DRAFT AGREEMENT ON THE MERGER OF MPI INTO ETABLISSEMENTS MAUREL & PROM BETWEEN ETABLISSEMENTS MAUREL & PROM S.A. SURVIVING ENTITY AND MPI S.A. MERGED ENTITY

Exhibit I

ENGLISH LANGUAGE TRANSLATION

FOR INFORMATION PURPOSES ONLY

DRAFT AGREEMENT ON THE MERGER OF MPI INTO

ETABLISSEMENTS MAUREL & PROM

BETWEEN

ETABLISSEMENTS XXXXXX & PROM S.A.

SURVIVING ENTITY

AND

MPI S.A.

MERGED ENTITY

2 NOVEMBER 2015

1

ENGLISH LANGUAGE TRANSLATION

FOR INFORMATION PURPOSES ONLY

This document is a free English translation of the draft agreement on the merger of MPI into MAUREL & PROM. This translation has been prepared solely for the information and convenience of the shareholders of MPI and MAUREL & PROM and other readers. No assurances are given as to the accuracy or completeness of this translation and MPI and XXXXXX & PROM assumes no responsibility with respect to this translation or any misstatement or omission that may be contained therein. In the event of any ambiguity or discrepancy between this translation and the original French version of the draft merger agreement, the French version shall prevail.

Important information

This document does not constitute and shall not be construed as an offer or the solicitation of an offer to purchase, sell or exchange any securities of MAUREL & PROM or MPI. In particular, it does not constitute an offer or the solicitation of an offer to purchase, sell or exchange of securities in any jurisdiction (including the US, the United Kingdom, Australia, Canada and Japan) in which it would be unlawful or subject to registration or qualification under the laws of such jurisdiction.

This business combination is made for the securities of a foreign company, and is subject to disclosure requirements of a foreign country that are different from those of the United States. Financial statements included in any of the documents made available to the public in the context of the business combination have been prepared in accordance with foreign accounting standards that may not be comparable to the financial statements of United States companies.

It may be difficult for you to enforce your rights and any claim you may have arising under the US federal securities laws, since the issuer is located in a foreign country, and some or all of its officers and directors may be residents of a foreign country. You may not be able to sue a foreign company or its officers or directors in a foreign court for violations of the U.S. securities laws. It may be difficult to compel a foreign company and its affiliates to subject themselves to a U.S. court’s judgment.

In connection with the proposed transaction, the required information documents will be filed with the Autorité des Marchés Financiers (“AMF”). Investors and shareholders are strongly advised to read, when available, the information documents that have been filed with the AMF because they will contain important information.

Shareholders and investors may obtain free copies of documents filed with the AMF at the AMF’s website at xxx.xxx-xxxxxx.xxx or directly from MAUREL & PROM’s website (xxx.xxxxxxxxxxxx.xx) or MPI’s website (xxx.xxxxxxxxx.xx).

2

ENGLISH LANGUAGE TRANSLATION

FOR INFORMATION PURPOSES ONLY

DRAFT MERGER AGREEMENT

BETWEEN THE UNDERSIGNED:

MPI S.A.,

A French société anonyme with a share capital of EUR 11,533,653.40, having its registered office at 00 xxx x’Xxxxx, 00000 Xxxxx, registered as a company in Paris under number 517 518 247 and represented by Xx Xxxxxx Xxxxxxx in his capacity as Managing Director (Directeur Général), duly authorised for the purposes hereof in a decision of the board of directors dated 15 October 2015;

hereinafter “MPI”.

FIRST PARTY,

AND:

ETABLISSEMENTS MAUREL & PROM S.A.,

A French société anonyme with a share capital of EUR 93,604,436.31, having its registered office at 00 xxx x’Xxxxx, 00000 Xxxxx, registered as a company in Paris under number 457 202 331 and represented by Xx Xxxxxx Xxxxxxx, in his capacity as Managing Director (Directeur Général), duly authorised for the purposes hereof in a decision of the board of directors dated 15 October 2015;

hereinafter “XXXXXX & PROM”.

SECOND PARTY,

MPI and MAUREL & PROM are hereinafter referred to collectively as the “Parties” and individually as a “Party”.

This draft merger agreement (the “Agreement”) has been agreed with a view to the merger of MPI into MAUREL & PROM (the “Merger”); the provisions set out below will govern the Merger.

* *

*

3

ENGLISH LANGUAGE TRANSLATION

FOR INFORMATION PURPOSES ONLY

TABLE OF CONTENTS

| 1. | CHARACTERISTICS OF THE COMPANIES | 6 | ||||

| 1.1 | Presentation of MAUREL & PROM | 6 | ||||

| 1.2 | Presentation of MPI | 7 | ||||

| 1.3 | Existing relations between the Parties | 8 | ||||

| 1.3.1 Share capital | 8 | |||||

| 1.3.2 Shared corporate officers | 8 | |||||

| 1.3.3 Tax regime | 8 | |||||

| 2. | MOTIVATIONS AND OBJECTIVES OF THE MERGER | 9 | ||||

| ARTICLE 1. | PLANNED MERGER OF MPI INTO MAUREL & PROM | 10 | ||||

| ARTICLE 2. | MERGER AUDITORS AND INDEPENDENT EXPERT | 10 | ||||

| ARTICLE 3. | CONDITIONS PRECEDENT AND FINAL COMPLETION OF THE MERGER | 10 | ||||

| 3.1 | Conditions precedent | 10 | ||||

| 3.2 | Merger Completion | 11 | ||||

| ARTICLE 4. | FINANCIAL STATEMENTS USED FOR ESTABLISHING TERMS OF THE TRANSACTION | 11 | ||||

| 4.1 | MPI financial statements | 11 | ||||

| 4.2 | XXXXXX & PROM financial statements | 11 | ||||

| ARTICLE 5. | DESCRIPTION AND EVALUATION OF ASSETS AND LIABILITIES TO BE TRANSFERRED | 12 | ||||

| 5.1 | Transferred assets | 12 | ||||

| 5.2 | Transferred liabilities | 13 | ||||

| 5.3 | Dividends distributed since 31 December 2014 and exceptional distribution | 14 | ||||

| 5.4 | Net assets transferred | 14 | ||||

| 5.5 | Off balance sheet commitments | 14 | ||||

| ARTICLE 6. | TRANSFER OF ASSETS AND LIABILITIES | 14 | ||||

| ARTICLE 7. | TRANSFERRED EMPLOYEES | 15 | ||||

| ARTICLE 8. | TRANSITION PERIOD | 15 | ||||

| 8.1 | Cooperation between the Parties | 15 | ||||

| 8.2 | Management of MPI and XXXXXX & PROM | 15 | ||||

| ARTICLE 9. | SHARE EXCHANGE RATIO | 15 | ||||

| ARTICLE 10. | REMUNERATION OF CONTRIBUTION AND MAUREL & PROM SHARE CAPITAL INCREASE | 16 | ||||

| 10.1 | Vesting rights and rights attached to the new shares | 16 | ||||

| 10.2 | Effect of the Merger on MPI Free Shares and MPI Free Preferred Shares | 17 | ||||

