LOAN AGREEMENT Fixed Rate Dated as of August 17, 2006 between BEHRINGER HARVARD FERNCROFT, LLC as Borrower, and BARCLAYS CAPITAL REAL ESTATE INC., as Lender

Exhibit 10.1

Fixed Rate

Dated as of August 17, 2006

between

BEHRINGER HARVARD FERNCROFT, LLC

as Borrower,

and

BARCLAYS CAPITAL

REAL ESTATE INC.,

as Lender

TABLE OF CONTENTS

|

|

|

|

Page |

|

|

ARTICLE 1 |

|

DEFINED TERMS AND CONSTRUCTION GUIDELINES |

|

1 |

|

|

|

|

|

|

|

Section 1.01 |

|

Defined Terms |

|

1 |

|

Section 1.02 |

|

General Construction |

|

15 |

|

|

|

|

|

|

|

ARTICLE 2 |

|

MAXIMUM LOAN AMOUNT; PAYMENT TERMS; ADVANCES; DEFEASANCE |

|

15 |

|

|

|

|

|

|

|

Section 2.01 |

|

Commitment to Lend |

|

15 |

|

Section 2.02 |

|

Calculation of Interest |

|

15 |

|

Section 2.03 |

|

Payment of Principal and Interest |

|

16 |

|

Section 2.04 |

|

Payments Generally |

|

17 |

|

Section 2.05 |

|

Prepayment Rights |

|

18 |

|

|

|

|

|

|

|

ARTICLE 3 |

|

CASH MANAGEMENT |

|

22 |

|

|

|

|

|

|

|

Section 3.01 |

|

Lockbox |

|

22 |

|

Section 3.02 |

|

Transfers to Cash Management Account; Trigger Event |

|

22 |

|

|

|

|

|

|

|

ARTICLE 4 |

|

ESCROW AND RESERVE REQUIREMENT |

|

23 |

|

|

|

|

|

|

|

Section 4.01 |

|

Creation and Maintenance of Escrows and Reserves |

|

23 |

|

Section 4.02 |

|

Tax Escrow |

|

24 |

|

Section 4.03 |

|

Insurance Premium Escrow |

|

25 |

|

Section 4.04 |

|

Immediate Repair Escrow Account |

|

26 |

|

Section 4.05 |

|

Replacement Reserve Account |

|

27 |

|

Section 4.06 |

|

TI/LC Reserve Account |

|

27 |

|

Section 4.07 |

|

TI/LC Designated Reserve Account |

|

28 |

|

Section 4.08 |

|

Earnout Reserve Account |

|

29 |

|

Section 4.09 |

|

Vacant Space Reserve Account |

|

30 |

|

|

|

|

|

|

|

ARTICLE 5 |

|

COMPLETION OF REPAIRS RELATED TO RESERVE ACCOUNTS; CONDITIONS TO RELEASE OF FUNDS |

|

31 |

|

|

|

|

|

|

|

Section 5.01 |

|

Conditions Precedent to Disbursements from Certain Reserve Accounts |

|

31 |

|

Section 5.02 |

|

Waiver of Conditions to Disbursement |

|

33 |

|

Section 5.03 |

|

Direct Payments to Suppliers and Contractors |

|

33 |

|

Section 5.04 |

|

Performance of Reserve Items |

|

34 |

|

|

|

|

|

|

|

ARTICLE 6 |

|

LOAN SECURITY AND RELATED OBLIGATIONS |

|

35 |

|

|

|

|

|

|

|

Section 6.01 |

|

Security Instrument and Assignment of Rents and Leases |

|

35 |

|

Section 6.02 |

|

Assignment of Property Management Contract |

|

35 |

|

Section 6.03 |

|

Assignment of Operating Agreements |

|

35 |

i

|

Section 6.04 |

|

Pledge as Property; Grant of Security Interest |

|

35 |

|

Section 6.05 |

|

Environmental Indemnity Agreement |

|

35 |

|

Section 6.06 |

|

Guaranty of Borrower Sponsors |

|

35 |

|

Section 6.07 |

|

Letter of Credit |

|

35 |

|

|

|

|

|

|

|

ARTICLE 7 |

|

SINGLE PURPOSE ENTITY REQUIREMENTS |

|

36 |

|

|

|

|

|

|

|

Section 7.01 |

|

Commitment to be a Single Purpose Entity |

|

36 |

|

Section 7.02 |

|

Definition of Single Purpose Entity |

|

37 |

|

|

|

|

|

|

|

ARTICLE 8 |

|

REPRESENTATIONS AND WARRANTIES |

|

40 |

|

|

|

|

|

|

|

Section 8.01 |

|

Organization; Legal Status |

|

40 |

|

Section 8.02 |

|

Power; Authorization; Enforceable Obligations |

|

40 |

|

Section 8.03 |

|

No Legal Conflicts |

|

41 |

|

Section 8.04 |

|

No Litigation |

|

41 |

|

Section 8.05 |

|

Business Purpose of Loan |

|

41 |

|

Section 8.06 |

|

Warranty of Title |

|

41 |

|

Section 8.07 |

|

Condition of the Property |

|

42 |

|

Section 8.08 |

|

No Condemnation |

|

42 |

|

Section 8.09 |

|

Requirements of Law |

|

42 |

|

Section 8.10 |

|

Operating Permits |

|

42 |

|

Section 8.11 |

|

Separate Tax Xxx |

|

00 |

|

Xxxxxxx 0.00 |

|

Xxxxx Xxxx |

|

42 |

|

Section 8.13 |

|

Adequate Utilities |

|

42 |

|

Section 8.14 |

|

Public Access |

|

42 |

|

Section 8.15 |

|

Boundaries |

|

43 |

|

Section 8.16 |

|

Mechanic Liens |

|

43 |

|

Section 8.17 |

|

Assessments |

|

43 |

|

Section 8.18 |

|

Insurance |

|

43 |

|

Section 8.19 |

|

Leases |

|

43 |

|

Section 8.20 |

|

Management Agreement |

|

44 |

|

Section 8.21 |

|

Financial Condition |

|

44 |

|

Section 8.22 |

|

Taxes |

|

44 |

|

Section 8.23 |

|

No Foreign Person |

|

44 |

|

Section 8.24 |

|

Federal Regulations |

|

44 |

|

Section 8.25 |

|

Investment Company Act; Other Regulations |

|

44 |

|

Section 8.26 |

|

ERISA |

|

44 |

|

Section 8.27 |

|

No Illegal Activity as Source of Funds |

|

44 |

|

Section 8.28 |

|

Compliance with Anti-Terrorism, Embargo, Sanctions and Anti-Money Laundering Laws |

|

45 |

|

Section 8.29 |

|

Brokers and Financial Advisors |

|

45 |

|

Section 8.30 |

|

Complete Disclosure; No Change in Facts or Circumstances |

|

45 |

|

Section 8.31 |

|

Survival |

|

45 |

ii

|

ARTICLE 9 |

|

BORROWER COVENANTS |

|

45 |

|

|

|

|

|

|

|

Section 9.01 |

|

Payment of Debt and Performance of Obligations |

|

45 |

|

Section 9.02 |

|

Payment of Taxes and Other Lienable Charges |

|

45 |

|

Section 9.03 |

|

Insurance |

|

46 |

|

Section 9.04 |

|

Obligations upon Condemnation or Casualty |

|

50 |

|

Section 9.05 |

|

Inspections and Right of Entry |

|

55 |

|

Section 9.06 |

|

Leases and Rents |

|

55 |

|

Section 9.07 |

|

Use of Property |

|

56 |

|

Section 9.08 |

|

Maintenance of Property |

|

56 |

|

Section 9.09 |

|

Waste |

|

57 |

|

Section 9.10 |

|

Compliance with Laws |

|

57 |

|

Section 9.11 |

|

Financial Reports, Books and Records |

|

57 |

|

Section 9.12 |

|

Performance of Other Agreements |

|

59 |

|

Section 9.13 |

|

Existence; Change of Name; Location as a Registered Organization |

|

59 |

|

Section 9.14 |

|

Property Management |

|

60 |

|

Section 9.15 |

|

ERISA |

|

60 |

|

Section 9.16 |

|

Compliance with Anti-Terrorism, Embargo, Sanctions and Anti-Money Laundering Laws |

