2 Injunctive Relief. It is therefore agreed that the other party to this Agreement who is entitled to the benefit of the covenants and provisions of this Agreement which have been breached, in addition to any other rights or remedies which they may have, will be entitled to immediate injunctive relief to enforce such covenants and provisions, and that in the event that any such action or proceeding is brought in equity to enforce them, the defaulting or breaching party will not urge a defense that there is an

adequate remedy at law.

Arbitration.

Any dispute under this Agreement will be resolved by binding arbitration conducted in accordance with the rules and procedures of the American Arbitration Association as they are then in effect in the County of Los Angeles, State of California. In order to select an arbitrator, each party to the dispute will select an arbitrator of its choice through JAMS, and those selected arbitrators will then select by mutual agreement a single arbitrator through JAMS for the proceeding. The decision of the arbitrator will be final and binding on the parties to this Agreement, and judgment thereon may be entered in the Superior Court for the County of Bernardino or any other court having

jurisdiction. Each party to this Agreement will advance one-half of the arbitrator’s fees; however, all costs of the arbitration proceeding to enforce this Agreement, including attorneys’ fees and witness expenses, will be paid by the party against whom the arbitrator rules. It is expressly agreed that the parties to any such arbitration may take discovery as contemplated and provided for by California Code of Civil Procedure §1283.05. Notwithstanding anything herein to the contrary, the parties hereto will not be required to submit a claim to arbitration if the claim is for temporary or preliminary equitable or injunctive relief that could not practicably be heard in a timely fashion through the arbitration process.

Waivers.

If any party at any time waives any rights hereunder resulting from any breach by the other party of any of the provisions of this Agreement, such waiver is not to be construed as a continuing waiver of other breaches of the same or other provisions of this Agreement. Resort to any remedies referred to herein will not be construed as a waiver of any other rights and remedies to which such party is entitled under this Agreement or otherwise.

- 12 -

Successors and Assigns.

Each covenant and representation of this Agreement will inure to the benefit of and be binding upon each of the parties, their personal representatives, assigns and other successors in interest.

Entire and Sole Agreement.

This Agreement and its exhibits and schedules constitute the entire agreement between the parties and supersede all other agreements, representations, warranties, statements, promises and undertakings, whether oral or written, with respect to the subject matter of this Agreement. This Agreement may be modified or amended only by a written agreement signed by the parties against whom the amendment is sought to be enforced.

Governing Law.

This Agreement will be governed by the laws of California without giving effect to applicable conflict of laws provisions. With respect to any disputes arising out of or relating to this Agreement, each party agrees that any disputes that are not resolved by the parties will be submitted to binding arbitration with the American Arbitration Association located in Santa Xxxxxxx County, California; provided, that any party may seek equitable remedies under this Agreement without referring them to binding arbitration.

Counterparts.

This Agreement may be executed simultaneously in any number of counterparts, each of which counterparts will be deemed to be an original, and such counterparts will constitute but one and the same instrument.

Attorneys’ Fees and Costs.

In the event that either party must resort to legal action in order to enforce the provisions of this Agreement or to defend such action, the prevailing party will be entitled to receive reimbursement from the nonprevailing party for all reasonable attorneys’ fees and all other costs incurred in commencing or defending such action, or in enforcing this Agreement, including but not limited to post judgment costs.

Assignment.

This Agreement may not be assigned by any party without prior written consent of the other parties.

Remedies.

Except as otherwise expressly provided herein, none of the remedies set forth in this Agreement are intended to be exclusive, and each party will have all other remedies now or hereafter existing at law, in equity, by statute or otherwise. The election of any one or more remedies will not constitute a waiver of the right to pursue other available remedies.

- 13 -

Section Headings.

The section headings in this Agreement are included for convenience only, are not a part of this Agreement and will not be used in construing it.

Severability.

In the event that any provision or any part of this Agreement is held to be illegal, invalid or unenforceable, such illegality, invalidity or unenforceability will not affect the validity or enforceability of any other provision or part of this Agreement.

Notices.

Each notice or other communication hereunder must be in writing and will be deemed to have been duly given on the earlier of (i) the date on which such notice or other communication is actually received by the intended recipient thereof, or (ii) the date five (5) days after the date such notice or other communication is mailed by registered or certified mail (postage prepaid) to the intended recipient at the following address (or at such other address as the intended recipient will have specified in a written notice given to the other parties hereto):

If to Buyer or Buyer’s Subsidary:

000 Xxxxxxx Xxxxxx

Xxxxx Xxxxxxx, Xxxxxxxxxx 00000

Attention; Xxxxxxx Xxxx, Chief Executive Officer

Telephone Number: (000) 000-0000

Facsimile Number: (000) 000-0000

Email Address: xxxxxxx@xxxxxxxxx.xxx

If to Seller:

RadioLoyalty, Inc.

000 Xxxxxxx Xxxxxx

Xxxxx Xxxxxxx, Xxxxxxxxxx 00000

Attention; Xxxxx Xxxxxxx, President

Telephone Number: (000) 000-0000

Facsimile Number: (000) 000-0000

Email Address: xxxxx@xxxxxxxxxxxx.xxx

- 14 -

Publicity.

Except as may be required in order for a party to comply with applicable laws, rules, or regulations or to enable a party to comply with this Agreement, no press release, notice to any third party or other publicity concerning the transactions contemplated by this Agreement will be issued, given or otherwise disseminated without the prior approval of each of the parties hereto; provided, however, that such approval will not be unreasonably withheld.

Confidentiality.

Any information, including but not limited to data, business information (including customer lists and prospects), technical information, computer programs and documentation, programs, files, specifications, drawings, sketches, models, samples, tools or other data, oral, written or otherwise, (hereinafter called “Information”), furnished or disclosed by one party to the other for the purpose of the contemplated transaction herein, will remain the disclosing party’s property until the Closing at which time all such Information will become the property of Buyer. All copies of such Information in written, graphic or other tangible form must be returned to the disclosing party

immediately upon written request if the transaction contemplated herein is not consummated. Unless such Information was previously known to receiving party free of any obligation to keep it confidential, or has been or is subsequently made public by the disclosing party or a third party, it must be kept confidential by the receiving party, will be used only in performing due diligence pursuant to this Agreement, and may not be used for other purposes except upon such terms as may be agreed upon between Seller and Buyer in writing.

(Signatures on following page.)

