The Transactions

Exhibit 99.1

The Transactions

On July 3, 2015, MediFAX-EDI, LLC (“MediFAX”), a Tennessee limited liability company and our wholly owned subsidiary, and Alto Merger Sub Inc., a Delaware corporation and wholly owned subsidiary of MediFAX (“Altegra Merger Sub”), entered into an Agreement and Plan of Merger (the “Altegra Merger Agreement”) by and among MediFAX, Altegra Merger Sub, Altegra Health, Inc., a Delaware corporation (“Altegra”) and Parthenon Investors III, L.P., a Delaware limited partnership, solely in its capacity as the Stockholders’ Representative, providing for the merger of Altegra Merger Sub with and into Altegra (the “Altegra Merger”) with Altegra surviving the Altegra Merger as a direct wholly owned subsidiary of MediFAX and indirect wholly owned subsidiary of Emdeon. The closing of the Altegra Merger is currently anticipated to occur in the third calendar quarter of 2015, subject to the satisfaction of various conditions, including the expiration or termination of the waiting period under the Xxxx-Xxxxx-Xxxxxx Antitrust Improvements Act of 1976, as amended (“HSR Act”).

Pursuant to the terms of the Altegra Merger Agreement, MediFAX is expected to pay approximately $910.0 million (the “Purchase Price”) in cash for Altegra at the closing of the Altegra Merger, which Purchase Price is subject to post-closing adjustments based on working capital, indebtedness and transaction expenses as of the closing date of the Altegra Merger.

At the effective time of the Altegra Merger, each issued and outstanding share of common stock of Altegra (the “Altegra Common Stock”) shall cease to exist and be converted into the right to receive, upon delivery of a duly-executed and completed letter of transmittal, the per share portion of the consideration in the Altegra Merger. Each issued and outstanding option for Altegra Common Stock shall be terminated and each option holder shall, upon delivery of a duly-executed option cancelation acknowledgement agreement, be entitled to receive the per share portion of the consideration in the Altegra Merger for each such option held less the exercise price per share underlying such option.

The Altegra Merger will be financed by borrowings from new term loans under our senior secured credit facilities in an aggregate amount of $395.0 million (the “2015 Incremental Term Loans”), the proceeds from the issuance of senior notes, the proceeds of an equity contribution from the Sponsors (the “Equity Contribution”) and available cash on hand (including proceeds of revolving loans under our senior secured credit facilities) (collectively, the “Acquisition Financing”).

In connection with the Altegra Merger, we have entered into a commitment letter with affiliates of the initial purchasers (the “Debt Commitment Parties”), pursuant to which the Debt Commitment Parties have committed to provide the Company with the Incremental Term Loans and alternative financing in form of senior unsecured loans under a bridge facility (the “Bridge Facility”) in the event this offering is not consummated or is not consummated in full. The Bridge Facility will only be drawn in the event we do not receive gross proceeds of at least $250.0 million from this offering prior to the consummation of the Altegra Merger.

The offering of the notes and the borrowings of the 2015 Incremental Term Loans, borrowing under our revolving credit facility, the Equity Contribution, the Altegra Merger and other related transactions are collectively referred to as the “Transactions.”

In the twelve months ended June 30, 2015, Altegra generated revenue and Pro Forma Adjusted EBITDA of $211.8 million and $59.0 million, respectively. After giving effect to the acquisition of Altegra, our pro forma revenue and Pro Forma Adjusted EBITDA for the twelve months ended June 30, 2015 would have been $1.6 billion and $463.2 million, respectively, and pro forma secured leverage and pro forma net total leverage would have been 4.0x and 6.0x, respectively.

1

Strategic Rationale

The strategic rationale for the Altegra Merger is the following:

Solutions and Services that Address Emerging Growth Markets. Altegra’s solutions address growing markets around government-sponsored health plans and emerging healthcare payment models. Altegra’s offerings support health plans in the Medicare Advantage market, as well as the Managed Medicaid and commercial exchange marketplace. The growth in these markets has been robust and is expected to expand to over 120 million covered lives by 2019, with additional populations entering the addressable market through the emergence of ACOs and other risk-bearing providers. The growth from covered lives is supplemented by increasing adoption of risk adjustment and quality metrics across healthcare payment models. As rising healthcare costs continue to fuel the shift towards value-based care, Xxxxxxx’s proprietary technology and intervention platforms provide the underlying infrastructure necessary to enable the transition to payment methods that are more closely aligned with the delivery of higher quality and more cost-effective care. We believe we can strengthen Altegra’s existing offerings by leveraging the enhanced and timely data that is available through our Intelligent Healthcare Network.

Sophisticated Data and Analytics Platform. Altegra has the ability to aggregate large volumes of data from disparate sources and analyze this data in a dynamic regulatory environment. Altegra’s integrated software and analytics platforms provide customers with differentiated risk adjustment and coding solutions that provide support as they navigate marketplace disruption, including the growth in exchange-based insurance markets and the transition to value-based healthcare.

Increased Revenue Mix to Software and Analytics. Altegra provides a sophisticated suite of integrated analytics offerings that are built on a cloud-based platform developed with algorithmic tools that assist health plans in the management and administration of its members. Over the past few years, we have enhanced our focus around our software and analytic capabilities, and Xxxxxxx’s solutions enhance this strategy. Pro forma for the Transactions, Emdeon would have increased its software and analytics revenue by 77%, shifting its software and analytics mix from 25% to 37% of solutions revenue, while reducing its network solutions mix from 34% to 28% of solutions revenue, for the twelve months ended June 30, 2015.

Improved Capabilities of Both Companies. Altegra’s analytic tools and solutions fit in well with our software and analytics offerings. By leveraging our technology and healthcare data expertise, the combination of Altegra’s risk adjustment and quality analytics and Emdeon’s Intelligent Healthcare Network, will enable the delivery of innovative products designed to help customers elevate care quality, optimize financial performance and improve the member and patient experience.

Improved Cross-Selling Opportunity. Altegra serves over 200 customers, including 21 of the 25 top Medicare Advantage plans and all of the top five Managed Medicaid plans. Although Emdeon regularly interacts with a similar set of customers, the increased breadth of solutions will allow us to deepen our relationship with these clients, while creating significant cross-sell opportunities for our existing solutions. As providers across the U.S. shift their attention to capitated reimbursement models, introduce their own health plans and generally become risk-taking organizations, we believe Xxxxxxx’s services will be instrumental to their success. Given Xxxxxx’s long standing relationship with these providers, the combined company will be well-positioned to serve this expanding market for healthcare data analytics. Our workflow embedded toolsets further facilitate this cross-sell opportunity, reducing implementation costs and minimizing time to launch.