| 10.2.1 Effect of the Merger on MPI Free Shares | 17 | |||||

| 10.2.2 Effect of the Merger on MPI Free Preferred Shares | 17 | |||||

| 10.3 | Unallocated new shares representing fractional rights | 17 | ||||

| 10.4 | Unclaimed new shares | 17 | ||||

| ARTICLE 11. | MERGER PREMIUM | 17 | ||||

4

ENGLISH LANGUAGE TRANSLATION

FOR INFORMATION PURPOSES ONLY

| ARTICLE 12. | OWNERSHIP AND EFFECTIVE DATE OF THE MERGER FOR ACCOUNTING AND TAX PURPOSES | 18 | ||||

| ARTICLE 13. | CHARGES AND CONDITIONS | 18 | ||||

| 13.1 | General charges and conditions | 18 | ||||

| 13.2 | Charges and conditions pertaining to MAUREL & PROM | 19 | ||||

| 13.3 | Charges and conditions pertaining to MPI | 20 | ||||

| ARTICLE 14. | REPRESENTATIONS | 20 | ||||

| 14.1 | Representations of MAUREL & PROM | 20 | ||||

| 14.2 | Representations of MPI | 21 | ||||

| ARTICLE 15. | DISSOLUTION OF MPI | 21 | ||||

| ARTICLE 16. | TAX PROVISIONS | 21 | ||||

| 16.1 | General undertaking to file tax returns | 21 | ||||

| 16.2 | Retroactive effect | 22 | ||||

| 16.3 | Corporate income tax | 22 | ||||

| 16.4 | Value Added Tax (VAT) | 23 | ||||

| 16.5 | Registration tax | 24 | ||||

| 16.6 | Other taxes | 24 | ||||

| ARTICLE 17. | MISCELLANEOUS PROVISIONS | 24 | ||||

| 17.1 | Costs | 24 | ||||

| 17.2 | Delivery of documents | 24 | ||||

| 17.3 | Governing law and jurisdiction | 25 | ||||

| 17.4 | Notifications | 25 | ||||

| 17.5 | Validity | 25 | ||||

| 17.6 | Amendments and waivers | 25 | ||||

| 17.7 | Formalities | 25 | ||||

| 17.8 | Powers | 25 | ||||

5

ENGLISH LANGUAGE TRANSLATION

FOR INFORMATION PURPOSES ONLY

RECITALS

| 1. | CHARACTERISTICS OF THE COMPANIES |

| 1.1 | Presentation of MAUREL & PROM |

MAUREL & PROM is a French société anonyme incorporated on 1 November 1919 and initially created for a term of 99 years and 2 months. The company’s term was extended by 99 years from 13 October 2014 until 13 October 2113, unless extended again or liquidated in advance of its term.

The corporate purpose of MAUREL & PROM in France and abroad is as follows:

| • | the management of all shares and membership rights and, to this end, the acquisition of interests in any company, group or association, particularly by way of purchase, subscription and contribution, as well as the sale in any form of said shares or membership rights; |

| • | the prospecting and exploitation of all mineral deposits, particularly liquid or gaseous hydrocarbon deposits and related products; |

| • | the leasing, acquisition, transfer and sale of all xxxxx, land, deposits, concessions, operating permits and prospecting permits, either on its own account or on behalf of third parties, whether by participation or otherwise, and the transportation, storage, processing, transformation and trading of all natural or synthetic hydrocarbons, all liquid or gaseous products or by-products of the subsoil, and all minerals or metals; |

| • | the acquisition of any buildings and their management or sale; |

| • | trading in all products and commodities; and |

| • | generally, the direct or indirect participation in all commercial, industrial, real estate, agricultural and financial transactions, in France or other countries, either by the formation of new companies or by the contribution, subscription or purchase of shares or membership rights, merger, joint venture or otherwise, and generally all transactions of any kind whatsoever directly or indirectly related to these activities and likely to facilitate development or management. |

MAUREL & PROM’s registered office and identifying number on the companies register, and its share capital, are stated above at the beginning of the present document.

XXXXXX & PROM’s financial year begins each year on 1 January and ends on 31 December.

XXXXXX & PROM is governed by an 8-member board of directors: Xx Xxxx-Xxxxxxxx Xxxxx, chairman of the board, Xx Xxxxxxxx Xxxxxxxxx, Xx Xxxxxx Xxxxxxx d’Armaillé, Xx Xxxxxx Xxxxxxx, Xx Xxxxxxxx de Xxxxxx xx Xxxxxxxx, Xx Xxxxx Xxxxxx, Xx Xxxxxx Xxxxxxx, Xx Xxxxxxxx Xxxxxx Xxxxx xx Xxxxxxxx and Xx Xxxx Xxxxxxxx, and managed by Managing Director Xx Xxxxxx Xxxxxxx.

Auditing is handled by the firms KPMG S.A. and International Audit Company as incumbent Statutory Auditors, and by the firm Xxxxxxxx Xxxxxx and Ms Xxxxxxxx Xxxxxxxxxx as alternate Statutory Auditors.

6

ENGLISH LANGUAGE TRANSLATION

FOR INFORMATION PURPOSES ONLY

The share capital of MAUREL & PROM is EUR 93,604,436.31, divided into 121,564,203 fully paid up shares of the same category with a par value of EUR 0.77 each.

MAUREL & PROM has issued the following securities:

| • | Bonds redeemable into new shares and/or exchangeable into existing shares issued on 6 June 2014 and due 1 July 2019 (“ORNANE 2019”). On the date of the Agreement, a total of 14,658,169 shares could potentially be issued upon exercise of the attribution right of shares attached to the ORNANE 2019; |

| • | Bonds redeemable into new shares and/or exchangeable into existing shares issued on 12 May 2015 due 1 July 2021 (“ORNANE 2021”). On the date of the Agreement, a total of 10,435,571 shares could potentially be issued upon exercise of the attribution right of shares attached to the ORNANE 2021; |

| • | Share warrants granted on 19 May 2010 due 31 December 2015 (“MAUREL & PROM Warrants”). On the date of the Agreement, a total of 13,364,625 shares could potentially be issued upon exercise of MAUREL & PROM Warrants; |

| • | Free shares to be allocated on a definitive basis on 28 March 2016, for which the lock-up period expires on 28 March 2018 (the “MAUREL & PROM Free Shares”). On the date of the Agreement, a total of 56,840 shares could potentially be issued upon final allocation of MAUREL & PROM Free Shares. |

MAUREL & PROM had 31 employees as at 31 December 2014.

| 1.2 | Presentation of MPI |

MPI is a French société anonyme incorporated on 13 October 2009 for a term of 99 years, i.e. until 12 October 2108 unless extended again or liquidated in advance of its term.