|

61 |

|

Section 9.17 |

|

Deposit of Additional Collateral |

|

61 |

|

|

|

|

|

|

|

ARTICLE 10 |

|

NO TRANSFERS OR ENCUMBRANCES; DUE ON SALE |

|

61 |

|

|

|

|

|

|

|

Section 10.01 |

|

Prohibition Against Transfers |

|

61 |

|

Section 10.02 |

|

Lender Approval |

|

61 |

|

Section 10.03 |

|

Intentionally Deleted |

|

62 |

|

Section 10.04 |

|

Other Releases of the Mortgaged Property |

|

62 |

|

Section 10.05 |

|

Anti-Terrorism Compliance; Substantive Consolidation Opinion |

|

62 |

|

|

|

|

|

|

|

ARTICLE 11 |

|

EVENTS OF DEFAULT; REMEDIES |

|

63 |

|

|

|

|

|

|

|

Section 11.01 |

|

Events of Default |

|

63 |

|

Section 11.02 |

|

Remedies |

|

65 |

|

Section 11.03 |

|

Cumulative Remedies; No Waiver; Other Security |

|

67 |

|

Section 11.04 |

|

Enforcement Costs |

|

67 |

|

Section 11.05 |

|

Application of Proceeds |

|

67 |

|

|

|

|

|

|

|

ARTICLE 12 |

|

NONRECOURSE – LIMITATIONS ON PERSONAL LIABILITY |

|

68 |

|

|

|

|

|

|

|

Section 12.01 |

|

Nonrecourse Obligation |

|

68 |

|

Section 12.02 |

|

Personal Liability for Certain Losses |

|

68 |

|

Section 12.03 |

|

Full Personal Liability |

|

69 |

|

Section 12.04 |

|

No Impairment |

|

69 |

|

Section 12.05 |

|

No Waiver of Certain Rights |

|

69 |

|

|

|

|

|

|

|

ARTICLE 13 |

|

INDEMNIFICATION |

|

69 |

|

|

|

|

|

|

|

Section 13.01 |

|

Indemnification Against Claims |

|

69 |

|

Section 13.02 |

|

Duty to Defend |

|

70 |

iii

|

ARTICLE 14 |

|

SUBROGATION; NO USURY VIOLATIONS |

|

70 |

|

|

|

|

|

|

|

Section 14.01 |

|

Subrogation |

|

70 |

|

Section 14.02 |

|

No Usury |

|

70 |

|

|

|

|

|

|

|

ARTICLE 15 |

|

SALE OR SECURITIZATION OF LOAN |

|

71 |

|

|

|

|

|

|

|

Section 15.01 |

|

Splitting the Note |

|

71 |

|

Section 15.02 |

|

Lender’s Rights to Sell or Securitize |

|

72 |

|

Section 15.03 |

|

Dissemination of Information |

|

72 |

|

Section 15.04 |

|

Securitization Indemnification |

|

72 |

|

|

|

|

|

|

|

ARTICLE 16 |

|

BORROWER FURTHER ACTS AND ASSURANCES PAYMENT OF SECURITY RECORDING CHARGES |

|

73 |

|

|

|

|

|

|

|

Section 16.01 |

|

Further Acts |

|

73 |

|

Section 16.02 |

|

Replacement Documents |

|

73 |

|

Section 16.03 |

|

Borrower Estoppel Certificates |

|

74 |

|

Section 16.04 |

|

Recording Costs |

|

75 |

|

Section 16.05 |

|

Publicity |

|

75 |

|

|

|

|

|

|

|

ARTICLE 17 |

|

LENDER CONSENT |

|

75 |

|

|

|

|

|

|

|

Section 17.01 |

|

No Joint Venture; No Third Party Beneficiaries |

|

75 |

|

Section 17.02 |

|

Lender Approval |

|

75 |

|

Section 17.03 |

|

Performance at Borrower’s Expense |

|

75 |

|

|

|

|

|

|

|

ARTICLE 18 |

|

MISCELLANEOUS PROVISIONS |

|

76 |

|

|

|

|

|

|

|

Section 18.01 |

|

Notices |

|

76 |

|

Section 18.02 |

|

Entire Agreement; Modifications; Time of Essence |

|

77 |

|

Section 18.03 |

|

Binding Effect; Joint and Several Obligations |

|

77 |

|

Section 18.04 |

|

Duplicate Originals; Counterparts |

|

77 |

|

Section 18.05 |

|

Unenforceable Provisions |

|

77 |

|

Section 18.06 |

|

Governing Law |

|

77 |

|

Section 18.07 |

|

Consent to Jurisdiction |

|

77 |

|

Section 18.08 |

|

WAIVER OF TRIAL BY JURY |

|

78 |

|

|

|

|

|

|

|

Exhibit A |

|

Intentionally Deleted |

|

|

|

Exhibit B |

|

Disbursement Request Form |

|

|

|

Exhibit C |

|

Immediate Repairs |

|

|

|

Exhibit D |

|

Organizational Chart |

|

|

|

Exhibit E |

|

Rent Roll |

|

|

|

Exhibit F |

|

Replacements |

|

|

iv

Fixed Rate

THIS LOAN AGREEMENT is made as of the 17th day of August, 2006 by BEHRINGER HARVARD FERNCROFT, LLC, a Delaware limited liability company (“Borrower”), as borrower, and BARCLAYS CAPITAL REAL ESTATE INC., a Delaware corporation (together with its successors and assigns, “Lender”), as lender.

Background

Borrower desires to obtain a commercial mortgage loan from Lender in the original principal amount of $18,000,000.00 in lawful money of the United States of America. Lender is willing to make such loan to Borrower on the terms and conditions set forth in this Loan Agreement.

Agreement

NOW, THEREFORE, in consideration of such loan and for other good and valuable consideration, the receipt and sufficiency of which are hereby acknowledged, and intending to be legally bound hereby, Borrower and Lender agree as follows:

ARTICLE 1

DEFINED TERMS AND CONSTRUCTION GUIDELINES

Section 1.01 Defined Terms. The following terms have the meanings set forth below:

“Additional Collateral” means a cash deposit from Borrower to Lender that (i) shall be held by Lender in an account that should not be deemed a trust fund, as additional security for the Loan, (ii) is the least amount necessary to cause, when added to the amount that is the denominator of the Loan to Value Ratio calculation, the Loan to Value Ratio to equal no more than 75%, and (iii) shall be deposited with Lender within ten days of Lender’s request following Lender’s determination that Guarantor has failed to satisfy the Net Worth Test or the Liquidity Test.

“Affiliate” of any Person means (a) any other Person which (i) directly or indirectly, owns more than forty percent (40%) of the beneficial or equity interests in such Person or (ii) directly or indirectly, is in Control of, is Controlled by or is under common Control with, such Person; (b) any other Person who is a director or officer of (i) such Person, (ii) any subsidiary of such Person, or (iii) any Person described in clause (a) above; or (c) any corporation, limited liability company or partnership which has as a director any Person described in clause (b) above.

“Anti-Terrorism Laws” shall mean, collectively, (a) the Uniting and Strengthening America by Providing Appropriate Tools Required to Intercept and Obstruct Terrorism Act of 2001 (Public Law 000 00) (Xxx XXX XXXXXXX Xxx), (x) Executive Order No. 13224 on Terrorist Financing, effective September 24, 2001, and relating to Blocking Property and

Prohibiting Transactions With Persons Who Commit, Threaten to Commit, or Support Terrorism, (c) the International Emergency Economic Power Act, 50 U.S.C. §1701 et seq. and (d) all other Legal Requirements relating to money laundering or terrorism.

“Applicable Interest Rate” has the meaning set forth in Section 2.02(b) hereof.

“Approved Budget” has the meaning set forth in Section 9.11(a)(v) hereof.

“Assignment of Leases and Rents” means the Assignment of Leases and Rents dated on or about the date hereof from Borrower, as assignor, to Lender, as assignee, assigning to Lender all of Borrower’s right, title and interest in and to the Leases and the Rents with respect to the Property.

“Assignment of Property Management Contract” means an Assignment of Property Management Contract and Subordination of Management Fees dated on or about the date hereof from Borrower, as assignor, to Lender, as assignee, and acknowledged by Property Manager, or, as applicable, any other Assignment of Property Management Contract executed pursuant to Section 9.14 hereof.

“Bankruptcy Code” means the Bankruptcy Reform Act of 1978 codified as 11 U.S.C. §101 et seq., and the regulations issued thereunder, both as hereafter modified from time to time.

“Borrower” has the meaning in the introductory paragraph of this Loan Agreement.

“Business Day” or “business day” means any day other than a Saturday, a Sunday, or days when Federal Banks located in the State of New York are closed for a legal holiday or by government directive.