- 15 -

IN WITNESS WHEREOF, this Agreement has been entered into as of the date first above written.

| Seller: | RadioLoyalty, Inc. | ||

| a California corporation | |||

|

By:

|

|||

| Xxxxx Xxxxxxx, President | |||

| Buyer’s Subsidiary: | StreamTrack Media, Inc. | ||

| a California corporation | |||

|

Date

|

By:

|

||

| Xxxxxxx Xxxx, Chief Executive Officer | |||

- 16 -

EXHIBIT A

XXXX OF SALE OF ASSETS

1

XXXX OF SALE OF ASSETS

RadioLoyalty, Inc., a California corporation (“Seller”), hereby sells and conveys to StreamTrack Media, Inc. (Buyer’s Subsidiary), a wholly owned subsidiary of Lux Digital Pictures, Inc., a Wyoming corporation (“Buyer”), all of the tangible and intangible assets (the “Assets”) to be transferred to Buyer’s Subsidiary pursuant to the terms of that certain Asset Purchase Agreement (“Agreement”), made and entered into as of August 31, 2012, by and among Lux Digital Pictures, Inc., a Wyoming corporation, StreamTrack Media Inc., a California corporation, and RadioLoyalty, a California corporation, and assigns the Assets to Buyer’s Subsidiary forever,

free and clear of all liens and encumbrances other than those assumed by the Buyer and Buyer’s Subsidiary in the Agreement.

Seller warrants and agrees to defend the title to all of the Assets for the benefit of Buyer’s Subsidiary and assigns against all persons.

IN WITNESS WHEREOF, Seller has signed and delivered this Xxxx of Sale to Buyer’s Subsidiary on August 31, 2012 at Los Angeles, California.

| RadioLoyalty, Inc. | |||

| a California corporation | |||

|

|

By:

|

||

| Xxxxx Xxxxxxx, President | |||

2

EXHIBIT B

CERTIFICATE OF OBLIGATION TO ISSUE SHARES

1

CERTIFICATE OF OBLIGATION TO ISSUE SHARES

Lux Digital Pictures, Inc., a Wyoming corporation (“Buyer”) hereby covenants to issue to RadioLoyalty, Inc., a California corporation (“Seller”), after the Closing of the Asset Purchase Agreement, dated August 31, 2012, by and between Buyer and Seller, and within five (5) business days after the recording of Amended and Restated Articles of Incorporation with the Wyoming Secretary of State by the Buyer effecting the next reverse split of its issued and outstanding common stock, issue to the Seller a number of shares of Buyer’s common stock (the “Shares”) such that on the date of the issuance of the Shares, the Seller and its affiliates will own a number of shares of

the Buyer’s common stock equal to approximately 90% of the total issued and outstanding shares of Buyer’s common stock, including and taking into account all shares of the Buyer’s common stock already owned by the Seller and its affiliates on the Share issuance date, and assuming the conversion of all outstanding Series A Convertible Preferred Stock of the Buyer; provided, that the calculation of the number of Shares issuable to the Seller pursuant to this Certificate will reflect that the dilution caused by outstanding shares of the Buyer’s common stock that are in the public float on the Share issuance date will be borne 90% by the Seller and 10% by the holders of the Buyer’s outstanding Series A Convertible Preferred Stock (i.e. on the Share issuance date, the Seller will own 90% of the Buyer’s outstanding common stock that is not in the

Buyer’s public float and, assuming the conversion of all outstanding Series A Convertible Preferred Stock of Buyer on the Share issuance date, the holders of such Series A Convertible Preferred Stock will collectively own 10% of the Buyer’s outstanding common stock that is not in the Buyer’s public float).

IN WITNESS WHEREOF, Buyer has signed and delivered this Certificate to Seller on August 31, 2012 at Los Angeles, California.

| Lux Digital Pictures, Inc. | |||

| a Wyoming corporation | |||

|

By:

|

|||

| Xxxxxxx Xxxx, Chief Executive Officer | |||

2

EXHIBIT C

LIST OF ACQUIRED ASSETS

1

Exhibit C

List of Acquired Assets

Buyer and the Buyer’s Subsidiary expressly acknowledge receipt under separate cover of copies of all material contracts and each and every domain name referenced below in the Content List of this Exhibit comprising a portion of the acquired assets. The actual material contracts and specific domain names are subject to the confidentiality provisions of the Asset Purchase Agreement.

Content List:

5512 Domain Names

237 Agency/Advertiser Agreements

2

Exhibit C - Continued

|

Servers

|

135

|

Vendors

|

|

|

Switches

|

26

|

Net2Ez

|

|

|

Routers

|

4

|

COX

|

|

|

Firewalls

|

5

|

IMPULSE

|

|

|

Workstations

|

45

|

Godaddy

|

|

|

Laptops

|

5

|

Trustico

|

|

|

Phones

|

60

|

Moniker

|

|

|

Domains

|

xxxxxx.xxx

|

||

|

tcast

|

|||

|

Software Licenses

|

all digital

|

||

|

MS Server 2003

|

cpanel

|

||

|

MS Server 2008

|

Proton Labs

|

||

|

Windows XP

|

Qtrax/Brilliant

|

||

|

Windows 7

|

GD3

|

||

|

Adobe CS3, CS4

|

|||

|

Sugar CRM

|

|||

|

Platforms and Software

|

Databases

|

||

|

Listmanagement

|

RL user DB

|

||

|

LP Manager

|

Sugar CRM database

|

||

|

Xxxxx.xxxx

|

Datintel database

|

||

|

Admaximizer

|

206 repositories

|

||

|

Radioloyalty

|

|||

|

UniversalPlayer

|

|||

|

HDIRADIO

|

|||

|

xxxxxxxxxx.xxx

|

|||

|

Jetcast

|

|||

|

RL IOS APP

|

|||

|

RL HTML 5

|

|||

|

RL Andriod

|

|||

|

Slider

|

|||

|

Toolbar

|

|||

|

lenco media

|

|||

|

microgravity media

|

|||

|

Simply Lead Gen

|

|||

|

sugarcrm

|

|||

|

Replaceyour

|

|||

|

Discount Lead Network

|

|||

|

Student Matching Service(s)