The corporate purpose of MPI in France and abroad is as follows:

| • | the holding and management of all shares and membership rights and, to this end, the acquisition of interests in any company, group or association, particularly by way of purchase, subscription and contribution, as well as the sale in any form of the said shares or membership rights; |

| • | the prospecting and exploitation of all mineral deposits, particularly liquid or gaseous hydrocarbon deposits and related products; |

| • | the leasing, acquisition, transfer and sale of all xxxxx, land, deposits, concessions, operating permits and prospecting permits, either on its own account or on behalf of third parties, whether by participation or otherwise, and the transport, storage, processing, transformation and trading of all natural or synthetic hydrocarbons, all liquid or gaseous products or by-products of the subsoil, and all minerals or metals; |

| • | the acquisition, management or sale of any buildings; |

| • | the trading in any products and commodities; |

| • | the issuance of any guarantees, first demand guarantees, collateral and other sureties, particularly to the benefit of any group, undertaking or company in which it holds an interest, in the context of its activities, and the financing or refinancing of its activities; and |

| • | generally speaking, the Company’s direct or indirect participation in all commercial, industrial, real estate, agricultural and financial transactions, in France or other countries, either by the formation of new companies or by the contribution, subscription or purchase of shares or membership rights, merger, joint venture or otherwise, and generally all transactions of any kind whatsoever directly or indirectly related to these activities and likely to facilitate development or management. |

7

ENGLISH LANGUAGE TRANSLATION

FOR INFORMATION PURPOSES ONLY

MPI’s registered office and identifying number on the companies register, and its share capital, are stated above at the beginning of the present document.

MPI’s financial year begins each year on 1 January and ends on 31 December.

MPI is governed by a 9-member board of directors: Xx Xxxx-Xxxxxxxx Xxxxx, chairman of the board, Xx Xxxxxxxx Xxxxxxxxx, Xx Xxxxxxxx Xxxxxxx, Xx Xxxxxx Xxxxxxx, Xxxxxxxx de Xxxxxx xx Xxxxxxxx, Xx Xxxxxxxxx Xxxxxxxx, Xx Xxxxxxxxx Xxxxxxxx Xxxxx, Mr Ambroisie Xxxxxx Chukwueloka Xxxxxxx, and MACIF represented by Xx Xxxxxxx Xxxxx, and managed by Managing Director Xxxxxx Xxxxxxx, and Deputy Managing Director Xxxxxx Xxxxxxx.

Auditing is handled by the firms KPMG S.A. and International Audit Company as incumbent Statutory Auditors, and by the firm Xxxxxxxx Xxxxxx and Xx Xxxxxxxx Xxxxxxx as alternate Statutory Auditors.

Share capital of MPI is EUR 11,533,653.40, divided into 115,336,534 fully paid up shares of the same category with a par value of EUR 0.10 each.

MPI has issued the following securities:

| • | Free shares definitively allocated on 20 June 2015 for which the lock-up period expires on 20 June 2017 (the “MPI Free Shares”); |

| • | Free preferred shares convertible into ordinary shares to be definitively allocated on 22 May 2017, for which the lock-up period expires on 22 May 2019 and the conversion period on 22 May 2022 (the “MPI Free Preferred Shares”). On the date of the Agreement, a total of 75,000 shares could potentially be issued upon conversion of MPI Free Preferred Shares. |

MPI had 4 employees as at 31 December 2014.

| 1.3 | Existing relations between the Parties |

| 1.3.1 | Share capital |

As at the date hereof, MAUREL & PROM and MPI do not have any cross-holdings.

| 1.3.2 | Shared corporate officers |

Xx Xxxx-Xxxxxxxx Xxxxx is chairman of the board for MAUREL & PROM and for MPI.

Xx Xxxxxxxx Xxxxxxxxx, Xx Xxxxxxxx de Xxxxxx xx Xxxxxxxx and Xx Xxxxxx Xxxxxxx are directors on the boards of directors for MAUREL & PROM and for MPI.

Xx Xxxxxx Xxxxxxx is MAUREL & PROM Managing Director and MPI Deputy Managing Director.

| 1.3.3 | Tax regime |

MAUREL & PROM and MPI are both subject to the rules for corporation tax.

8

ENGLISH LANGUAGE TRANSLATION

FOR INFORMATION PURPOSES ONLY

| 2. | MOTIVATIONS AND OBJECTIVES OF THE MERGER |

XXXXXX & PROM and MPI must currently face a difficult macroeconomic environment following the sudden drop in the price of oil, the lack of visibility related to their size, which limits their access to the best conditions that the financial markets have to offer and restricts their capacity for external growth in a capital-intensive industry.

Their merger is part and parcel of the consolidation trend within the sector affecting independent oil and gas exploration and production companies across the market. It would give the combined entity greater financial capacity through:

The merger is a strategic step in consolidation of the sector to which all independent oil exploration and production companies face. It would enable the combined entity to benefit from a reinforced financial capacity resulting from:

| • | a combination of significant cash flows from production in Gabon and Tanzania and dividends from Seplat in Nigeria; |

| • | better access to financial markets; and |

| • | substantial cost synergies and tax savings which, for example, would have represented EUR 14.5 million for the 2014 financial year on a pro forma basis, of which EUR 12 million in tax savings and EUR 2.5 million in operating expenses corresponding to listing, structural and management costs of MPI. |

The merger would also enable the combined entity to benefit from an attractive combination of already developed onshore assets, offering a favourable oil (variable price)/gas (fixed price) product mix and greater geographic diversification combining (i) onshore operated assets generating substantial oil production with long-term visibility (including through Ezanga permit in Gabon held at 80%) (ii) operated assets that began producing gas on 20 August 2015 offering exposure to East African countries (Tanzania), (iii) a significant stake (21.76%) in Seplat, one of the leading indigenous operators in Nigeria with strong potential for growth, (iv) significant upside development and potential value increase in Canada and (v) exploration zones in Colombia, Myanmar and Namibia.

The consolidated entity would offer investors an attractive investment vehicle in terms of liquidity and market capitalisation with an optimized balance sheet and sustainable funding, ranking it among the top-tier independent European oil exploration/production companies.

In light of the above, XXXXXX & PROM and MPI have decided to proceed with the Merger.

* *

*

9

ENGLISH LANGUAGE TRANSLATION

FOR INFORMATION PURPOSES ONLY

NOW THEREFORE, the Parties have drawn up this Agreement.