“Cash Flow Available for Debt Service” means, for a specified period, (a) Operating Income less (b) Operating Expenses.

“Cash Management Account” shall have the meaning set forth in the Cash Management Agreement.

“Cash Management Agreement” means the Cash Management Agreement dated on or about the date hereof between Borrower, Property Manager and Lender.

“Casualty” means the occurrence of damage or destruction to the Property, or any part thereof, by fire, flood, vandalism, windstorm, hurricane, earthquake, acts of terrorism or any other casualty.

“Closing Date” means August 21, 2006.

“Condemnation” means the taking by any Governmental Authority of the Property or any part thereof through eminent domain or otherwise (including, without limitation, any transfer made in lieu of or in anticipation of the exercise of such taking).

2

“Control” means the possession, directly or indirectly, of the power to direct or cause the direction of the management and policies of a Person whether through ownership of voting securities, beneficial interests, by contract or otherwise. The definition is to be construed to apply equally to variations of the word “Control” including “Controlled,” “Controlling” or “Controlled by.”

“Debt” means the aggregate of all principal and interest payments that accrue or are due and payable in accordance with the Loan Agreement, together with any other amounts due under the Loan Documents. The terms “Debt” and “Loan” have the same meaning whenever used in the Loan Documents.

“Debt Service Coverage Ratio” means, as to a specific period, the ratio of (a) the Cash Flow Available for Debt Service, to (b) the principal and interest that would be due and payable based upon the Applicable Interest Rate (for purposes of the calculation, assuming that the Interest Only Period shall have expired).

“Default Rate” has the meaning set forth in Section 2.04(e) hereof.

“Defeasance” has the meaning set forth in Section 2.05(b)(i) hereof.

“Defeasance Collateral” has the meaning set forth in Section 2.05(b)(iii) hereof.

“Defeasance Pledge Agreement” has the meaning set forth in Section 2.05(b)(ii) hereof.

“Disbursement Request” means a written request from Borrower delivered to Lender, substantially in the form attached hereto as Exhibit B, signed by a Responsible Officer of Borrower and requesting Lender to disburse funds from a Reserve Account. Each Disbursement Request shall describe in reasonable detail the use of the funds requested by the Disbursement Request and shall have attached to it, as applicable: (a) the original invoices, or copies of the original invoices, for all items or materials purchased or services performed which are to be funded by the Disbursement Request, and (b) copies of all permits, licenses and approvals, if any, by any Governmental Authority confirming completion of the Reserve Items. If an original invoice(or copy of an original) is not available, Borrower shall be required to evidence, to Lender’s satisfaction, the amounts expended for which reimbursement is requested.

“Disclosure Documents” has the meaning set forth in Section 15.03 hereof.

“Earnout Criteria” means, collectively, each of the following: (a) the Property has sufficient income to maintain a Debt Service Coverage Ratio (based on the Loan amount that Lender determines, in accordance with Section 4.08, can be supported by the cash flow of the Property) of at least 1.15:1.00; (b) no Event of Default shall have occurred and be continuing and no event shall have occurred and be continuing that with notice or time (or both) would be deemed an Event of Default; (c) the Property maintains a Loan to Value Ratio of no more than 75%; (d) no Cash Flow Sweep (as defined in the Cash Management Agreement) shall have occurred and be continuing; and (e) Borrower has delivered to Lender (unless previously delivered to Lender in connection with a disbursement under Section 4.08 hereof) (i) an executed lease from each tenant demising all or a portion of the Vacant Space, and (ii) an executed estoppel certificate from each such tenant indicating that such tenant (A) has commenced

3

payment of rent, (B) is in possession of the premises demised under its lease, (C) is operating its business in accordance with the terms of its lease, and (D) has no claim or offset against Borrower.

“Earnout Period” means the time period between the Closing Date and September 1, 2009.

“Earnout Reserve Account” means an account held by Lender, or Lender’s designee, in which the Earnout Reserve Deposit will be held, which shall not constitute a trust fund.

“Earnout Reserve Deposit” has the meaning set forth in Section 4.08 hereof.

“Eligible Account” means an identifiable account which is separate from all other funds held by the holding institution that is either (a) an account or accounts maintained with a federal or state chartered depository institution or trust company which complies with the definition of Eligible Institution or (b) a segregated trust account or accounts maintained with the corporate trust department of a federal or state chartered depository institution or trust company acting in its fiduciary capacity which, in the case of a state chartered depository institution or trust company is subject to regulations substantially similar to 12 C.F.R. §9.10(b), having in either case a combined capital and surplus of at least $50,000,000 and subject to supervision or examination by federal and state authority. An Eligible Account will not be evidenced by a certificate of deposit, passbook or other instrument.

“Eligible Institution” means (a) KeyBank, N.A. or (b) a federal or state chartered depository institution or trust company insured by the Federal Deposit Insurance Corporation the short term unsecured debt obligations or commercial paper of which are rated at least A-1 by S&P, P-1 by Xxxxx’x Investors Service, Inc. and F-1+ by Fitch, Inc. in the case of accounts in which funds are held for thirty (30) days or less or, in the case of accounts in which funds are held for more than thirty (30) days, the long term unsecured debt obligations of which are rated at least “AA” by Fitch, Inc. and S&P and “Aa2” by Xxxxx’x Investors Service, Inc.

“Environmental Indemnity” means the Environmental Indemnity Agreement dated on or about the date hereof from Borrower and the other Environmental Indemnitors named therein to Lender.

“Equity Interests” means (a) partnership interests (whether general or limited) in an entity which is a partnership; (b) membership interests in an entity which is a limited liability company; or (c) the shares or stock interests in an entity which is a corporation.

“ERISA” means the Employee Retirement Income Security Act of 1974, and the regulations issued thereunder, all as amended or restated from time to time.

“Event of Default” means any of the events specified in Section 11.01 hereof.

“FRB Release” has the meaning set forth in Section 2.05(c) hereof.

“Full Disbursement Event” has the meaning set forth in the Cash Management Agreement.

4

“GAAP” means generally accepted accounting principles in the United States of America as in effect from time to time.

“Governmental Authority” means any nation or government, any state or other political subdivision thereof, and any Person exercising executive, legislative, judicial, regulatory or administrative functions of or pertaining to such government.

“Guarantor” means Behringer Harvard Opportunity Reit I, Inc., and any other entity or individual liable under the Guaranty and Environmental Indemnity, or any replacement thereof.

“Guaranty” means the Guaranty( Exceptions to Nonrecourse Liability) dated on or about the date hereof from Guarantor to Lender.

“Immediate Repairs” means the repairs or improvements to the Property identified on Exhibit C hereto.

“Immediate Repair Deposit” has the meaning set forth in Section 4.04(b) hereof, subject to adjustment as set forth in Section 4.04(d) hereof.

“Immediate Repair Escrow Account” means an account held by Lender, or Lender’s designee, in which the Immediate Repair Deposit will be held, which shall not constitute a trust fund.

“Improvements” has the meaning set forth in the Security Instrument.

“Indemnified Claim” means the basis for the Indemnified Party’s claim for indemnification under Article 13 hereof.

“Indemnified Parties” means Lender, together with its successors and assigns, which shall include, without limitation, any owner or prior owner or holder of the Note, any servicer of the Loan, any investor, or holder of a full or partial interest in the Loan, any receiver or other fiduciary appointed in a foreclosure or other proceeding under any Requirements of Law regarding creditors’ rights, any officers, directors, shareholders, partners, members, employees, agents, servants, representatives, contractors, subcontractors, Affiliates of any and all of the foregoing, in all cases whether during the term of the Loan or as part of, or following, a foreclosure of the Security Instrument.

“Insurance Premiums” means the premiums for the insurance Borrower is required to provide pursuant to Section 9.03 hereof.

“Insurance Premium Escrow Account” means an account held by Lender, or Lender’s designee, in which Borrower’s initial deposit for Insurance Premiums paid on the Closing Date and the Monthly Insurance Deposits will be held.

“Interest Only Payment” shall mean the monthly payment of interest, at the Applicable Interest Rate, accrued on the outstanding principal balance of the Loan, due and payable on each Payment Due Date during the Interest Only Period hereunder.

5

“Interest Only Period” means that period commencing on the Payment Due Date of October 1, 2006 through and including the Payment Due Date of September 1, 2011.

“Issuer Group” has the meaning set forth in Section 15.04 hereof.

“Issuer Person” has the meaning set forth in Section 15.04 hereof.

