Pricing Agreement

Exhibit 1.2

April 3, 2013

Barclays Capital Inc.

As representative of the several Underwriters

named in Schedule I (the “Representative”)

Ladies and Gentlemen:

Barclays Bank PLC (the “Bank”) proposes to issue $1,000,000,000 aggregate principal amount of 7.75% Fixed to Fixed Rate Contingent Capital Notes due April 2023 Callable April 2018 (the “Notes”). Each of the Underwriters hereby undertakes to purchase at the subscription prices set forth in Schedule II hereto the amount of Notes set forth opposite the name of such Underwriter in Schedule I hereto, such payment to be made at the Time of Delivery set forth in Schedule II hereto. The obligations of the Underwriters hereunder are several but not joint.

Each of the provisions of the Underwriting Agreement—Standard Provisions, dated October 6, 2010 (the “Underwriting Agreement”), is incorporated herein by reference in its entirety, and shall be deemed to be a part of this Agreement to the same extent as if such provisions had been set forth in full herein; and each of the representations and warranties set forth therein shall be deemed to have been made at and as of the date of this Agreement, except that each representation and warranty with respect to the Prospectus in Section 2 of the Underwriting Agreement shall be deemed to be a representation and warranty as of the date of the Prospectus and also a representation and warranty as of the date of this Agreement in relation to the Prospectus as amended or supplemented relating to the Notes. Each reference to the Representatives herein and in the provisions of the Underwriting Agreement so incorporated by reference shall be deemed to refer to you. Unless otherwise defined herein, terms defined in the Underwriting Agreement are used herein as therein defined. The Representative designated to act on behalf of each of the Underwriters of Designated Securities pursuant to Section 14 of the Underwriting Agreement and the address referred to in such Section 14 is set forth in Schedule II hereto.

In addition, the Bank represents and warrants to, and agrees with, each of the Underwriters that the listing prospectus in respect of the Designated Securities, expected to be dated on or about April 8, 2013, as of its date, will contain all material information with regard to the Bank and its subsidiaries, such information will be true and accurate in all material respects and not misleading and will not omit to state any other fact required to be stated therein or the omission of which would make any information contained therein misleading in any material respect and all reasonable enquiries will have been made to ascertain such facts and to verify the accuracy of all such information and otherwise will comply with the relevant rules made under Section 73A of the U.K. Financial Services and Markets Xxx 0000.

An amendment to the Registration Statement, or a supplement to the Prospectus, as the case may be, relating to the Designated Securities, in the form heretofore delivered to you, is now proposed to be filed with the Commission.

The Applicable Time for purposes of this Pricing Agreement is 1:45 p.m. New York time on April 3, 2013. Each “free writing prospectus” as defined in Rule 405 under the Securities Act for which each party hereto has received consent to use in accordance with Section 7 of the Underwriting Agreement is listed in Schedule III hereto and is attached as an Exhibit hereto.

If the foregoing is in accordance with your understanding, please sign and return to us the counterpart hereof, and upon acceptance hereof by you, on behalf of each of the Underwriters, this letter and such acceptance hereof, including the provisions of the Underwriting Agreement incorporated herein by reference, shall constitute a binding agreement between each of the Underwriters on the one hand and the Bank on the other.

| Very truly yours, | ||

| BARCLAYS BANK PLC | ||

| /s/ X. Xxxxxxxx | ||

| Name: | X. Xxxxxxxx | |

| Title: | Managing Director, Barclays Treasury | |

Accepted as of the date hereof

at New York, New York

On behalf of itself and each of the other Underwriters

| BARCLAYS CAPITAL INC. | ||

| /s/ Xxxxx Xxxxx | ||

| Name: | Xxxxx Xxxxx | |

| Title: | Managing Director | |

SCHEDULE I

| Principal Amount of the Notes |

||||

| Underwriter |

||||

| Barclays Capital Inc. |

$ | 580,000,000 | ||

| BNP Paribas Securities Corp. |

$ | 75,000,000 | ||

| Xxxxxxx Lynch, Pierce, Xxxxxx & Xxxxx Incorporated |

$ | 75,000,000 | ||

| Xxxxxx Xxxxxxx & Co. LLC |

$ | 75,000,000 | ||

| Xxxxx Fargo Securities, LLC |

$ | 75,000,000 | ||

| Banco Bilbao Vizcaya Argentaria, S.A. |

$ | 10,000,000 | ||

| Capital One Southcoast, Inc. |

$ | 10,000,000 | ||

| Commerz Markets LLC |

$ | 10,000,000 | ||

| ING Bank N.V. Belgian Branch |

$ | 10,000,000 | ||

| Lloyds Securities Inc. |

$ | 10,000,000 | ||

| Mediobanca – Banca di Credito Finanziario S.p.A. |

$ | 10,000,000 | ||

| Mizuho Securities USA Inc. |

$ | 10,000,000 | ||

| RBC Capital Markets, LLC |

$ | 10,000,000 | ||

| Santander Investment Securities Inc. |

$ | 10,000,000 | ||

| Scotia Capital (USA) Inc. |

$ | 10,000,000 | ||

| SMBC Nikko Capital Markets Limited |

$ | 10,000,000 | ||

| TD Securities (USA) LLC |

$ | 10,000,000 | ||

| Total |

$ | 1,000,000,000 | ||

I-1

SCHEDULE II

Titles of Designated Securities

$1,000,000,000 7.75% Fixed to Fixed Rate Contingent Capital Notes due April 2023 Callable April 2018

Price to Public:

100% of principal amount

Subscription Price by Underwriters:

99.00% of the aggregate principal amount with respect to the Notes; in addition, with respect to $121,850,000 aggregate principal amount of such Notes, Barclays Capital Inc. will receive an additional commission of 0.50% of such aggregate principal amount for the benefit of certain dealers.

In addition, the Bank agrees to pay a structuring fee of 0.50% on the aggregate principal amount of the Notes to Barclays Capital Inc.

Form of Designated Securities:

The Notes will be represented by one or more global notes registered in the name of Cede & Co., as nominee of The Depository Trust Company issued pursuant to the Dated Subordinated Debt Securities Indenture dated October 12, 2010 between Barclays Bank PLC and The Bank of New York Mellon, as supplemented by the Second Supplemental Indenture to be dated April 10, 2013 between Barclays Bank PLC and The Bank of New York Mellon.

Securities Exchange, if any:

London Stock Exchange.

Interest Rate:

Interest will accrue on the Notes from the date of their issuance. From (and including) the date of issuance to (but excluding) the Reset Date, interest will accrue on the notes at an initial rate equal to 7.75% per annum, and thereafter at a rate equal to the sum of (1) the prevailing Mid Market Swap Rate (as defined herein) on the Reset Determination Date and (2) 6.833% per annum, from and including the Reset Date.

Interest Payment Dates:

Interest will be payable on the Notes semi-annually in arrear on April 10 and October 10 in each year, commencing on October 10, 2013.

Reset Date:

April 10, 2018.

Reset Determination Date:

The second Business Day immediately preceding the Reset Date.