|

|||

|

U.S. Xxx App. No. 13/559,503 - RadioLoyalty

|

|||

|

RL Blackberry Playbook APP

|

|||

3

Exhibit C - Continued

|

SERVERS

|

|

||||

|

IBM 3650

|

IBM 0000 | Xxxx Xxxxxx |

Xxxx Xxxxxxx

|

Xxxxxxxx

|

|

|

XX00X0X

|

XX00X0X

|

chassis-01

|

Xxxxxxxx

|

Xxxx 00

|

|

|

XX00X0X

|

XX00X0X

|

chassis-02

|

Korin

|

Core 02

|

|

|

KQ75T5F

|

KQ94K4K

|

chassis-03

|

yajirobe

|

Switch 1

|

|

|

KQ75T5X

|

KQ94K4G

|

chassis-04

|

yamcha

|

Switch 2

|

|

|

KQ93Y2W

|

KQ94K4W

|

chassis-05

|

tien

|

Switch 1

|

|

|

KQ75R5N

|

KQ94K5X

|

chassis-06

|

android17

|

Switch 2

|

|

|

KQ93Y8K

|

KQ94K5A

|

blades-0-60

|

android18

|

Switch 3

|

|

|

KQ93Y8L

|

KQ94K4V

|

db0

|

Switch 1

|

||

|

KQ95W0R

|

db1

|

Switch 2

|

|||

|

KQ94K4H

|

pbx01

|

Switch 1

|

|||

|

KQ94K5M

|

pbx02

|

Switch 2

|

|||

|

KQ94K4L

|

stagingdb

|

Switch 1

|

|||

|

KQ94K4N

|

devdb

|

Switch 2

|

|||

|

KQ94K5C

|

sbutil01

|

6500-01

|

|||

|

KQ94K4R

|

1850 01-06

|

6500-02

|

|||

|

KQ94K5L

|

force 10 x 2

|

||||

|

KQ95W2H

|

cisco 3560

|

||||

|

KQ94K5T

|

|||||

|

KQ94K5H

|

|||||

|

KQ94K4P

|

|||||

|

KQ94K5B

|

|||||

|

KQ94K4X

|

|||||

|

KQ94K5W

|

|||||

|

KQ94K4D

|

|||||

|

KQ94K5P

|

|||||

|

KQ94K4T

|

|||||

|

KQ94K5N

|

|||||

|

KQ94K5V

|

|||||

| KQ94K5K | |||||

| XX00X0X | |||||

| XX00X0X | |||||

| web01 | |||||

| web02 | |||||

| web03 | |||||

| web04 | |||||

| web05 | |||||

| web06 | |||||

| lax2-db01 | |||||

| lax2-db02 | |||||

| lax2-db03 | |||||

| lax2-db04 | |||||

| lax2-db05 | portal-01 | ||||

| itutil01 | portal-02 | ||||

4

Exhibit C - Continued

|

Workstations

|

MISC

|

|

30 Lenovo

|

big xerox

|

|

10 Dell

|

big dell

|

|

3 IMAC

|

switches

|

|

5 Laptops

|

xxx switches

|

|

4x TVs

|

|

Repository List:

|

|

VMCToGMOD

|

|

admaxadserver

|

|

admaximizer

|

|

admaximizer2

|

|

admaximizerads

|

|

admaximizerapi

|

|

admaximizernetwork

|

|

admaxmedia

|

|

admaxv2dev

|

|

adtagsext

|

|

alre

|

|

amcatphoneapi

|

|

aoldomains

|

|

autodialer

|

|

bidnotifier

|

|

bigautoexchange

|

|

bizopper

|

|

bobeubanks

|

|

breastcancer

|

|

xxxxx.xxxx

|

|

buydiscount

|

|

calls

|

|

cancelsites

|

|

cartraderlive

|

|

cbcredit

|

|

ccproc

|

|

cellcard

|

|

cerberus

|

|

clg

|

|

clg_site

|

|

clockin

|

|

codebase

|

|

commerceplanet

|

|

coreg

|

|

costa_rica_update

|

|

cryptoproxy

|

5

Exhibit C - Continued

|

csclub

|

|

csrwire

|

|

dartapi

|

|

dbscripts

|

|

debtblueamerica

|

|

debtwrestler

|

|

demosites

|

|

dialerhub

|

|

discountleadnetwork

|

|

discountnetwork

|

|

ds_cc_reports

|

|

ds_portal_reports

|

|

dsleadloader

|

|

easybizzonline

|

|

eauctionautos

|

|

emailapi

|

|

exporter

|

|

exporter_old

|

|

fighting

|

|

fightingmobi

|

|

fightingweb

|

|

financialwellness

|

|

geoip

|

|

getmyonlinedegree

|

|

getmyonlinedegree_orig

|

|

gmod_cc_reports

|

|

gmod_portal_reports

|

|

gossipwidget

|

|

grssoap

|

|

xxxxxxxx.xxx

|

|

hoodiaedge

|

|

hotfreeprinting

|

|

housingdirect

|

|

ibillpay

|

|

iis

|

|

importer

|

|

ineedagooddiet

|

|

intellicast

|

|

interaccurate

|

|

internetcollegedirectory

|

|

invadmin

|

|

investinginsuccess

|

|

iventa

|

|

xxxxxxx.xxx

|

|

jetcrm

|

|

jobsites

|

|

kingsransom

|

|

leadgen

|

|

legacyarticles

|

6

Exhibit C - Continued

|

legacymedia

|

|

legacynetwork

|

|

lencomedia

|

|

lencomobile

|

|

lencomobile-mx

|

|

lencomultimedia

|

|

lencotechdev

|

|

liquid-cgi

|

|

listmanagement

|

|

livehelp-server

|

|

lp

|

|

media

|

|

memberapi

|

|

meta_harvester

|

|

mhealthsafeconnect

|

|

mms

|

|

mms_wordpress

|

|

montecitorei

|

|

montecitorei-wp

|

|

msprofitconfirmation

|

|

mychat

|

|

myfreeresumeonline

|

|

myonlinechat

|

|

mysoftwaretutor

|

|

mytechcard

|

|

mytechcardllc

|

|

nagios

|

|

netconfig

|

|

newave

|

|

newswidgetsite

|

|

nicacentury21

|

|

nwve

|

|

offmylists

|

|

omaramedia

|

|

onlinesupplier

|

|

onthenetdegree

|

|

opsReporting

|

|

osactionline

|

|

osal

|

|

osfulfill

|

|

osimaging

|

|

osjobs

|

|

parkeddomains

|

|

parknprofit

|

|

parknprofitExtra

|

|

pbx

|

|

pbxconfig

|

|

player

|

|

playercleanup

|

7

Exhibit C - Continued

|

pnpscripts

|

|

poweradmin

|

|

prequalify

|

|

projects

|

|

radioloyalty

|

|

radioloyaltydart

|

|

xxxxxxxxxx.xxx

|

|

replaceyour

|

|

repolist.php

|

|

repos.list

|

|

rlIphone

|

|

rlapi

|

|

rlconfigflash

|

|

rldevices

|

|

rlhtml5player

|

|

rliphone

|

|

rlplayerflash

|

|

rpc

|

|

rpcsoap

|

|

rt3-soap

|

|

rtx

|

|

sdinstore

|

|

session

|

|

sigdemo

|

|

signup

|

|

sitebuilder

|

|

sitebuilder.jud

|

|

sitebuildergenie

|

|

slider

|

|

smellaround

|

|

sms

|

|

sndslice

|

|

solidwavepc

|

|

squirrel

|

|

squirrelmail

|

|

staticsync

|

|

sugarcrm

|

|

superauctionpro

|

|

superflyadvertising

|

|

svnserve.authz

|

|

svnserve.conf

|

|

svnserve.passwd

|

|

systems

|

|

thefinancialhelpline

|

|

tsr

|

|

twittermaximizer

|

|

ultimatesearchguide

|

|

usajobnetworks

|

|

util

|

8

Exhibit C - Continued

|

validator

|

|

verifi

|

|

verifiqueryapi

|

|

virtualactivation

|

|

virtualmoneycenter

|

|

vistapacificaheights

|

|

vurtego

|

|

weatherwidgetsite

|

|

widgets

|

|

wordpress

|

|

wp-auto

|

|

wp-career

|

|

wp-insurance

|

|

wp-legal

|

|

xssrewriter

|

9

Exhibit C - Continued

|

Codebase Line Count (Partial) included RadioLoyalty and Meta Harvester Code that is not included below but included in the transaction:

|

||

|

App Store, Universal Player, HTML5 Player, Ios Player, Andriod Player, xxxxx.xxxx, list management, admaximizer, sugarcrm, LP Manager, Slider and the list of databases that power the above and below applications.

|

|

SLOC

|

Directory

|

SLOC-by-Language (Sorted) | |||||

|

29877

|

includes

|

php=29877

|

|||||

|

18103

|

top_dir

|

php=18097,xml=6

|

|||||

|

13808

|

tests

|

php=12848,xml=574,python=225,ansic=161

|

|||||

|

8021

|

amfphp

|

php=8000,xml=21

|

|||||

|

7434

|

notInUse

|

php=7434

|

|||||

|

4453

|

cron

|

php=4445,sh=8

|

|||||

|

2280

|

reps

|

php=2280

|

|||||

|

1621

|

webservices

|

php=1621

|

|||||

|

1152

|

station-guide

|

php=1152

|

|||||

|

1040

|

in-stream

|

php=1040

|

|||||

|

854

|

players

|

xml=854

|

|||||

|

560

|

configurator

|

php=320,xml=240

|

|||||

|

222

|

station-guideTes

|

php=222

|

|||||

|

160

|

loyalty

|

php=160

|

|||||

|

132

|

guide

|

php=132

|

|||||

|

125

|

bluehornet

|

xml=74,php=51

|

|||||

|

107

|

reporting

|

php=107

|

|||||

|

81

|

order

|

php=81

|

|||||

|

32

|

monitors

|

php=32

|

|||||

|

6

|

admaxmedia

|

php=6

|

|||||

|

2

|

adplayerz

|

php=2

|

|||||

|

0

|

about

|

(none)

|

|||||

|

0

|

animation

|

(none)

|

|||||

|

0

|

css

|

(none)

|

|||||

|

0

|

img

|

(none)

|

|||||

|

0

|

includes-site

|

(none)

|

|||||

|

0

|

js

|

(none)

|

|||||

|

0

|

launch-page

|

(none)

|

|||||

|

0

|

loyatly-platform

|

(none)

|

|||||

|

0

|

presentationDistribution

|

(none)

|

|||||

|

0

|

products

|

(none)

|

|||||

|

0

|

radio

|

(none)

|

|||||

|

0

|

services

|

(none)

|

|||||

|

0

|

tutorials

|

(none)

|

10

Exhibit C - Continued

| Totals grouped by language (dominant language first): | |||||

| php: | 87907 |

(97.60%)

|

|||

| xml: | 1769 |

(1.96%)

|

|||

| python: | 225 |

(0.25%)

|

|||

| ansic: | 161 |

(0.18%)

|

|||

| sh: | 8 |

(0.01%)

|

|||

| Total Physical Source Lines of Code (SLOC) = 90,070 | |||||

| SLOC |

Directory

|

SLOC-by-Language (Sorted) | |||

| 617 | top_dir |

python=617

|

|||

| 502 | imports |

python=502

|

|||

| 406 | tests |

python=406

|

|||

| 0 | cron |

(none)

|

|||

| 0 | docs |

(none)

|

|||

| 0 | software |

(none)

|

|||

| Totals grouped by language (dominant language first): | |||||

| python: |

1525 (100.00%)

|

||||

| Total Physical Source Lines of Code (SLOC) = 1,525 | |||||

11

EXHIBIT D

LIST OF ASSUMED LIABILITIES

1

Exhibit D

List of Assumed Liabilities

Buyer and Buy’s Subsidiary expressly acknowledges receipt under separate cover of copies of all material contracts referenced below in the Content List of this Exhibit D comprising a portion of the assumed liabilities. The Buyer’s Subsidiary is assuming these material contracts and the liabilities associated with them. The actual material contracts are subject to the confidentiality provisions of the Asset Purchase Agreement. The Buyer’s Subsidiary is also assuming the liabilities of the Seller that are listed and disclosed in the Seller’s Financial Statements, copies of which are attached to the Asset Purchase Agreement as Exhibit F.

Content List:

1124 Active Broadcasters Agreements

172 Publisher Agreements

96 Sales and Marketing Agreements

49 Affiliate and Network Agreements

2

EXHIBIT E

VALUATION OF ASSETS

1

Valuation of Capital

Structure

Radio Loyalty, Inc.

As of 5/31/2012

Issued on 8/31/2012

By

Axiom Valuation Solutions

Valuation of Capital Structure for Radio Loyalty

Table of Contents

Section 1: Engagement Overview

Section 2: Company Overview

Section 3: Industry Overview

Section 4: Valuation Theory and Analysis

Appendices

|

8/31/2012

|

Axiom Valuation Solutions

|

Page 2 of 63

|

Valuation of Capital Structure for Radio Loyalty

DETAILED TABLE OF CONTENTS

|

Table of Contents

|

2 | |||

|

Detailed Table of Contents

|

3 | |||

|

Index to Charts and Tables

|

4 | |||

|

Section 1: Engagement Overview

|

5 | |||

|

Limiting Conditions

|

5 | |||

|

Summary of Findings

|

7 | |||

|

Section 2: Company Overview

|

9 | |||

|

Company Overview

|

9 | |||

|

Management Team

|

9 | |||

|

Facilities

|

10 | |||

|

Capital Structure

|

10 | |||

|

Financial Analysis

|

10 | |||

|

Section 3: Industry Overview

|

13 | |||

|

Guideline Public Company Analysis

|

13 | |||

|

Multiples Applied

|

15 | |||

|

Guideline Transactions Analysis

|

20 | |||

|

Section 4: Valuation Theory and Analysis

|

21 | |||

|

Valuation Overview

|

21 | |||

|

Valuation and the Stage of Business Development

|

21 | |||

|

Risk versus Return

|

22 | |||

|

Calculating the Firm-Specific Cost of Capital

|

23 | |||

|

Enterprise Value

|

26 | |||

|

Appendix A: About Axiom Valuation Solutions

|

30 | |||

|

Appendix B: Professional Qualifications

|

31 | |||

|

Xxxxxxx X. Xxxxxxx, Ph.D.