2

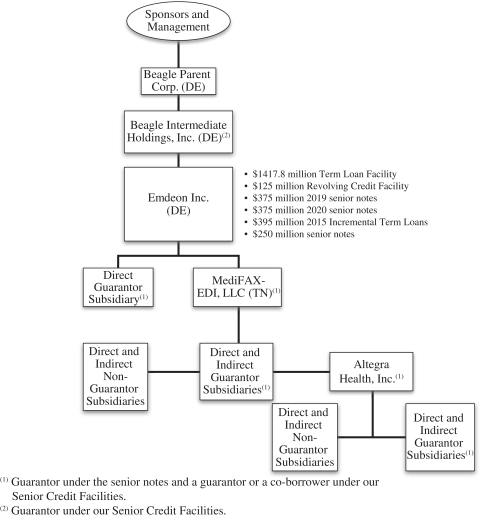

Our Corporate Structure

Following the consummation of the Altegra Merger, our corporate structure will be as follows:

3

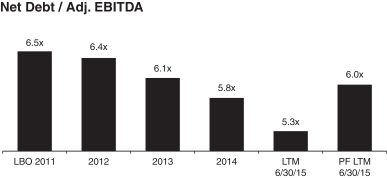

Certain Financial Ratios

| Unaudited | ||||

| Pro Forma Twelve Months Ended June 30, 2015 |

||||

| Credit Statistics: | ||||

| Ratio of net debt to Pro Forma Adjusted EBITDA |

6.0 | x | ||

| Ratio of secured net debt to Pro Forma Adjusted EBITDA(1) |

4.0 | x | ||

| Ratio of Pro Forma Adjusted EBITDA to cash interest expense |

2.6 | x | ||

| (1) | Revolving facility and original issue discount are excluded from this ratio. |

4

Risks Related to Our Business

We face significant competition for our solutions.

The markets for our various solutions are intensely competitive, continually evolving and, in some cases, subject to rapid technological change. We face competition from many healthcare information systems companies and other technology companies within segments of the healthcare information technology and services markets. We also compete with certain of our customers that provide internally some of the same solutions that we offer. Our key competitors include: (i) healthcare transaction processing companies, including those providing electronic data interchange (“EDI”), and/or internet-based services and those providing services through other means, such as paper and fax; (ii) healthcare information system vendors that support providers and payers and their revenue and payment cycle management and clinical information exchange processes, including physician and dental practice management, hospital information and electronic medical record system vendors; (iii) large information technology and healthcare consulting service providers; (iv) health insurance companies, pharmacy benefit management companies, hospital management companies and pharmacies that provide or are developing electronic transaction and payment distribution services for use by providers and/or by their members and customers; (v) healthcare payments and communication solutions providers, including financial institutions and payment processors that have invested in healthcare data management assets and print and mail vendors; (vi) government program eligibility and enrollment services companies; (vii) payment integrity companies; (viii) consumer engagement and transparency companies; and (ix) providers of healthcare risk adjustment, quality and other data and analytics solutions. In addition, major software, hardware, information systems and business process outsourcing companies, both with and without healthcare companies as their partners, offer or have announced their intention to offer products or services that are competitive with solutions that we offer.

Within certain of the markets in which we operate, we face competition from entities that are significantly larger and have greater financial resources than we do and have established reputations for success. Other companies have targeted these markets for growth, including by developing new technologies utilizing internet-based systems. We may not be able to compete successfully with these companies and these or other competitors may commercialize products, services or technologies that render our products, services or technologies obsolete or less marketable.

Some of our customers compete with us and some, instead of using a third-party provider, perform internally some of the same services that we offer.

Some of our existing customers compete with us or may plan to do so or belong to alliances that compete with us or plan to do so, either with respect to the same solutions we provide to them or with respect to some of our other lines of business. For example, some of our payer customers currently offer—through affiliated clearinghouses, web portals and other means—electronic data transmission services to providers that allow the provider to bypass third-party EDI service providers such as us, and additional payers may do so in the future. The ability of payers to replicate our solutions may adversely affect the terms and conditions we are able to negotiate in our agreements with them and our transaction volume with them, which directly relates to our

5

revenues. We may not be able to maintain our existing relationships for connectivity services with payers or develop new relationships on satisfactory terms, if at all. In addition, some of our solutions allow payers and providers to outsource business processes that they have been or could be performing internally and, in order for us to be able to compete, use of our solutions must be more efficient for them than use of internal resources.

If we are unable to retain our existing customers, our business, financial condition and results of operations could suffer.

Our success depends substantially upon the retention of our customers, particularly due to our recurring revenue model. We may not be able to retain some of our existing customers if we are unable to continue to provide solutions that our payer customers believe enable them to achieve improved efficiencies and cost-effectiveness, and that our provider and pharmacy customers believe allow them to more effectively manage their revenue cycle, increase reimbursement rates and improve cash flows. We also may not be able to retain customers if our electronic and/or paper-based solutions contain errors or otherwise fail to perform properly, if our pricing structure is no longer competitive or upon expiration of our contracts. Historically, we have enjoyed high customer retention rates; however, we may not be able to maintain high retention rates in the future. Our recurring revenues depend in part upon maintaining this high customer retention rate, and if we are unable to maintain our historically high customer retention rate, our business, financial condition and results of operations could be adversely impacted.

If we are unable to connect to a large number of payers and providers, our solutions would be limited and less desirable to our customers.

Our business largely depends upon our ability to connect electronically to a substantial number of payers, such as insurance companies, Medicare and Medicaid agencies and pharmacy benefit managers, and providers, such as hospitals, physicians, dentists, laboratories and pharmacies. The attractiveness of some of the solutions we offer to providers, such as our claims management and submission services, depends in part on our ability to connect to a large number of payers, which allows us to streamline and simplify workflows for providers. These connections may be made either directly or through a clearinghouse. We may not be able to maintain our links with a large number of payers on terms satisfactory to us and we may not be able to develop new connections, either directly or through other clearinghouses, on satisfactory terms. The failure to maintain these connections could cause our solutions to be less attractive to our provider customers. In addition, our payer customers view our connections to a large number of providers as essential in allowing them to receive a high volume of transactions and realize the resulting cost efficiencies through the use of our solutions. Our failure to maintain existing connections with payers, providers and other clearinghouses or to develop new connections as circumstances warrant, or an increase in the utilization of direct links between payers and providers, could cause our electronic transaction processing systems to be less desirable to healthcare constituents, which would reduce the number of transactions that we process and for which we are paid, resulting in a decrease in revenues and an adverse effect on our financial condition and results of operations.

The failure to maintain our relationships with our channel partners or significant changes in the terms of the agreements we have with them may have an adverse effect on our ability to successfully market our solutions.

We have entered into contracts with our channel partners to market and sell some of our solutions. Most of these contracts are on a non-exclusive basis. However, under contracts with some of our channel partners, we may be bound by provisions that restrict our ability to market and sell our solutions to potential customers. Our arrangements with some of these channel partners involve negotiated payments to them based on percentages of revenues they generate. If the payments prove to be too high, we may be unable to realize acceptable margins, but if the payments prove to be too low, the channel partners may not be motivated to produce a sufficient volume of revenues. The success of these contractual arrangements will depend in part upon the channel partners’ own competitive, marketing and strategic considerations, including the relative advantages of using alternative products being developed and marketed by them or our competitors. If any of these channel partners

6

are unsuccessful in marketing our solutions or seek to amend the financial or other terms of the contracts we have with them, we will need to broaden our marketing efforts to increase focus on the solutions they sell and alter our distribution strategy, which may divert our planned efforts and resources from other projects. In addition, as part of the packages these channel partners sell, they may offer a choice to their customers between solutions that we supply and similar solutions offered by our competitors or by the channel partners directly. If our solutions are not chosen for inclusion in these packages, the revenues we earn from our channel partner relationships will decrease. Lastly, we could be subject to claims and liability, as a result of the activities, products or services of these channel partners or other resellers of our solutions. Even if these claims do not result in liability to us, investigating and defending these claims could be expensive, time-consuming and result in adverse publicity that could harm our business.