II-1

Mid Market Swap Rate:

“Mid Market Swap Rate” means the mid market U.S. dollar swap rate Libor basis having a five-year maturity appearing on Bloomberg page “ISDA 01” (or such other page as may replace such page on Bloomberg, or such other page as may be nominated by the person providing or sponsoring the information appearing on such page for purposes of displaying comparable rates) at 11:00 a.m. (New York time) on the Reset Determination Date, as determined by the Calculation Agent. If such swap rate does not appear on such page (or such other page or service), the Mid Market Swap Rate shall instead be determined by the Calculation Agent on the basis of (i) quotations provided by the principal office of each of four major banks in the U.S. dollar swap rate market (which banks shall be selected by the Calculation Agent in consultation with the Issuer no less than 20 calendar days prior to the Reset Determination Date) (the “Reference Banks”) of the rates at which swaps in U.S. dollars are offered by it at approximately 11.00 a.m. (New York time) (or thereafter on such date, with the Calculation Agent acting on a best efforts basis) on the Reset Determination Date to participants in the U.S. dollar swap rate market for a five-year period and (ii) the arithmetic mean expressed as a percentage and rounded, if necessary, to the nearest 0.001% (0.0005% being rounded upwards) of such quotations. If the Mid Market Swap Rate is still not determined on the Reset Determination Date in accordance with the foregoing procedures, the Mid Market Swap Rate shall be the mid market U.S. dollar swap rate Libor basis having a five-year maturity that appeared on the most recent Bloomberg page “ISDA 01” (or such other page as may replace such page on Bloomberg, or such other page as may be nominated by the person providing or sponsoring the information appearing on such page for purposes of displaying comparable rates) that was last available prior to 11.00 a.m. (New York time) on the Reset Date, as determined by the Calculation Agent.

Calculation Agent:

The Bank of New York Mellon, acting through its London branch, or its successor appointed by the Issuer. All determinations and any calculations made by the Calculation Agent for the purposes of calculating the Mid Market Swap Rate shall be conclusive and binding on the holders of the Notes, the Issuer and the trustee, absent manifest error. The Calculation Agent shall not be responsible to the Issuer, Noteholders or any third party for any failure of the Reference Banks to provide quotations as requested of them or as a result of the Calculation Agent having acted on any quotation or other information given by any Reference Bank which subsequently may be found to be incorrect or inaccurate in any way.

Record Dates:

The 15th calendar day preceding each Interest Payment Date, whether or not such day is a Business Day.

Sinking Fund Provisions:

No sinking fund provisions.

II-2

Redemption Provisions for Notes:

Subject to certain conditions, the Notes are redeemable, at the option of the Bank, (i) on April 10, 2018, (ii) in the event of certain changes in tax law or regulation or the official application or interpretation thereof, and (iii) in the event the Bank determines that the Notes are fully excluded from Tier 2 Capital within the meaning of the capital adequacy requirements of the Prudential Regulation Authority or any other regulation, directive or other binding rules, standards or decisions adopted by the institutions of the European Union, in each case as specified in the preliminary prospectus supplement dated March 26, 2013 (as supplemented by the final term sheet dated April 3, 2013).

Time of Delivery:

April 10, 2013 by 9:30 a.m. New York time.

Specified Funds for Payment of Subscription Price of Designated Securities:

By wire transfer to a bank account specified by the Bank in same day funds.

Value Added Tax:

| (a) | If the Bank is obliged to pay any sum to the Underwriters under this Agreement, which is the consideration for a supply made by the Underwriters to the Bank for value added tax (“VAT”) purposes and any VAT is properly charged on such supply for which the Underwriters are required to account to HM Revenue & Customs, the Bank shall pay to the Underwriters an amount equal to such VAT on receipt of a valid VAT invoice; |

| (b) | If the Bank is obliged to pay a sum to the Underwriters under this Agreement to reimburse any fee, cost, charge or expense properly incurred by the Underwriters under or in connection with this Agreement (the “Relevant Cost”), the Bank shall pay to the Underwriters an amount which: |

| (i) | if for VAT purposes the Relevant Cost is consideration for a supply of goods or services made to the Underwriters, is equal to any input VAT incurred by the Underwriters on that supply of goods and services, but only if and to the extent that the Underwriters are not entitled to recover such input VAT from HM Revenue & Customs (whether by repayment or credit) provided, however, that the Underwriters shall reimburse the Bank for any amount paid by the Bank in respect of irrecoverable input VAT pursuant to this paragraph (i) if and to the extent such input VAT is subsequently recovered from HM Revenue & Customs (whether by repayment or credit); |

| (ii) | if for VAT purposes the Relevant Cost is a disbursement for VAT purposes properly incurred by the Underwriters under, or in connection with, this Agreement as agent on behalf of the Bank, is equal to any part of the Relevant Cost which represents VAT provided, however, that the Underwriters shall use best endeavors to procure that the actual supplier of the goods or services which the Underwriters received as agent issues a valid VAT invoice to the Bank. |

Closing Location: Linklaters LLP, Xxx Xxxx Xxxxxx, Xxxxxx XX0X 0XX, Xxxxxx Xxxxxxx.

II-3

Name and address of Representative:

Designated Representative: Barclays Capital Inc.

Address for Notices:

Barclays Capital Inc.

000 Xxxxxxx Xxxxxx

Xxx Xxxx, XX 00000

Attn: Syndicate Registration

Selling Restrictions:

Each Underwriter of Designated Securities represents, warrants and agrees with the Bank that, in connection with the distribution of the Designated Securities, directly or indirectly, it: (i) has only communicated or caused to be communicated, and will only communicate or cause to be communicated, any invitation or inducement to engage in investment activity (within the meaning of Section 21 of the Financial Services and Markets Xxx 0000 (the “FSMA”)) received by it in connection with the issue or sale of any Designated Securities in circumstances in which Section 21(1) of the FSMA would not, if the Bank were not an “authorized person”, apply to the Bank; and (ii) has complied and will comply with all applicable provisions of the FSMA with respect to anything done by it in relation to the Designated Securities in, from or otherwise involving the United Kingdom.

Other Terms and Conditions:

As set forth in the Prospectus Supplement dated April 3, 2013 relating to the Designated Securities, incorporating the Prospectus dated August 31, 2010 relating to the Designated Securities.

II-4

SCHEDULE III

Issuer Free Writing Prospectuses:

Investor Presentation dated March 26, 2013, attached hereto as Exhibit A.

Final Term Sheet, dated April 3, 2013, attached hereto as Exhibit B.

III-1

EXHIBIT A

Investor Presentation, dated March 26, 2013

Contingent

Capital

Notes

26 March 2013

Marketing

Deck |

Contingent Capital Notes -

Executive Summary

Following our inaugural Contingent Capital Notes (CCNs) transaction in November, we

are pleased to invite indications of interest for a similar transaction

•

The development of a stable and viable contingent capital market represents an

important step in transitioning European bank capital structures to meet

CRD IV requirements with maximum efficiency, from both a cost and

diversification perspective •

Our primary considerations in issuing a second CCN transaction at this time

include: -

Additional build out of the contingent capital market

-

Desire

to

proactively

transition

to

our

CRD

IV

“target”

capital

structure

-

100% “loss absorbing capital”

benefit from UK regulatory authorities

-

Incremental upgrade of Tier 2 (T2) capital to loss absorbing capital.