|

31 | |||

|

Related Experience

|

32 | |||

|

Selected Publications

|

32 | |||

|

Appendix C: Valuation and Firm Financial Data

|

34 | |||

|

Appendix D: Industry Overview

|

51 | |||

|

Executive Summary

|

51 | |||

|

Key External Drivers

|

51 | |||

|

Current Performance

|

52 | |||

|

Depressed operations

|

52 | |||

|

Advertising dip led to restructuring

|

53 | |||

|

Expanding radio’s reach

|

53 | |||

|

Industry Outlook

|

54 | |||

|

Consolidation

|

54 | |||

|

Slow Recovery

|

54 | |||

|

Spotlight on satellite

|

55 | |||

|

Appendix E: The U.S Economic Outlook

|

56 | |||

|

General Overview

|

56 | |||

|

Gross Domestic Product and the Inflation Outlook

|

58 | |||

|

The Interest Rate Outlook

|

60 | |||

|

Summary

|

61 | |||

|

Appendix F: Certification and Conditions

|

62 | |||

|

Appraisal Certification

|

62 | |||

|

Statement Of Contingent And Limiting Conditions

|

63 |

|

8/31/2012

|

Axiom Valuation Solutions

|

Page 3 of 63

|

Valuation of Capital Structure for Radio Loyalty

|

INDEX TO CHARTS AND TABLES

|

||||

|

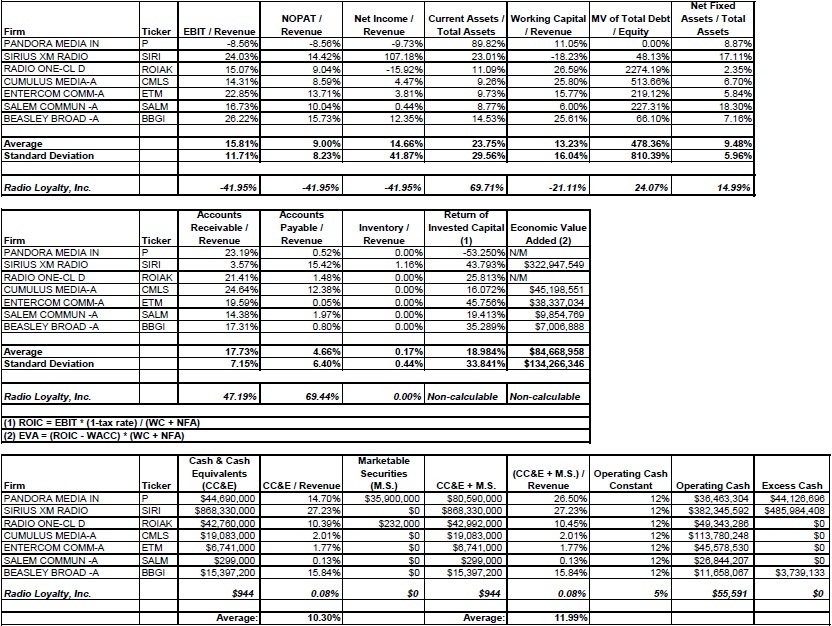

Table 1-1: Fair Value of Radio Loyalty’s Capital Structure

|

7 | |||

|

Table 1-2: Radio Loyalty Capital Structure at the Valuation Date

|

8 | |||

|

Table 1-3: Radio Loyalty Enterprise Valuation Results

|

8 | |||

|

Table 2-1: Radio Loyalty Capital Structure

|

10 | |||

|

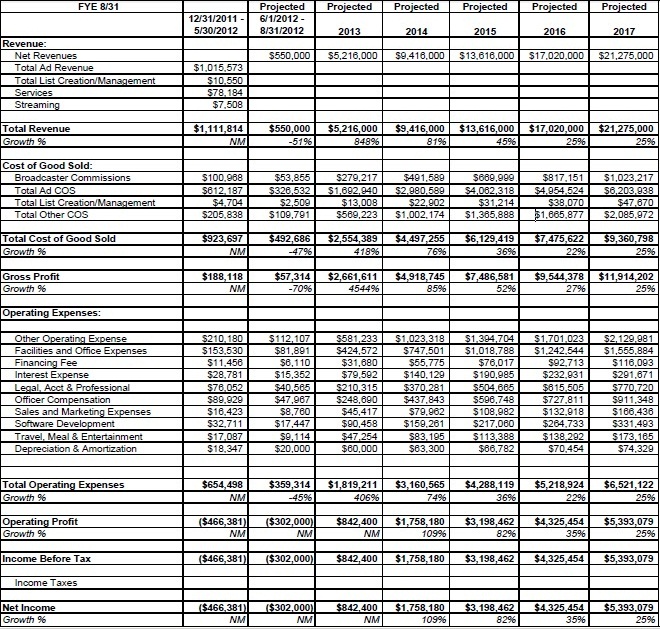

Table 2-2: Radio Loyalty Historical and Projected Income Statement

|

