Contract

Exhibit 10.3

Business loan agreement

Lloyds TSB

Fixed rate only or Fixed rate followed by Variable rate using funds from European Investment Bank

For lending unregulated under the Consumer Credit Xxx 0000 to Companies, Sole Traders and Partnerships (including Limited Liability Partnerships) carrying on business in England

and Wales and/or Scotland.

Guidance notes

Please write clearly in the white

spaces with capital letters or cross the boxes.

Calls may be monitored or recorded in case we need to check we have carried out your instructions correctly and to

help improve our quality of service.

We aim to provide the highest level of customer service possible. However if you experience a problem we will always seek to

resolve this as quickly and efficiently as possible.

You can request a copy of our “How to voice your concerns” leaflet from your relationship team,

business team or any branch. Our complaint procedures are also on our website xxx.xxxxxxxxx.xxx

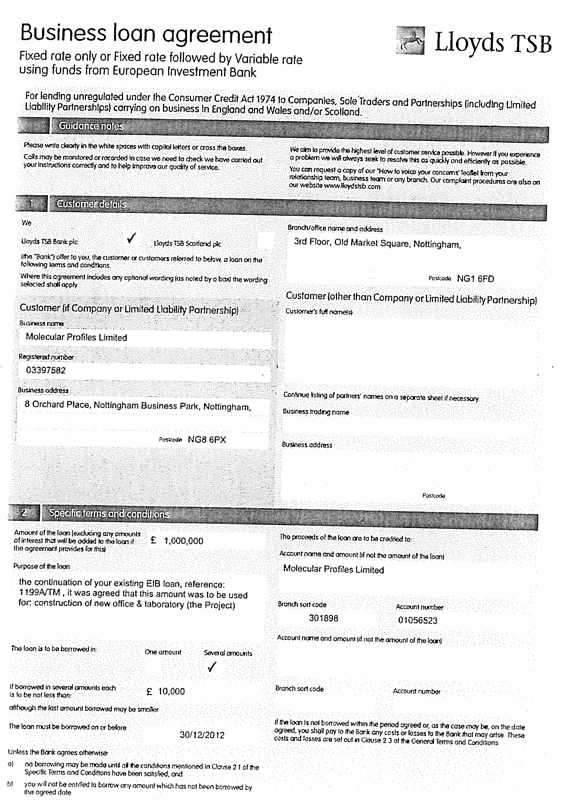

1 Customer details

We

Branch/office name and address

Lloyds TSB Bank plc x

Lloyds TSB Scotland plc ¨

0xx Xxxxx, Xxx Xxxxxx Xxxxxx, Xxxxxxxxxx,

Xxxxxxxx XX0 0XX

[the “Bank”] offer to you, the customer or customers referred to

below, a loan on the following terms and conditions.

Where this agreement includes any optional wording (as noted by a box) the wording selected shall apply

Customer (other than Company or Limited Liability Partnership)

Customer’s full name(s)

Customer (if Company or Limited Liability

Partnership)

Business name

Molecular Profiles Limited

Registered number

03397582

Business address

0 Xxxxxxx Xxxxx, Xxxxxxxxxx Xxxxxxxx Xxxx, Xxxxxxxxxx,

Xxxxxxxx XX0 0XX

Continue listing of partners’ names on a separate sheet if necessary.

Business trading name

Business address

Postcode

2 Specific terms and conditions

Amount of the loan [excluding any amounts of interest that will be added to the loan if the agreement provides for this

£ 1,000,000

The proceeds of the loan are to be credited to:

Account name and amount (if not the amount of the loan)

Purpose of the loan

Molecular Profiles Limited

the continuation of your existing EIB loan, reference: 1199A/TM ,

it was agreed that this amount was to be used for: construction of new office & laboratory (the Project)

Branch sort code

301898

Account number

00000000

The loan is to be borrowed in:

One amount ¨

Several amounts x

Account name and amount (if not the amount of the loan)

If borrowed in several amounts each is to be not less than:

£ 10,000

Branch sort code

Account number

although the last amount borrowed may be smaller

If the loan is not borrowed within the period

agreed or, as the case may be, on the date agreed, you shall pay to the Bank any costs or losses to the Bank that may arise. These costs and losses are set out in Clause 2.3 of the General Terms and Conditions

The loan must be borrowed on or before

30/12/2012

Unless the Bank agrees otherwise:

a) no borrowing may be made until all the conditions

mentioned in Clause 2.1 of the Specific Terms and Conditions have been satisfied, and

b) you will not be entitled to borrow any amount which has not been borrowed

by the agreed date.

2 Specific terms and conditions continued

2.1

Preconditions and security

Unless received by the Bank prior to the date on which this agreement is signed by the Bank, the Bank is to receive in form and

substance acceptable to the Bank the security (if any) listed in the Security Schedule and the documents, evidence or other requirements of the preconditions (if any) set out in the Preconditions Schedule.

Any security received should be accompanied by such evidence as the Bank may reasonably require to confirm the value of such security and to confirm that such security is fully

effective.

2.2 Fees and costs

You shall pay any costs and expenses incurred

by the Bank in assessing the loan, in the preparation of this agreement, in the preparation, valuation, taking or release of any guarantee or security at any time, given in connection with this agreement and in connection with the revaluation of any

such security from time to time. The Bank will provide you with a written estimate of the amount of any such costs and expenses incurred by the Bank during the term of the loan before such costs are incurred

The following charges shall be paid by you on demand by the Bank. These charges are to be paid even if the loan is not borrowed. If these charges include any estimated costs or

fees, such costs or fees are based on the facts known to the Bank at the date the Bank signed this agreement. The actual amount charged to you in respect of these initial costs and expenses may be more or less than the figure(s) quoted.

As mentioned in Clauses 2, 3 & 6 of the General Terms and Conditions, other costs may arise in connection with the loan.

If during any fixed rate period you repay or are required to repay the loan early or in part under Clauses 2.2, 3.4, 5.5 or 6.1 of the General Terms and Conditions or under any

Additional Terms and Conditions, you shall pay to the Bank the administration fee and any Break Costs as provided in Clause 2.3 of the General Terms and Conditions and in addition (unless specified otherwise in this agreement) any early repayment

charges required by Section 2.6 of the Specific Terms and Conditions.

If during any variable rate period you repay or are required to repay the loan early or in

part under Clauses 2.2 or 5.5 of the General Terms and Conditions or under any Additional Terms and Conditions, you shall pay to the Bank (unless specified otherwise in this agreement any early repayment changes required by Section 2.6 of the

Specific Terms and Conditions

Arrangement fee

£

Option fee

£

Security costs

Estimated

Actual

£

Valuation fee

Estimated

Actual

£

2.3 Interest

Please cross only one box.

The rate of interest payable on the loan will be.

+ Do not use this option if dealing direct

with Treasury/Financial Markets division

‡ Use this option for Treasury/Finance Markets division fixed rate lending.

* Delete as appropriate.

¨ + Fixed Rate,

% per annum

* for the term of the loan/* until

the “Review Date”

x ‡Fixed

Rate,

1.56%

per annum above the rate (inclusive of regulatory costs - see

Clause 3.2 of the General Terms and Conditions) quoted by the Bank at about the time of borrowing

* for the term of the loan/* until

60 months after draw down

the “Review Date”

¨ ‡Fixed Rate,

%

per annum (inclusive of regulatory costs - see Clause 3.2 of the General Terms and Conditions)

* for the term of the loan/* until

the “Review Date”

If a fixed rate is specified above as being applicable to the loan for less than the term of the loan, the role of interest payable on the loan from the Review Date will (unless at

any time you request otherwise and the Bank agrees to such request) be:

Base Rate plus

1.95%

per annum, currently

2.45%

per annum in total

2.4 Payment of interest

Please complete only one section.

Interest shall be:

¨ paid by you.

The first interest payment date will be:

After that interest will be paid by you.

Monthly ¨

Quarterly ¨

added to the loan,

The first date

interest will be added to the loan is:

After that interest will be added to the loan:

Monthly ¨

Quarterly ¨

x paid by you until a certain date and then added to the loan.