•

These CCNs will be a T2 security that includes a write-off feature should the

Group’s published Core Tier 1 (CT1) / Common Equity Tier 1

(CET1) ratio, as appropriate, fall below 7% (Trigger Event). We expect

that,

absent

a

Trigger

Event,

and

consistent

with

the

principles

of

the

draft

EU

Recovery

and

Resolution

Directive

(RRD),

the

CCNs

will

rank

and

be

treated

as

pari

passu

with

Barclays’

other

T2

securities

•

Subject to investor feedback, our preference would be for a 10NC5 security (given

the flexibility afforded by the call feature), as we transition to our

end-state capital structure •

Based on our current interpretation of CRD IV, we anticipate that investors will

benefit from the following factors before CT1/CET1 trigger is

breached: -

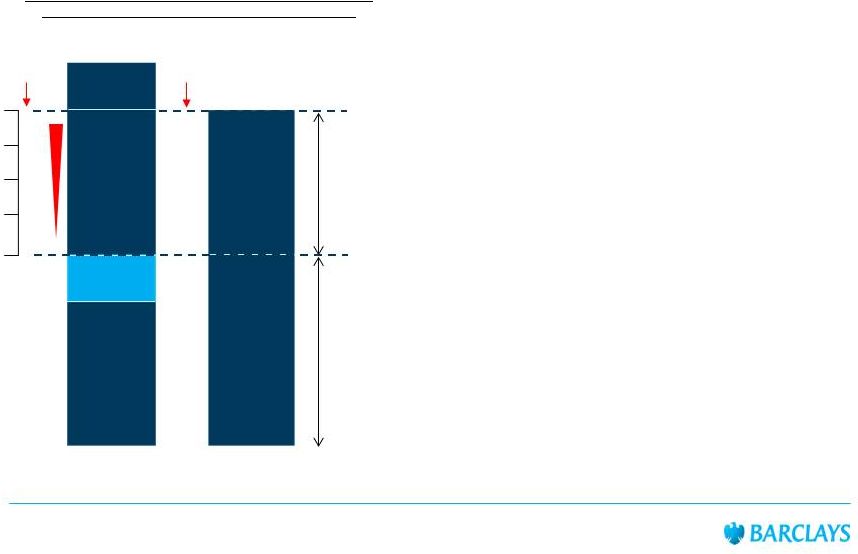

Capital

buffer

of

4.0%

(£15.3bn)

against

our

31

December

2012

CT1

ratio,

post

IFRS

10

1

and

warrant

exercise

2

,

of

11.0%

-

Barclays minimum CRD IV G-SIFI CET1 ratio requirements of 9.0%, below which

distribution prohibitions apply

-

Internal capital management buffer targeting a minimum 10.5% CET1 ratio,

post-CRD IV transition. 2 | Contingent Capital

Notes | 26 March 2013 1

Implementation

of

IFRS

10

on

1

January

2013

resulted

in

a

12bps

decrease

in

31

December

2012

CT1

ratio

of

10.9%

2

Warrants fully exercised in February 2013, resulting in increase in Barclays

PLC’s CT1 equity capital by £750m, equivalent to an additional 19bps on its 31 December 2012

CT1 ratio of 10.9% |

End-State Capital Structure

Our

“target”

capital

structure

was

articulated

during

the

marketing

process

for

the

November

2012

transaction

and

anticipates

expected

CRD

IV

requirements

and

ICB

proposals

•

Common Equity Tier 1 (CET1) target:

3 | Contingent Capital Notes | 26

March 2013 9%

7%

10.5%

10.9%

£42.1bn

XX0

Xxxxxxxx X0 0000

capital structure

(Basel 2.5)

2.4%

£9.5bn

T1 (traditional)

3.8%

£14.4bn

T2

17.1% Total

Capital Ratio

17.0% Total

Capital Ratio

Barclays “Target”

CRD IV / ICB capital

structure

2%

contingent

capital

4.5%

Equity

2.5% Capital

conservation

buffer

2.0% G-SIFI

1.5%

internal buffer

1.5%

AT1

5.0%

T2 / senior

unsecured

-

Reconstitutes the G-SIFI buffer on a Trigger Event, and

-

Reduces

“moral

hazard”

for

fixed

income

investors

that an

excessive CCN layer could introduce.

-

A 2% CCN layer, assuming a 7% Trigger Event:

-

We are targeting a 2% CCN layer, with a 7% trigger event,

comprising the 1.5% AT1 requirement and a further 0.5%

T2

in

the

end-state;

though

we

will

“flex”

these

proportions in

transition

•

Contingent Capital Notes (CCN) Target:

-

While a minimum of 2% T2 capital is required under CRD IV, the

Independent Commission on Banking (ICB) proposals require

17% primary loss absorbing capacity (PLAC)

-

PLAC can be met with senior unsecured debt. Accordingly, we

anticipate that 5% T2/senior unsecured will be required to meet

the ICB 17% PLAC proposal.

•

Tier 2 (T2) target:

-

CRD

IV

incentivises

a

minimum

1.5%

of

AT1

which

has

to

be in

contingent capital form. Without this, excess equity would be

required to avoid distribution restrictions (see next slide).

•

Additional Tier 1 (AT1) target:

-

Minimum regulatory requirements of 4.5% CET1 and 4.5%

“combined

buffer

requirement”

(excluding

counter-cyclical buffer)

-

Minimum

“internal

capital

management

buffer”

of

1.5%

CET1, to

manage business as usual volatility in CET1 ratio. |

Value

of Contingent Capital under CRD IV We

view

the

issuance

of

additional

CCNs

in

T2

form

as

the

most

efficient

way

to

deepen

the

contingent

capital

market

and

prepare

for

AT1

CCNs

that

are

key

to

our

end-state

capital

target

•

In this example, the target minimum CET1 capital ratio of

10.5% comprises:

-

Minimum regulatory requirements of 4.5% CET1 (Art. 87

of CRR)

-

4.5%

“combined

buffer

requirement”

under

Art.

122

of

CRD IV, excluding counter-cyclical buffer,

-

Minimum 1.5% CET1 “internal capital management

buffer”, to manage business as usual volatility in CET1

ratio.

•

Art. 87 of CRD IV incentivises 1.5% of AT1 to be used to make

up

the

total

T1

requirement

of

6%.

If

no

AT1

capital

is

held,

this additional 1.5% T1 minimum regulatory requirement will

have to be met with CET1, which will not then be available to

protect the “combined buffer requirement”

•

Art. 131 of CRD IV imposes restrictions on discretionary

distributions

if

the

“combined

buffer

requirement”

is

breached

•

The benefit of holding 1.5% AT1 to the bank in this example is

clear, without it:

-

1.5% CET1 internal management buffer vanishes

-

Art. 131 distribution restrictions would apply if CET1

reduced by 1bp

-

To re-instate a minimum 1.5% CET1 internal buffer against

distribution restrictions, the bank would need to operate with

12% CET1 on a business as usual basis.

•

Developing the AT1 market necessitates the development of a

deep and scalable contingent capital market. T2 CCNs

represent the most efficient means of doing so at this time.