ARTICLE 1. PLANNED MERGER OF MPI INTO MAUREL & PROM

Subject to satisfaction of the Conditions Precedent (as defined below) and in keeping with the conditions set out herein, MPI hereby transfers all its assets and liabilities together with all the standard legal and de facto guarantees in such matters in accordance with the conditions provided in articles L.236-1 et seq. and R.236-1 et seq. of the French Commercial Code (Code de commerce) to MAUREL & PROM, which accepts this transfer. It is understood that:

| • | as the Parties have decided to give the Merger retroactive effect for accounting and tax purposes, the effective date of the Merger for accounting and tax purposes will be the first day of the then current MPI financial year on the Final Completion Date (hereinafter the “Effective Date”) in accordance with article L.236-4 of the French Commercial Code; |

| • | All MPI assets and liabilities will be transferred to MAUREL & PROM such as they exist on the Final Completion Date (as this term is defined below); |

| • | the Merger will entail the transfer of all MPI assets and liabilities, including any items not expressly referred to herein (the list set out in Article 5 is non-exhaustive), with no exceptions or reservations; |

| • | XXXXXX & PROM will become the debtor of MPI creditors in lieu and stead of MPI, but without such substitution involving any novation with regards to said creditors. |

| ARTICLE 2. | MERGER AUDITORS AND INDEPENDENT EXPERT |

In accordance with articles L.236-10 and R.236-6 of the French Commercial Code, Xx Xxxxxxx Xxxxxxxx and Xx Xxxxxxx Xxxxxxxx were appointed as Merger Auditors in an order issued by the presiding judge of the Paris Commercial Court on 1 September 2015. Their mission is to (i) examine the terms of the merger and specifically, to verify that the relative values attributed to XXXXXX & PROM and MPI shares are appropriate and the exchange ratio is equitable and (ii) assess the value of the contributions in kind to be made as part of the merger between MAUREL & PROM and MPI.

The firm Associés en Finance, represented by Xx Xxxxxx Xxxxxxxxxx, was appointed by the MPI board of directors as independent expert on 27 August 2015 at the recommendation of its ad hoc committee. The independent expert submitted a report to the board dated 15 October 2015, which included an opinion on the fairness of the planned exchange ratio.

| ARTICLE 3. | CONDITIONS PRECEDENT AND FINAL COMPLETION OF THE MERGER |

| 3.1 | Conditions precedent |

The Merger and resulting dissolution of MPI are subject to the satisfaction of the following conditions precedent stipulated for the benefit of each party:

| • | confirmation by the French market authority, the Autorité des marchés financiers (“AMF”), that the Merger will not result in an obligation for Xxxxxxxx X.X. to launch a public bid shares of MAUREL & PROM and MPI pursuant to article 236-6 of the General Regulations of the AMF; |

| • | approval of the Exceptional Distribution (such as defined in ARTICLE 5.3 of the Agreement) at the MPI extraordinary general meeting of the shareholders; |

| • | approval of the Merger, this Agreement, and the resulting dissolution of MPI at the MPI extraordinary general meeting of the shareholders; |

| • | approval of the Merger, this Agreement, and the resulting MAUREL & PROM issue of new shares as consideration for the merger of MPI into MAUREL & PROM at the MAUREL & PROM extraordinary general meeting of the shareholders; |

(the “Conditions Precedent”).

10

ENGLISH LANGUAGE TRANSLATION

FOR INFORMATION PURPOSES ONLY

| 3.2 | Merger Completion |

The Merger and resulting dissolution of MPI will be fully completed at 11.59 pm on the fourth trading day following the approval of the Merger by the shareholders of MAUREL & PROM and of MPI if the last Condition Precedent has been satisfied within the above-mentioned timeframe or, if the last Condition Precedent has not been satisfied within the above-mentioned timeframe, at 11.59 pm on the date the last Condition Precedent is satisfied (the “Final Completion Date”).

Satisfaction of the Conditions Precedent will be considered to be adequately demonstrated vis-à-vis any party on presentation of a certified extract of the minutes to the MPI and MAUREL & PROM board of directors’ meetings recording the satisfaction of the Conditions Precedent.

If the Conditions Precedent have not been satisfied by 29 February 2016 (inclusive), the Agreement will deemed null and void and no compensation will be owed by either Party to the other.

Completion of the Merger will be recorded in the compliance statement (déclaration de régularité et de conformité) signed by the Parties in accordance with articles L.236-6 and R.236-4 of the French Commercial Code.

| ARTICLE 4. | FINANCIAL STATEMENTS USED FOR ESTABLISHING TERMS OF THE TRANSACTION |

| 4.1 | MPI financial statements |

The terms and conditions of the Agreement have been established by reference to MPI’s consolidated annual financial statements and individual financial statements as at 31 December 2014, using the same methods and presentation as for the previous annual balance sheet (“Transaction Financial Statements”). The Transaction Financial Statements are appended hereto in Schedule 4.1.

The MPI consolidated financial statements as at 31 December 2014 and as at 30 June 2015 and the individual financial statements as at 31 December 2014 will be made available to the shareholders in accordance with article R.236-3 of the French Commercial Code.

| 4.2 | XXXXXX & PROM financial statements |

The terms and conditions of the Agreement have been established by reference to MAUREL & PROM’s consolidated annual financial statements and individual financial statements as at 31 December 2014, using the same methods and presentation as for the previous annual balance sheet. These financial statements are appended hereto in Schedule 4.2.

The MAUREL & PROM consolidated financial statements as at 31 December 2014 and as at 30 June 2015 and the individual financial statements as at 31 December 2014 will be made available to the shareholders in accordance with article R.236-3 of the French Commercial Code.

11

ENGLISH LANGUAGE TRANSLATION

FOR INFORMATION PURPOSES ONLY

It is understood, however, that the reference to the MPI assets and liabilities covered in the Transaction Financial Statements for the purpose establishing the Merger terms and conditions will not affect the actual content of such assets and liabilities, which will be transferred to MAUREL & PROM such as they exist on the Final Completion Date.

| ARTICLE 5. | DESCRIPTION AND EVALUATION OF ASSETS AND LIABILITIES TO BE TRANSFERRED |

MPI will transfer all its assets, rights, obligations, and all other assets or liabilities to MAUREL & PROM.

Pursuant to the applicable accounting regulations, valuation of the assets transferred by MPI is determined on a on an actual value basis. The actual value of the assets transferred from MPI to MAUREL & PROM was determined using the multi-criteria method described in Schedule 5.

The list of assets and liabilities, rights, securities, and obligations set out below is non-exhaustive and for information only; all MPI assets and liabilities are to be transferred in full to MAUREL & PROM such as they exist on the Final Completion Date. It is understood that all additional information that may prove necessary to make a precise, complete, or special description, inter alia for the purpose of completing legal registration formalities and enacting the transfer that ensues from the Merger, may be provided in inventories, tables, agreements, and statements that may be collected together in one or more documents supplementing or rectifying the present document, and will be drawn up with input from both Parties.