The first interest payment date will be:

one month after drawdown

After that interest will be paid by you:

Monthly

x

Quarterly ¨

The first date interest will be added to the loan is

61 months after draw down

After that interest will be added to the loan:

Monthly

x

Quarterty ¨

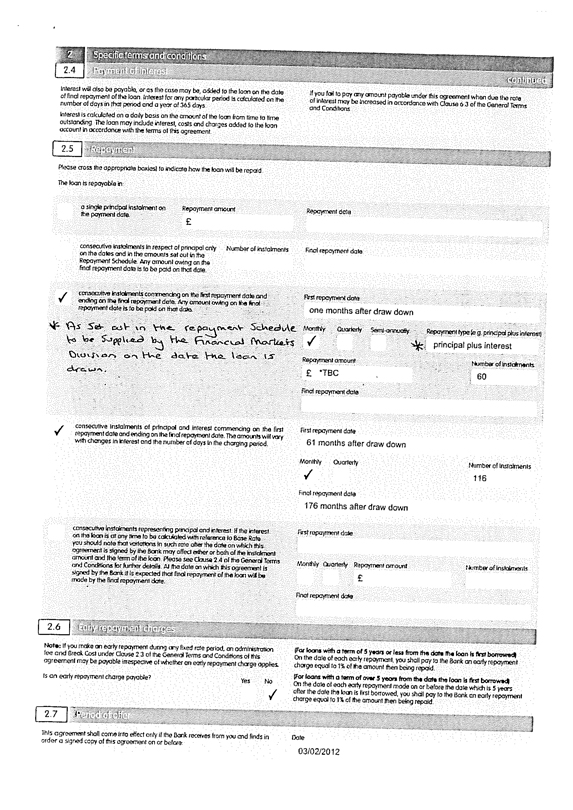

2 Specific terms and conditions

2.4 Payment of

interest continued

Interest will also be payable, or as the case may be, added to the loan on the date of final repayment of the loan. Interest for any particular

period is calculated on the number of days in that period and a year of 365 days.

Interest is calculated on a daily basis on the amount of the loan from time to

time outstanding. The loan may include interest, costs and charges added to the loan account in accordance with the terms of this agreement.

If you fail to pay any

amount payable under this agreement when due the rate of interest may be increased in accordance with Clause 6.3 of the General Terms and Conditions.

2.5 Repayment

Please cross the appropriate box(es) to indicate how the loan will be repaid

The loan is repayable in

¨ a

single principal instalment on the payment date

Repayment amount

£

Repayment date

¨ consecutive

instalments in respect of principal only on the dates and in the amounts set out in the Repayment Schedule. Any amount owing on the final repayment date is to be paid on that date.

Number of instalments

Final repayment date

x consecutive instalments commencing on the first repayment date and ending on the final repayment date. Any amount owing on the

final repayment date is to be paid on that date.

First repayment date

one

months after draw down

* As set out in the repayment Schedule to be Supplied by the Financial Markets Division on the date the loan is drawn.

x Monthly

¨ Quarterly

¨ Semi-annually

Repayment type (e.g. principal plus interest)

* principal plus interest

Repayment amount

£ *TBC

Number of instalments

60

Final repayment date

x consecutive instalments of principal and interest commencing on the First repayment date and ending on the final repayment date.

The amounts will vary with changes in interest and the number of days in the charging period.

First repayment date

61 months after draw down

Monthly x

Quarterly ¨

Number of

instalments

116

Final repayment date

176 months after draw down

¨ consecutive

instalments representing principal and interest. If the interest on the loan is at any time to be calculated with reference to Base Rate you should note that variations in such rate after the date on which this agreement is signed by the Bank may

affect either or both of the instalment amount and the term of the loan. Please see Clause 2.4 of the General Terms and Conditions for further details. At the date on which this agreement is signed by the Bank it is expected that final repayment of

the loan will be made by the final repayment date.

First repayment date

Monthly ¨

Quarterly ¨

Repayment amount

£

Number of instalments

Final repayment date

2.6 Early repayment charges

Note: If you make an early repayment during any fixed rate period,

an administration fee and Break Cost under Clause 2.3 of the General Terms and Conditions of this agreement may be payable irrespective of whether an early repayment charge applies.

Is an early repayment charge payable? Yes ¨ No x

(For loans with a term of 5 years or less from the date the loan is first borrowed)

On the

date of each early repayment, you shall pay to the Bank an early repayment charge equal to 1% of the amount then being repaid.

(For loans with a term of over 5

years from the date the loan is first borrowed)

On the date of each early repayment made on or before the date which is 5 years after the date the loan is first

borrowed, you shall pay to the Bank an early repayment charge equal to 1% of the amount then being repaid.

2.7 Period of offer

This agreement shall come into effect only if the Bank receives from you and finds in order a signed copy of this agreement on or before:

Date

03/02/2012

3 The schedules

Preconditions Schedule

The Bank has received in form and substance acceptable to it a full appraisal of the Project, including a detailed cashflow of the projected cost. The appraisal is to be prepared

by a party acceptable to the Bank and is to show no issues of concern to the Bank.

The Bank has received your written instruction for the loan monies to be placed

in an account with the Bank and between the following parties: Molecular Profiles Limited, Nominated Signatory from Three Sixty Project Management Limited and a Representative of the Quantity Surveyor (to be) nominated on behalf of Xxxxxx Xxxxxx.

The Bank has received such evidence as it may require to confirm that no less than £500,000 of your own moneys to be spent towards the Project has been

placed into an account with the Bank and between the following parties: Molecular Profiles Limited, Nominated Signatory from Three Sixty Project Management Limited and a Representative of the Quantity Surveyor (to be) nominated on behalf of Xxxxxx

Xxxxxx.

Security Schedule

An unlimited debenture from Molecular Profiles

Limited, and

A first legal charge from Molecular Profiles Limited over the freehold land and buildings at 0 Xxxxxxx Xxxxx, Xxxxxxxxxx Xxxxxxxx Xxxx, Xxxxxxxxxx,

XX0 0XX.

Repayment Schedule

Date

Amount

Date

Amount

4 General terms and conditions

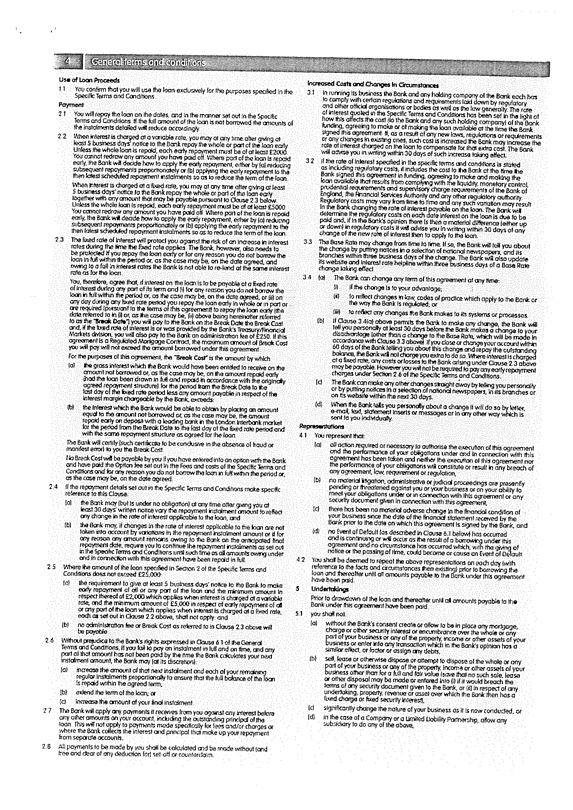

Use of Loan

Proceeds

1.1 You confirm that you will use the loan exclusively for the purposes specified in the Specific Terms and Conditions.

Payment

2.1 You will repay the loan on the dates, and in the manner set out in the Specific

Terms and Conditions. If the full amount of the loan is not borrowed the amounts of the instalments detailed will reduce accordingly.

2 .2 When interest is charged

at a variable rate, you may at any time after giving at least 5 business days notice to the Bank repay the whole or part of the loan early. Unless the whole loan is repaid, each early repayment must be of at least £2000. You cannot redraw any

amount you have paid off. Where part of the loan is repaid early, the Bank will decide how to apply the early repayment, either by (of reducing subsequent repayments proportionately or (b) applying the early repayment to the then latest scheduled

repayment instalments so as to reduce the term of the loan.

When interest is charged at a fixed rate, you may at any time after giving at least 5 business days

notice to the Bank repay the whole or part of the loan early together with any amount that may be payable pursuant to Clause 2.3 below. Unless the whole loan is repaid, each early repayment must be of at least £5000. You cannot redraw any

amount you have paid off. Where part of the loan is repaid early, the Bank will decide how to apply the early repayment, either by (a) reducing subsequent repayments proportionately or (b) applying the early repayment to the then latest scheduled

repayment instalments so as to reduce the term of the loan.

2.3 The fixed rate of interest will protect you against the risk of an increase in interest rates

during the time the fixed rate applies. The Bank, however, also needs to be, protected if you repay the loan early or for any reason you do not borrow the loan in full within the period or, as the case may be, on the date agreed, and owing to a fall

in interest rates the Bank is not able to re-lend at the same interest rate as for the loan.