4 | Contingent Capital Notes | 26

March 2013 4.5%

equity

Capital structure with 4.5%

CET1 and 1.5% AT1 to

meet T1 minimum

4.5% CRD IV

buffers held in

equity

1.5% internal

buffer held

in equity

6.0%

equity

1.5%

AT1 capital

4.5% CRD IV

buffers held

in equity

Capital structure with

6.0% CET1 and no AT1

to meet T1 minimum

Example Minimum Tier 1 Requirements and Regulatory

Buffers, assuming minimum CET1 target of 10.5%

4.5%

3.375%

2.25%

1.125%

0%

60%

40%

20%

0%

Minimum 6%

T1 ratio

under CRR

Art. 87

4.5% Equity

buffer

requirement

under CRD IV

Art. 122

Restrictions on

distributions are linear as

the combined buffer

requirement falls

below 4.5%

CRD IV Art. 131 restrictions

on distributions if

combined buffer

requirement < 4.5% |

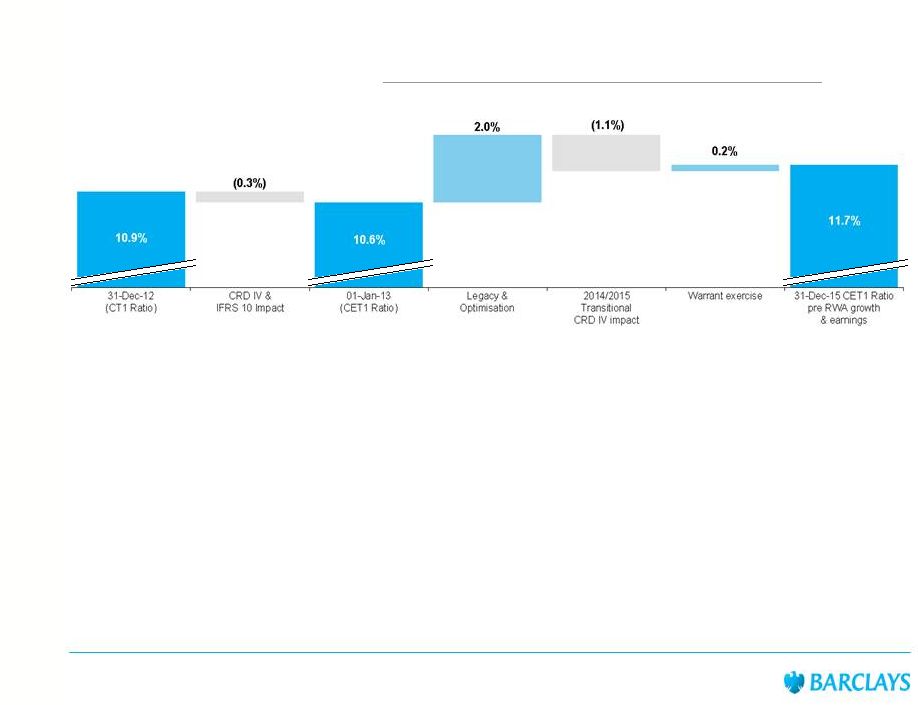

Transitional CET1 ratio projections

Despite

new

regulatory

requirements

and

assuming

no

capital

generation

through

earnings,

we

anticipate

our

transitional

CET1

ratio

to

strengthen

over

time,

as

we

seek

to

implement identified

RWA

mitigating

actions

•

Prior

to

implementation

of

CRD

IV,

the

7%

Trigger

Event

will

be

measured

by

reference

to

Barclays’

current

published

CT1

ratio

(10.9%),

calculated

in

line

with

FSA

guidance

set

out

in

a

letter

to

the

British

Bankers

Association

in

2009

1

•

Upon implementation of CRD IV, the 7% Trigger Event will be measured by reference

to the CRD IV CET1 ratio, on the basis

of

the

transition

rules

set

out

by

FSA

in

its

press

release

of

26

October

2012

2

•

Current

capital

buffer

of

4.0%

(£15.3bn)

against

our

31

December

2012

CT1

ratio,

post

IFRS10

3

and

warrant

exercise

4

,

of

11.0%

•

Key

assumptions

5

:

-

No CET1 capital generated or lost through earnings or losses

-

CET1 capital is impacted by CRD IV transitional adjustments and warrant exercise

-

RWA

projections

include

£75bn

gross

savings

through

identified

efficiencies

(resulting

in

an

estimated

200bps

transitional

CET1

ratio increase) and exclude any business growth

-

Market conditions prevailing at end of December 2012 hold through 2015.

5 | Contingent Capital Notes | 26

March 2013 4

1

FSA letter to BBA on 1 May 2009

(xxxx://xxx.xxx.xxx.xx/xxxx/xxxxx/xxx_xxxxxx.xxx) 2

FSA announcement on 26 October 2012

(xxxx://xxx.xxx.xxx.xx/xxxxx/xxxx/xxxxxxxxxxxxx/xxxxx/xxx/xxx_xxx/xxxxxxxxxxxx-xxxxxxxxxx)

3

Implementation

of

IFRS

10

on

1

January

2013

resulted

in

a

12bps

decrease

in

31

December

2012

CT1

ratio

of

10.9%

4

Warrants fully exercised in February 2013, resulting in increase in Barclays

PLC’s CT1 equity capital by £750m, equivalent to an additional 19bps on 31 December 2012 CT1 ratio of 10.9%

5

These

assumptions

are

subject

to

significant

uncertainties,

as

described

in

the

“Risk

Factors”

section

starting

on

page

72

of

our

Annual

Report

in

20-F

for

the

year

ended

December

31, 2012 and in the

preliminary prospectus supplement that will be filed with the SEC with respect to

the CCNs and a copy of which will be provided to prospective investors |

Contingent Capital Notes: Key Terms & Conditions

6 | Contingent Capital Notes | 26

March 2013 Terms

are

similar

to

the

previous

CCN

issuance

and,

in

addition,

include

acknowledgement

Issuer

Barclays Bank PLC

Expected Issue

Ratings

BBB-/ BBB-

(S&P/Fitch)

Currency / Offering

USD / SEC Registered

Subordination

Subordinated, pari passu

with existing Lower T2, in insolvency, absent a Trigger Event. Barclays expects

that the UK

resolution

authority

would

exercise

its

“bail-in”

power

having

regard

to

the

hierarchy

of

creditor

claims.

Maturity

[10NC5

/

10

year

bullet]

[one-time

call

on

[March]

[

]

2018]

Interest

[[Fixed/Floating] / reset on call date]. No interest deferral

Capital Adequacy

Trigger Event

7%

CET1

ratio

(CT1

capital

before

CRD

IV

implementation

date

and

CET1

capital

after

CRD

IV

implementation

date -

transitioned as per FSA guidance -

divided by risk-weighted assets calculated as per FSA standards

applicable on the calculation date) measured on a quarterly basis or on any other

date on which the CET1 ratio is calculated and subsequently published as

required by the FSA Write-off by means of

Automatic

Write-down

Following a Capital Adequacy Trigger Event, an Automatic Write-down of the

Notes will occur such that Holder’s rights to principal and interest

on the Notes are permanently written off and Holders will have no further rights

against the Issuer

Contractual

Acknowledgement of

UK bail-in power

Acknowledgement

under

New

York

law

that

the

Notes

will

be

subject

to

future

UK

bank

“bail-in”

power,

which,

if

exercised

by

the

relevant

UK

resolution

authority,

may

result

in

the

cancellation

of

all,

or

a

portion

of,

the

principal amount of, or interest on, the Notes and/or the conversion of all or a

portion of the principal amount of, or interest on, the Notes into shares

or other obligations of Barclays Bank PLC or another person Tax Call

At price of 100% if required to pay Additional Amounts or interest payments no

longer deductible for UK corporation tax purposes or Issuer is

de-grouped for United Kingdom tax purposes as a result of a change in law

(including any material amendments to, or failure to enact, UK Finance Act

2013) Regulatory Call

At price of 100% if fully excluded from Tier 2 Capital

Denominations

USD 200,000, integral amounts of USD 1,000 in excess thereof

Listing

London

Governing Law

New York law, save for subordination which will be governed by English law

of

a

prospective

statutory

UK

bank

resolution

bail-in

power |

Recovery and Resolution Directive (RRD)