Our business and future success may depend on our ability to cross-sell our solutions.

Our ability to generate revenue and growth partly depends on our ability to cross-sell our solutions to our existing customers and new customers. We expect our ability to successfully cross-sell our solutions will be one of the most significant factors influencing our growth. We may not be successful in cross-selling our solutions because our customers may find our additional solutions unnecessary or unattractive. Our failure to sell additional solutions to existing customers could affect our ability to grow our business.

We have faced and will continue to face pressure to reduce our prices, which may reduce our margins, profitability and competitive position.

As electronic transaction processing further penetrates the healthcare market or becomes highly standardized, competition among electronic transaction processors is increasingly focused on pricing. This competition has placed, and could place further pressure on us to reduce our prices in order to retain market share. If we are unable to reduce our costs sufficiently to offset declines in our prices, or if we are unable to introduce new innovative offerings with higher margins, our results of operations could decline.

In addition, many healthcare industry constituents are consolidating to create integrated healthcare delivery systems with greater market power. As provider networks, such as hospitals, and payer organizations, such as private insurance companies, consolidate, competition to provide the types of solutions we provide may become more intense and the importance of establishing and maintaining relationships with key healthcare industry constituents could become more significant. These healthcare industry constituents have, in the past, and may, in the future, try to use their market power to negotiate price reductions for our solutions. If we are forced to reduce prices, our margins will decrease and our results of operations will decline, unless we are able to achieve corresponding reductions in expenses.

Our ability to generate revenue could suffer if we do not continue to update and improve our existing solutions and develop new ones.

We must improve the functionality of our existing solutions in a timely manner and introduce new and valuable healthcare information technology and service solutions in order to respond to technological and regulatory developments and, thereby, retain existing customers and attract new ones. For example, from time to time, government agencies may alter format and data code requirements applicable to electronic transactions. In addition, our customers sometimes request that our solutions be customized to satisfy particular security protocols, modifications and other contractual terms in excess of industry norms and our standard configurations. These customer imposed requirements may impact the profitability of particular solutions and customer engagements. We may not be successful in responding to technological and regulatory developments or changing customer needs. The pace of change in the markets we serve is rapid, and there are frequent new product and service introductions by our competitors and channel partners who use our solutions in their offerings. If we do not respond successfully to technological and regulatory changes, as well as evolving industry standards and customer demands, our solutions may become obsolete. Technological changes also may result in the offering of

7

competitive solutions at lower prices than we are charging for our solutions, which could result in our losing sales unless we lower the prices we charge. If we do lower our prices on some of our solutions, we will need to increase our margins on these solutions in order to maintain our overall profitability. In addition, the solutions we develop or license may not be able to compete with the alternatives available to our customers.

Our business will suffer if we fail to successfully integrate acquired businesses and technologies or to appropriately assess the risks in particular transactions.

We have historically acquired and, in the future, plan to acquire, businesses, technologies, services, product lines and other assets. The successful integration of any businesses and assets we acquire into our operations, on a cost-effective basis, can be critical to our future performance. The amount and timing of the expected benefits of any acquisition, including potential synergies, are subject to significant risks and uncertainties. These risks and uncertainties include, but are not limited to, those relating to:

| • | our ability to maintain relationships with the customers of the acquired business; |

| • | our ability to cross-sell solutions to customers with which we have established relationships and those with which the acquired businesses have established relationships; |

| • | our ability to retain or replace key personnel of the acquired business; |

| • | potential conflicts in payer, provider, pharmacy, vendor or marketing relationships; |

| • | our ability to coordinate organizations that are geographically diverse and may have different business cultures; and |

| • | compliance with regulatory and other requirements. |

We cannot guarantee that any acquired businesses will be successfully integrated with our operations in a timely or cost-effective manner, or at all. Failure to successfully integrate acquired businesses or to achieve anticipated operating synergies, revenue enhancements or cost savings could have an adverse effect on our business, financial condition and results of operations.

Although our management attempts to evaluate the risks inherent in each transaction and to evaluate acquisition candidates appropriately, we may not properly ascertain all such risks and the acquired businesses and assets may not perform as we expect or enhance the value of our company as a whole. Acquired companies or businesses also may have larger than expected liabilities that are not covered by the indemnification, if any, that we are able to obtain from the sellers. Furthermore, the historical financial statements of the companies we have acquired or may acquire in the future are prepared by management of such companies and are not independently verified by our management. In addition, any pro forma financial statements prepared by us to give effect to such acquisitions may not accurately reflect the results of operations of such companies that would have been achieved had the acquisition of such entities been completed at the beginning of the applicable periods. Finally, there are no assurances that we will continue to acquire businesses at valuations consistent with our prior acquisitions or that we will complete acquisitions at all.

More risks related to the acquisition and integration of Altegra are set forth below in the “Risks Related to the Acquisition and Integration of Altegra” risk factor.

Achieving market acceptance of new or updated solutions is necessary in order for them to become profitable and will likely require significant efforts and expenditures.

Our future financial results will depend in part on whether our new or updated solutions receive sufficient customer acceptance. These solutions include, without limitation:

| • | electronic billing, payment and remittance services for payers, providers and patients that complement our existing payment and communication services; |

8

| • | electronic prescriptions from healthcare providers to pharmacies and pharmacy benefit managers; |

| • | our other pre- and post-adjudication services for payers and providers; |

| • | payment integrity and fraud, waste and abuse services for payers and providers; |

| • | government program eligibility and enrollment services for providers; |

| • | accounts receivable management, denial management, appeals and collection improvement services for providers; |

| • | healthcare and information technology consulting services for payers; |

| • | decision support, clinical information exchange or other business intelligence and data analytics solutions; |

| • | consumer engagement and transparency services; and |

| • | healthcare risk adjustment and quality solutions. |

Achieving market acceptance for new or updated solutions is likely to require substantial marketing efforts and expenditure of significant funds to create awareness and demand by constituents in the healthcare industry. In addition, deployment of new or updated solutions may require the use of additional resources for training our existing sales force and customer service personnel and for hiring and training additional salespersons and customer service personnel. Failure to achieve broad penetration in target markets with respect to new or updated solutions could have an adverse effect on our business prospects and financial results.

An economic downturn or volatility could have a material adverse effect on our business, financial condition and results of operations.