You, therefore, agree that, if interest on the loan is to be payable

at a fixed rate of interest during any part of its term and (i) for any reason you do not borrow the loan in full within the period or, as the case may be, on the date agreed, or (ii) on any day during any fixed rate period you repay the loan early

in whole or in part or are required (pursuant to the terms of this agreement to repay the loan early(the date referred to in (i) or, as the case may be, (ii) above being hereinafter referred to as the “Break Date”) you will pay to the Bank

on the Break Date the Break Cast and, if the fixed rate of interest is or was provided by the Bank’s Treasury/Financial Markets division, you will also pay to the Bank an administration fee of £250. If this agreement is a Regulated

Mortgage Contract, the maximum amount of Break Cost you will pay will not exceed the amount borrowed under this agreement

For the purposes of this agreement, the

“Break Cost” is the amount by which:

(a) the gross interest which the Bank would have been entitled to receive on the amount not borrowed or, as the case

may be, on the amount repaid early (had the loan been drawn in full and repaid in accordance with the originally agreed repayment structure) for the period from the Break Date to the last day of the fixed rate period less any amount payable in

respect of the interest margin chargeable by the Bank, exceeds:

(b) the interest which the Bank would be able to obtain by placing an amount equal to the amount

not borrowed or, as the case may be, the amount repaid early on deposit with a leading bank in the London Interbank market for the period from the Break Date to the last day of the fixed rate period and with the same repayment structure as agreed

for the loan.

The Bank will certify (such certificate to be conclusive in the absence of fraud or manifest error) to you the Break Cost.

No Break Cost will be payable by you if you have entered into an option with the Bank and have paid the Option fee set out in the Fees and costs of the Specific Terms and

Conditions and for any reason you do not borrow the loan in full within the period or, as the case may be, on the date agreed.

2.4 If the repayment details set out

in the Specific Terms and Conditions make specific reference to this Clause:

(a) the Bank may (but is under no obligation) at any time after giving you at least 30

days’ written notice vary the repayment instalment amount to reflect any change in the rate of interest applicable to the loan, and

b) the Bank may, if

changes in the rate of interest applicable to the loan are not taken into account by variations in the repayment instalment amount or if for any reason any amount remains owing to the Bank on the anticipated final repayment date, require you to

continue the repayment instalments as set out in the Specific Terms and Conditions until such time as all amounts owing under and in connection with this agreement have been repaid in full.

2.5 Where the amount of the loan specified in Section 2 of the Specific Terms and Conditions does not exceed £25,000:

(a) the requirement to give at least 5 business days, notice to the Bank to make early repayment of all or any part of the loan and the minimum amount in respect thereof of

£2,000 which applies when interest is charged at a variable rate, and the minimum amount of £5,000 in respect of early repayment of all or any part of the loan which applies when interest is charged at a fixed rate, each as set out in

Clause 2.2 above, shall not apply and

(b) no administration fee or Break Cost as referred to in Clause 2.3 above will be payable.

2.6 Without prejudice to the Bank’s rights expressed in Clause 6.1 of the General Terms and Conditions, if you fail to pay an instalment in full and on time, and any part of

that amount has not been paid by the time the Bank calculates your next instalment amount, the Bank may (at its discretion):

(a) increase the amount of that next

instalment and each of your remaining regular instalments proportionally to ensure that the full balance of the loan is repaid within the agreed term,

(b) extend

the term of the loan; or

(c) increase the amount of your final instalment

2.7

The Bank will apply any payments it receives from you against any interest before any other amounts on your account, including the outstanding principal of the loan. This will not apply to payments made specifically for fees and/or charges or where

the Bank collects the interest and principal that make up your repayment from separate accounts.

2.8 All payments to be made by you shall be calculated and be made

without (and free and clear of any deduction for) set-off or counterclaim.

Increased Costs and Changes In Circumstances

3.1 In running its business the Bank and any holding company of the Bank each has to comply with certain regulations and requirements laid down by regulatory and other official

organisations or bodies as well as the law generally. The rate of interest quoted in the Specific Terms and Conditions has been set in the light of how this affects the cost (to the Bank and any such holding company) of the Bank funding, agreeing to

make or of making the loan available at the time the Bank signed this agreement. If, as a result of any new laws, regulations or requirements or any changes in existing ones, such cost is increased the Bank may increase the rate of interest charged

on the loan to compensate for that extra cost. The Bank will advise you in writing within 30 days of such increase taking effect.

3.2 If the rate of interest

specified in the specific terms and conditions is stated as including regulatory costs, it includes the cost to the Bank at the time the Bank signed this agreement in funding, agreeing to make and making the loan available that results from

complying with the liquidity, monetary control, prudential requirements and supervisory charge requirements of the Bank of England, the Financial Services Authority and any other regulatory authority. Regulatory costs may vary from time to time and

any such variation may result in the Bank changing the rate of interest payable on the loan. The Bank will determine the regulatory costs on each date interest on the loan is due to be paid and, if in the Bank’s opinion there is then a material

difference (either up or down) in regulatory costs it will advise you in writing within 30 days of any change of the new rate of interest then to apply to the loan.

3.3 The Base Rate may change from time to time. If so, the Bank will tell you about the change by putting notices in a selection of national newspapers, and its

branches within three business days of the change. The Bank will also update its website and interest rate helpline within three business days of a Base Rate change taking effect.

3.4 (a) The Bank can change any term of this agreement at any time:

(i) if the change is to

your advantage,

(ii) to reflect changes in law, codes of practice which apply to the Bank or the way the Bank is regulated; or

(iii) to reflect any changes the Bank makes to its systems or processes.

(b) If Clause 3.4(a)

above permits the Bank to make any change, the Bank will left you personally at least 30 days before the Bank makes a change to your disadvantage (other than a change to the Base Rate, which will be made in accordance with Clause 3.3 above). If you

close or change your account within 60 days of the Bank telling you about this change and repay the outstanding balance, the Bank will not charge you extra to do so. Where interest is charged at a fixed rate, any costs or losses to the Bank arising

under Clause 2-3 above may be payable. However you will not be required to pay any early repayment charges under Section 2.6 of the Specific Terms and Conditions.

(c) The Bank can make any other changes straight away by telling you personally or by putting notices in a selection of national newspapers, in its branches or on

its website within the next 30 days.

(d) When the Bank tells you personally about a change it will do so by letter, e-mail, text, statement inserts or messages or

in any other way which is sent to you individually.

Representations

4.1 You

represent that:

(a) all action required or necessary to authorise the execution of this agreement and the performance of your obligations under and in connection

with this agreement has been taken and neither the execution at this agreement nor the performance of your obligations will constitute or result in any breach of any agreement, law, requirement or regulation,

(b) no material litigation, administrative or judicial proceedings are presently pending or threatened against you or your business or on your ability to meet your obligations

under or in connection with this agreement or any security document given in connection with this agreement,

(c) there has been no material adverse change in the

financial condition of your business since the date of the financial statement received by the Bank prior to the date on which this agreement is signed by the Bank, and

(d) no Event of Default (as described in Clause 6.1 below) has occurred and is continuing or will occur as the result of a borrowing under this agreement and no circumstance has

occurred which, with the giving of notice or the passing of time, could become or cause an Event of Default.

4.2 You shall be deemed to repeat the above

representations on each day (with reference to the facts and circumstances then existing) prior to borrowing the loan and thereafter until all amounts payable to the Bank under this agreement have been paid.

5 Undertakings

Prior to drawdown of the loan and thereafter until all amounts payable to the

Bank under this agreement have been paid.

5.1 you shall not:

(a) without the

Bank’s consent create or allow to be in place any mortgage, charge or other security interest or encumbrance over the whole or any part of your business or any of the property, income or other assets of your business or enter into any

transaction which in the Bank’s opinion has a similar effect, or factor or assign any debts,

(b) sell, lease or otherwise dispose or attempt to dispose of the

whole or any part of your business or any of the property, income or other assets of your business other than for a full and fair value (save that no such sale, lease or other disposal may be made or entered into (i) if it would breach the terms of

any security document given to the Bank, or (ii) in respect of any undertaking, property, revenue or asset over which the Bank then has a fixed charge or fixed security interest).

(c) significantly change the nature of your business as it is now conducted, or

(d) in the

case of a Company or a Limited Liability Partnership, allow any subsidiary to do any of the above.