•

On 6 June 2012, the European Commission

published a proposed RRD

•

The

proposal

includes

a

“bail-in”

power

that

provides resolution authorities with the power to

write-down or convert eligible liabilities into equity

in failing institutions and is applicable to all

liabilities (with certain exceptions)

•

The proposed RRD also provides resolution

authorities with the power to write-down and to

convert AT1 and T2 capital instruments, such as

the CCNs, from 1 January 2015

•

Bail-in tool for other eligible liabilities is expected

to be applicable from 1 January 2018

•

AT1 and T2 liabilities should only be written-down

and/or converted once CET1 instruments have

been exhausted

•

The proposed RRD contains a requirement for the

inclusion in the contractual provisions of

instruments which are governed by the law of

non-Member State jurisdictions a term by which

the creditor recognises that the instrument may

be subject to the statutory write-down and

conversion powers and agrees to be bound by

any write-down and/or conversion effected by the

resolution authority

Recovery and Resolution Plans

Terms of CCN clarify the expectation that investors would be treated as T2

consistently with other creditors of that class in the event a future statutory

bail-in regime is introduced in the UK 7 |

Contingent Capital Notes | 26 March 2013 Excerpt from

the Preliminary Prospectus Supplement

dated

March

26,

2013

(page

S-30)

By its acquisition of the notes, each holder of the notes acknowledges, agrees to

be bound by and consents to the exercise of any U.K. bail-in power (as

defined

below)

by

the

relevant

U.K.

resolution

authority

that

may

result

in

the

cancellation of all, or a portion, of the principal amount of, or interest on, the

notes and/or the conversion of all, or a portion, of the principal amount

of, or interest on, the notes into shares or other securities or other

obligations of the Issuer or another person, and the rights of the holders

under the notes are subject to the provisions of any U.K. bail-in power

which are expressed to implement such a cancellation or conversion.

For

these

purposes,

a

“U.K.

bail-in

power”

is

any

statutory

write-down

and/or

conversion

power

existing

from

time

to

time

under

any

laws,

regulations,

rules or

requirements relating to the resolution of credit institutions and investment firms

incorporated in the United Kingdom in effect and applicable in the United

Kingdom to the Issuer or other members of the Group, including but not

limited to any such laws, regulations, rules or requirements which are

implemented, adopted

or

enacted

within

the

context

of

a

European

Union

directive

or

regulation

of

the

European

Parliament

and

of

the

Council

establishing

a

framework

for

the

recovery

and

resolution

of

credit

institutions

and

investment

firms, pursuant to which obligations of a credit institution or investment firm or

any

of

its

affiliates

can

be

cancelled

and/or

converted

into

shares

or

other

securities or obligations of the obligor or any other person (and a reference to

the “relevant U.K. resolution authority”

is to any authority with the ability to exercise a

U.K. bail-in power).

According to the principles proposed in the draft RRD, Barclays expects that the

relevant U.K. resolution authority would exercise its U.K. bail-in

powers in respect of the notes having regard to the hierarchy of creditor

claims and that the

holders

of

the

notes

would

be

treated

pari

passu

with

all

Other

Pari

Passu

Claims at that time being subjected to the exercise of the U.K. bail-in

powers. |

8 | Contingent Capital Notes | 26

March 2013 Disclaimer

This presentation has been produced by Barclays Bank PLC (“Barclays”) solely for use at this

investor presentation held in connection with the offering of the Barclays Contingent Capital

Notes (“CCNs”) and may not be reproduced or redistributed, in whole or in part, to any other person. Barclays has filed a registration statement (including a prospectus) and

will file a preliminary prospectus supplement with the U.S. Securities and Exchange Commission

(“SEC”) for the offering of the CCNs to which this investor presentation relates. Before

you invest, you should read the prospectus in that registration statement, the preliminary prospectus

supplement relating to the offering of the CCNs and other documents that Barclays will file with

the SEC for more complete information about Barclays and the offering of the CCNs. You may obtain these documents free of charge by visiting the SEC online

database (XXXXX®) on the SEC’s website at (xxxx://xxx.xxx.xxx). The prospectus dated August

31, 2010 is available under the following link: xxxx://xxx.xxx.xxx/Xxxxxxxx/xxxxx/xxxx/000000/000000000000000000/xx0xxx.xxx

. The preliminary prospectus supplement dated on or about March 26, 2013 when filed with the SEC,

will be available under the following link: xxxx://xxx.xxx.xxx/xxxxx.xxxxx. Alternatively, you may

obtain a copy of the prospectus and the preliminary prospectus supplement from Barclays Capital

Inc. by calling 0-000-000-0000. This presentation is only being

distributed to and is only directed at (i) persons who are outside the United Kingdom or (ii) to investment professionals falling within Article 19(5) of the

Financial Services and Markets Xxx 0000 (Financial Promotion) Order 2005 (the “Order”)

or (iii) high net worth entities, and other persons to whom it may lawfully be communicated,

failing within Article 49(2)(a) to (d) of the Order (all such persons together being

referred to as “relevant persons”). Any investment activity to which this communication may relate is

only available to; and any invitation, offer, or agreement to engage in such investment activity will

be engaged in only with, relevant persons. Any person who is not a relevant person should not

act or rely on this document or any of its contents. Forward-looking Statements

This presentation contains certain forward-looking statements within the meaning of Section 21E of

the U.S. Securities Exchange Act of 1934, as amended, and Section 27A of the U.S. Securities

Act of 1933, as amended, with respect to certain of the Barclays Group’s plans and its current goals and expectations relating to its future financial condition and

performance. Barclays cautions readers that no forward-looking statement is a guarantee of future

performance and that actual results could differ materially from those contained in the

forward-looking statements. These forward-looking statements can be identified by the fact that they do not relate only to historical or current facts. Forward-looking statements

sometimes use words such as “may”, “will”, “seek”, “continue”,

“aim”, “anticipate”, “target”, “expect”, “estimate”, “intend”, “plan”, “goal”, “believe”, “projected”, “achieve” or other words of

similar meaning. Examples of forward-looking statements include, among others, statements

regarding Barclays future financial position, income growth, assets, impairment charges,

business strategy, capital ratios (including, in particular, its projected CT1 and CET1 ratios),

leverage, payment of dividends, projected levels of growth in the banking and financial

markets, projected costs, commitments in connection with the Transform Programme, estimates of capital

expenditures and plans and objectives for future operations and other statements that are not

historical fact. By their nature, forward-looking statements involve risk and uncertainty because they relate to future events and circumstances, including, but

not limited to, UK domestic, Eurozone and global macroeconomic and business conditions, the effects of

continued volatility in credit markets, market related risks, such as changes in interest rates

and foreign exchange rates, effects of changes in valuation of credit market exposures, changes in valuation of issued notes, the policies and actions of governmental

and regulatory authorities (including requirements regarding capital and group structures and the

potential for one or more countries exiting the Eurozone), changes in legislation, the further

development of standards and interpretations under International Financial Reporting Standards (“IFRS”) and prudential capital rules applicable to past, current and future

periods, evolving practices with regard to the interpretation and application of standards, the

outcome of current and future legal proceedings, the success of future acquisitions and other

strategic transactions, and the impact of competition – a number of such factors being beyond the Barclays Group’s control. In particular, the CRD IV rules, including with respect

to the calculation of common equity tier 1 capital and risk weighted assets, have not been finalized

and remain subject to change by European legislators, and the Financial Services Authority of

the United Kingdom (the “FSA”), may also alter its stated approach to the adoption of CRD IV in the United Kingdom, and, accordingly, the basis on which certain

calculations in this investor presentation are made may be different than the requirements under the

final CRD IV rules as they apply in the United Kingdom. As a result of these uncertain

events and circumstances, the Barclays Group’s actual future results and capital ratios may differ materially from the plans, goals, and expectations set forth in the Barclays