The United States economy has experienced significant economic uncertainty and volatility during recent years. A weakening of economic conditions could lead to reductions in demand for our solutions. For example, our revenues can be adversely affected by the impact of lower healthcare utilization trends driven by high unemployment and other economic factors. Further, weakened economic conditions or a recession could reduce the amount of income patients are able to spend on healthcare services. As a result, patients may elect to delay or forgo seeking healthcare services, which could further reduce healthcare utilization and our transaction volumes or decrease payer and provider demand for our solutions. Also, high unemployment rates could cause commercial payer membership to decline which also could lessen healthcare utilization and decrease our transaction volumes. In addition, as a result of volatile or uncertain economic conditions, we may experience the negative effects of increased financial pressures on our payer and provider customers. For instance, our business, financial condition and results of operations could be negatively impacted by increased competitive pricing pressure and a decline in our customers’ credit worthiness, which could result in us incurring increased bad debt expense. If we are not able to timely and appropriately adapt to changes resulting from a weak economic environment, our business, results of operations and financial condition may be materially and adversely affected.

There are increased risks of performance problems during times when we are making significant changes to our solutions or to systems we use to provide services. In addition, implementation of our solutions and cost savings initiatives may cost more, may not provide the benefits expected, may take longer than anticipated or may increase the risk of performance problems.

In order to respond to technological and regulatory changes and evolving industry standards, our solutions must be continually updated and enhanced. The software and systems that we use to provide services are inherently complex and, despite testing and quality control, we cannot be certain that errors will not be found in any changes, enhancements, updates and new versions that we market or use. Even if new or modified solutions do not have performance problems, our technical and customer service personnel may have difficulties in installing them or in providing any necessary training and support to customers.

9

Implementation of changes in our technology and systems may cost more or take longer than originally expected and may require more testing than initially anticipated. While new hardware and software will be tested before it is used in production, we cannot be sure that the testing will uncover all problems that may occur in actual use. If significant problems occur as a result of these changes, we may fail to meet our contractual obligations to customers, which could result in claims being made against us or in the loss of customer relationships. In addition, changes in our technology and systems may not provide the additional functionality or other benefits that were expected.

In addition, we also periodically implement efficiency measures and other cost saving initiatives to improve our operating performance. These efficiency measures and other cost saving initiatives may not provide the benefits anticipated or do so in the time frame expected. Implementation of these measures also may increase the risk of performance problems due to unforeseen impacts on our organization, systems and processes.

Disruptions in service or damages to our data or other operation centers, or other software or systems failures, could adversely affect our business.

Our data and operation centers are essential to our business. Our operations depend on our ability to maintain and protect our computer systems, many of which are located in our primary data centers that we operate in Memphis and Nashville, Tennessee. We have consolidated several satellite data centers and plan to continue such consolidation. Our business and results of operations are also highly dependent on our payment and communication operations, which are primarily conducted in Bridgeton, Missouri and Toledo, Ohio. We conduct business continuity planning and maintain insurance against fires, floods, other natural disasters and general business interruptions to mitigate the adverse effects of a disruption, relocation or change in operating environment; however, the situations we plan for and the amount of insurance coverage may not be adequate in any particular case. The occurrence of any of these events could result in interruptions, delays or cessations in service to users of our solutions, which could impair or prohibit our ability to provide our solutions, reduce the attractiveness of our solutions to our customers and adversely impact our financial condition and results of operations.

We also rely on a limited number of suppliers and contractors to provide us with a variety of solutions, including telecommunications and data processing services necessary for our transaction services and processing functions and software developers for the development and maintenance of certain software products we use to provide our solutions. If these suppliers do not fulfill their contractual obligations or choose to discontinue their products or services, our business and operations could be disrupted, our brand and reputation could be harmed and our financial condition and operating results could be adversely affected.

If the security measures protecting our information technology systems are breached or fail, we could be subject to liability, and customers may curtail or stop using our solutions.

Our business relies to a significant degree upon the secure electronic transmission, use and storage of sensitive information, including personal health information, financial information and other confidential data. Despite the implementation of security measures, our infrastructure, data centers and systems that we interface with, including the internet and related systems and our vendors, may be vulnerable to physical break-ins, hackers, improper employee or contractor access, computer viruses, programming errors, denial-of-service attacks, terrorist attacks or other attacks by third parties or similar disruptive problems. We cannot predict whether our security measures will be adequate to prevent all possible security threats. Any of these events, including the unauthorized access, misappropriation, disclosure or loss of sensitive information, including financial or personal health information, or a significant disruption of our network, could adversely affect our ability to provide our solutions and fulfill contractual demands, could require us to devote significant financial and other resources to mitigate such problems and could increase our future security costs, including through organizational changes, deploying additional personnel and protection technologies, further training of employees and engaging third party experts and consultants. Moreover, unauthorized access, use or disclosure of certain confidential information in our possession could result in civil or criminal liability or regulatory action,

10

including potential fines and penalties, as well as costs relating to required notifications, credit monitoring services and other necessary expenses. In addition, any actual or perceived breach of our security measures may deter customers from using or purchasing our solutions in the future. The occurrence of any of these events could disrupt our business and operations or harm our brand and reputation, either of which could adversely affect our financial condition and operating results.

Recently, there have been a number of high profile security breaches involving the improper dissemination of personal information of individuals both within and outside of the healthcare industry. Lawsuits resulting from these security breaches have sought significant monetary damages. While we maintain liability insurance coverage, claims could exceed the amount of our applicable insurance coverage, if any, or this coverage may not continue to be available on acceptable terms or in sufficient amounts.

We may be liable to our customers and may lose customers if we provide poor service, if our solutions do not comply with our agreements or if our software solutions or transmission systems contain errors or experience failures.

We must meet our customers’ service level expectations and our contractual obligations with respect to our solutions. Failure to do so could subject us to liability, as well as cause us to lose customers. In some cases, we rely upon third-party contractors to assist us in providing our solutions. Our ability to meet our contractual obligations and customer expectations may be impacted by the performance of our third-party contractors and their ability to comply with applicable laws and regulations. For example, our electronic payment and remittance solutions depend in part on the ability of our vendors to comply with applicable banking, financial service and payment card industry requirements and their failure to do so could cause an interruption in the solutions we provide or require us to seek alternative solutions or relationships.

Errors in the software and systems we use to provide services to customers also could cause serious problems for our customers. In addition, because of the large amount of data we collect and manage, it is possible that hardware failures and errors in our systems would result in data loss or corruption or cause the information that we collect to be incomplete or contain inaccuracies that our customers could regard as significant. For example, errors in our transaction processing systems can result in payers paying the wrong amount, making payments to the wrong payee or delaying payments. Since some of our solutions relate to laboratory ordering and reporting and electronic prescriptions, an error in our systems also could result in injury to a patient. If problems like these occur, our customers may seek compensation from us or may seek to terminate their agreements with us, withhold payments due to us, seek refunds from us of part or all of the fees charged under our agreements, request a loan or advancement of funds or initiate litigation or other dispute resolution procedures. In addition, we may be subject to claims against us by others affected by any such problems.