4 General terms and conditions continued

5.2 you

shall promptly provide the Bank with copies of any financial information that the Bank may from time to time reasonably request, including but not limited to;

(a)

copies of your financial statement within 180 days of the end of each financial year, and

(b) copies of your periodic management accounts of such intervals as the

Bank may require in a form acceptable to the Bank within 30 days of the end of the period to which they relate. The Bank may at its option require such management accounts to incorporate an age-analysis of debtors, a schedule of all tenancies (if

any) of any property held by the Bank as security at the date of the accounts, and/or a breakdown of stock in trade.

5.3 you shall maintain with reputable

underwriters or insurance companies adequate insurance on and over your business and the assets of your business, such insurance to be against such risks and to the extent usual for persons carrying on a business such as that carried on by you and,

from time to time upon request of the Bank, you shall furnish the Bank with evidence of such Insurance.

5.4 If you have taken out a general insurance policy in

connection with the loan, the Bank will hold any money the Bank receives in relation to the insurance including any claims payments paid to the Bank by the Insured in its capacity as a bank approved by the Financial Services Authority, rather than

as a trustee for you (or in Scotland as on agent for you), and the Financial Services Authority’s client money rules do not apply to the money so held. Any insurance benefits the Bank receives from your insurance company, relating to the

repayment of the loan, will be used towards paying off what you owe in this agreement.

5.5 If the ratio of the loan to the value of the security given to the Bank

is at any time higher than that applicable on the date this agreement was signed by the Bank and unless any specific requirement is set out in any Additional Terms and Conditions added to this agreement (which requirement shall take precedence over

this Clause) you agree promptly to:

(a) reduce the loan (in accordance with Clause 2 above including paying any costs or losses to the Bank arising under Clause

2.3 above and any early repayment charges it required under Section 2.6 of the Specific Terms and Conditions), or

(b) provide the Bank with additional

security acceptable to the Bank, and

(c) provide such evidence as the Bank may from time to time require to confirm the value of such security and to confirm that

the security remains effective.

The Bank may have the security given to it revalued at any time during the term of the loan where, for example, the Bank needs to

meet any regulatory requirements or to check that the value continues to be adequate security for repayment of the loan. You will pay the cost incurred by the Bank (acting reasonably) for each revolution.

5.6 you shall conform at all times with all applicable EU and national laws including, but not limited to, environmental laws (as defined in Clause 7.16 below).

5.7 you shall, from time to time and upon reasonable notice given by the Bank

(following a

request made by the European Investment Bank to the Bank), permit any person(s) appointed by the European Investment Bank or any person(s) with appropriate authority from the Court of Auditors at the European Commission to inspect all sites.

Installations and works used by you and connected in any way with the purposes specified In the Specific Terms and Conditions, the inspection being for the purpose of ascertaining whether you are using the loan exclusively for those purposes in

accordance with the terms and conditions of this agreement, and you shall provide such persons with all necessary assistance and information for such on inspection [the Bank reserves the right to appoint a person to accompany the person appointed by

the European Investment Bank or authorised by the European Commission on such an inspection), and

5.8 you shall deliver to the Bank such Information as the

European Investment Bank shall reasonably require concerning your activities and general financial position and you hereby agree that the Bank may disclose such information including, but not limited to, the financial statement] to the European

Investment Bank.

Default and Termination

6.1 The events listed in (a) to

(j) of this Clause 6.1 are called “Events of Default” As

soon as an Event of Default happens or at any time thereafter, by giving notice to you, the

Bank may cancel any obligations it has to fend money to you and may also make the loan become repayable on demand. When the loan is repayable on demand, you must repay the loan to the Bank together with all interest which has accrued on the loan and

any other amounts owing under or in connection with this agreement including any costs and losses arising under Clause 2.3 above but you will not be required to pay any early repayment charges under Section 2.6 of the Specific Terms and

Conditions) as soon as the Bank requests you to pay these amounts. The Bank may do this at the time the loan becomes repayable on demand or at any later time.

Events of Default

(a) you fail to pay when due any indebtedness owed by you

to the Bank.

(b) you fail to comply with any other obligation or undertaking to the Bank, or with the terms of this agreement or any other agreement with the Bank,

or an event of default arises in connection with any other agreement with the Bank,

(c) you fail to pay when due any indebtedness owed by you to another creditor

or any of your creditors changes (or obtains the right to change the original date on which that indebtedness is or was due to be paid to an earlier date or a result of your failure to comply with obligations in connection with that Indebtedness.

(d) any representation or statement mode by you to the Bank, whether or not in connection with this agreement, proves to have been incorrect or inaccurate when

made or deemed made.

(e) any guarantee, other security or other document or arrangement relied upon by the Bank in connection with the loan ceases to be continuing

or ceases to remain fully effective or notice of discontinuance is received by the Bank or if the Bank reasonably believes that the effectiveness of any such document or arrangement is in doubt or If any provision of such document or arrangement Is

not complied with for any reason or any favourable tax treatment afforded to any pension policy or to any life policy held by or charged to the Bank ceases to be available.

(f) In the case of a Company or a Limited Liability Partnership:

(i) any person with a legal

claim takes possession or a receiver, administrator, custodian, trustee, liquidator or similar official is appointed of the whole or any part of your business or of any of the assets of your business or an administration application is presented or

made for the making of an administration order or a notice of intention to appoint on administrator is issued by you or your directors or (in the case of a Limited Liability Partnership) your members or by the holder of a qualifying floating charge

or notice of appointment of an administrator is filed by any person with the court or a Judgment, decree or diligence Is made or granted against you,

(ii)

proceedings are commenced or a petition is presented or an order is made or a resolution is passed for your winding up or you are or become insolvent,

(iii) you

stop or threaten to stop payment of your debts generally or you are deemed by law unable to pay your debts or you or your directors or (in the case of a Limited Liability Partnership) your members convene or become obliged to convene a meeting of

shareholders, members or creditors with a view to winding up or an application is made in connection with a moratorium or a proposal to creditors for a voluntary arrangement is made by you or you take any action (including entering negotiations)

with a view to readjustment, rescheduling, forgiveness or deferred of any part of your indebtedness,

(v) the persons who now control you cease to have such

control, or

(v) any of the events set out in this Clause 6.1(f) occur in relation to any parent or subsidiary or any guarantor of or provider of security or the

loan or, in the case of any individual that provides any guarantee or other security for the loan, a petition is presented for a bankruptcy or sequestration order against any such individual or any such individual dies or becomes incapable of

managing his or her affairs by reason of mental disorder, or any action is taken in any jurisdiction which is similar or analogous to any of these events in respect of you or any of the aforementioned parties. (g) in all other cases

(i) any person with a legal claim takes possession or a receiver.

administrator judicial

factor, interim trustee, trustee in sequestration or similar official is appointed of the whole or any part of your business or of any of your business assets or on application or a petition Is presented or made for either on administration or a

bankruptcy order against you or a judgment, decree or diligence is made or granted against you,

(ii) a petition is presented or an order is made for your winding

up (if you are a partnership) or you resolve either to cease trading or to wind up your business in any way or dissolve such business for any reason,

(iii) you

stop or threaten to stop payment of your debts generally or you are deemed by tow unable to pay your debts or on application is made in connection with a moratorium or a proposal to creditors for a voluntary arrangement by you or you take any action

(including entering negotiations) with a view to readjustment, rescheduling, forgiveness or deferral of any part of your indebtedness, (iv) you die or become Incapable of managing and administering your property and affairs by reason of mental

disorder or (if you are a partnership) there is any change in the membership of partnership, or

(v) any of the events set out in this Clause 6.1(g) occur in

relation to any guarantor of or provider of security for the loan or any action is taken In any jurisdiction which is similar or analogous to any of these events in respect of you or any guarantor of or provider of security,

(h) you cease or threaten to cease to carry on your business in the normal course or you fail to maintain or breach any franchise, licence or right necessary to conduct your

business or breach any legislation relating to your business, inducing but not limited to any applicable environmental protection laws,

(i) you fail or have failed

to disclose to the Bank any important Information that is relevant to the loan or the security required or you undertake or are subject to any action or occurrence which the Bank reasonably believes could place at risk the payment of any amount

owing to the Bank, or

(j) you do not have a servicing account

6.2 If any

Event of Default happens or anything happens that might reasonably be expected to lead to an Event of Default, you shall inform the Bank Immediately

6.3 If any

amount payable to respect of this agreement is not paid when due (including any amount payable under this Clause 6) we may require you to pay interest on that amount at the default rate from the date on which the amount was due until it is paid to

the Bank (whether before or after Judgment). Interest, if unpaid, may be added to the amount in default at monthly intervals. The default rate shall be the rate determined by the Bank to be 3% per annum higher than the rate of interest

specified in the Specific Terms and Conditions that would normally apply.