Group’s forward-looking statements. Any forward-looking statements made herein or in the

documents incorporated by reference herein speak only as of the date they are made. Except as

required by the FSA, the London Stock Exchange plc (“LSE”) or applicable law, Barclays expressly disclaims any obligation or undertaking to release publicly any updates

or revisions to any forward-looking statement contained in this investor presentation or the

documents incorporated by reference herein to reflect any changes in expectations with regard

thereto or any changes in events, conditions or circumstances on which any such statement is based. The reader should, however, consult any additional disclosures that

Barclays has made or may make in documents that the Barclays Group has filed or may file with the

SEC. |

9 | Contingent Capital Notes | 26

March 2013 Disclaimer (continued)

Certain non-IFRS measures

This investor presentation includes a calculation of transitional Common Equity Tier 1

(“CET1”) ratio as at 1 January 2013. Transitional CET1 ratio is a regulatory measurement that is

not yet required to be disclosed and, as such, represents a non-IFRS measure. Management views its

transitional CET1 ratio as a key measure in monitoring the Group’s capital position.

Transitional CET1 ratio has been calculated on the basis of our current interpretation of the new capital requirements regulation and capital requirements directive that

implement Basel 3 proposals within the EU (known as CRD IV), including transitional provisions in line

with the FSA’s statement on CRD IV transitional provisions in October 2012, assuming they

were applied as at 1 January 2013. The methodologies for calculating this measurement is not yet finalised: they are subject to further revisions ahead of their

implementation date and our interpretation of this calculations may not be consistent with other

financial institutions. For more information on the calculation of this measurement and the

impacts of Basel 3, see pages 130-134 of our Annual Report on Form 20-F for the year ended December 31, 2012 (“2012 Form 20-F”). See also pages 131-132 of our 2012 Form

20-F for information on our Core Tier 1 ratio calculated on the basis that currently applies to

the Barclays Group under applicable regulatory requirements. INVESTING forth under “Risk

Factors” of the preliminary prospectus supplement which will be filed with the SEC and “Risk Review -Risk factors” beginning on page 72 of our 2012 Form 20-F. In

particular, you should be aware that, upon the occurrence of a Capital Adequacy Trigger Event, which

will result in an Automatic Write-Down (each as defined in the preliminary prospectus

supplement to be filed with the SEC), holders of CCNs will lose their entire investment in the CCNs. Barclays urges you to consult your investment, legal, tax, accounting

and other advisors before you invest in the CCNs.

References to internet websites in this presentation are made for informational purposes only, and

information found at such websites is not incorporated by reference into this

presentation.

IN

THE

CCNs

IS

SPECULATIVE

AND

INVOLVES

RISK

OF

LOSING

YOUR

ENTIRE

INVESTMENT.

You

should

carefully

review,

among

other

things,

the

matters

set |

Treasury

Xxxxxx Xxxxxxx

x00 (0)00 0000 0000

xxxxxx.xxxxxxx@xxxxxxxx.xxx

Investor Relations

Xxxxxxx Xxxxx

x00 (0)00 0000 0000

xxxxxxx.xxxxx@xxxxxxxx.xxx

Capital Products

Xxxxx Xxxxxxxxx

x00 (0)00 0000 0000

xxxxx.xxxxxxxxx@xxxxxxxx.xxx

Website

xxxx://xxxxx.xxxxxxxx.xxx/xxxxx-xxxxxxxx/xxxxxxxx-xxxxxxxxx#xxxx-xxxxxxxxx

Xxxxxxxx Xxxxxxxx

x00 (0)00 0000 0000

xxxxxxxx.xxxxxxxx@xxxxxxxx.xxx

Xxxxxxx Xxxxx

x00 (0)00 0000 0000

xxxxxxx.xxxxx@xxxxxxxx.xxx

Debt Capital Markets

Xxx Xxxxxxxxxx

x00 (0)00 0000 0000

xxxxxx.xxxxxxxxxx@xxxxxxxx.xxx

Contact Information

10 | Contingent Capital Notes | 26

March 2013 |

EXHIBIT B

Final Term Sheet for the Notes, dated April 3, 2013

Pricing Term Sheet

| Issuer: | Barclays Bank PLC | |

| Expected Issue Ratings: | BBB- (S&P), BBB- (Fitch)1 | |

| Status: | Dated Subordinated Debt | |

| Legal Format: | SEC Registered | |

| Principal Amount: | USD 1,000,000,000 | |

| Trade Date: | 3 April, 2013 | |

| Settlement Date: | 10 April, 2013 | |

| Maturity Date: | 10 April, 2023 | |

| Optional Call Date: | 10 April, 2018 (one time call only) | |

| Initial Interest Period: | ||

| Initial Fixed Rate: | 7.75%, from and including 10 April, 2013 to, but excluding, the Reset Date | |

| Reset Date: | 10 April, 2018 | |

| Initial Interest Payment Dates: | Semi-annually in arrear on each of 10 April and 10 October in each year up to and including the Reset Date, commencing on 10 October, 2013. | |

| Day Count: | 30/360, following, unadjusted | |

| Benchmark Treasury: | UST 0.75 3/31/18 | |

| Spread to Benchmark: | +701.9 bps | |

| Spread to Mid Market Swap Rate: | +683.3 bps | |

| Interest Period Following the Reset Date: | ||

| Fixed Rate Following the Reset Date: | The prevailing Mid Market Swap Rate on the Reset Determination Date plus 6.833%, from and including the Reset Date (see below for definition of Mid Market Swap Rate). | |

| Interest Payment Dates Following the Reset Date: | Semi-annually in arrear on each of 10 April and 10 October in each year, commencing on 10 October, 2018 and ending on the Maturity Date. | |

| Day Count: | 30/360, following, unadjusted | |

| Spread to Mid Market Swap Rate: | +683.3 bps | |

| Reset Determination Date: | “Reset Determination Date” means the second Business Day immediately preceding the Reset Date. | |

1 Note: A securities rating is not a recommendation to buy, sell or hold securities and may be subject to revision or withdrawal at any time.