“Land” has the meaning set forth in the Security Instrument.

“Lease” has the meaning set forth in the Security Instrument.

“Lease Guaranty” has the meaning set forth in the Security Instrument.

“Leasing Commissions” means leasing commissions incurred by Borrower in connection with the leasing of the Property or any portion thereof (including any so-called “override” leasing commissions which may be due to any leasing or rental agent engaged by Borrower for the Property if an agent other than such agent also is entitled to a leasing commission, and leasing commissions earned under the Property Management Contract, but excluding commissions due any principal, member, general partner or shareholder of Borrower or any Affiliate of Borrower, unless such commissions are provided for in the Property Management Contract or are equal to or less than similar commissions that would be required to be paid to independent third parties for such services).

“Lender” has the meaning in the introductory paragraph of this Loan Agreement.

“Letter of Credit” has the meaning set forth in Section 6.07 hereof.

“Lien” means any mortgage, pledge, hypothecation, assignment, deposit arrangement, encumbrance, lien (statutory or otherwise), or other security agreement of any kind or nature whatsoever (including, without limitation, any conditional sale or other title retention agreement, the filing of any financing statement under the UCC or comparable law of any jurisdiction in respect of any of the foregoing and a mechanics’ or materialman’s lien).

“Liquidity” means cash and unencumbered, marketable securities.

“Liquidity Test” means that Guarantor’s Liquidity, as calculated by Lender in accordance with Lender’s underwriting standards on the basis of information provided by Guarantor shall be at least $2,000,000.00.

“Loan” means the aggregate of all principal and interest payments that accrue or are due and payable in accordance with the Loan Agreement, together with any other amounts due under the Loan Documents. The terms “Loan” and “Debt” have the same meaning whenever used in the Loan Documents.

“Loan Agreement” means this Loan Agreement.

“Loan Documents” means, collectively, this Loan Agreement, the Note, the Security Instrument, the Assignment of Leases and Rents, the Assignment of Property Management

6

Contract, the Environmental Indemnity, the Guaranty, the Lockbox Agreement, the Cash Management Agreement and any and all other documents and agreements executed in connection with the Loan, as each such agreement may be modified, supplemented, consolidated, extended or reinstated from time to time.

“Loan to Value Ratio” means with respect to a specified time, the ratio obtained by dividing (a) the then-outstanding principal balance of the Loan, by (b) either, as selected in Lender’s discretion, the “as-is” or “as-stabilized” value of the Property as set forth in the appraisal obtained by Lender in connection with its underwriting of the Loan or any update thereto requested by Lender at Borrower’s cost, whichever is most recent.

“Lockbox Account” means the Account and Lockbox as such terms are defined in the Lockbox Agreement.

“Lockbox Agreement” means the Blocked and Control Agreement dated on or about the date hereof between Borrower, XX Xxxxxx Chase Bank, N.A. and Lender.

“Lockbox Suspension” has the meaning set forth in the Cash Management Agreement.

“Losses” means any and all claims, suits, liabilities (including, without limitation, strict liabilities and liabilities under federal and state securities laws), actions, proceedings, obligations, debts, damages, losses, costs, expenses, fines, penalties, charges, fees, judgments, awards, and amounts paid in settlement of whatever kind or nature (including without limitation reasonable legal fees and other costs of defense).

“Major Lease” means any Lease (i) that consists of 25,000 rentable square feet or more including any expansion options or (ii) which has a term of more than six (6) years, exclusive of any extension or options to renew. Lender may, in Lender’s sole discretion, aggregate any and all Leases to Affiliates to determine whether such Leases should be treated as a Major Lease.

“Material Adverse Effect” means, with respect to any circumstance, act, condition or event of whatever nature (including any adverse determination in any litigation, arbitration, or governmental investigation or proceeding), whether singly or in conjunction with any other event, act, condition or circumstances, whether or not related, which in Lender’s reasonable judgment, has or results in a material adverse change in, or a materially adverse effect upon (a) the business, operations or financial condition of Borrower or Guarantor; (b) the ability of Borrower or Guarantor to perform its obligations under any Loan Document to which it is a party; (c) the use, value or condition of the Property; (d) compliance of the Property with any Requirements of Law; (e) the validity, priority or enforceability of any Loan Document or the liens, rights (including, without limitation, recourse against the Property) or remedies of Lender hereunder or thereunder; or (f) the occupancy rate of the Property.

“Maturity Date” has the meaning set forth in Section 2.03(c) hereof.

“Maximum Loan Amount” means the maximum principal amount of $18,000,000.00 in lawful money of the United States of America, to be advanced to Borrower pursuant to this Loan Agreement. Reference in the Loan Agreement to “Maximum Loan Amount” mean the

7

maximum principal amount, irrespective of actual principal amount outstanding or actually advanced to Borrower during the term of the Loan.

“Monthly Insurance Deposit” means, with respect to the specified period, an amount equal to one-twelfth (1/12) of the Insurance Premiums that Lender estimates will be payable during the next ensuing twelve (12) months, subject to adjustment as set forth in Section 4.03(d) hereof.

“Monthly Replacement Reserve Deposit” has the meaning set forth in Section 4.05(b) hereof, subject to adjustment as set forth in Section 4.05(d) hereof.

“Monthly Tax Deposit” means, with respect to the specified period, an amount equal to one-twelfth (1/12) of the Taxes that Lender estimates will be payable during the next ensuing twelve (12) months, subject to adjustment as set forth in Section 4.02(d) hereof.

“Monthly TI/LC Deposit” has the meaning set forth in Section 4.06(b) hereof, subject to adjustment as set forth in Section 4.06(d) hereof.

“Net Worth” means, as of a given date, a Person’s equity calculated in conformance with GAAP by subtracting total liabilities from total tangible assets.

“Net Worth Test” means that the Net Worth of Guarantor, as calculated by Lender in accordance with Lender’s underwriting standards on the basis of information provided by Guarantor shall be at least $20,000,000.

“Note” means the Promissory Note dated on or about the date hereof from Borrower to the order of Lender in the original principal amount equal to the Maximum Loan Amount.

“Obligations” means the Loan, and all other obligations and liabilities of the Borrower to Lender, whether direct or indirect, absolute or contingent, due or to become due, or now existing or hereafter incurred, which may arise under, out of, or in connection with the Loan or the Loan Documents, whether on account of principal, interest, fees, indemnities, costs, expenses (including, without limitation, all reasonable fees and disbursements of legal counsel) or otherwise.

“OFAC List” means the list of specially designated nationals and blocked persons subject to financial sanctions that is maintained by the U.S. Treasury Department, Office of Foreign Assets Control and any other similar list maintained by the U.S. Treasury Department, Office of Foreign Assets Control pursuant to any Requirements of Law, including, without limitation, trade embargo, economic sanctions, or other prohibitions imposed by Executive Order of the President of the United States. The OFAC List is accessible through the internet website xxx.xxxxx.xxx/xxxx/x00xxx.xxx.

“Open Date” has the meaning set forth in Section 2.05(a) hereof.

“Operating Account” means that certain account in the name of Borrower at XX Xxxxxx Xxxxx Bank, N.A., account number 707690350, and ABA No. 0000-0000-0.

8

“Operating Agreements” has the meaning set forth in the Security Instrument.

“Operating Expenses” means all cash expenses actually incurred by or charged to Borrower (appropriately pro-rated for any expenses that, although actually incurred in a particular period, also relate to other periods), with respect to the ownership, operation, leasing and management of the Property in the ordinary course of business, determined in accordance with GAAP and adjusted by Lender in accordance with Lender’s customary underwriting procedures and policies then in effect which Operating Expenses are also adjusted by underwritten reserves for Replacements, Tenant Improvements and Leasing Commissions and any other underwritten reserves as determined by Lender whether or not required to be reserved. Operating Expenses shall specifically exclude (1) costs of Tenant Improvements and Leasing Commissions, (2) capital expenditures, (3) depreciation, (4) payments made in connection with the payment of the outstanding principal balance of the Loan, (5) costs of Restoration following a Casualty or Condemnation, (6) funds disbursed from any Reserve Account, and (7) any other non-cash items.

“Operating Income” means all gross cash income, revenues and consideration received or paid to or for the account or benefit of Borrower resulting from or attributable to the operation or leasing of the Property determined in accordance with GAAP adjusted by Lender in accordance with Lender’s customary underwriting procedures and policies then in effect, but excluding any income or revenues from a sale, refinancing, Casualty or Condemnation, payment of rents more than one (1) month in advance, lease termination payments, payments from any other events not related to the ordinary course of operations of the Property, and in connection with a calculation relating to satisfaction of the Earnout Criteria or the requirements for a Full Disbursement Event, rents received from any tenant subject to a lease with a term that is within 12 months of termination or expiration as of the determination.