The assets and liabilities to be transferred (as these appear in the Transaction Financial Statements) are as follows:

| 5.1 | Transferred assets |

MPI assets which are to be transferred to MAUREL & PROM include the goods, rights and values listed below (without limitation):

| In thousands of EUR | Gross | Depreciation | Individual MPI NAV as at 31/12/2014 |

Re-valuation and adjustment |

Actual value |

|||||||||||||||

| Seplat |

21 317 | 0 | 21 317 | 118 863 | 140 180 | |||||||||||||||

| Saint-Xxxxx Energie |

14 232 | 0 | 14 232 | 14 232 | ||||||||||||||||

| Cardinal |

6 060 | 4 448 | 1 612 | (1 612 | ) | 0 | ||||||||||||||

| MPNATI |

83 | 83 | 83 | |||||||||||||||||

| Financial assets |

41 692 | 4 448 | 37 245 | 117 251 | 154 496 | |||||||||||||||

| Inventory and outstanding receivables |

0 | 0 | 0 | 0 | ||||||||||||||||

| Receivables |

50 | 0 | 50 | 50 | ||||||||||||||||

| Loans to Seplat |

3 | 0 | 3 | 3 | ||||||||||||||||

| Loans to MPNATI |

314 | 0 | 314 | 314 | ||||||||||||||||

| Loans to Saint-Xxxxx Energie |

44 396 | 0 | 44 396 | (6 315 | ) | 38 081 | ||||||||||||||

| Incoming dividends |

5 950 | 0 | 5 950 | 5 950 | ||||||||||||||||

| Other receivables |

6 | 0 | 6 | 6 | ||||||||||||||||

| Own shares |

10 627 | 143 | 10 485 | (10 485 | ) | 0 | ||||||||||||||

| Cash and cash equivalents |

251 003 | 0 | 251 003 | 251 003 | ||||||||||||||||

| Prepaid expenses |

22 | 0 | 22 | 22 | ||||||||||||||||

| Unrealised foreign exchange losses |

1 968 | 0 | 1 968 | (1 968 | ) | 0 | ||||||||||||||

| Current assets |

314 340 | 143 | 314 197 | (18 767 | ) | 295 430 | ||||||||||||||

| Total assets transferred |

356 032 | 4 591 | 351 442 | 98 484 | 449 926 | |||||||||||||||

12

ENGLISH LANGUAGE TRANSLATION

FOR INFORMATION PURPOSES ONLY

The main assets being transferred are Seplat securities, Saint-Xxxxx Energie securities and loans to Saint-Xxxxx Energie and cash/cash equivalents.

The actual value of MPI’s stake in Seplat has been determined at EUR 140 million. This is based on the average share price at 1 month, 2 months, 3 months and 4 months before 8 October 2015 (date on which the figures have been calculated for the boards of directors of MAUREL & PROM and MPI dated 15 October 2015 which approved the Agreement), i.e., EUR 1.16 per Seplat share (or GBP 0.8440 based on the average EUR/GBP exchange rate of 0.725 over the same period).

The determination of the actual value of MPI’s stake in Saint-Xxxxx Energie is based on MPI’s share (two-thirds) in past costs, in keeping with the oil sector practice when valuing assets for farm-out agreements.

The actual value of MPI assets to be transferred to MAUREL & PROM therefore totals: EUR 449,926,032.

It is understood that the transferred assets include all property and rights that MPI owns as at the Final Completion Date.

| 5.2 | Transferred liabilities |

MPI liabilities, all of which XXXXXX & PROM will assume as debtor on the Final Completion Date, include the debts listed below (without limitation):

| In thousands of EUR | Book value as at 31/12/2014 |

Adjustment | Actual value | |||||||||

| Provisions for foreign exchange losses |

(1 968 | ) | 1 968 | 0 | ||||||||

| Provisions for IFC |

(106 | ) | (106 | ) | ||||||||

| Provisions |

(2 073 | ) | 1 968 | (106 | ) | |||||||

| Debts for the Cardinal stake |

(1 612 | ) | 1 612 | 0 | ||||||||

| Trade notes |

(937 | ) | (937 | ) | ||||||||

| Tax and social security liabilities |

(11 411 | ) | (11 411 | ) | ||||||||

| Other payables |

(666 | ) | (666 | ) | ||||||||

| Unrealised foreign exchange gains (on loans to Saint-Xxxxx Energie) |

(4 535 | ) | 4 535 | 0 | ||||||||

| Debts |

(19 160 | ) | 6 146 | (13 014 | ) | |||||||

| Total liabilities transferred |

(21 234 | ) | 8 114 | (13 119 | ) | |||||||

The actual value of all MPI debts to be transferred to MAUREL & PROM therefore totals: EUR 13,119,425.

It is understood that any additional liabilities arising with MPI during the interval between the end of the reporting period for the Transaction Financial Statements (the “Reporting Date”) and the Final Completion Date, and generally any liability that is related to the MPI business and neither known nor foreseeable on the date hereof and appears at a later date will be assumed by XXXXXX & PROM.

13

ENGLISH LANGUAGE TRANSLATION

FOR INFORMATION PURPOSES ONLY

| 5.3 | Dividends distributed since 31 December 2014 and exceptional distribution |

On 22 May 2015, the shareholders of MPI held a combined (ordinary and extraordinary) general meeting, at which they decided, at the proposal of the board of directors, to distribute dividends of EUR 0.30 per MPI share with dividend rights (excluding treasury shares), namely a total distributed amount of EUR 33,260,222.10.

In addition, the MPI general meeting of shareholders convened to approve the Merger and resulting dissolution of MPI is also to take a decision on an exceptional distribution of EUR 0.45 per share with dividend rights (the “Exceptional Distribution”) (see below Schedule 9) for a total amount of approximately EUR 49,797,000.

| 5.4 | Net assets transferred |

The total net assets transferred from MPI to MAUREL & PROM according to the above descriptions and valuations is EUR 353,749,589 determined as follows:

| Calculation of net assets transferred | In thousands of EUR |

|||

| Transferred assets |

449 926 | |||

| Assumed liabilities |

(13 119 | ) | ||

| Deduction for the 2015 distribution of dividends out of 2014 reserves by MPI |

(33 260 | ) | ||

| Deduction for the MPI Exceptional Distribution |

(49 797 | ) | ||

| Total net assets transferred |

353 750 | |||

The representative of MAUREL & PROM, in his official capacity, therefore expressly discharges MPI from submitting a more detailed description and hereby declares that he has reviewed the detail of the transferred net assets prior to the date hereof at the MPI registered office.

| 5.5 | Off balance sheet commitments |

MAUREL & PROM will be the beneficiary of commitments made to MPI and will replace MPI in bearing responsibility for the commitments it has made.

Aside from the first demand guarantee presented below, no significant off balance sheet commitments have been either made by or given to MPI and will be assumed by XXXXXX & PROM.