11 | |||

|

Table 2-3: Radio Loyalty Historical and Projected Income Statement

|

11 | |||

|

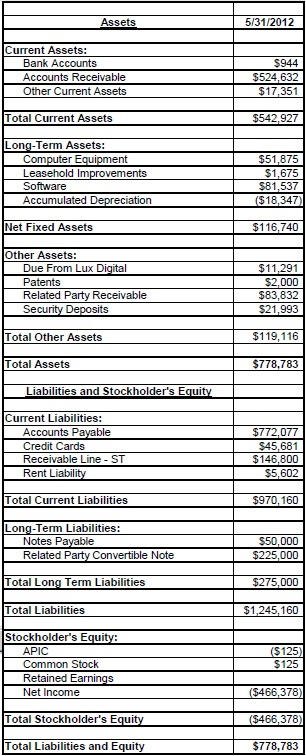

Table 2-4: Radio Loyalty Balance Sheet

|

12 | |||

|

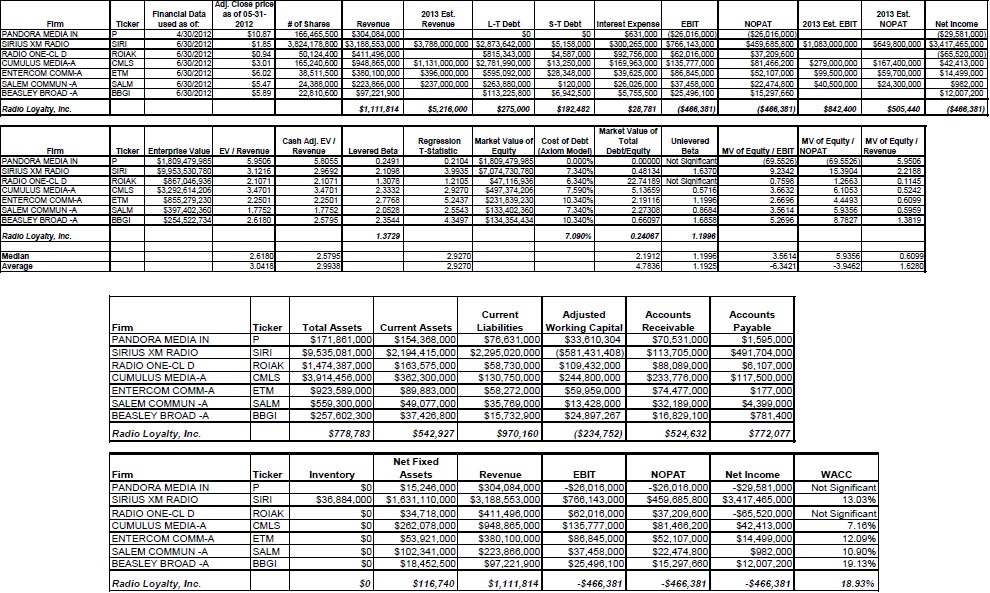

Table 3-1: Public Guideline Firms – Financial Data

|

16 | |||

|

Table 3-2: Public Guideline Firms –Ratio Analysis

|

17 | |||

|

Table 3-3: Valuation of Radio Loyalty using the Median Projected Multiple

|

19 | |||

|

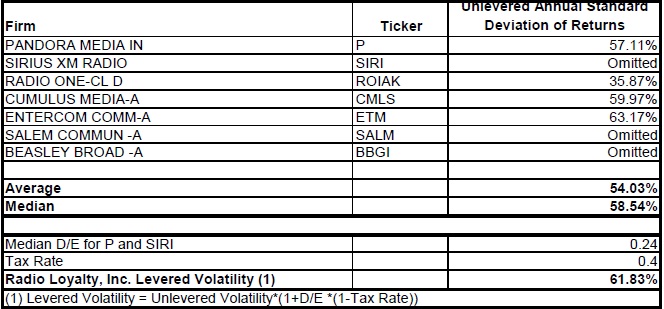

Table 3-4: Radio Loyalty Common Stock Price Volatility Calculation

|

20 | |||

|

Table 4-1: Stages of Business Development

|

21 | |||

|

Table 4-2: Valuation Approaches for Different Stages of Business Development

|

22 | |||

|

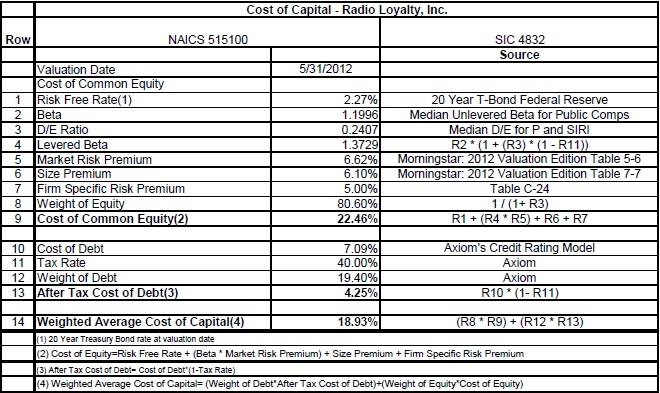

Table 4-3: Calculating the Cost of Capital for Radio Loyalty

|

24 | |||

|

Table 4-4: Discounted Cash Flow Analysis

|

25 | |||

|

Table 4-5: Enterprise Valuation Summary

|

26 | |||

|

Table 4-6: Contingent Claims Model Inputs

|

27 | |||

|

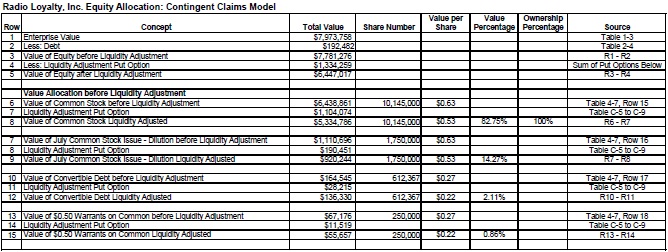

Table 4-7: Contingent Claims Model Value Allocation

|

28 | |||

|

Table C-1: Convertible Debt Income Stream and Conversion

|

34 | |||

|

Table C-2: Warrant Schedule

|

35 | |||

|

Table C-3: Common Call Option Pricing

|

35 | |||

|

Table C-4: $0.50 Warrants and Convertible Debt Exercise Pricing

|

36 | |||

|

Table C-5: Common Stock Liquidity Discount Put Option

|

36 | |||

|

Table C-6: July Common Stock Issue Liquidity Discount Put Option

|

37 | |||

|