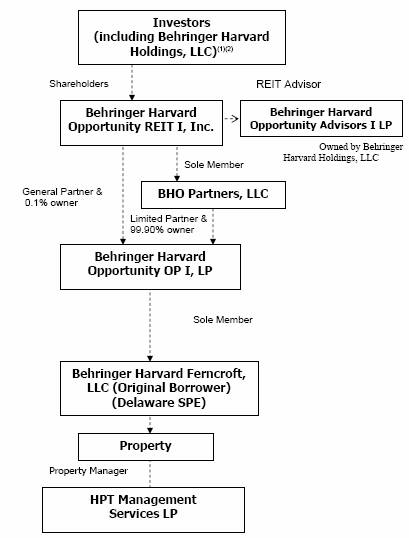

“Organizational Chart” means the chart attached hereto as Exhibit D which shows all persons or entities having an ownership interest in Borrower.

“Other Charges” means all ground rents, maintenance charges, impositions (other than Taxes) and similar charges (including, without limitation, vault charges and license fees for the use of vaults, chutes and similar areas adjoining the Property), now or hereafter assessed or imposed against the Property, or any part thereof, together with any penalties thereon.

“Payment Due Date” has the meaning set forth in Section 2.03(b) hereof. It is the date that a regularly scheduled Interest Only Payment, during the Interest Only Period, and payment of principal and interest, after the expiration of the Interest Only Period, is due.

“Permitted Encumbrances” means only those exceptions shown in the Title Insurance Policy and each other Lien which has been approved in writing by Lender.

“Permitted Transfer” means each of the following:

(a) Transfers of Equity Interests which, in the aggregate over the term of the Loan (i) do not exceed forty-nine percent (49%) of the total interests in Borrower or in Guarantor, as applicable; (ii) do not result in any Person holding an Equity Interest in Borrower, which exceeds forty-nine percent (49%) of the total Equity

9

Interests in Borrower; and (iii) do not result in a change of Control of Borrower or Guarantor.

(b) Transfers with respect to any Person whose stocks or certificates are traded on a nationally recognized stock exchange or that is a reporting company under the Securities Exchange Act of 1934, as amended.

(c) Transfers which have been approved by Lender in accordance with Section 10.02 hereof.

(d) Permitted Encumbrances.

(e) All Transfers of worn out or obsolete furnishings, fixtures or equipment that are promptly replaced with property of equivalent value and functionality if such property is used in, and material to, the operation of the Property.

(f) All Major Leases which have been approved by Lender in accordance with this Loan Agreement.

(g) All Leases which are not Major Leases and which have been approved by the Lender pursuant to Section 9.06 hereof or that do not require Lender’s approval pursuant to Section 9.06 hereof.

(h) Transfers of Equity Interests in a Borrower by or on behalf of the member of such Borrower who is deceased or declared judicially incompetent, to such member’s heirs, legatees, devisees, executors, administrators, estate or personal representatives.

(i) Transfers of Equity Interests in a Borrower by the member of such Borrower for bona fide estate planning purposes to (i) such member’s spouse, children (and spouses of children), siblings, parents, or grandchildren, or (ii) trusts established for the benefit of such member or such member’s spouse, children (and spouses of children), siblings, parents or grandchildren.

“Person” means an individual, partnership, limited partnership, corporation, limited liability company, business trust, joint stock company, trust, unincorporated association, joint venture, governmental authority or other entity of whatever nature.

“Personal Property” has the meaning set forth in the Security Instrument.

“Prohibited Prepayment” has the meaning set forth in Section 2.05(c) hereof.

“Prohibited Prepayment Fee” has the meaning set forth in Section 2.05(c) hereof.

“Property” has the meaning set forth in the Security Instrument.

“Property Manager” means HPT Management Services L.P., a Texas limited partnership.

10

“Property Management Contract” means the Amended and Restated Property Management and Leasing Agreement dated March 9, 2006, between Borrower and Property Manager which provides for the management of the Property for Borrower by Property Manager, as assigned to Borrower pursuant to that certain Partial Assignment and Assumption of Amended and Restated Property Management and Leasing Agreement executed in connection with the closing of the Loan.

“PV” has the meaning set forth in Section 2.05(c)(ii) hereof.

“Qualified Loan Amount” has the meaning set forth in Section 4.08 hereof.

“Rating Agencies” means Fitch, Inc., Xxxxx’x Investors Service, Inc. and S&P, or any successor entity of the foregoing, or any other nationally recognized statistical rating organization to the extent that any of the foregoing have been or will be engaged by Lender or its designees in connection with or in anticipation of Securitization or any other sale or grant of participation interest in the Loan (or any part thereof).

“Rating Confirmation” means a written confirmation from each of the Rating Agencies (unless otherwise agreed by Lender) that an action shall not result in a downgrade, withdrawal or qualification of any securities issued in connection with a Securitization.

“Release” has the meaning set forth in Section 2.05(b)(i) hereof.

“Release Date” has the meaning set forth in Section 2.05(b)(ii) hereof.

“REMIC Trust” means a “real estate mortgage investment conduit” within the meaning of Section 860D of the Code that holds an interest in the Loan.

“Rent Roll” means a statement from Borrower substantially in the form attached hereto as Exhibit E detailing the names of all tenants of the Property, the portion of Property occupied by each tenant, the base rent and any other charges payable under each Lease, the term of each Lease, the beginning date and expiration date of each Lease, whether any tenant is in default under its Lease (and detailing the nature of such default), and any other information as is reasonably required by Lender, all certified by a Responsible Officer to be true, correct and complete.

“Rents” has the meaning set forth in the Security Instrument.

“Replacement Reserve Account” means an account held by Lender, or Lender’s designee, in which the Monthly Replacement Reserve Deposits will be held, which shall not constitute a trust fund.

“Replacements” means the scheduled repairs and replacements to the Property identified on Exhibit F hereto.

“Reporting Default” means, without reference to any cure period under Article 11, each instance that any of the following occur: (a) failure to deliver any of the reports, information, statements or other materials required under Section 9.11 hereof within thirty (30) calendar days

11

after written notice from Lender, or (b) failure to permit Lender or its representatives to inspect or copy books and records relating to the Property within five (5) Business Days of Lender’s written request.

“Requirements of Law” means (a) the organizational documents of an entity, and (b) any law, regulation, ordinance, code, decree, treaty, ruling or determination of an arbitrator, court or other Governmental Authority, or any Executive Order issued by the President of the United States, in each case applicable to or binding upon such Person or to which such Person, any of its property or the conduct of its business is subject including, without limitation, laws, ordinances and regulations pertaining to the zoning, occupancy and subdivision of real property.

“Reserve Accounts” means, individually and collectively, as the context requires, the Tax Escrow Account, the Insurance Premiums Escrow Account, the Immediate Repair Escrow Account, the Replacement Reserve Account, the TI/LC Reserve Account, the TI/LC Designated Reserve Account, the Earnout Reserve Account and the Vacant Space Reserve Account.

“Reserve Item” means, individually and collectively, as the context requires, the Immediate Repairs, the Replacements, the Tenant Improvements and the Leasing Commissions.

“Responsible Officers” means, as to any Person, an individual who is a manager, managing member, a general partner, the chief executive officer, the president or any vice president of such Person or, with respect to financial matters, the chief financial officer or treasurer of such Person or any other officer authorized by such Person to deliver documents with respect to financial matters pursuant to this Loan Agreement.

“Restoration” means the repairs, replacements, improvements, or rebuilding of or to the Property following a Casualty or Condemnation.

“Restoration Deficiency Deposit” has the meaning set forth in Section 9.04(d) hereof. All amounts deposited by Borrower with Lender as the Restoration Deficiency Deposit shall become a part of the Restoration Proceeds and disbursed by Lender for Restoration on the same conditions applicable to disbursement of Restoration Proceeds and, until so disbursed, are pledged to Lender as security for the Loan and Obligations.

“Restoration Holdback” has the meaning set forth in Section 9.04(e) hereof.

“Restoration Proceeds” has the meaning set forth in Section 9.04(b) hereof.

“SAS Premises” has the meaning set forth in the Cash Management Agreement.