Regarding the oil exploration programme project on Anticosti in Quebec, MPI has given MAUREL & PROM a first demand guarantee for a maximum amount of EUR 33,333,333 representing two thirds of the maximum amount that could be owed by XXXXXX & PROM pursuant to the guarantee agreement.

| ARTICLE 6. | TRANSFER OF ASSETS AND LIABILITIES |

XXXXXX & PROM will pay the debts to third parties that are recorded as MPI liabilities, whether these debts are already in existence on the Reporting Date and have not yet been paid as at the Final Completion Date, or are contracted thereafter in the interval between the Reporting Date and the Final Completion Date, including all costs and expenses generated by the dissolution of MPI.

However it is understood that the provisions of the Agreement once final cannot in any way be deemed to qualify as acceleration of payment or acknowledgment of debt to a creditor; each creditor being required to establish and document its rights.

14

ENGLISH LANGUAGE TRANSLATION

FOR INFORMATION PURPOSES ONLY

| ARTICLE 7. | TRANSFERRED EMPLOYEES |

Pursuant to article L.1224-1 of the French Employment Code, XXXXXX & PROM will take on all current employment contracts with MPI that are in effect as at the Final Completion Date, together with all related undertakings and obligations and all MPI obligations vis-à-vis said employees.

The list of MPI employees transferred to MAUREL & PROM is set out in Schedule 7.

| ARTICLE 8. | TRANSITION PERIOD |

| 8.1 | Cooperation between the Parties |

Beginning with the signature hereof and until the Final Completion Date, the Parties hereby undertake:

| • | to cooperate in good faith and make their best effort so the Merger is completed at the earliest opportunity, and in particular, to take all necessary steps to ensure the Conditions Precedent are satisfied as soon as possible from the date of the Agreement. The Parties undertake to keep each other informed of all steps taken and the progress towards satisfying the Conditions Precedent, and to ensure the other Party is able to make its own observations and comments on said progress; |

In light of the bank finance agreements, XXXXXX & PROM undertakes to obtain the banks’ agreement to the Merger, in keeping with the procedures set out in said financing agreements, before the Final Completion Date;

| • | to make their best efforts and fully cooperate with the AMF in order to prepare, file and register the information document on the Merger that will be made available to the MPI and MAUREL & PROM shareholders prior to the general meetings of the two companies convened to approve the Merger. Said document will be prepared following the outline presented in Appendix II to AMF Instruction no. 2005-11; |

To this end, the Parties will fully cooperate and exchange all necessary information and, where relevant, the responses to be made to the additional information requests they may receive from the AMF. The Parties will keep one another regularly and promptly informed of how the review and registration of said document is progressing and will provide one another with copies of any request and/or official correspondence with the AMF in connection with the Merger. The Parties will consult one another before making any replies to the AMF and will ask the AMF to invite the other Party to attend any meeting that is organised between the AMF and one of the Parties.

| 8.2 | Management of MPI and XXXXXX & PROM |

As from signature of this Agreement and until the Final Completion Date, XXXXXX & PROM and MPI undertake to operate their businesses in the ordinary course as an ordinary prudent person, i.e. to engage in reasonable and customary day-to-day management.

| ARTICLE 9. | SHARE EXCHANGE RATIO |

The share exchange ratio proposed to MAUREL & PROM and MPI shareholders is set at 1 MAUREL & PROM share for 1.75 MPI shares (i.e. 4 XXXXXX & PROM shares for 7 MPI shares), implementing the respective valuations of the Parties set out in Schedule 9, such valuation being calculated, as specified in Schedule 9, post Exceptional Distribution.

The methods used to determine the excahnge ratio are set out in Schedule 9.

15

ENGLISH LANGUAGE TRANSLATION

FOR INFORMATION PURPOSES ONLY

| ARTICLE 10. | REMUNERATION OF CONTRIBUTION AND MAUREL & PROM SHARE CAPITAL INCREASE |

MAUREL & PROM will issue new shares as consideration for the MPI shares.

Consequently, in accordance with the exchange ratio of 1.75 MPI shares for 1 MAUREL & PROM share, 63,234,026 fully paid-up new MAUREL & PROM shares with a par value of EUR 0.77 each will be issued by XXXXXX & PROM as new shares for a total share capital increase of EUR 48,690,200.02.

Newly created shares will be allocated to the owners of the 110,659,545 shares that make up the MPI share capital (which are entitled to consideration) as at the Final Completion Date in proportion to their equity holdings.

After the Merger, the MAUREL & PROM share capital will have increased from EUR 93,604,436.31 to EUR 142,294,636.33. It will be divided into 184,798,229 fully paid-up shares of the same category with a par value of EUR 0.77 each.

As the exchange ratio for the Merger will be 1 MAUREL & PROM share for 1.75 MPI shares, the shareholders without the requisite proportion or a multiple thereof must transfer the share franctions or acquire the necessary rights to achieve the requisite proportion. MPI shareholders will be responsible for selling or purchasing share fractions, and MPI shareholders owning a number of MPI shares on the Final Completion Date such that they are not entitled to a whole number of new MAUREL & PROM shares will be deemed to have expressly agreed to participate in the mechanism described below for the disposal of new MAUREL & PROM share fractions.

| 10.1 | Vesting rights and rights attached to the new shares |

The shares issued by XXXXXX & PROM in consideration of the Merger will carry current dividend rights as from the Final Completion Date. As soon as they are issued, they will rank equally with outstanding shares and be submitted to all provisions of the articles of association and the same obligations; in particular they will entitle holders to all dividends, interim dividends, or distributions from reserve accounts that may be decided upon after the issue date.

All new MAUREL & PROM shares will be eligible for trading once the issue of new shares in consideration for the Merger has been fully completed pursuant to the provisions of article L.228-10 of the French Commercial Code. A request for a listing of the new shares issued by MAUREL & PROM on the regulated market of Euronext Paris (compartment A) will be made at the earliest opportunity following the issue date, under the same identification number as the existing shares making up the share capital of MAUREL & PROM (ISIN code FR0000051070). The terms for the listing of the new shares issued by MAUREL & PROM will be specified in a Euronext Paris notice.

Unless the relevant MPI shareholders agree otherwise, any divided ownership of MPI shares will automatically be transferred to the new MAUREL & PROM shares issued as consideration for MPI shares and in accordance with the ratio of such dividend ownership.

In accordance with article L.225-124 of the French Commercial Code, new MAUREL & PROM registered shares issued as consideration for the Merger will include double voting rights, if the MPI shares being exchanged carried double voting rights. For shareholders who have held registered MPI shares for less than four (4) years, the period for which the MPI shares exchanged in the Merger have been registered in the name of the same shareholder will be taken into account when calculating the period of four (4) years of ownership of double voting rights for the new MAUREL & PROM shares remitted in exchange.