| Mid Market Swap Rate: | “Mid Market Swap Rate” means the mid market U.S. dollar swap rate Libor basis having a five-year maturity appearing on Bloomberg page “ISDA 01” (or such other page as may replace such page on Bloomberg, or such other page as may be nominated by the person providing or sponsoring the information appearing on such page for purposes of displaying comparable rates) at 11:00 a.m. (New York time) on the Reset Determination Date, as determined by the Calculation Agent. If such swap rate does not appear on such page (or such other page or service), the Mid Market Swap Rate shall instead be determined by the Calculation Agent on the basis of (i) quotations provided by the principal office of each of four major banks in the U.S. dollar swap rate market (which banks shall be selected by the Calculation Agent in consultation with the Issuer no less than 20 calendar days prior to the Reset Determination Date) (the “Reference Banks”) of the rates at which swaps in U.S. dollars are offered by it at approximately 11.00 a.m. (New York time) (or thereafter on such date, with the Calculation Agent acting on a best efforts basis) on the Reset Determination Date to participants in the U.S. dollar swap rate market for a five-year period and (ii) the arithmetic mean expressed as a percentage and rounded, if necessary, to the nearest 0.001% (0.0005% being rounded upwards) of such quotations. If the Mid Market Swap Rate is still not determined on the Reset Determination Date in accordance with the foregoing procedures, the Mid Market Swap Rate shall be the mid market U.S. dollar swap rate Libor basis having a five-year maturity that appeared on the most recent Bloomberg page “ISDA 01” (or such other page as may replace such page on Bloomberg, or such other page as may be nominated by the person providing or sponsoring the information appearing on such page for purposes of displaying comparable rates) that was last available prior to 11.00 a.m. (New York time) on the Reset Date, as determined by the Calculation Agent.

The Fixed Rate following the Reset Date may be less than the Initial Fixed Rate. | |

| Business Days: | New York, London | |

| Reoffer Yield: | 7.75% | |

| Price to Public: | 100.000% | |

| Estimated Underwriter Compensation: | Estimated to be a maximum of approximately 2.0% of principal amount of the Notes, including a structuring fee of 0.50% payable to Barclays Capital Inc. | |

| Estimated Net Proceeds: | USD 980,000,000 | |

| Principal Redemption: | 100.000% | |

| Interest Deferral: | None. | |

| Joint Bookrunners: | Barclays Capital Inc., BNP Paribas Securities Corp., Xxxxxxx Lynch, Pierce, Xxxxxx & Xxxxx Incorporated, Xxxxxx Xxxxxxx & Co. LLC and Xxxxx Fargo Securities, LLC. | |

| Co-lead managers: | Banco Bilbao Vizcaya Argentaria, S.A., Capital One Southcoast, Inc., COMMERZBANK AKTIENGESELLSCHAFT, ING Bank N.V. Belgian Branch, Lloyds TSB Bank plc, Mediobanca – Banca di Credito Finanziario S.p.A., Mizuho Securities USA Inc., Royal Bank of Canada Europe Limited, Santander Investment Securities Inc., Scotia Capital (USA) Inc., SMBC Nikko Capital Markets Limited, TD Securities (USA) LLC | |

| Ranking: | Subordinated obligations. In winding up or administration of the Issuer, the Notes shall rank at least pari passu with other dated subordinated obligations and other securities of the Issuer which in each case by law rank, or by their terms are expressed to rank, pari passu with the Notes (including the Issuer’s $1.25 billion 5.14% Lower Tier 2 Notes due October 2020 and the Issuer’s $3 billion 7.625% Contingent Capital Notes due November 2022) | |

| Capital Adequacy Trigger Event: | A “Capital Adequacy Trigger Event” shall occur if the CET1 Ratio as of the last day of each fiscal quarter or as of any other business day on which the CET1 Ratio is calculated upon the instruction of the Prudential Regulation Authority (as defined in the prospectus supplement) (the “PRA”), as the case may be, is less than 7.00% on such date.

“CET1 Ratio” means, on the relevant date, the ratio of CET1 Capital to the Risk Weighted Assets (each as defined in the prospectus supplement) of Barclays PLC and its consolidated subsidiaries (the “Group”), calculated by Barclays PLC on a consolidated basis in accordance with PRA guidelines applicable to the Group, expressed as a percentage.

“CET1 Capital” means, on the relevant date, (i) before the CRD IV implementation date, “core tier 1 capital” of the Group, less applicable deductions, and (ii) after the CRD IV implementation date, the “common equity tier 1 capital” of the Group, less applicable deductions, in either case as calculated by Barclays PLC on a consolidated basis in accordance with PRA guidelines applicable to the Group (as more fully described in the prospectus supplement).

The term “core tier 1 capital” shall have the meaning assigned to such term in the capital adequacy standards and guidelines of the PRA and “common equity tier 1 capital” shall have the meaning assigned to such term in CRD IV, subject to the transitional arrangements as implemented by the PRA. | |

| Automatic Write-Down: | If a Capital Adequacy Trigger Event occurs, then an Automatic Write-Down will occur.

“Automatic Write-Down” means the automatic write-down of the full principal amount of the Notes that has not become due to zero and the cancellation of the notes upon the expiration of the Suspension Period (as defined in the prospectus supplement).

Any Automatic Write-Down will result in holders not having any rights with respect to repayment of the principal amount of the Notes that has not become due or the payment of interest on such Notes for any period from (and including) the interest payment date falling immediately prior to the occurrence of such Automatic Write-Down, except for any rights of the holders with respect to any payments under the Notes that were due and payable prior to the date of such Automatic Write-Down. As a result, the holders will lose their entire investment in the Notes. Prior to the date on which an Automatic Write-Down occurs, the Issuer will give an Automatic Write-Down Notice to the trustee and the holders via The Depository Trust Company (“DTC”). Following the receipt of the Automatic Write-Down Notice by DTC and the commencement of the Suspension Period, DTC shall suspend all clearance and settlement of the Notes. As a result, holders will not be able to settle the transfer of any Notes from the commencement of the Suspension Period, and any sale or other transfer of the Notes that a holder may have initiated prior to the commencement of the Suspension Period that is scheduled to settle during the Suspension Period will be rejected by DTC and will not be settled within DTC.

Each purchaser of the Notes by its acquisition of the Notes and as a holder of Notes:

(1) consents to the Automatic Write-Down and acknowledges that such Automatic Write-Down of its Notes following a Capital Adequacy Trigger Event may occur without any further action on such holder’s part and authorizes, directs and requests DTC and any direct participant in DTC or other intermediary through which it holds such notes to take any and all necessary action, if required, to implement the Automatic Write-Down; and

(2) (i) agrees to all the terms and conditions of the Notes, including, without limitation, those related to the occurrence of a Capital Adequacy Trigger Event and any related Automatic Write-Down, (ii) agrees that effective upon, and following, the occurrence of the Automatic Write-Down, other than with respect to payments that have become due and payable prior to such Automatic Write-Down, no amount shall be due and payable to the holders under the Notes, and the holders shall not have the right to give a direction to the trustee with respect to the Capital Adequacy Trigger Event and any related Automatic Write-Down and (iii) waives, to the extent permitted by the Trust Indenture Act, any claim against the trustee arising out of its acceptance of its trusteeship for the Notes, including, without limitation, claims related to or arising out of or in connection with a Capital Adequacy Trigger Event and/or the Automatic Write-Down. | |

| Agreement with Respect to Exercise of UK Bail-in Power: | By its acquisition of the Notes, each holder of the Notes acknowledges, agrees to be bound by and consents to the exercise of any U.K. bail-in power (as defined below) by the relevant U.K. resolution authority that may result in the cancellation of all, or a portion, of the principal amount of, or interest on, the Notes and/or the conversion of all, or a portion, of the principal amount of, or interest on, the Notes into shares or other securities or other obligations of the Issuer or another person (other than in respect of each of the foregoing, payments of principal and interest that have become due and payable prior to the exercise of the U.K. bail-in power), and the rights of the holders under the Notes are subject to the provisions of any U.K. bail-in power which are expressed to implement such a cancellation or conversion.