6.4 You shall indemnify the Bank against any costs incurred or losses reasonably

sustained by the Bank as the result of any Event of Default happening or any failure by you to pay any amount demanded by the Bank as a result of an Event of Default

6.5 You shall also pay any costs and expenses reasonably incurred by the Bank in enforcing or perfecting any security for the loan and in enforcing or preserving

its rights under this agreement.

Other

7.1 This agreement (and any

non-contractual obligations arising out of or in connection with this agreement) shall be construed and have effect in accordance with the applicable law and is subject to the jurisdiction of the Courts in the jurisdiction of the applicable law. The

applicable law will be the laws of England and Wales or the laws of Scotland, it will be the governing law of the country in which the branch or office of the Bank given at the heading of this agreement is situated on the date this agreement is

signed by the Bank. The Bank may take action against you in any other jurisdiction where proceedings may be lawfully commenced.

4 General terms and conditions continued

7 2 No

delay or omission by the Bank in exercising any of its rights hereunder shall operate or be construed as a waiver, nor shall any single or partial exercise of any such right prevent any other or further exercise of any other right.

7 3 if the loan is to be borrowed, or if any payment becomes due from you, on a day which is not a business day then the amount concerned will be borrowed or, as the case may be,

will become payable on the next business day.

7 4 The Bank may use any credit balance there may be an any of your accounts held with the Bank towards payment of

any amounts owed by you to the Bank under this agreement without notifying you beforehand, whether such credit balances are in sterling or any other currency or are deposited for fixed or determinable periods

7.5 Unless otherwise agreed by the Bank you shall at all times during the term of this agreement keep a servicing account with the Bank and all amounts from time to time due to the

Bank under this agreement may be debited to that account. The Bank recommends that you make sure you have enough funds to meet all such payments as they become due. If you do not maintain such an account with the Bank, the Bank may (without

prejudice to its rights under Cause 6.1 above) add to your loan account any interest that is to be paid by you but which is not paid on the date it is due for payment. The Bank may charge interest on any amount so added to the loan account.

7.6 Any security given to the Bank (whether given before the date on which this agreement is signed by the Bank or at any time in the future and whether or not

specified in this agreement shall, unless otherwise agreed by the Bank, be security not only for the loan but also for all other moneys and liabilities whether certain or contingent at any time due, owing or incurred by you to the Bank.

7.7 The Bank may sell, assign, transfer, securities or otherwise dispose of in any manner its rights or obligations under this agreement to any other person, or enter into

transactions which have the effect of transferring the economic or credit risks and/or rewards of the Bank under this agreement with any other person. You will promptly execute any documents that the Bank may reasonably require to give effect to any

such assignment, assignation, transfer, securitisation or other disposal. You may not assign, transfer or otherwise dispose of any of your rights, obligations or benefits under this agreement.

7.8 In the event of, or in connection or contemplation of, a proposed sale, assignment, securitisation, transfer or other disposal of risks and/or rewards of the loan for part of

it or sale, assignment, transfer, securitisation or other disposal of any of the Bank’s rights under this agreement the Bank may disclose information about you, your finances and this agreement to any potential purchaser, assignee, transferee,

counterparty to an agreement transferring risks and/or rewards, rating agencies, listing authorities, their and our advisers, or any other person to whom the Bank may deem it necessary to disclose such information to in relation to any proposed

sale, securitisation, transfer, assignment or transfer of risks and/or rewards,

7.9 You consent to the Bank disclosing information about you, your finances and

this agreement to any person providing any security for any of your obligations, and to them giving us information about you

7.10 This agreement and all

communications from you to the Bank in connection with this agreement and the loan (all of which are to be sent in writing to the Bank) shall, in the case of a Company or Limited Liability Partnership, be signed an your behalf either in accordance

with the mandate given by you to the Bank, or if requested by the Bank, in accordance with a specific resolution of your Board of Directors/Members, or in the case of a partnership, shall be signed by all partners unless otherwise agreed by the

Bank, or in all other cases, shall be signed in accordance with the mandate given by you to the Bank.

7.11 Any change to this agreement other than the changes to

be made by the Bank as provided in this agreement must be mode in writing and be signed by the contracting parties.

7.12 If the loan is available to more than one

person, each and every undertaking and liability of all of you under and in connection with this agreement shall be joint and several and references to you shall mean any one or more of you. Therefore each of you is jointly and separately

responsible for complying with the terms and conditions of this agreement and for repaying all the liabilities under this agreement and not just a share of them. The Bank may take action against all or any one of you

7.13 This agreement is for the benefit of the contracting parties only and shall not confer any benefit on or be enforceable by a third party

7.14 The Specific Terms and Conditions and General Terms and Conditions together with any Additional Terms and Conditions attached to this agreement shall be read and construed as

one agreement

7.15 In this agreement the following terms shall have the following meanings: the “Bank” includes its successors and assigns.

“Base Rates” means the official bank rate from time to time of Bank of England (or any rate at any time replacing that rate) which will be displayed in the Bank’s

branch where your account is held and on the Bank’s website, currently xxx.xxxxxxxxx.xxx/xxxxxxxx, and may be varied (either up or down) by the Bank of England at any time. “a business day” means a day other than a Saturday or a

Sunday on which banks are open for normal business in the jurisdiction of the applicable law “control” shall have the meaning given to it in Section 840 of the Income and Corporation Taxes Act 1906 or any amendment to or restatement

of that Act for the time being in force “current account” means your main business current account with the Bank “environment” means the following, in so far as they affect human well-being (a) fauna and flora;

(b) soil, water, air, climate and the landscape, and (c) cultural heritage and the built environment “environmental laws” means EU law and national laws and regulations as apply in the jurisdiction of the applicable law referred to in

Clause 7.1 above, as well as applicable international treaties, of which a principal objective is the preservation, protection or improvement of the environment “financial statement” means at any particular time the latest balance sheet

and profit and loss account of your business together with the notes to both. You must ensure they are audited or signed by an independent accountant if required by law or if reasonably required by the Bank. YOU must also ensure that,

unless the Bank allows otherwise (the Bank will not unreasonably withhold or delay its permission), they are prepared on the same basis and (except to the extent necessary to reflect any changes In generally accepted accounting principles) in

accordance with the same accounting principles as the latest such balance sheet and profit and loss account received by the Bank prior to the date on which this agreement is signed by the Bank.

“loan” means, of any particular time, the total amount which may be borrowed by you under this agreement or, if appropriate, the total amount which has been debited to

the loan account and remains outstanding at such time. The loan may, at any time, include any interest, costs and charges added to the loan account in accordance with this agreement.

“month” means a calendar month.

“parent” and subsidiary” shall have

respectively the meaning given to parent undertaking and subsidiary undertaking in Section 1162 of the Companies Xxx 0000 or any amendment to or restatement of that Act for the time being in force. During any period in which you do not have a

subsidiary, all references to your subsidiaries shall be ignored and the relevant text read and construed accordingly. “Regulated Mortgage Contract” means a contract where the loan is provided to on individual (i.e. sole trader or

partnership) and the loan is secured by a first legal mortgage on land in the UK where at least 40% of that land is used or is intended to be used as or in the connection with a dwelling by the borrower or a close family member.

“servicing account” means an account through which the Bank channels your and the Bank’s payments under this agreement. You may use your current account with the

Bank as your servicing account.

“your business” shall include, in the case of a Company or a limited liability Partnership, the business of your

subsidiaries

7.16 The Bank will not be liable for any loss, damage, interruption, delay or non-performance in connection with this agreement to the extent that it

is caused by events which are beyond the Bank’s reasonable control which may include for example explosion, terrorism, war, riot or other civil disturbance or failure or interruption of any electronic communications system caused by someone

else

7.17 If you do not pay the Bank what you owe under this agreement and the Bank does not require you to pay interest on that amount at the default rate

pursuant to Cause 6.3 above and the Bank obtains judgment against you in a court,

the Bank may continue to charge interest on the judgment amount at the role

specified in Section 2.3 of the Specific Terms and Conditions of this agreement.

7.18 If any term or provision in this agreement shall in whole or in part be

held to any extent to be invalid, void, illegal or unenforceable under any enactment or rule of law, that term or provision shall to that extent be deemed not to form part of

this agreement and the enforceability of the remainder of this agreement shall not be affected

7.19 You may at any time substitute any property charged to the Bank with alternative property If the alternative property has a value at least equal to the value

of the property to be released. When the Bank is satisfied that the alternative security is fully effective, it will discharge the security being substituted. Use of Personal Information and Credit, Fraud and Identification Checks When you apply to

open an account, we will check our own records for information on individuals who are Key Account Parties. “Key Account Parties” are individual who are sole traders, proprietors, partners, directors, members, beneficial owners, trustees or

other controlling officials of the business or organisation including signatories to the account.