16

ENGLISH LANGUAGE TRANSLATION

FOR INFORMATION PURPOSES ONLY

| 10.2 | Effect of the Merger on MPI Free Shares and MPI Free Preferred Shares |

| 10.2.1 | Effect of the Merger on MPI Free Shares |

New MAUREL & PROM shares will be issued in consideration of the Merger and exchanged for MPI Free Shares still under lock-up period, it being understood that (i) new MAUREL & PROM shares will be allocated in consideration of the MPI Free Shares at the exchange ratio applicable for the Merger and (ii) the new MAUREL & PROM shares issued in consideration of the MPI Free Shares will be subject to the remaining lock-up period for the MPI Free Shares and other applicable terms of the MPI Free Shares plan in accordance with article L.000-000-0 III of the French Commercial Code and the terms of the MPI Free Shares plan.

| 10.2.2 | Effect of the Merger on MPI Free Preferred Shares |

In accordance with the provisions of articles L.000-000-0 and L.228-17 of the French Commercial Code and (ii) of article 16 of the MPI Free Preferred Share plan of 22 May 2015, XXXXXX & PROM will automatically replace MPI in MPI’s obligations towards the beneficiaries of the MPI Free Preferred Shares, it being specified that the exchange ratio will be applied to the maximum number of MPI shares obtained from the conversion of the MPI Free Preferred Shares. The relevant bodies of MAUREL & PROM will propose securities with equivalent features to the beneficiaries under the conditions set forth by law.

| 10.3 | Unallocated new shares representing fractional rights |

Pursuant to the provisions of articles L.228-6-1 and R.228-12 of the French Commercial Code, any new shares not allocated to MPI shareholders that represent fractional rights will be sold. The sale of these new shares and the allocation of the proceeds from the sales must occur within thirty (30) days as from the latest date the whole number of allocated shares is recorded on the holder’s account.

The new shares representing fractional rights will be sold on Euronext Paris through a clearing bank. The bank will be selected to facilitate the remittal and payment of net proceeds from the sale of new shares representing fractional rights in order to allocate the proceeds to the relevant MPI shareholders. The designated intermediary will sell the new shares on the Euronext Paris regulated market on behalf of participating MPI shareholders. Shareholders participating in the sale of fractional rights will receive net proceeds pro rata to their participation in the scheme. For the avoidance of doubt, it is understood that no interest will be paid on the cash amount to be received by MPI shareholders in consideration for a share fractions, even where payment of said amount has been delayed.

| 10.4 | Unclaimed new shares |

Pursuant to the provisions of articles L.228-6-3 and R.228-14 of the French Commercial Code, new shares whose holders are unknown to the custody account keeper (teneur de compte) or holders who have not been reached by notices for ten (10) full years may be sold after a period of one (1) year in accordance with the terms set out in article R.228-12, second paragraph of the French Commercial Code.

| ARTICLE 11. | MERGER PREMIUM |

The difference between (i) the net assets to be transferred, i.e. EUR 353,749,589, and (ii) the amount of the share capital increase of MAUREL & PROM, i.e. EUR 48,690,200.02, constitutes the merger premium, in an amount of EUR 305,059,388.98, which will be recorded in the financial statements in accordance with applicable laws and regulations.

17

ENGLISH LANGUAGE TRANSLATION

FOR INFORMATION PURPOSES ONLY

This amount will be recorded as a liability in the MAUREL & PROM balance sheet under item “Merger Premium”, on which the rights of all existing and future shareholders of MAUREL & PROM will apply.

The merger premium may be allocated in accordance with currently applicable principles as decided by the general meeting of the shareholders of MAUREL & PROM. A proposal will be submitted to the MAUREL & PROM shareholders at the general meeting convened to approve the Merger to authorise the board of directors to deduct any amounts from the merger premium for the purpose of (i) replenishing all regulated reserves or provisions recorded in the MPI balance sheet as part of the liabilities on the balance sheet of MAUREL & PROM; (ii) paying, out of the merger premium, all expenses, taxes and fees incurred or payable as a result of the Merger; (iii) paying, out of the merger premium, all amounts required to ensure that the legal reserve account corresponds to one tenth of the new post-Merger share capital amount; and (iv) paying, out of the merger premium, all omitted or undisclosed liabilities pertaining to the transferred assets.

| ARTICLE 12. | OWNERSHIP AND EFFECTIVE DATE OF THE MERGER FOR ACCOUNTING AND TAX PURPOSES |

Ownership of all assets and rights of MPI (including any assets and rights omitted from the Agreement or from the financial statements of MPI) will be transferred to MAUREL & PROM on the Final Completion Date. XXXXXX & PROM undertakes to accept all transferred assets and liabilities such as they exist on the Final Completion Date.

Pursuant to the provisions of article L.236-4 2° of the French Commercial Code, MAUREL & PROM and MPI expressly agree that the effective date of the Merger from an accounting and tax point of view will be retroactive to the first day of the then current MPI financial year on the Final Completion Date and will therefore occur prior to the date upon which the Merger proposal is submitted to the shareholders of MAUREL & PROM and MPI for approval, such that all earnings or losses generated by any and all transactions carried out by MPI commencing on the first day of its financial year in progress on the Final Completion Date and until the Final Completion Date will be recorded by XXXXXX & PROM in so far as these transactions will be deemed to have been carried out by XXXXXX & PROM.

| ARTICLE 13. | CHARGES AND CONDITIONS |

| 13.1 | General charges and conditions |

Pursuant to the provisions of article L.236-14 of the French Commercial Code, non-bondholders creditors of MAUREL & PROM and MPI with claims arising prior to the publication date of the Agreement have a period of thirty (30) days to oppose the merger as from the last date of publication as provided for in article R.236-2 of the French Commercial Code or as from the date on which the Agreement is published on the website of each of the Parties, as provided for in article R.236-2-1 of the French Commercial Code. Any opposition by a creditor must be submitted to the Commercial Court, which may dismiss the claim or order its repayment or the granting of guarantees if any such guarantees are offered by XXXXXX & PROM and if they are deemed sufficient. Failing the repayment of the claims or granting of guarantees as ordered, the Merger will not be enforceable against the opposing creditors. In accordance with the law, any opposition made by a creditor will not prevent the Parties from proceeding with any operations pertaining to the Merger.