For these purposes, a “U.K. bail-in power” is any statutory write-down and/or conversion power existing from time to time under any laws, regulations, rules or requirements relating to the resolution of credit institutions and investment firms incorporated in the United Kingdom in effect and applicable in the United Kingdom to the Issuer or other members of the Group, including but not limited to any such laws, regulations, rules or requirements which are implemented, adopted or enacted within the context of a European Union directive or regulation of the European Parliament and of the Council establishing a framework for the recovery and resolution of credit institutions and investment firms, pursuant to which obligations of a credit institution or investment firm or any of its affiliates can be cancelled and/or converted into shares or other securities or obligations of the obligor or any other person (and a reference to the “relevant U.K. resolution authority” is to any authority with the ability to exercise a U.K. bail-in power).

According to the principles proposed in the draft RRD, Barclays expects that the relevant U.K. resolution authority would exercise its U.K. bail-in powers in respect of the notes having regard to the hierarchy of creditor claims and that the holders of the notes would be treated pari passu with all Other Pari Passu Claims (as defined in the prospectus supplement) at that time being subjected to the exercise of the U.K. bail-in powers.

By its acquisition of the Notes, each holder of the Notes, to the extent permitted by the Trust Indenture Act, waives any and all claims against the trustee for, agrees not to initiate a suit against the trustee in respect of, and agrees that the trustee shall not be liable for, any action that the trustee takes, or abstains from taking, in either case in accordance with the exercise of the U.K. bail-in power by the relevant U.K. resolution authority with respect to the Notes.

| |

| By its acquisition of the Notes, each holder shall be deemed to have (i) consented to the exercise of any U.K. bail-in power as it may be imposed without any prior notice by the relevant U.K. resolution authority of its decision to exercise such power with respect to the notes and (ii) authorized, directed and requested DTC and any direct participant in DTC or other intermediary through which it holds such notes to take any and all necessary action, if required, to implement the exercise of any U.K. bail-in power with respect to the Notes as it may be imposed, without any further action or direction on the part of such holder. | ||

| Tax Call: | The Issuer may, at its option, redeem the Notes upon giving notice, in whole but not in part, at a redemption price equal to 100% of their principal amount, together with any accrued but unpaid interest to the date fixed for redemption, upon the occurrence of a Tax Event (subject to (i) the provisions described under “Conditions on Redemption” below, (ii) the circumstance that entitles the Issuer to exercise such right of redemption of the notes not being (in the opinion of the Issuer) reasonably foreseeable at the Settlement Date and (iii) in the case of each Tax Event, such obligation not being able to be avoided by the Issuer taking reasonable measures available to it).

A “Tax Event” shall be deemed to have occurred in the event of any change in tax law or regulation or the official application or interpretation thereof including, without limitation, (a) any failure to enact the U.K. Finance Xxx 0000 or (b) any material amendment (whether at the time of enactment or thereafter) to the draft U.K. Finance Xxx 0000 published on December 11, 2012 relating to the taxation of Tier 2 Capital) that would (1) require the Issuer (or any successor entity) to pay additional amounts to holders, (2) result in the Issuer (or any successor entity) not being entitled to claim a deduction in respect of any payments in computing its (or any successor entity’s) taxation liabilities or materially reducing the amount of such deduction or (3) result in the Issuer (or any successor entity) not, as a result of the Notes being in issue, being able to have losses or deductions set against the profits or gains, or profits or gains offset by the losses or deductions, of companies it (or any successor entity) is or would otherwise be so grouped for applicable United Kingdom tax purposes (whether under the group relief system current as at the date of issue of the notes or any similar system or systems having like effect as may from time to time exist). | |

| Regulatory Call: | The Issuer may, at its option, redeem the Notes upon giving notice, in whole but not in part, at a redemption price equal to 100% of their principal amount, together with any accrued but unpaid interest to the date fixed for redemption, upon the occurrence of a Regulatory Event (subject to (i) the provisions described under “Conditions on Redemption” below and (ii) the circumstance that entitles the Issuer to exercise such right of redemption of the notes not being (in the Issuer’s opinion) reasonably foreseeable at the Settlement Date).

A “Regulatory Event” means that the Issuer determines that for any reason the Notes are fully excluded from the Group’s Tier 2 Capital within the meaning and for the purposes of (1) the capital adequacy requirements of the PRA or (2) any other regulation, directive or other binding rules, standards or decisions adopted by the institutions of the European Union. | |

| Optional Call: | The Issuer may, at its option, redeem the Notes, in whole but not in part, on 10 April, 2018 at 100% of their principal amount, together with any accrued but unpaid interest to (but excluding) the date fixed for redemption (subject to the provisions described under “Conditions on Redemption” below). | |

| Conditions on Redemption: | Notwithstanding any other provision:

(1) the Issuer may redeem the Notes prior to their Maturity Date only if the Issuer has obtained the PRA’s prior consent (as (and to the extent) required by applicable law and regulation) for the redemption of the relevant Notes in question; and

(2) in the event of a redemption prior to the fifth anniversary of the Settlement Date, only if (i) the circumstance that entitles the Issuer to exercise that right of redemption is the result of a change in the applicable tax treatment or regulatory classification of the Notes; and (ii) if at the time of the exercise of the right of redemption (and if and to the extent required at such time), the Issuer complies with the PRA’s main Pillar 1 rules applicable to the Issuer and other BIPRU firms (within the meaning of the PRA’s General Prudential Sourcebook) and will continue to do so after the redemption of the Notes. | |

| Denominations: | USD 200,000 and integral multiples of USD 1,000 in excess thereof | |

| ISIN/CUSIP: | US06739FHK03 / 00000XXX0 | |

| Documentation: | To be documented under the Issuer’s SEC registered shelf | |

| Clearing | DTC | |

| Listing: | London | |

| Calculation Agent: | The Bank of New York Mellon, acting through its London branch, or its successor appointed by the Issuer. All determinations and any calculations made by the Calculation Agent for the purposes of calculating the Mid Market Swap Rate shall be conclusive and binding on the holders of the Notes, the Issuer and the trustee, absent manifest error. The Calculation Agent shall not be responsible to the Issuer, Noteholders or any third party for any failure of the Reference Banks to provide quotations as requested of them or as a result of the Calculation Agent having acted on any quotation or other information given by any Reference Bank which subsequently may be found to be incorrect or inaccurate in any way. | |

| Governing Law: | New York law, except for subordination provisions which will be governed by the laws of England and Wales. | |

The Issuer has filed a registration statement, including a prospectus and preliminary prospectus supplement, with the U.S. Securities and Exchange Commission (the “SEC”) for this offering. Before you invest, you should read each of these documents and the other documents the Issuer has filed with the SEC for more complete information about the Issuer and this offering. You may get these documents for free by searching the SEC online database (XXXXX®) at xxx.xxx.xxx. Alternatively, you may obtain a copy of the prospectus from Barclays Capital Inc. by calling 0-000-000-0000, BNP Paribas Securities Corp. at 0-000-000-0000, Xxxxxxx Lynch, Pierce, Xxxxxx & Xxxxx Incorporated at 1-800-294-1322, Xxxxxx Xxxxxxx & Co. LLC at 0-000-000-0000 or Xxxxx Fargo Securities, LLC at 0-000-000-0000.