We may also carry out a search through credit reference agencies

on these individuals. The credit reference agencies will keep a record of this search and this record may be used by other organisations to verify their identities. We may also check or share information with fraud prevention agencies to prevent

fraud and money laundering. When you apply for credit and credit related or other facilities, we may carry out a search through credit reference agencies on you and/or Key Account Parties. The credit reference agencies will keep a record of this

search whether or not the application proceeds. A record of the search on personal files will not be made available to other organisations. A record of the search on the business We will be made available to other organisations. We may also check or

share Information with fraud prevention agencies to prevent fraud and money laundering

When you have an account with us, we may disclose how you have run your

account(s) to credit reference agencies. If you borrow and do not repay in full and on time, we may tell the credit reference agencies. We may make periodic searches of the Lloyds Barking Group records and credit reference agencies to manage your

account(s) including to make decisions whether to continue or extend existing credit The Lloyds Banking Group includes us and a number of other companies using brands including Xxxxxx X00, Xxxxxxx and Bank of Scotland, and their associated companies

More information on the Lloyds Banking Group can be found at xxx.xxxxxxxxxxxxxxxxxx.xxx.

For these purposes “associated companies” includes Lloyds

Banking Group plc and any subsidiary, affiliate or other firm directly or indirectly controlled from time to time by either Lloyds Banking Group plc or us.

We may

also check and share information with fraud prevention agencies to prevent fraud and money laundering

If false or Inaccurate information is provided or fraud is

suspected, details may be passed to fraud prevention agencies and other relevant agencies.

If you or Key Account Parties ask, we will let you or them which credit

reference and fraud prevention agencies we have used so you or they can get a copy of your or their details from these agencies.

This is a condensed guide to the

use of your personal and business information by us and at credit reference and fraud prevention agencies. If you would like to read full details of how data may be used, please visit our website at xxx.xxxxxxxxx.xxx/xxxxxxxxxx/xxxxxxxxxxxx or

contact your relationship manager or relationship team

5 Declaration for exemption relating to businesses (sections 16B and 189(1) and (2) Consumer Credit Act

1974)

Only applicable if you are a sole trader or a partnership of two or three partners or on unincorporated body)

I am/We are* entering this agreement wholly or predominantly for the purposes of a business carried an by me/us* or intended to be carried on by me/us * l/We* understand that I/we*

will not have the benefit of the protection and remedies that would be available to me/us* under the Consumer Credit Xxx 0000 II this agreement were a regulated agreement under that Act

I/We* understand that this declaration does not affect the powers of the court to make an order under section 140B of the Consumer Credit Xxx 0000 in relation to a credit agreement

where it determines that the relationship between the creditor and the debtor is unfair to the debtor

I am/We are* aware that, If I am/we are* in any doubt as to

the consequences of the agreement not being regulated by the Consumer Credit Xxx 0000 I/we should seek independent legal advice.

*Delete as appropriate.

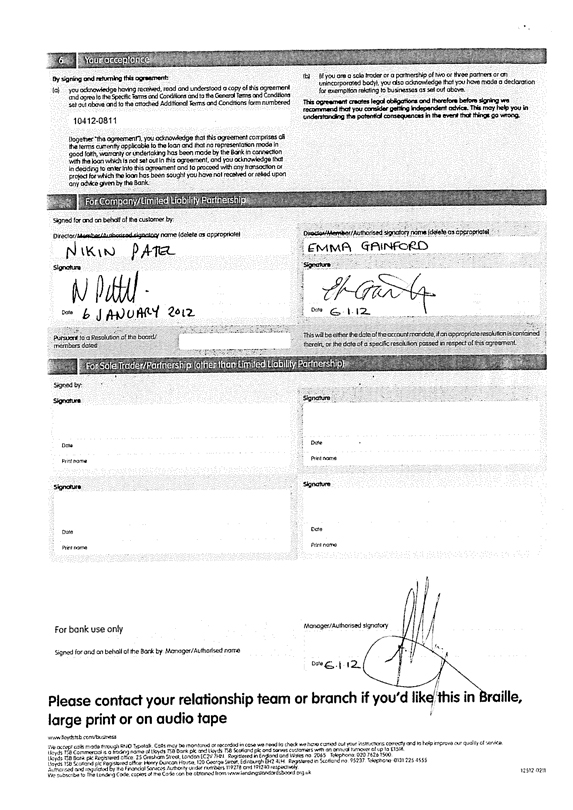

6 Your acceptance

By signing and returning this

agreement:

(a) you acknowledge having received, read and understood a copy of this agreement and agree to the Specific: Terms and Conditions and to the General

Terms and Conditions set out above and to the attached Additional Terms and Conditions forms numbered

10412-0811

(together “the agreement”), you acknowledge that this agreement comprises all the terms currently applicable to the loan and that no representation made In good faith,

warranty or undertaking has been mode by the Bank in connection with the loan which Is not set out In this agreement, and you acknowledge that in deciding to enter into this agreement and to proceed with any transaction or project for which the loan

has been sought you hove not received or relied upon any advice given by the Bank.

(b) (if you are a sole trader or a partnership of two or three partners or an

unincorporated body) you also acknowledge that you have made a declaration for exemption relating to businesses as set out above.

This agreement creates legal

obligations and therefore before signing we recommend that you consider taking independent advice. This may help you understand the potential consequences in the event that things go wrong.

Please note that if interest is to be, or is, payable at a fixed rate and you do not borrow the loan within period agreed or, as the case may be, on the date agreed or, for any

reason, you repay early or are required to repay early, the loan or any part of the loan, you will have to compensate the Bank for its costs and losses.

For

Company/Limited Liability Partnership

Signed for and on behalf of the customer by:

Director/name (delete as appropriate) Director/ Authorised signatory name (delete as appropriate)

Xxxxx Xxxxx XXXX GAINFORD

Date 6 January 2012

Signature Signature

/s/ Xxxxx Xxxxx /s/ EMMA GAINFORD

Date 6.1.12

Pursuant to a Resolution of the board/ members dated

This will be either the date of the account mandate, if an appropriate resolution is contained therein or the date of a specific resolution passed in respect of this agreement.

For Sole Trader/Partnership (other than Limited Liability Partnership)

Signed

by

Signature

Date

Print name

Signature

Date

Print name

Signature

Date

Print name

Signature

Date

Print name

For bank use only Manager/Authorized Signatory

Signed for and on behalf of the Bank by :

Manager/Authorised name /s/ Xxx Xxxxx

Date 6112

Please contact your

relationship team or branch if you’d like this in Braille, large print or on audio tape

xxx.xxxxxxxx.xxx/xxxxxxxx

We accept calls made through RNID Typetalk. Calls may be monitored or recorded in case we need to check we have carried out your instructions correctly and to help improve our

quality of service.

Lloyds TSB Commercial is a trading name of Lloyds TSB Bank plc and Lloyds TSB Scotland plc and serves customers with an annual turnover of up

to £15M.

Lloyds TSB Bank plc Registered office 00 Xxxxxxx Xxxxxx Xxxxxx XX0X Registered in England and Wales no. 2065 Telephone 000 0000 0000.

Lloyds TSB Scotland plc Registered office Xxxxx Xxxxxx Xxxxx, 000 Xxxxxx Xxxxxx, Xxxxxxxxx XX0 00X Registered in Scotland no 95237 Telephone 0000 000 0000

Authorised and regulated by the Financial Services Authority under numbers 119278 and 191240 respectively. We subscribe to The Lending Code, copies of the Code can be obtained from

xxx.xxxxxxxxxxxxxxxxxxxxxx.xxx.xx.

12511-0211

| Additional Terms and Conditions Financial Covenants |

|

Please contact your business team or branch if you’d like this in Braille, large print or on audio tape. We accept calls made through RNID Typetalk. Calls may be monitored or recorded in case we need to check we have carried out your instructions correctly and to help improve our quality of service.

When this document has been signed by x Lloyds TSB Bank plc Lloyds TSB Scotland plc (the “Bank” and Molecular Profiles Limited *carrying on business under the name of the terms and conditions below marked with an “X” will be added to the terms and conditions set out in the BUSINESS LOAN AGREEMENT which was signed by the Bank on (the “Agreement”). These Additional Terms and Conditions shall apply for as long as any moneys are owing to the Bank under the Agreement or the Bank is under any obligation under the Agreement.