“S&P” means Standard & Poor’s Ratings Services, a division of The XxXxxx-Xxxx Companies, Inc., and any successor thereto.

“Scheduled Debt Payments” has the meaning set forth on Section 2.05(b)(iii) hereof.

“Securities Act” means the Securities Act of 1933 and any successor statute thereto and the related regulations issued thereunder, all as amended from time to time.

12

“Securities Liabilities” has the meaning provided in Section 15.04 hereof.

“Securities Exchange Act” means the Securities Exchange Act of 1934, and any successor statute thereto and the related regulations issued thereunder, all as amended from time to time.

“Securitization” or “Securitize” means the sale of the Loan, by itself or as part of a pool with other loans, in a transaction whereby mortgage pass-through certificates or other securities evidencing a beneficial interest, backed by the Loan or such pool of loans, will be sold as a rated or unrated public offering or private placement.

“Security Instrument” means the Mortgage, Assignment of Rents and Leases, Security Agreement and Fixture Filing encumbering the Property and executed by Borrower to Lender or to a trustee for the benefit of Lender, as the case may be, to secure Borrower’s payment of the Loan and performance of the Obligations.

“Single Purpose Entity” has the meaning set forth in Section 7.02 hereof.

“SPE Equity Owner” has the meaning set forth in Section 7.02(b) hereof.

“Standard Lease Form” means, as applicable, the standard form of lease agreement used by Borrower for the rental of commercial units at the Property, in each case in the form certified to Lender as of the Closing Date or subsequently approved by Lender in writing.

“Successor Borrower” has the meaning set forth on Section 2.05(b) hereof.

“Tax Code” means the Internal Revenue Code of 1986 and the related Treasury Department regulations issued thereunder, including temporary regulations, all as amended from time to time.

“Tax Escrow Account” means an account held by Lender, or Lender’s designee, in which Borrower’s initial deposit for Taxes made on the Closing Date and the Monthly Tax Deposits will be held, which shall not constitute a trust fund.

“Taxes” means all real estate taxes, government assessments or impositions, lienable water charges, lienable sewer rents, assessments due under owner association documents, ground rents, vault charges and license fees for the use of vaults chutes and all other charges (other than the Other Charges), now or hereafter levied or assessed against the Land and Improvements.

“Tenant Improvements” means improvements made to the Property to prepare the same for tenant occupancy in connection with each Lease and made by Borrower in conformity with the terms of the related Lease and this Loan Agreement.

“TI/LC Designated Reserve Account” has the meaning set forth in the Cash Management Agreement.

“TI/LC Reserve Account” means an account held by Lender, or Lender’s designee, in which the Monthly TI/LC Deposits will be held, which shall not constitute a trust fund.

13

“TI/LC Threshold” has the meaning set forth in Section 4.06(b) hereof.

“Title Insurance Policy” means the mortgagee title insurance policy obtained by Lender in connection with the Loan, and, until the issuance of such policy, the commitment for title insurance as marked-up as of the Closing Date, in either case in form and substance (with such endorsements and affirmative coverages) as is satisfactory to Lender, insuring that the Security Instrument constitutes a perfected first Lien against the Property in the Maximum Loan Amount, subject only to Permitted Encumbrances.

“Transfer” means any action other than a Permitted Transfer by which either (a) the legal or beneficial ownership of the Equity Interests in Borrower or in the Guarantor or (b) the legal or equitable title to the Property, or any part thereof, or (c) the cash flow from the Property or any portion thereof (excluding transfers of cash flow from), is sold, assigned, transferred, hypothecated, pledged or otherwise encumbered or disposed of, in each case (a), (b), or (c) whether undertaken, directly or indirectly, or occurring by operation of law or otherwise, including, without limitation, each of the following actions:

(i) the sale, conveyance, assignment, grant of an option with respect to, mortgage, deed in trust, pledge, grant of a security interest in, or any other transfer, as security or otherwise, of the Property or with respect to the Leases or Rents (or any thereof);

(ii) the grant of an easement across the Property (other than minor easements not having a Material Adverse Effect) or any other agreement granting rights in or restricting the use or development of the Property (including, without limitation, air rights);

(iii) an installment sale wherein Borrower agrees to sell the Property for a price to be paid in installments; or

(iv) an agreement by Borrower leasing, for other than actual occupancy by a space tenant thereunder, all or a substantial part of the Property.

“Transferee” has the meaning provided in Section 6.07 hereof.

“Trigger Event” has the meaning provided in the Cash Management Agreement.

“UCC” means the Uniform Commercial Code in effect in the State where the Property is located or such other State which governs the perfection of a security interest in the applicable collateral, as from time to time amended or restated. For purposes of the application of the UCC to the Lockbox Account, the Cash Management Account and the Reserve Accounts, the parties agree that such accounts shall be deemed located in the State where the Property is located.

“Underwriter Group” has the meaning provided in Section 15.04 hereof.

“U.S. Obligations” means obligations or securities not subject to prepayment, call or early redemption, each of which qualifies as a “Government security” as defined in

14

Section 2(a)(16) of the Investment Company Act of 1940, as amended (15 U.S.C. §80a-1 et seq.), together with all revenues and proceeds of such obligations or securities.

“Vacant Space” means a portion of the Property that is unoccupied and not subject to a Lease as of the Closing Date.

“Vacant Space Disbursement Conditions” has the meaning provided in Section 4.09 hereof.

“Vacant Space Reserve Account” means an account held by Lender, or Lender’s designee, in which the Vacant Space Reserve Deposit will be held, which shall not constitute a trust fund.

“Vacant Space Reserve Deposit” has the meaning provided in Section 4.09 hereof.

“Verizon Premises” has the meaning set forth in the Cash Management Agreement.

Section 1.02 General Construction. Defined terms used in this Loan Agreement may be used interchangeably in singular or plural form, and pronouns are to be construed to cover all genders. All references to this Loan Agreement or any agreement or instrument referred to in this Loan Agreement shall mean such agreement or instrument as originally executed and as hereafter amended, supplemented, extended, consolidated or restated from time to time. The words “herein,” “hereof” and “hereunder” and other words of similar import refer to this Loan Agreement as a whole and not to any particular subdivision; and the words “Article” and “section” refer to the entire article or section, as applicable and not to any particular subsection or other subdivision. Reference to days for performance means calendar days unless business days are expressly indicated.

ARTICLE 2

MAXIMUM LOAN AMOUNT; PAYMENT TERMS; ADVANCES; DEFEASANCE

Section 2.01 Commitment to Lend.

(a) Maximum Loan Amount Approved. Subject to the terms and conditions set forth herein, and in reliance on Borrower’s representations, warranties and covenants set forth herein, Lender agrees to loan the Maximum Loan Amount to Borrower. The Loan shall be evidenced by this Loan Agreement and by the Note made by Borrower to the order of Lender and shall bear interest and be paid upon the terms and conditions provided herein.

(b) Advance of Maximum Loan Amount. On the Closing Date, Lender shall advance the entire Maximum Loan Amount to Borrower.

Section 2.02 Calculation of Interest.

(a) Calculation Basis. Interest due on the Loan shall be paid in arrears, calculated based on a 360-day year and paid for the actual number of days elapsed for any whole or partial month in which interest is being calculated.

15

(b) Applicable Interest Rate. Interest shall accrue on outstanding principal at the rate 6.33% per annum (“Applicable Interest Rate”).

(c) Adjustment for Impositions on Loan Payment. All payments made by Borrower hereunder shall be made free and clear of, and without reduction for, or on account of, any income, stamp or other taxes, levies, imposts, duties, charges, fees, deductions or withholdings hereafter imposed, levied, collected, withheld or assessed by any government or taxing authority (other than taxes on the overall net income or overall gross receipts of Lender imposed as a result of a present or former connection between Lender and the jurisdiction of the government or taxing authority imposing such that this exclusion shall not apply to a connection arising solely from Lender’s having executed, delivered, performed its obligations under, received a payment under, or enforced this Loan Agreement or any other Loan Document). If any such amounts are required to be withheld from amounts payable to Lender, the amounts payable to Lender under the Loan Documents shall be increased to the extent necessary to yield to Lender, after payment of such amounts, interest or any such other amounts payable at the rates or in the amounts specified herein. If any such amounts are payable by Borrower, Borrower shall pay all such amounts by their due date and promptly send Lender a certified copy of an original official receipt showing payment thereof. If Borrower fails to pay such amounts when due or to deliver the required receipt to Lender, Borrower shall indemnify Lender for any incremental taxes, interest or penalties that may become payable by Lender as a result of any such failure.