Table C-7: Convertible Debt Liquidity Discount Put Option

|

37 | |||

|

Table C-8: $0.50 Warrant Liquidity Discount Put Option

|

38 | |||

|

Table C-9: Stock Price Data for Public Guideline Firms

|

39 | |||

|

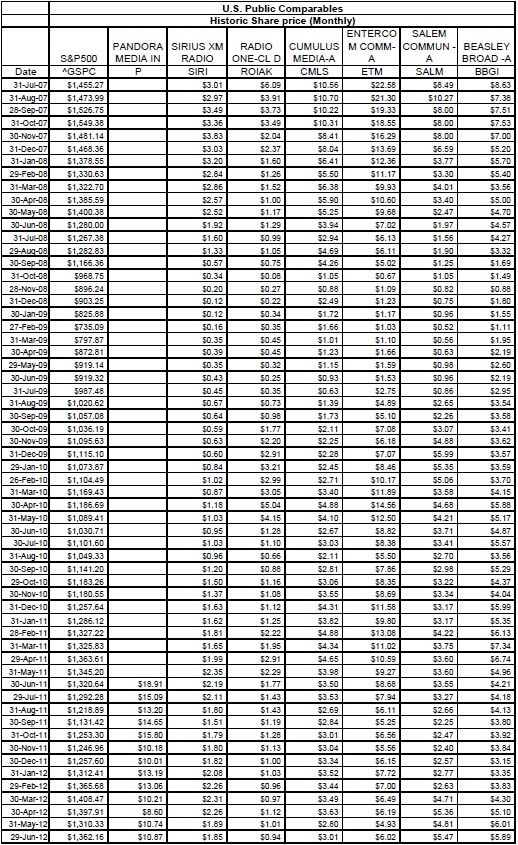

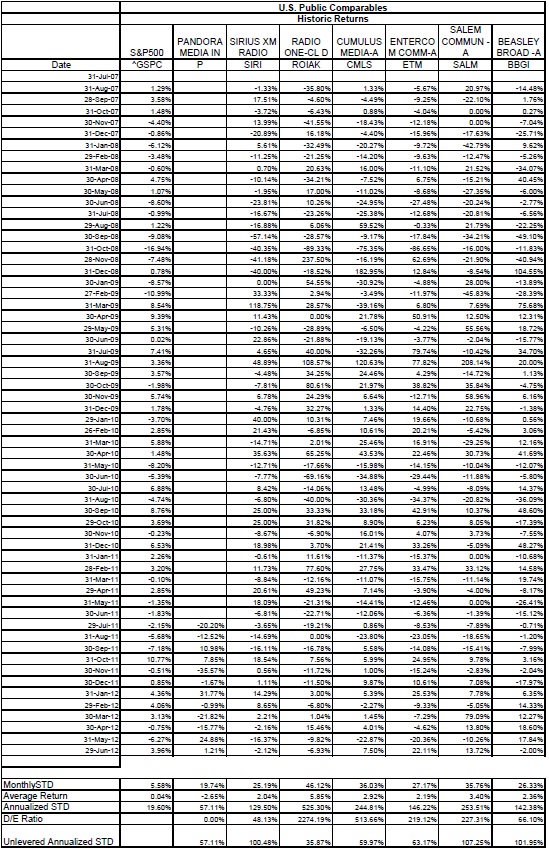

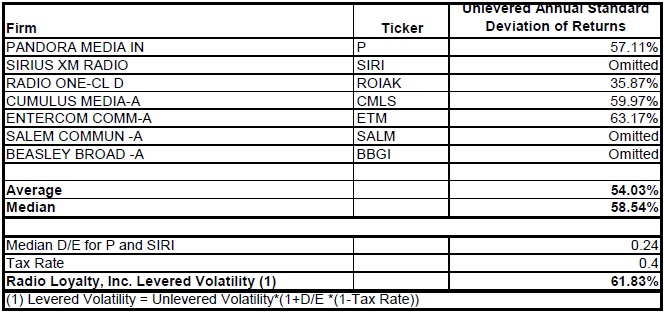

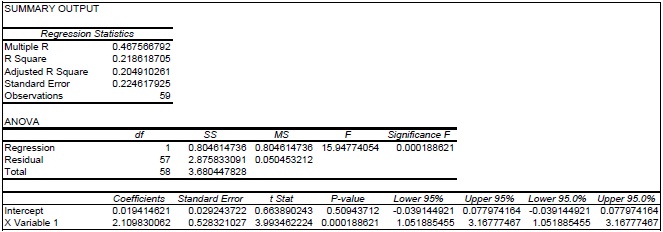

Table C-10: Stock Return Data for Public Guideline Firms

|

40 | |||

|

Table C-11: Radio Loyalty Common Stock Price Volatility Calculation

|

41 | |||

|

Table C-12: P Beta Calculation

|

42 | |||

|

Table C-13: SIRI Beta Calculation

|

42 | |||

|

Table C-14: ROIAK Beta Calculation

|

42 | |||

|

Table C-15: CMLS Beta Calculation

|

43 | |||

|

Table C-16: ETM Beta Calculation

|

43 | |||

|

Table C-17: XXXX Beta Calculation

|

43 | |||

|

Table C-18: BBGI Beta Calculation

|

44 | |||

|

Table C-19: Weighted Average Cost of Capital of Public Guideline Firms

|

45 | |||

|

Table C-20: Financial Data of Public Guideline Firms for the Credit Rating Model

|

46 | |||

|

Table C-21: Cost of Debt for Public Guideline Firms

|

46 | |||

|

Table C-22: D/E Ratio for Public Guideline Firms

|

47 | |||

|

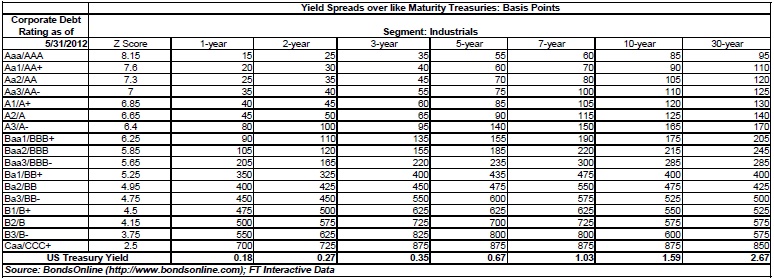

Table C-23: Corporate Yield Spreads in Industrial Segment as of 5/31/2012

|

48 | |||

|

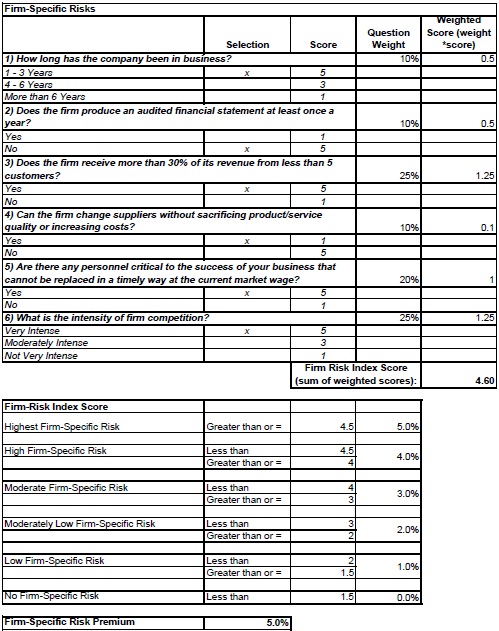

Table C-24: Firm Specific Risk Premium

|

49 | |||

|

Table C-25: Radio Loyalty Change in Net Fixed Assets Projections

|

49 | |||

|

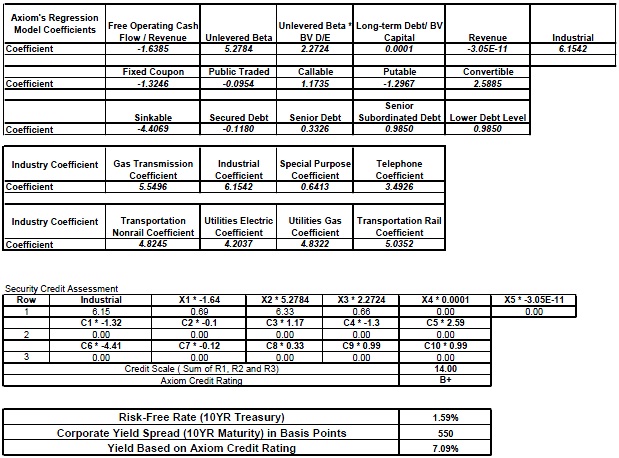