The covenants will be tested at the frequency annotated below against (a) each financial statement, if the covenant is marked as being tested annually, and/ or (b) against your management accounts or, if appropriate, against your tenancy schedules, if the covenant is marked as being tested monthly or quarterly For the avoidance of doubt:

| (a) | you are required to provide the Bank with sufficient information to enable the Bank to test the covenants. This information is to be provided pursuant to the Agreement, and |

| (b) | the covenants will be tested for the period of the accounts unless, in the case of a monthly or quarterly test the covenant is also marked as being tested on a rolling 12 months. In this case, each test will be for the 12 month period ending on the test date. |

| Frequency of Covenant testing | ||||||||||||

| Monthly | Quarterly | Annually | Rolling 12 months | |||||||||

| CFADS to debt service | CFADS is not at any time to be less than % of the aggregate of the consolidated principal repayments and the consolidated interest paid and payable (whether to the Bank or to any other person,) for the period covered by the accounts. | ¨ | ¨ | ¨ | ¨ | |||||||

| EBITDA to debt service | EBITDA is not at any time to be less than % of the aggregate of the consolidated principal repayments and the consolidated interest paid and payable (whether to the Bank or to any other person) for the period covered by the accounts. | ¨ | ¨ | ¨ | ¨ | |||||||

| Minimum retained profit | Retained Profit of not less than £ is to be reported in each financial statement (commencing with the financial statement as at | ¨ | ||||||||||

| Interest cover | Your consolidated Profit Before Taxation and interest paid and payable is not at any time to be less than % of the consolidated interest paid and payable (whether to the Bank or to any other person, for the period covered by the accounts | ¨ | ¨ | ¨ | ¨ | |||||||

| Gross rental cover | The total Rental Income received by you from all Property is not at any time to be less than % of the aggregate of the principal repayments and the interest paid and payable to the Bank for the period covered by the accounts | ¨ | ¨ | ¨ | ¨ | |||||||

| Minimum gross rent | The total rental income received by you from all Property is not for any year to be less than £ | ¨ | ¨ | ¨ | ¨ | |||||||

| Frequency of Covenant testing | ||||||||||||

| Monthly | Quarterly | Annually | ||||||||||

| x | Minimum net worth | Net Worth is at all times to be maintained at not less than £ 4,000,000 | ¨ | ¨ | x | |||||||

| Gearing | Borrowing is not at any time to exceed % of Net Worth | ¨ | ¨ | ¨ | ||||||||

| Good trade debtors cover | Good Book Debts (after taking into account any amounts ranking in priority to amounts owing to the Bank) are not at any time to be less than % of your utilisation of all facilities provided to you by the Bank. | ¨ | ¨ | ¨ | ||||||||

| Loan to value | The total amount owing to the Bank (whether certain or contingent) by you is not at any time to exceed the aggregate of % of the latest valuation received by the Bank of all Property (after taking into account any amounts ranking in priority to amounts owing to the Bank) | ¨ | ¨ | ¨ | ||||||||

| * | delete as appropriate |

Definitions

Borrowing shall include all your land, if you have any subsidiaries, all of your subsidiaries’) borrowed moneys and all liabilities and indebtedness, whether or not then due, under acceptance credits and hire purchase, instalment credit, factoring, invoice discounting or similar agreements but excluding trade debts and liabilities far the payment of tax. If you are a company or a limited liability partnership, Borrowing shall exclude all loans from your directors or, as the case may be, members.

CFADS (Cash Flow available for Debt Service) means your consolidated Profit Before Taxation and interest paid and payable after adding back depreciation, amortisation of goodwill and other non-cash profit and loss items, plus or minus net movements in working capital, less tax paid, dividends paid and payable or, as the case may be, drawings made available and capital expenditure paid (net of capital expenditure funded by asset disposals and/or hire purchase and/or finance leasing).

EBITDA means your consolidated Profit Before Taxation, depreciation, amortisation of goodwill and of other intangibles and interest paid and payable (but after dividends paid and payable or, as the case may be, after drawings made available).

Good Book Debts means those debts due to you in the normal course of business (over which a charge or security interest has been given to the Bank in a form acceptable to the Bank) but excluding (a) any debts arising from the sale of goods acquired which remain subject to reservation of title, (b) any debts more than 3 months old or considered by you or your auditors (if appropriate) to be irrecoverable, (c) any contract debtors, and (d) any contra or intra-group debts.

Net Worth shall mean at any particular time:

(a) if you are a company or a limited liability partnership the aggregate of the amount paid up on your issued share capital (if you have any) and the consolidated distributable and non-distributable reserves of you and your subsidiaries but (i) after deducting the total of any debit balance on profit and loss account and the book value of goodwill and any other intangible assets, and (ii) excluding any minority interests in subsidiaries and any increase in the valuation of assets subsequent to the date of the financial statement, or

(b) if you are not a company or a limited liability partnership, the net aggregate of all credit balances (after deducting any debit balances) of your Capital Accounts (or the accounts similarly styled in the financial statement which, for the avoidance of doubt, shall not include any loan moneys) less the book value of goodwill and any other intangible assets, excluding any increase in the valuation of assets subsequent to the date of the financial statement but, at the discretion of the Bank, increased to include the amount of (it any undrawn profits, and (ii) any taxation reserves

Profit After Taxation and Profit Before Taxation shall include items of an exceptional nature and shall exclude items of an extraordinary nature unless taken into account at the Bank’s discretion for the purpose of any relevant calculation.

Property means freehold and/or leasehold property (or, if in Scotland, heritable property owned or leased) over which a charge or security interest has been given to the Bank in a form acceptable to the Bank.

Rental Income means income derived from rents and service charges, excluding sums charged in respect of insurance premiums, any statutory charges and any intra-group rental income.

Retained Profit means your consolidated Profit After Taxation and dividends paid and payable (or, as the case may be, after drawings made available) and after deducting any profit attributable to minority interests in subsidiaries and after taking into account any items of an extraordinary nature and any items of an exceptional nature.

| Note: | If you do not have any subsidiaries, references in these Additional Terms and Conditions to “subsidiaries” and to “consolidated” shall be ignored and the relevant text shall be read and construed accordingly. |

This document creates legal obligations and therefore before signing we recommend that you consider getting independent advice. This may help you in understanding the potential consequences in the event that things go wrong.

| For Sole Trader/Partnership (other than Limited Liability Partnership) | ||||||||

| Signed by | ||||||||

| Print name | Print name | |||||||

| Signature | Signature | |||||||

| Date | Date | |||||||

| Print name | Print name | |||||||

| Signature | Signature | |||||||

| Date | Date | |||||||

| Print name | Print name | |||||||

| Signature | Signature | |||||||

| Date | Date | |||||||

| For Company / Limited Liability Partnership | ||||||||

| Signed for and on behalf of | ||||||||

| MOLECULAR PROFILES LTD | ||||||||

| by | and by | |||||||

| Print name | Print name | |||||||

| XXXXX XXXXX | XXXX GAINFORD | |||||||

| Signature | Signature | |||||||

| /s/ Xxxxx Xxxxx | /s/ Emma Gainford | |||||||

| Date 6 JANUARY 2012 | Date 6-1-12 | |||||||

| *Director/Member/Authorised Signatory | *Director/Member/Authorised Signatory/Secretary | |||||||

| Pursuant to a resolution of the board/members dated # | ||||||||

| Date | ||||||||

| Signed for and on behalf of the Bank by | ||||||||

| *Manager/Authorised Signatory | * Delete as appropriate. | |||||||

| /s/ Xxx Xxxxx | # This will be either the date of the account mandate, if an appropriate resolution is contained therein or the date of a specific resolution passed in respect of the loan. | |||||||

| Date 6-1-12 | ||||||||

Lloyds TSB Bank plc Registered Office 00 Xxxxxxx Xxxxxx, Xxxxxx XX0X 0XX Registered in England and Wales, no 2065

Lloyds TSB Scotland plc Registered Office Xxxxx Xxxxxx Xxxxx, 000 Xxxxxx Xxxxxx, Xxxxxxxxx XX0 0XX Registered in Xxxxxxxx, xx 00000

Authorised and regulated by the Financial Services Authority under numbers 119278 and 191240 respectively.