(d) Intentionally Deleted.

(e) Acceleration. Notwithstanding anything to the contrary contained herein, if Borrower is prohibited by law from paying any amount due to Lender under Section 2.02(c) or (d), Lender may elect to declare the unpaid principal balance of the Loan, together with all unpaid interest accrued thereon and any other amounts due hereunder, due and payable within one hundred twenty (120) days of Lender’s written notice to Borrower. No Prohibited Prepayment Fee shall be due in such event. Lender’s delay or failure in accelerating the Loan upon the discovery or occurrence of an event under Section 2.02(c) shall not be deemed a waiver or estoppel against the exercise of such right.

Section 2.03 Payment of Principal and Interest.

(a) Payment at Closing. If the Loan is funded on a date other than the first (1st) day of a calendar month, Borrower shall pay to Lender at the time of funding an interest payment calculated by multiplying (i) the number of days from and including the date of funding to (but excluding) the first (1st) day of the next calendar month by (ii) a daily rate based on the interest rate and calculated for a 360-day year.

(b) Payment Dates. Commencing on the first (1st) day of October, 2006 and continuing on the first (1st) day of each and every successive month thereafter (each a “Payment Due Date”) during the Interest Only Period, Borrower shall pay an Interest Only Payment together with any amounts then due pursuant to Section 2.02 of this Loan Agreement, and commencing on October 1, 2011, and continuing on each Payment Due Date thereafter, through and including the Payment Due Date immediately prior to the Maturity Date, Borrower shall pay

16

consecutive monthly payments of principal and interest of $111,767.34 and any amounts due pursuant to Section 2.02 of this Loan Agreement. Lender shall have the right at the time of Securitization, upon not less than ten (10) days prior written notice to Borrower, to change the Payment Due Date to a different calendar day and, if requested by Lender, Borrower shall promptly execute an amendment to this Agreement to evidence such change.

(c) Maturity Date. On the first (1st) day of September, 2013 (“Maturity Date”), Borrower shall pay the entire outstanding principal balance of the Loan, together with all accrued but unpaid interest thereon and all other amounts due under this Loan Agreement, the Note or any other Loan Document.

Section 2.04 Payments Generally.

(a) Delivery of Payments. All payments due to Lender under this Loan Agreement and the other Loan Documents are to be paid to Lender at Lender’s office located at 000 Xxxxx Xxxxxx Xxxx, Xxxxxxxx, Xxx Xxxxxx 00000-0000, Attn: Xxxxxxxx Xxxxx/CMBS Payments, or at such other place as Lender may designate to Borrower in writing from time to time. All amounts due under this Loan Agreement and the other Loan Documents shall be paid in immediately available funds without setoff, counterclaim or any other deduction whatsoever.

(b) Credit for Payment Receipt. No payment due under this Loan Agreement or any of the other Loan Documents shall be deemed paid to Lender until received by Lender at its designated office on a business day prior to 2:00 p.m. Eastern time. Any payment received after the time established by the preceding sentence shall be deemed to have been paid on the immediately following business day. Where a Payment Due Date falls on a date other than a business day, the Payment Due Date shall be deemed the first business day immediately thereafter.

(c) Invalidated Payments. If any payment received by Lender is deemed by a court of competent jurisdiction to be a voidable preference or fraudulent conveyance under any bankruptcy, insolvency or other debtor relief law, and is required to be returned by Lender, then the obligation to make such payment shall be reinstated, notwithstanding that the Note may have been marked satisfied and returned to Borrower or otherwise canceled, and such payment shall be immediately due and payable upon demand.

(d) Late Charges. Borrower shall pay to Lender, immediately and without demand, a late fee equal to five percent (5%) of the delinquent payment if any payment due on a Payment Due Date is not received by Lender in full on or before (i) the sixth (6th) calendar day of the month in which such Payment Due Date occurs (or, if such sixth (6th) calendar day is not a Business Day, the Business Day immediately preceding such sixth (6th) calendar day), or (ii) if the Payment Due Date is changed in accordance with Section 2.02(b) above, the calendar day of the month determined by Lender in its sole discretion. The late fee set forth in the immediately preceding sentence shall not apply to the final payment due on the Maturity Date.

(e) Default Interest Rate. Upon the occurrence of an Event of Default (including the failure of Borrower to pay the Loan in full on or before the Maturity Date), the interest rate payable on the Loan shall immediately increase to the Applicable Interest Rate plus

17

five hundred (500) basis points (“Default Rate”) and continue to accrue at the Default Rate until full payment is received or such Event of Default is cured, as applicable. Interest at the Default Rate also shall accrue on any judgment obtained by Lender in connection with collection of the Loan or enforcement of any obligations due under the other Loan Documents until such judgment amount is paid in full.

(f) Application of Payments. Payments of principal and interest due from Borrower shall be applied first to the payment of late fees, then to Lender advances made to protect the Property or to perform obligations which Borrower failed to perform, then to the payment of accrued but unpaid interest, and then to reduction of the outstanding principal. Following an Event of Default, Lender may apply all payments to amounts then due in any manner and in any order determined by Lender, in its sole discretion. No principal amount repaid may be reborrowed.

Section 2.05 Prepayment Rights.

(a) Prepayment. Borrower acknowledges that Lender is making the Loan to it at the interest rate and upon the other terms herein set forth in reliance upon Borrower’s promise to pay the Loan over the full stated term of this Loan Agreement and that Lender may suffer loss or other detriment if Borrower were to prepay all or any portion of the Note prior to its stated Maturity Date. Except as provided in this Section 2.05, Borrower agrees that Borrower has no right to prepay all or any part of the Loan prior to the Maturity Date. On and after the first day of the twelfth (12th) month preceding the Maturity Date (the “Open Date”), Borrower may prepay the Loan in whole, but not in part, provided Borrower pays with such prepayment (a) all accrued interest and all other outstanding amounts then due and unpaid under this Loan Agreement and under the other Loan Documents, and (b) if the prepayment is not made on a Payment Due Date, Borrower pays with such prepayment the full interest amount that would have accrued for the period from the date of prepayment through the earlier of the next Payment Due Date or the Maturity Date, as applicable. Lender is not obligated to accept any prepayment unless accompanied by amounts required hereunder. Notwithstanding any contrary provision of this Loan Agreement, Lender may at any time apply proceeds from a casualty or condemnation to principal, without penalty or premium, as provided in this Loan Agreement.

(b) Voluntary Defeasance of the Loan.

(i) Defeasance to Release Property from Security Instrument. Subject to Borrower’s compliance with all terms and conditions of this Section 2.05(b), Borrower may defease the Loan in whole, but not in part, in the manner hereinafter set forth (“Defeasance”) on any Business Day after the Lock-out Period Expiration Date (defined below) and obtain a release (“Release”) of the Property from the lien of the Security Instrument. Once a Defeasance has been completed, the Loan will be secured by the Defeasance Collateral (defined below), and thereafter the Loan cannot be the subject of any further Defeasance nor prepaid in whole or in part, notwithstanding any provision of this Section 2.05 to the contrary. “Lock-out Period Expiration Date” means the earlier to occur of (i) the third (3rd) anniversary of the Closing Date, or (ii) the second (2nd) anniversary of the “startup day” (within the meaning of Section 860G(a)(9) of the Tax

18

Code) of the REMIC Trust established in connection with the last Securitization involving any portion of the Loan.

(ii) Conditions to Defeasance. Borrower may cause a Release upon the satisfaction of the following conditions (all as reasonably approved by Lender):

(A) no Event of Default shall exist under any of the Loan Documents;

(B) not less than forty-five (45) (but not more than ninety (90) days prior written notice shall be given to Lender specifying a date (such date being on a Payment Due Date) on which the Defeasance Collateral (as hereinafter defined) is to be delivered (the “Release Date”);

(C) all accrued and unpaid interest and all other sums due under the Note, this Loan Agreement and under the other Loan Documents up to the Release Date including, without limitation, all fees, costs and expenses incurred by Lender and its agents in connection with such release (including, without limitation, reasonable legal fees and expenses for the review and preparation of the Defeasance Pledge Agreement (as defined below) and of the other materials described in Section 2.05(b)(ii)(D) below and any related documentation, and any servicing fees, Rating Agency fees or other costs related to such release), shall be paid in full on or prior to the Release Date;

(D) Borrower shall deliver to Lender on or prior to the Release Date:

1. The Defeasance Collateral which meets all requirements of subsection 2.05(b)(iii) below and is owned by Borrower, free and clear of all liens and claims of third-parties.