Our activities and the activities of our third party contractors involve the storage, use and transmission of financial and personal health information. Accordingly, security breaches of our or their computer systems or at our print and mail operation centers could expose us to a risk of loss or litigation, government enforcement actions and contractual liabilities. We cannot be certain that contractual provisions attempting to limit our liability in these areas will be successful or enforceable, or that other parties will accept such contractual provisions as part of our agreements. Any security breaches also could impact our ability to provide our solutions, as well as impact the confidence of our customers in our solutions, either of which could have an adverse effect on our business, financial condition and results of operations.

We attempt to limit, by contract, our liability for damages arising from our negligence, errors, mistakes or security breaches. However, contractual limitations on liability may not be enforceable or may otherwise not provide sufficient protection to us from liability for damages. We maintain liability insurance coverage, including coverage for errors and omissions. It is possible, however, that claims could exceed the amount of our applicable insurance coverage, if any, or that this coverage may not continue to be available on acceptable terms or in sufficient amounts. Even if these claims do not result in liability to us, investigating and defending against them

11

could be expensive and time consuming and could divert management’s attention away from our operations. In addition, negative publicity caused by these events may negatively impact market acceptance of our solutions, including unrelated solutions, or may harm our reputation and our business.

Recent and future developments in the healthcare industry could adversely affect our business.

Almost all of our revenue is either derived from the healthcare industry or could be affected by changes in healthcare spending. The healthcare industry is highly regulated and subject to changing political, legislative, regulatory and other influences. For example, the Patient Protection and Affordable Care Act, as amended by the Health Care and Education Reconciliation Act of 2010 (“ACA”) changes how healthcare services are covered, delivered and reimbursed through expanded coverage of uninsured individuals, reduced Medicare program spending and insurance market reforms. ACA seeks to increase health insurance coverage through the expansion of Medicaid, establishment of health insurance exchanges to facilitate the purchase of health insurance by individuals and small employers, imposing penalties on individuals who do not obtain health insurance and imposing fines on employers with 50 or more full-time employees that do not offer employees health insurance. ACA insurance market reforms include increased dependent coverage, prohibitions on excluding individuals based on pre-existing conditions and mandated minimum medical loss ratios for health plans. In addition, ACA provides for significant new taxes, including an industry user tax paid by health insurance companies, as well as an excise tax on health insurers and employers offering high cost health coverage plans. ACA also imposes significant Medicare Advantage funding cuts and material reductions to Medicare and Medicaid program spending. ACA further provides for additional resources to combat healthcare fraud, waste and abuse and also requires HHS to adopt additional standards for electronic transactions and to establish operating rules to promote uniformity in the implementation of each standardized electronic transaction.

While many of the provisions of ACA are not directly applicable to us, ACA affects the business of our payer, provider and pharmacy customers and the Medicaid programs of the states with which we have contracts. The provisions of ACA that are designed to expand health coverage potentially could result in an overall increase in transactions for our business and demand for our solutions; however, our customers may attempt to reduce spending to offset the increased costs associated with meeting the various ACA insurance market reforms. Likewise, as the Medicare payment reductions and other reimbursement changes impact our customers, our customers may attempt to seek price concessions from us or reduce their use of our solutions. Thus, ACA may result in a reduction of expenditures by customers or potential customers in the healthcare industry, which could have an adverse effect on our business, financial condition and results of operations. Further, we may experience increased costs from responding to new standardized transaction and implementation rules and our customers’ needs. In addition, implementation of the employer mandate was delayed for most employers until January 1, 2015 and will not be implemented for all employers until January 1, 2016. States may opt out of the Medicaid expansion, and the number of states that will ultimately participate and under what terms is not clear. The full impact of ACA, including its impact on our government eligibility and enrollment services offerings, is difficult to predict due to uncertainty regarding how many states will ultimately implement the Medicaid expansion, as well as the law’s complexity, lack of implementing regulations for all of the law’s provisions or limited interpretive guidance, remaining or new court challenges, implementation issues and the possibility of further delays, amendments or repeal.

Moreover, there are currently numerous federal, state and private initiatives and studies seeking ways to increase the use of information technology in healthcare as a means of improving care and reducing costs. For example, the American Recovery and Reinvestment Act of 2009 (“ARRA”) included federal subsidies that began in 2011 for eligible hospitals and eligible professionals that adopt and meaningfully use certified electronic health record (“EHR”) technology, and through December 2014 approximately $28 billion in payments have been distributed. These initiatives may result in additional or costly legal or regulatory requirements that are applicable to us and our customers, may encourage more companies to enter our markets, may provide advantages to our competitors and may result in the development of technology solutions that compete with ours. Any such initiatives also may result in a reduction of expenditures by customers or potential customers in the healthcare industry, which could have an adverse effect on our business.

12

In addition, other general reductions in expenditures by healthcare industry constituents could result from, among other things:

| • | government regulation or private initiatives that affect the manner in which providers interact with patients, payers or other healthcare industry constituents, including changes in pricing or means of delivery of healthcare solutions; |

| • | reductions in governmental funding for healthcare, in addition to reductions required by ACA, such as reductions resulting from the Budget Control Act of 2011, which requires automatic spending reductions of $1.2 trillion for federal fiscal years 2013 through 2021, minus any deficit reductions enacted by Congress and debt service costs, and laws that extend these cuts through 2024; and |

| • | adverse changes in business or economic conditions affecting payers, providers, pharmaceutical companies, medical device manufacturers or other healthcare industry constituents. |

Even if general expenditures by healthcare industry constituents remain the same or increase, other developments in the healthcare industry may result in reduced spending on information technology and services or in some or all of the specific markets we serve or are planning to serve. In addition, our customers’ expectations regarding pending or potential healthcare industry developments also may affect their budgeting processes and spending plans with respect to the types of solutions we provide. For example, use of our solutions could be affected by:

| • | changes in the billing patterns of providers; |

| • | changes in the design of health insurance plans; |

| • | changes in the contracting methods payers use in their relationships with providers; |

| • | decreases in marketing expenditures by pharmaceutical companies or medical device manufacturers, as a result of governmental regulation or private initiatives that discourage or prohibit promotional activities by pharmaceutical or medical device companies; and |

| • | successful implementation of government programs that streamline and standardize eligibility enrollment processes could result in decreased pricing or demand for our eligibility and enrollment solutions. |

The healthcare industry has changed significantly in recent years, and we expect that significant changes will continue to occur. The timing and impact of developments in the healthcare industry are difficult to predict. Furthermore, we are unable to predict how providers, payers, pharmacies and other healthcare market participants will respond to the various reform provisions contained in ACA, some of which are not yet fully implemented and could be further delayed, repealed or blocked. We cannot be sure that the markets for our solutions will continue to exist at current levels or that we will have adequate technical, financial and marketing resources to react to changes in those markets.

Government regulation, industry standards and other requirements creates risks and challenges with respect to our compliance efforts and our business strategies.