Licensed under the Consumer Credit Xxx 0000 under registration numbers 0004685 and 0198797 respectively

10412 0811

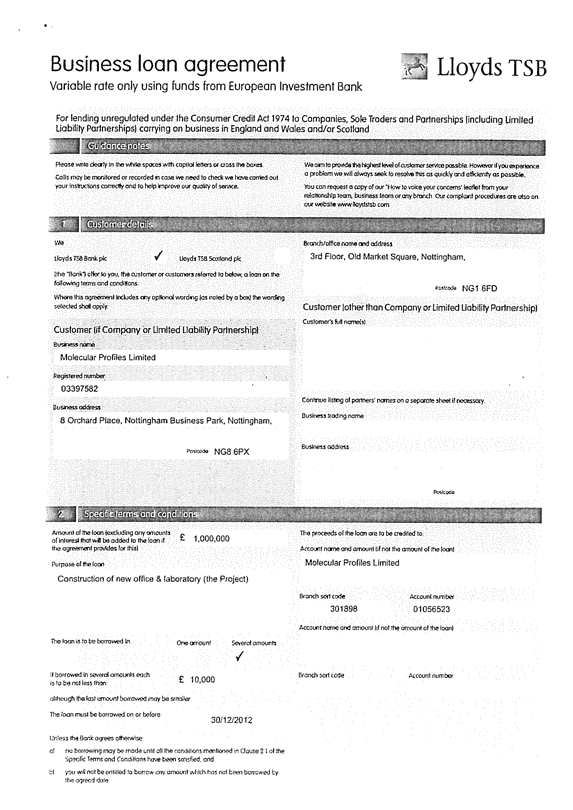

Business loan agreement Lloyds TSB

Variable rate

only using funds from European Investment Bank

For lending unregulated under the Consumer Credit Xxx 0000 to Companies, Sole Traders and Partnerships (including

Limited Liability Partnerships) carrying on business in England and Wales and/or Scotland

Guidance notes

Please write clearly in the while spaces with capitol letters or cross the boxes.

Calls may be

monitored or recorded in case we need to check we have carried out your instructors correctly and to help improve our quality of service.

We aim to provide the

highest level of customer service possible. However if you experience a problem we will always seek to resolve this as quickly and efficiency as possible.

You can

request a copy of our “How to voice your concerns” leaflet from your relationship team, business team or any branch. Our complaint procedures are also on our website xxx.xxxxxxxxx.xxx

1 Customer details

We

Lloyds TSB Bank plc x Lloyds TSB Scotland plc

(the “Bank”) offer to you, the customer or customers referred to below, a loan on the following terms and conditions.

Where this agreement includes any optional wording (as noted by a box) the wording selected shall apply.

Customer (other than Company or Limited Liability Partnership)

Business name

Molecular Profiles Limited

Registered number

03397582

Business address

0 Xxxxxxx Xxxxx, Xxxxxxxxxx Xxxxxxxx Xxxx, Xxxxxxxxxx,

Xxxxxxxx XX0 0XX

Branch/office name and address

0xx Xxxxx, Xxx Xxxxxx Xxxxxx, Xxxxxxxxxx,

Xxxxxxxx XX0 0XX

Customer (if Company or Limited Liability Partnership)

Customer’s full name(s)

Continue listing of partners’ names on a separate sheet if

necessary.

Business trading name

Business address

Postcode

2 Specific terms and conditions

Amount of the loan (excluding any amounts of interest that will be added to the loan if the agreement provides for this)

£1,000,000

Purpose of the loan

Construction of new office & laboratory (the Project)

The loan is to be borrowed in One

amount Several amounts

x

If

borrowed in several amounts each is to be not less than:

£10,000

although the lost amount borrowed may be smaller

The loan must be borrowed on

or before:

30/12/2012

Unless the Bank agrees otherwise:

a) no borrowing may be made until all the conditions mentioned in Clause 2.1 of the Specific Terms and Conditions have been satisfied, and

b) you will not be entitled to borrow any amount which has not been borrowed by the agreed date

The proceeds of the loan are to be credited to

Account name and amount (if

not the amount of the loan)

Molecular Profiles Limited

Branch sort code

Account number

301398 00000000

Account name and amount (if not the amount of

the loan)

Branch sort code Account number

2 Specific terms and conditions continued

2.1

Preconditions and security

Unless received by the Bank prior to the date on which this agreement is signed by the Bank, the Bank is to receive in form and

substance acceptable to the Bank the security (if any) listed in the Security Schedule and the documents, evidence or other requirements of the preconditions (if any) set out in the Preconditions Schedule.

Any security received should be accompanied by such evidence as the Bank may reasonably require to confirm the value of such security and to confirm that such security is fully

effective.

2.2 Fees and costs

You shall pay any costs and expenses incurred

by the Bank in assessing the loan. In the preparation of this agreement, in the preparation, valuation, taking or release of any guarantee of security at any time given in connection with this agreement and in connection with the revaluation of any

such security from time to time. The Bank will provide you with a written estimate of the amount of any such costs and expenses incurred by the Bank during the term of the loan before such costs are incurred.

The following charges shall be paid by you or demand by the Bank. These charges are to be paid even if the loan is not borrowed. If these charges include any estimated costs or

fees, such costs of fees are based on the facts known to the Bank of the date the Bank signed this agreement. The actual amount charged to you in respect of these initial costs and expenses may be more or less than the figure(s) quoted.

As mentioned in Clauses 2, 3 & 6 of the General Terms and Conditions and, if required by Section 26 of the Specific Terms and Conditions, other costs may arise in connection

with the loan.

Arrangement fee

£10,000

Security costs Estimated Actual

£ ¨ ¨

Valuation fee Estimated Actual

£ ¨ ¨

2.3 Interest

x Base Rate plus 1.95 % per annum

Base Rate is currently 0.50 % per annum

2.4 Payment of interest

Please

complete only one section. Interest shall be:

The first interest payment date will be:

x paid by you one month after draw down

After

that interest will be paid by you:

Monthly Quarterly

x ¨

The first date interest will be added to the loan is:

added to the loan.

After that interest will be added to the loan:

Monthly Quarterly

¨ paid by you until a

certain date and then added to the loan.

The first interest payment date will be: The first date interest will be added to the loan is:

After that interest will paid by you:

Monthly Quarterly

¨ ¨

After that interest will be added to the loan

Monthly Quarterly

¨ ¨

Interest will also be payable or as the case may be, added to the loan on the date of find repayment of the loan. Interest for any particular period is calculated on the number of

days in that period and a year of 365 days.

Interest is calculated on daily basis on the amount of the loan from time to time outstanding. The loan may include

interest, costs and charges added to the loan account in accordance with the terms of this agreement.

If you fail to pay any amount payable under this agreement

when due the rate of interest may be increased in accordance with Clause 6.3 of the General Terms and Conditions.

2 Specific terms and conditions

continued

2.5 Repayment

Please cross the appropriate box(es) to indicate how the loan

will be repaid. The loan is repayable in:

ü a single principal instalment on the payment date.

Repayment amount

£ 1,000,000

Repayment date

4 months after draw down

consecutive instalments in respect of principal only on the dates and in the amounts set out in the Repayment Schedule. Any amount owing on the final repayment date is to be paid

on that date.

Number of instalments

Find repayment date

consecutive instalments commencing on the first repayment date and ending on the final repayment date. Any amount owing on the final repayment date is to be paid on that date.

First repayment data

Monthly

¨

Quarterly ¨

Semi-annually ¨

Repayment type (e.g. principal

plus interest)

Repayment amount

Number of instalments

£

Final repayment date

consecutive instalments of principal and Interest commencing on the first repayment date and ending on the final repayment date. The amounts will vary with charges in interest and

the number of days in the changing period.

First repayment date

Monthly ¨

Quarterly ¨

Number of instalments

Find repayment date

consecutive instalments representing principal and interest. If the interest on the loan is at any time to be calculated with reference to Base Rate you should note that variations

in such rate after the date on which this agreement is signed by the Bank may affect either or both of the instalment amount and the term of the loan Please see Clause 2.3 of the General Terms and Conditions for further details. At the date on which

this agreement is signed by the Bank it is expected that final repayment of the loan will be made by the final repayment date.

First repayment date

Monthly ¨

Quarterly ¨

Repayment amount

£

Number of instalments

Find repayment date

is an early repayment charge payable?

2.6 Early repayment charges

Yes ¨

No

ü

(For loans with a term of 5 years or less from the date the loan is first borrowed)

On the date of each early repayment, you shall pay to the Bank an early repayment charge equal to 1% of the amount then being repaid.

(For loans with a term of over 5 years from the date the loan is first borrowed)

On the date

of each early repayment made on or before the date which is 5 years after the date the loan is first borrowed, you shall pay to the Bank an early repayment charge equal to 1% of the amount then being repaid.

2-7 Period of offer

This agreement shall come into effect only if the Bank receives from you

and finds in order a signed copy of this agreement on or before:

Date

03/02/2012

3 The Schedule

Preconditions Schedule

The Bank has received in form and substance acceptable to it a full appraisal of the Project, including a detailed cashflow of the projected cost. The appraisal is to be prepared

by a party acceptable to the Bank and is to show no issues of concern to the Bank.

The Bank has received your written instruction for the loan monies to be placed