2. A written certification of an independent certified public accounting firm (reasonably acceptable to Lender), confirming that the Defeasance Collateral will generate amounts sufficient to make all Scheduled Debt Payments as they fall due under the Note, including full payment due on the Note on the Maturity Date.

3. A pledge and security agreement in form and substance reasonably acceptable to Lender (“Defeasance Pledge Agreement”) and financing statements which pledge and create a first priority security interest in the Defeasance Collateral in favor of Lender.

4. Confirmation in writing from Lender’s custodian that it has received all of the Defeasance Collateral for the account and benefit of Lender.

19

5. A written certification from Borrower which confirms that, following Defeasance, Borrower continues to satisfy the “single purpose entity” requirements of this Loan Agreement.

6. Such legal opinions given by Borrower and/or any Successor Borrower reasonably acceptable to Lender or other counsel reasonably acceptable to Lender as Lender may require to confirm (i) that the Defeasance Collateral and the proceeds thereof have been validly pledged to Lender, that the Defeasance Pledge Agreement and other Loan Documents after the Defeasance are enforceable against Borrower in accordance with the respective terms and Lender has a perfected first priority security interest in the Defeasance Collateral, (ii) in the event of a bankruptcy proceeding or similar occurrence with respect to Borrower, none of the Defeasance Collateral nor any proceeds thereof will be property of Borrower’s estate under Section 541 of the Bankruptcy Code or any similar statute and the grant of security interest therein to Lender shall not constitute an avoidable preference under Section 547 of the Bankruptcy Code or applicable state law, (iii) the release of the lien of the Security Instrument and the pledge of Defeasance Collateral will not directly or indirectly result in or cause any REMIC that then holds the Note to fail to maintain its status as a REMIC and (iv) the defeasance will not cause any REMIC to be an investment company under the Investment Company Act of 1940.

7. Forms of all documents necessary to release the Property from the liens created by the Security Instrument and related UCC financing statements (collectively, “Release Instruments”), each in appropriate form required by the state in which the Property is located.

8. Such other certificates, confirmations, documents or instruments as Lender reasonably deems necessary in connection with the Defeasance, including, without limitation, a Rating Confirmation.

(iii) Purchase and Ownership of the Defeasance Collateral. The “Defeasance Collateral” must consist only of U.S. Obligations that provide for (A) redemption payments to occur prior, but as close as possible, to all successive Payment Due Dates occurring after the Release Date and (B) deliver redemption proceeds at least equal to the amount of principal and interest due on the Note on such Payment Due Date including full payment of all obligations under the Note on the Maturity Date or Open Date (“Scheduled Debt Payments”). The Defeasance Collateral shall be arranged such that redemption payments received from the Defeasance Collateral are paid directly to Lender to be applied on account of the Scheduled Debt Payments. Unless otherwise agreed in writing by Lender, the pledge of the Defeasance Collateral shall be effectuated through the book-entry facilities of a qualified securities intermediary designated by Lender (which may be Lender itself or an Affiliate of Lender if such party qualifies as a securities intermediary) in conformity with all applicable laws.

20

(iv) Successor Borrower Option. Borrower, at Borrower’s expense, has the right to designate an accommodation borrower (“Successor Borrower”) which satisfies Lender’s then current requirements for a “single purpose entity” to assume at the time of Defeasance ownership of the Defeasance Collateral and liability for all of Borrower’s obligations under this Loan Agreement, the Defeasance Pledge Agreement and the other Loan Documents (to the extent that liability thereunder survives repayment of the Loan and release of the Property. Such transfer and assumption shall be evidenced by a duly executed, written agreement reasonably satisfactory to Lender, whereupon Borrower and Guarantor (subject to satisfaction of all requirements of this Section 2.05(b)(ii)) shall be relieved from liability in connection with the Loan (except for those obligations which, by the express terms of the Loan Documents, survive payment of the Loan which shall be assumed by Successor Borrower). Notwithstanding any contrary provision in this Loan Agreement, no assumption fee is required upon a transfer of the Loan in accordance with this Section. If a Successor Borrower assumes Borrower’s obligations, Lender may require as a condition to Defeasance, such additional legal opinions as Lender reasonably deems necessary to confirm the valid creation and authority of the Successor Borrower (including a nonconsolidation opinion), the assignment and assumption of the Loan and Defeasance Collateral between Borrower and Successor Borrower, and the enforceability of the assignment documents and of the Loan Documents as the obligation of Successor Borrower, to be issued by counsel to Borrower and/or any Successor Borrower reasonably acceptable to Lender or other counsel reasonably acceptable to Lender.

(v) Intentionally Deleted.

(vi) Defeasance Costs and Expenses. Borrower shall pay all reasonable costs and expenses incurred by Lender in connection with Defeasance, which payment is required prior to Lender’s issuance of the Release and whether or not Defeasance is completed. Such expenses include, without limitation, the cost incurred by Lender to obtain Rating Confirmation contemplated by Section 2.05(b)(ii)(D)(8), the reasonable fees and disbursements of Lender’s legal counsel and a processing fee to cover Lender’s administrative costs to process Borrower’s Defeasance request. Lender reserves the right to require that Borrower post a deposit to cover costs which Lender reasonably anticipates will be incurred.

(c) Prohibited Prepayment Prior to Open Date. Except as otherwise set forth in Section 2.05(d), if payment of all or any part of the principal balance of the Loan is tendered by Borrower, a purchaser at foreclosure, a Guarantor, or any other Person prior to the Open Date, whether by reason of acceleration of the Loan or otherwise (a “Prohibited Prepayment”), such tender shall be deemed an attempt to circumvent the prohibition against prepayment set forth in Section 2.05(a) and, at Lender’s option, shall be an Event of Default. If a Prohibited Prepayment occurs and is accepted voluntarily or otherwise by Lender, then, in addition to all other rights and remedies available to Lender upon an Event of Default, a Prohibited Prepayment Fee (as defined below) shall be due to compensate Lender for damages suffered as a result of the Prohibited Prepayment, such amount shall be due in addition to the outstanding principal balance, all accrued and unpaid interest and other outstanding amounts due under the Loan Documents. The “Prohibited Prepayment Fee” shall be a prepayment premium equal to the greater of:

21

(i) one percent (1%) of the outstanding principal balance of Note, or

(ii) the excess, if any, of (A) the present value (“PV”) of all scheduled interest and principal payments due on each Payment Due Date in respect of the Loan for the period from the date of such accepted Prohibited Payment to the Maturity Date, including the principal amount of the Loan scheduled to be due on the Maturity Date, discounted at an interest rate per annum equal to the Index (defined below), based on a 360-day year of twelve 30-day months, over (B) the principal amount of the Loan outstanding immediately before such accepted Prohibited Prepayment [i.e., (PV of all future payments) - (principal balance at time of acceleration)]. The foregoing amount shall be calculated by Lender and shall be conclusive and binding on Borrower (absent manifest error).

For purposes hereof, “Index” means the average yield for “treasury constant maturities” published by the Federal Reserve Board in Federal Reserve Statistical Release H.15 (519) (“FRB Release”), for the second full week preceding the date of acceleration of the Maturity Date for instruments having a maturity coterminous with the remaining term of the Loan. If the FRB Release is no longer published, Lender shall select a comparable publication to determine the Index. If there is no Index for instruments having a maturity coterminous with the remaining term of the Loan, then the weighted average yield to maturity of the Indices with maturities next longer and shorter than such remaining average life to maturity shall be used, calculated by averaging (and rounding upward to the nearest whole multiple of 1/100 of 1% per annum, if the average is not such a multiple) the yields of the relevant Indices (rounded, if necessary, to the nearest 1/100 of 1% with any figure of 1/200 of 1% or above rounded upward).

(d) Prepayment as a Result of a Casualty or Condemnation. Prepayments arising from Lender’s application of insurance proceeds upon the occurrence of a Casualty or the application of a condemnation award upon the occurrence of a Condemnation may be made prior to the Open Date without being deemed a Prohibited Prepayment and, whenever made, without payment of the Prohibited Prepayment Fee.

(e) Notice Irrevocable. Notwithstanding any provision of this Loan Agreement to the contrary, Borrower’s notice of Defeasance in accordance with subsection 2.05(b) above shall be irrevocable, and the principal balance to be prepaid shall be absolutely and unconditionally due and payable on the date specified in such notice.

ARTICLE 3