The healthcare industry is highly regulated and subject to frequently changing regulatory and other requirements. Many healthcare laws and regulations are complex, and their application to specific services and relationships may not be clear. Because our customers are required to comply with these requirements, we may be impacted as a result of our contractual obligations even when we are not directly subject to them. For many of these requirements, there is little history of regulatory or judicial interpretation upon which to rely. In particular, many existing healthcare laws and regulations, when enacted, did not anticipate the healthcare information solutions that we provide, and these laws and regulations may be applied to our solutions in ways that we do not anticipate. ACA and other federal and state efforts to reform or revise aspects of the healthcare industry or to revise or create additional statutory and regulatory requirements could impact our operations, the use of our solutions and our ability to market new solutions, or could create unexpected liabilities for us. We also may be

13

impacted by non-healthcare laws, industry standards and other requirements as a result of some of our solutions. For example, laws, regulations and industry standards regulating the banking and financial services industry may impact our operations as a result of the electronic payment and remittance services we offer directly or through third-party vendors. We are unable to predict what changes to laws, regulations and other requirements might be made in the future or how those changes could affect our business or the costs of compliance.

We have attempted to structure our operations to comply with legal and other requirements applicable to us directly and to our customers and third-party contractors, but there can be no assurance that our operations will not be challenged or impacted by enforcement initiatives. Any determination by a court or agency that our solutions violate, or cause our customers to violate, applicable laws, regulations or other requirements could subject us or our customers to civil or criminal penalties. Such a determination also could require us to change or terminate portions of our business, disqualify us from serving customers who are or do business with government entities or cause us to refund some or all of our service fees or otherwise compensate our customers. In addition, failure to satisfy laws, regulations or other requirements could adversely affect demand for our solutions and could force us to expend significant capital, research and development and other resources to address the failure. Even an unsuccessful challenge by regulatory and other authorities or private whistleblowers could be expensive and time consuming, could result in loss of business, exposure to adverse publicity and injury to our reputation and could adversely affect our ability to retain and attract customers. Laws, regulations and other requirements impacting our operations include the following:

| • | HIPAA Privacy and Security Requirements. There are numerous federal and state laws and regulations related to the privacy and security of personal health information. In particular, regulations promulgated pursuant to the Health Insurance Portability and Accountability Act of 1996 (“HIPAA”) establish privacy and security standards that limit the use and disclosure of individually identifiable health information (known as “protected health information”) and require the implementation of administrative, physical and technological safeguards to protect the privacy of protected health information and ensure the confidentiality, integrity and availability of electronic protected health information. We are directly subject to certain provisions of the regulations as a “Business Associate” through our relationships with customers. We are also directly subject to the HIPAA privacy and security regulations as a “Covered Entity” with respect to our operations as a healthcare clearinghouse and, if the Altegra Merger is completed, with respect to Altegra’s clinical care visit services. |

The privacy regulations established under HIPAA also provide patients with rights related to understanding and controlling how their health information is used and disclosed. To the extent permitted by applicable privacy regulations and our contracts with our customers, we may use and disclose protected health information to perform our services and for other limited purposes, such as creating de-identified information, but other uses and disclosures, such as marketing communications, require written authorization from the individual or must meet an exception specified under the privacy regulations. Determining whether data has been sufficiently de-identified to comply with the HIPAA privacy standards and our contractual obligations may require complex factual and statistical analyses and may be subject to interpretation.

If we are unable to properly protect the privacy and security of protected health information entrusted to us, we could be found to have breached our contracts with our customers. Further, if we fail to comply with applicable HIPAA privacy and security standards, we could face civil and criminal penalties. HHS is required to perform compliance audits and has announced its intent to perform audits in 2015. In addition to enforcement by HHS, state attorneys general are authorized to bring civil actions seeking either injunctions or damages in response to violations that threaten the privacy of state residents. HHS has the discretion to impose penalties without being required to attempt to resolve violations through informal means, such as implementing a corrective action plan. Although we have implemented and maintain policies and processes to assist us in complying with these regulations and our contractual obligations, we cannot provide assurance regarding how these standards will be interpreted, enforced or applied to our operations.

14

| • | Other Privacy and Security Requirements. In addition to HIPAA, numerous other state and federal laws govern the collection, dissemination, use, access to and confidentiality of personal health information and healthcare provider information. Some states also are considering new laws and regulations that further protect the confidentiality, privacy and security of personal records or other types of medical information. In many cases, these state laws are not preempted by the HIPAA privacy standards and may be subject to interpretation by various courts and other governmental authorities. Further, the United States Congress and a number of states have considered prohibitions or limitations on the disclosure of medical or other information to individuals or entities located outside of the United States. |

| • | Data Protection and Breaches. In recent years, there have been a number of well-publicized data breaches involving the improper dissemination of personal information of individuals both within and outside of the healthcare industry. Many states have responded to these incidents by enacting laws requiring holders of personal information to maintain safeguards and take certain actions in response to a data breach, such as providing prompt notification of the breach to affected individuals. In many cases, these laws are limited to electronic data, but states are increasingly enacting or considering stricter and broader requirements. Under HIPAA, Covered Entities must report breaches of unsecured protected health information to affected individuals without unreasonable delay but not to exceed 60 days following discovery of the breach by a Covered Entity or its agents. Notification also must be made to HHS and, in certain circumstances involving large breaches, to the media. Business Associates must report breaches of unsecured protected health information to Covered Entities within 60 days of discovery of the breach by the Business Associate or its agents. A non-permitted use or disclosure is presumed to be a breach unless the Covered Entity or Business Associate establishes that there is a low probability the protected health information has been compromised. This presumption and the standard for determining whether a non-permitted use or disclosure constitutes a breach will likely result in a greater number of incidents involving the non-permitted use and disclosure of unsecured protected health information being classified as breaches and, thus, a greater number of required notifications |

In addition, the Federal Trade Commission (“FTC”) has prosecuted certain data breach cases as unfair and deceptive acts or practices under the Federal Trade Commission Act. Further, by regulation, the FTC requires creditors, which may include some of our customers, to implement identity theft prevention programs to detect, prevent and mitigate identity theft in connection with customer accounts. Although Congress passed legislation that restricts the definition of “creditor” and exempts many healthcare providers from complying with this rule, we may be required to apply additional resources to our existing process to assist our affected customers in complying with this rule.

We have implemented and maintain physical, technical and administrative safeguards intended to protect all personal data and have processes in place to assist us in complying with all applicable laws and regulations regarding the protection of this data and properly responding to any security breaches or incidents; however, we cannot be sure that these safeguards are adequate to protect all personal data or assist us in complying with all applicable laws and regulations regarding the protection of personal data and responding to any security breaches or incidents.

| • | HIPAA Transaction and Identifier Standards. HIPAA and its implementing regulations mandate format and data content standards and provider identifier standards (known as the National Provider Identifier) that must be used in certain electronic transactions, such as claims, payment advice and eligibility inquiries. As required by ACA, HHS has established standards that health plans must use for electronic fund transfers with providers, has established operating rules for certain transactions and is in the process of establishing operating rules to promote uniformity in the implementation of the remaining types of covered transactions. ACA also requires HHS to establish standards for health claims attachment transactions. Further, HHS adopted updated standard code sets for diagnoses and procedures known as the ICD-10 code sets. The use of the ICD-10 code sets is required by October 1, 2015. |

15

HHS has established a unique health plan identifier for health plans and that Covered Entities must use to identify health plans in standardized transactions beginning on November 7, 2016. HHS also has established an “other entity identifier” that entities involved in healthcare transactions that are not health plans, providers or individuals may opt to obtain and use.