Table C-26: Calculation of Cost of Debt

|

50 | |||

|

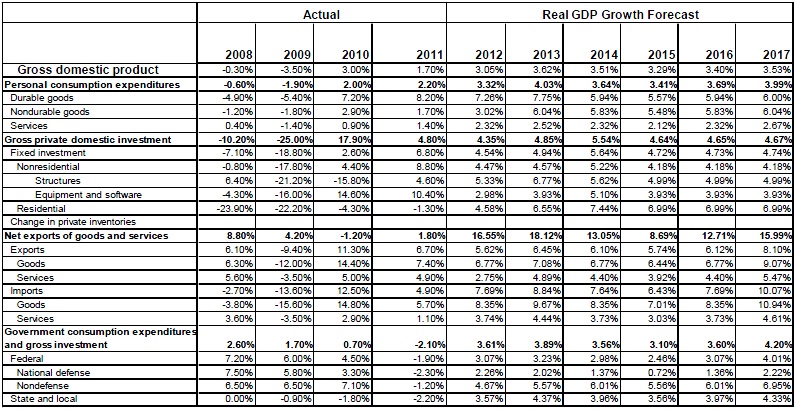

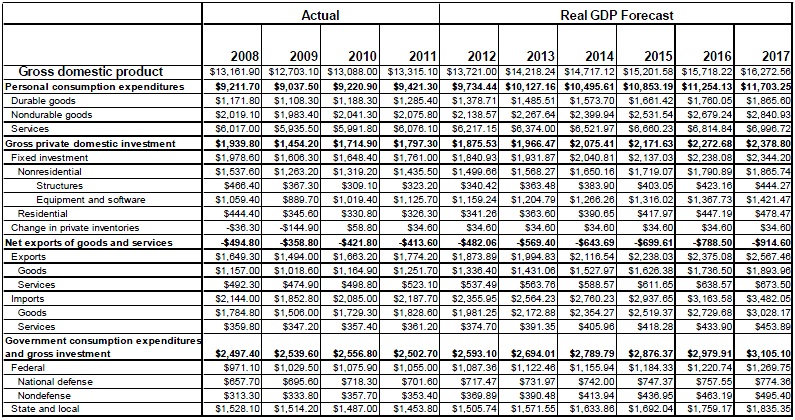

Table 3-1: Real GDP Growth Forecast

|

58 | |||

|

Table 3-2: Real GDP Forecast in Billions of Dollars

|

58 | |||

|

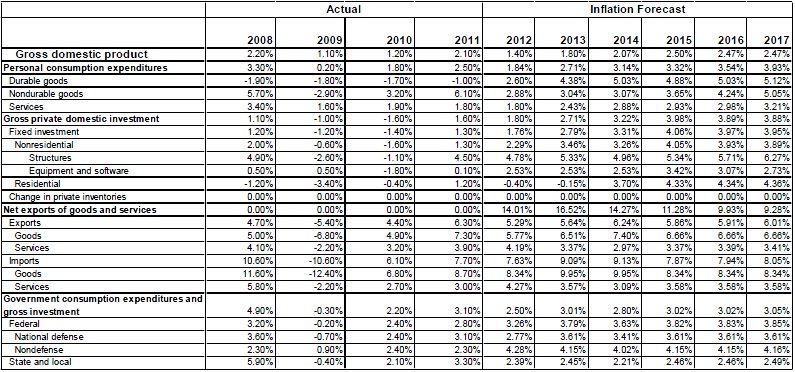

Table 3-3: Inflation Forecast

|

59 | |||

|

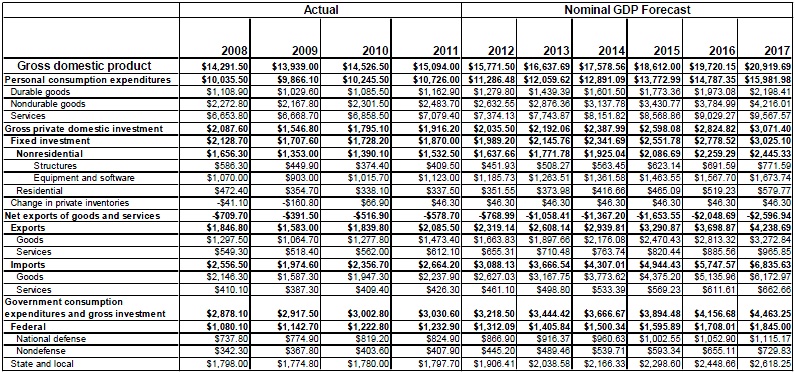

Table 3-4: Nominal GDP Forecast in Billions of Dollars

|

60 | |||

|

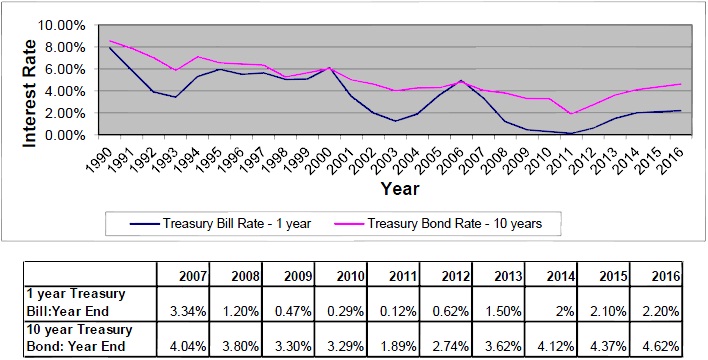

Chart 3-5: Interest Rate Forecast

|

60 | |||

|

8/31/2012

|

Axiom Valuation Solutions

|

Page 4 of 63

|

Valuation of Capital Structure for Radio Loyalty

Section 1: Engagement Overview

September 6, 2012

Mr. Xxxxxxx Xxxx

President & CEO

Radio Loyalty, Inc.

000 Xxxxxxx Xxxxxx

Xxxxx Xxxxxxx, XX 00000

Dear Xx. Xxxx,

Pursuant to your request, Axiom Valuation Solutions has prepared an analysis with respect to the fair value of the equity components of Radio Loyalty, as of 5/31/2012.1

This letter is intended to provide you with an overview of the purpose and scope of our analyses and our conclusions. Please refer to the attached report for a discussion and presentation of the analyses performed in connection with this engagement.

The standard of value underlying our analysis is fair value. Fair value is defined as:

The amount at which an asset (liability) could be bought (incurred) or sold (settled) in a current transaction between willing parties, that is, other than in a forced or liquidation sale.