Although our systems are capable of transmitting transactions that comply with requirements currently in effect, we will be required to modify our systems to accommodate new requirements. We have been modifying and will continue to modify our systems and processes to prepare for and implement changes to the transaction standards, code sets operating rules and identifier requirements; however, we may not be successful in responding to these changes and any responsive changes we make to our systems and software may result in errors or otherwise negatively impact our service levels. In addition, the compliance dates for ICD-10 code sets, new or modified transaction standards, operating rules and identifiers may overlap, which may further burden our resources.

We also may experience complications related to supporting customers that are not fully compliant with the revised requirements as of the applicable compliance or enforcement date. Some payers and healthcare clearinghouses with which we conduct business interpret HIPAA transaction requirements differently than we do or may require us to use legacy formats or include legacy identifiers as they transition to full compliance. For example, we continue to process transactions using legacy identifiers for non-Medicare claims that are sent to us to the extent that the intended recipients have not instructed us to suppress those legacy identifiers. Where payers or healthcare clearinghouses require conformity with their interpretations or require us to accommodate legacy transactions or identifiers as a condition of successful transactions, we seek to comply with their requirements, but may be subject to enforcement actions as a result. We continue to work with payers, providers, practice management system vendors and other healthcare industry constituents to implement the transaction standards and identifier standards. We cannot provide assurance regarding how the Centers for Medicare and Medicaid Services (“CMS”) will enforce the transaction and identifier standards or how CMS will view our practice of accommodating requests to process transactions that include legacy formats or identifiers for non-Medicare claims. Any regulatory change, clarification or enforcement action by CMS that prohibited the processing by healthcare clearinghouses or private payers of transactions containing legacy formats or identifiers could have an adverse effect on our business.

| • | Electronic Health Records. Medicare and Medicaid incentive payments are available for eligible hospitals and eligible professionals that adopt and meaningfully use EHR technology. Beginning in 2015, eligible hospitals and eligible professionals who fail to attest to the meaningful use of EHR technology will face reductions in Medicare payments. These incentives and the risk of reduced Medicare payments promote the adoption of EHR technology which may impact our business. |

| • | Anti-Kickback and Anti-Bribery Laws. A number of federal and state laws govern patient referrals, financial relationships with physicians and other referral sources and inducements to providers and patients, including restrictions contained in amendments to the Social Security Act, commonly known as the “federal Anti-Kickback Law.” The federal Anti-Kickback Law prohibits any person or entity from offering, paying, soliciting or receiving, directly or indirectly, anything of value with the intent of generating referrals of patients covered by Medicare, Medicaid or other federal healthcare programs. Violation of the federal Anti-Kickback Law is a felony. The Anti-Kickback Law contains a limited number of exceptions, and the Office of the Inspector General of HHS has created regulatory safe harbors to the federal Anti-Kickback Law. Activities that comply precisely with a safe harbor are deemed protected from prosecution under the federal Anti-Kickback Law. Failure to meet a safe harbor does not automatically render an arrangement illegal under the Anti-Kickback Law. The arrangement, however, does risk increased scrutiny by government enforcement authorities, based on its particular facts and circumstances. Our contracts and other arrangements may not meet an exception or a safe harbor. |

Many states also have similar anti-kickback laws that are not necessarily limited to items or services for which payment is made by a federal healthcare program. The laws in this area are both broad and vague and generally are not subject to frequent regulatory or judicial interpretation. We review our practices with regulatory experts in an effort to comply with all applicable laws and regulatory requirements.

16

However, we are unable to predict how these laws will be interpreted or the full extent of their application, particularly to services that are not directly reimbursed by federal healthcare programs, such as transaction processing services. Any determination by a state or federal regulatory agency that any of our activities or those of our customers or vendors violate any of these laws could subject us to civil or criminal penalties, could require us to change or terminate some portions of our business, could require us to refund a portion of our service fees, could disqualify us from providing services to customers who are or do business with government programs and could have an adverse effect on our business. Even an unsuccessful challenge by regulatory authorities of our activities could result in adverse publicity and could require a costly response from us.

| • | False or Fraudulent Claim Laws. We provide claims processing and other solutions to providers that relate to, or directly involve, the reimbursement of health services covered by Medicare, Medicaid, other federal healthcare programs and private payers. In addition, as part of our data transmission and claims submission services, we may employ certain edits, using logic, mapping and defaults, when submitting claims to third-party payers. Such edits are utilized when the information received from providers is insufficient to complete individual data elements requested by payers. If the Altegra Merger is completed, we will also provide services including risk analytics services, chart reviews, in-home assessments, audit functions, and enrollment and eligibility services, to Medicaid and Medicare managed care plans, commercial plans and other entities. These services, which include identifying diagnosis codes with respect to hierarchical condition categories, impact the amounts paid by Medicare and Medicaid payments to managed care plans. |

As a result of these aspects of our business, we may be subject to, or contractually required to comply with, numerous federal and state laws that prohibit false or fraudulent claims. False or fraudulent claims include, but are not limited to, billing for services not rendered, making or causing to be made or used a false record or statement that is material to a false claim, failing to refund known overpayments, misrepresenting actual services rendered, improper coding and billing for medically unnecessary items or services. Some of these laws, including restrictions contained in amendments to the Social Security Act, commonly known as the federal Civil Monetary Penalty Law, require a lower burden of proof than other fraud, waste and abuse laws. Federal and state governments increasingly use the federal Civil Monetary Penalty Law, especially where they believe they cannot meet the higher burden of proof requirements under the various criminal healthcare fraud provisions.

In addition, the FCA and some state false claims laws provide significant civil and criminal penalties for noncompliance and can be enforced by private individuals through “whistleblower” or qui tam actions on behalf of the government alleging that the defendant has defrauded the government. For example, the federal Civil Monetary Penalty Law provides for penalties ranging from $10,000 to $50,000 per prohibited act and assessments of up to three times the amount claimed or received. Further, violations of the FCA are punishable by treble damages and penalties of up to $11,000 per false claim, and whistleblowers may receive a share of amounts recovered. Civil penalties also may be imposed for the failure to report and return an overpayment made by the federal government within 60 days of identifying the overpayment and also may result in liability under the FCA. ACA provides that submission of a claim for an item or service generated in violation of the Anti-Kickback Law constitutes a false or fraudulent claim under the FCA. Whistleblowers and the federal government have taken the position and some courts have held, that providers who allegedly have violated other statutes, such as the Xxxxx Law, have thereby submitted false claims under the FCA. We rely on our customers to provide us with accurate and complete information and, if the Altegra Merger is completed, to appropriately use analytics, codes, reports and other information in connection with the services Altegra provides.

From time to time, constituents in the healthcare industry, including us, may be subject to actions under the FCA or other fraud, waste and abuse provisions, such as the federal Civil Monetary Penalty Law. Errors and the unintended consequences of data manipulations by us or our systems with respect to entry, formatting, preparation or transmission of information may be determined or alleged to be in violation of these laws and regulations or could adversely impact the compliance of our customers. Although we

17

believe our editing processes are consistent with applicable reimbursement rules and industry practice, a court, enforcement agency or whistleblower could challenge these practices. In addition, we cannot guarantee that state and federal agencies will regard any billing errors we process as inadvertent or will not hold us responsible for any compliance issues related to claims we handle on behalf of providers and payers. We cannot predict the impact of any enforcement actions under the various false claims and fraud, waste and abuse laws applicable to our operations. Even an unsuccessful challenge of our practices could cause adverse publicity and cause us to incur significant legal and related costs.

| • | Financial Services Related Laws and Rules. Financial services and electronic payment processing services are subject to numerous laws, regulations and industry standards. These laws may subject us, our vendors and our customers to liability as a result of our payment and communication solutions. Although we do not act as a bank, we offer solutions that involve banks, or vendors who contract with banks and other regulated providers of financial services. The various payment modalities that we offer our customers directly and through third party providers may be deemed regulated activity at the federal or state level, and, as a result, we may be affected by banking and financial services industry laws, regulations and standards, such as licensing requirements, solvency standards, reporting and disclosure obligations and requirements to maintain the privacy and security of nonpublic personal financial information. In addition, our payment and communication solutions may be affected by payment card industry operating rules and security standards, certification requirements, state prompt payment laws and other rules governing electronic funds transfers. If we fail to comply with any applicable payment and communication rules or requirements, we may be subject to fines and changes in transaction fees and may lose our ability to process payment transactions or facilitate other types of billing and payment solutions. Moreover, in addition to regulatory requirements related to electronic funds transfers, payment transactions processed using the Automated Clearing House Network are subject to network operating rules promulgated by the National Automated Clearing House Association, and these rules may affect our billing and payment practices. Further, our payment and communication solutions may impact the ability of our payer customers to comply with state prompt payment laws. These laws require payers to pay healthcare claims meeting the statutory or regulatory definition of a “clean claim” within a specified time frame. |

| • | United States Postal Service Laws and Regulations. Our payment and communication solutions provide mailing services primarily delivered through the United States Postal Service (“USPS”). Although we generally pass these costs through to our customers, postage is the most significant cost incurred in the delivery of our payment and communication solutions. Postage rates are dependent on the operating efficiencies of the USPS and legislative and regulatory mandates imposed on the USPS as a result of various fiscal and political factors. Accordingly, new USPS laws or regulations, including changes in the interpretation of existing regulations, changes in the operations of USPS and recent or future rate increases, may negatively impact our business and results of operations. For example, if measures taken by the USPS to reduce its operating costs are not effective, additional postage rate increases or other operational changes may occur. We also rely on significant discounts from the basic USPS postage rate structure, which could be changed or discontinued at any time. While we cannot predict the timing or magnitude of such changes, the current economic and political environment is likely to lead to further rate increases and/or changes in the operations, policies and regulatory interpretations of the USPS. Because we may be unable to implement changes mandated by the USPS in our operations or pass future rate increases through to our customers, any failure or alleged failure to comply with applicable laws and regulations, or any adverse applications of, or changes in, the USPS laws and regulations affecting our business, could have a material adverse effect on our operating results and/or financial condition. |

| • | Other State Laws. Most states have a variety of laws that may potentially impact our operations and business practices. For instance, if the Altegra Merger is completed, many states in which we would provide clinical care in-home assessment services prohibit corporations and other non-licensed entities from practicing medicine by employing physicians and certain non-physician practitioners. These prohibitions on the corporate practice of medicine impact how we structure our relationships with |

18

| physicians and other affected non-physician practitioners. If our arrangements with physicians or other practitioners were found to violate a corporate practice of medicine prohibition, our contractual arrangements with practitioners in such states could be adversely affected, which, in turn, may adversely affect both our operations and profitability. Further, we could face sanctions for aiding and abetting the violation of the state’s professional licensure statutes. We will continually monitor legislative, regulatory and judicial developments related to licensure and engage arrangements with professionals; however, new agency interpretations, federal or state legislation or regulations, or judicial decisions could require us to change how we operate, may increase our costs of services and could have a material adverse effect on our results of operations. |

Legislative changes and contractual limitations may impede our ability to utilize our offshore service capabilities.

In our operations, we have contractors, and, if the Altegra Merger is completed, will have employees, located outside of the United States who may have access to personal health information in order to assist us in performing services for our customers. From time to time, the United States Congress considers legislation that would restrict the transmission of personal health information regarding a United States resident to any foreign affiliate, subcontractor or unaffiliated third party without adequate privacy protections or without providing notice to the identifiable individual of the transmission and an opportunity to opt out. Some of the proposals considered would have required patient consent and imposed liability on healthcare businesses arising from the improper sharing or other misuse of personal health information. Congress also has considered creating a private civil cause of action that would allow an injured party to recover damages sustained as a result of a violation of these proposed restrictions. Furthermore, a number of states have considered prohibitions or limitations on the disclosure of medical or other personal information to individuals or entities located outside of the United States. If legislation of this type is enacted, our ability to utilize offshore resources may be impeded, and we may be subject to sanctions for failure to comply with the new mandates of the legislation. In addition, the enactment of such legislation could result in such work being performed at a lower margin of profitability, or even at a loss. Further, as a result of concerns regarding the possible misuse of personal health information, some of our customers have contractually limited or may seek to limit our ability to use our offshore resources. Use of offshore resources may increase our risk of violating our contractual obligations to our customers to protect the privacy and security of personal health information provided to us, which could adversely impact our reputation and operating results.

Failure by our customers to obtain proper permissions or provide us with accurate and appropriate data may result in claims against us or may limit or prevent our use of data which could harm our business.

We require our customers to provide necessary notices and obtain necessary permissions for the use and disclosure of the information that we receive. If they do not provide necessary notices or obtain necessary permissions, then our use and disclosure of information that we receive from them or on their behalf may be limited or prohibited by state or federal privacy or other laws. Such failures by our customers could impair our functions, processes and databases that reflect, contain or are based upon such data. For example, as part of our claims submission services, we rely on our customers to provide us with accurate and appropriate data and directives for our actions. While we have implemented features and safeguards designed to maximize the accuracy and completeness of claims content, these features and safeguards may not be sufficient to prevent inaccurate claims data from being submitted to payers. In addition, such failures by our customers could interfere with or prevent creation or use of rules, analyses or other data-driven activities that benefit us or make our solutions less useful. Accordingly, we may be subject to claims or liability for inaccurate claims data submitted to payers or for use or disclosure of information by reason of lack of valid notice or permission. These claims or liabilities could damage our reputation, subject us to unexpected costs and adversely affect our financial condition and operating results.

19

Certain of our solutions present the potential for embezzlement, identity theft or other similar illegal behavior by our employees or contractors with respect to third parties.