18

ENGLISH LANGUAGE TRANSLATION

FOR INFORMATION PURPOSES ONLY

| 13.2 | Charges and conditions pertaining to MAUREL & PROM |

The transfers made as part of the Merger will be subject to the standard legal charges and conditions applicable to such cases, including those listed below, which the representative of MAUREL & PROM undertakes to ensure are carried out and completed.

| • | MAUREL & PROM will be subrogated to all MPI rights and obligations relating to the assets and liabilities transferred via the Merger. |

| • | MAUREL & PROM will take all assets and rights transferred to it regardless of the form thereof, including all assets and rights omitted from the Agreement or the MPI financial statements, in the condition and state in which they are found on the Final Completion Date, with no available remedy against MPI on any basis. |

| • | As from the Final Completion Date, MAUREL & PROM will bear all taxes, contributions, premiums and subscriptions and all other expenses, taxes and fees relating to the business and assets transferred. |

| • | XXXXXX & PROM will carry out all applicable formalities with a view to rendering the transfer of assets enforceable against third parties. |

| • | XXXXXX & PROM will be subrogated to all rights and obligations pertaining to all employment contracts in force on the Final Completion Date in accordance with the law and by sole operation of the Merger. |

| • | MAUREL & PROM will be bound by all off-balance sheet commitments made by MPI on the same terms, including all forms of guarantee (caution, garantie, aval) granted by MPI, and will benefit from all related counter-guarantees and security and, more generally, all off-balance sheet commitments received. |

| • | As from the Final Completion Date, XXXXXX & PROM will be subrogated to all causes, actions and proceedings pending before the judicial courts and arbitral tribunals to which MPI is a party. XXXXXX & PROM will have full power to commence or act as a defendant in all pending or future judicial proceedings or arbitral actions in the stead of MPI, to agree to all decisions and to receive or pay all sums payable as a result of an award or settlement. |

| • | All securities and rights held or owned by MPI in third party companies will be transferred to MAUREL & PROM by sole operation of the Merger; MAUREL & PROM will thus become a shareholder of said companies or holder and/or owner of said rights subject to compliance with the applicable legal, regulatory and contractual conditions. The Parties will comply with the provisions of all laws, regulations, contracts and articles of association concerning the transferability of securities and rights, including those relating to approvals and pre-emptive rights if applicable in the event of a merger. MPI or, as applicable, MAUREL & PROM, will notify any and all necessary third parties of the transfer of the securities further to the Merger in accordance with the conditions applicable in each case. Any failure by the Parties to obtain an approval where such approval is legally required will not compromise the validity of the Merger or the Agreement. |

| • | As from the Final Completion Date, XXXXXX & PROM will bear and must perform all agreements, contracts and undertakings as may have been contracted by MPI and are in effect on the Final Completion Date. MAUREL & PROM will be subrogated at its own risk to all rights and obligations arising out of the above commitments, contracted by MPI, with no available remedy against the latter. Should the transfer of certain contracts or assets be conditional upon obtaining the agreement or approval of a co-contracting party or any other third party, MAUREL & PROM will request all necessary agreements or approvals. |

19

ENGLISH LANGUAGE TRANSLATION

FOR INFORMATION PURPOSES ONLY

| • | MAUREL & PROM will have sole rights to the dividends and other earnings due on the securities and rights in companies transferred to it by MPI and will take personal responsibility for transferring said securities and rights into its name following the Final Completion Date. |

| • | XXXXXX & PROM will have sole ownership of the trademarks, domain names and other intellectual property rights of MPI as from the Final Completion Date. Consequently, from such date MAUREL & PROM will have the exclusive right to use and exploit all such rights without restriction and as it deems fit throughout the territory in which they are protected, it being specified that MAUREL & PROM will assume and will be subrogated to all rights and obligations arising out of all agreements relating to said intangible assets concluded with third parties. |

| • | As from the Final Completion Date, XXXXXX & PROM will be automatically subrogated to all rights, actions, charges over property (hypothèques), liens (privilèges), guarantees and security interests, whether personal or over property, of all types as may be attached to all claims held by MPI. |

| • | MAUREL & PROM will complete, if necessary, all applicable formalities for the transfer of the assets and to render such transfer enforceable against all third parties; all necessary powers are hereby granted to the bearer of an excerpt from or copy of this Agreement. |

| 13.3 | Charges and conditions pertaining to MPI |

The transfers made as part of the Merger will be carried out with the standard guarantees and subject to the standard legal charges and conditions in such cases, including those listed below:

| • | As from the date hereof until the Final Completion Date and save with the approval of XXXXXX & PROM, MPI undertakes to refrain from entering into any agreements for the sale of the assets to be transferred and not to sign any agreement, contract or undertaking outside the ordinary course of business; |

| • | MPI will supply MAUREL & PROM with all information it may require, sign all documents and provide all relevant assistance to ensure that both the transfer of assets and rights and the Agreement are fully effective and enforceable over all third parties. |

| ARTICLE 14. | REPRESENTATIONS |

| 14.1 | Representations of MAUREL & PROM |

As at the date of the Agreement, MAUREL & PROM represents that:

| • | it has full capacity to contract and is not subject to any measures which could impair its civil capacity; |

| • | it has obtained the necessary authorisations from the appropriate decision-making bodies to sign and perform the Agreement; |

| • | it is a duly incorporated company, is not subject to any action for a declaration of invalidity and does not meet the criteria for early dissolution as provided by French law; |

20

ENGLISH LANGUAGE TRANSLATION

FOR INFORMATION PURPOSES ONLY

| • | it is not and has never been insolvent (en état de cessation des paiements), subject to pre-insolvency (conciliation, sauvegarde, sauvegarde financière, sauvegarde financière accélérée) or insolvency proceedings (redressement, liquidation judiciaire, liquidation amiable) or any other equivalent proceedings; |

| • | no proceedings have been brought against it that could fully or significantly impair its ability to carry on its business as currently carried on; and |

| • | there is no risk of confiscation or any other form of expropriation with respect to its assets and liabilities. |

| 14.2 | Representations of MPI |

As at the date of the Agreement, MPI represents that:

| • | it has full capacity to contract and is not subject to any measures which could impair its civil capacity; |

| • | it has obtained the necessary authorisations from the appropriate decision-making bodies to sign and perform the Agreement; |

| • | it is a duly incorporated company, is not subject to any action for a declaration of invalidity and does not meet the criteria for early dissolution as provided by French law; and |

| • | it is not and has never been insolvent, subject to pre-insolvency or insolvency proceedings or any other equivalent proceedings. |

Regarding the transfers made as part of the Merger, MPI represents that:

| • | no proceedings have been brought against it that could fully or significantly impair its ability to carry on its business as currently carried on; |

| • | there are no financial or other commitments, including any amounts payable as a result of a dispute or potential dispute, that might affect the valuation of the assets transferred as part of the Merger; and |

| • | there is no risk of confiscation or any other form of expropriation with respect to its assets and liabilities. |

| ARTICLE 15. | DISSOLUTION OF MPI |

XXXXXX & PROM and MPI agree that the Merger will be complete on the Final Completion Date.

Pursuant to the provisions of article L.236-3 I of the French Commercial Code, as a result of the transfer of all of its assets and liabilities to MAUREL & PROM, MPI will be automatically dissolved without liquidation on the Final Completion Date.

The shares issued by XXXXXX & PROM to remunerate the Merger will be directly allocated to the shareholders of MPI based on the exchange ratio defined in Article ARTICLE 9 above.

| ARTICLE 16. | TAX PROVISIONS |

| 16.1 | General undertaking to file tax returns |

The representatives of MAUREL & PROM and MPI will ensure that these companies comply with all applicable laws with respect to the returns to be filed for the payment of corporate income tax (impôt sur les sociétés) and all other forms of tax to which the Merger gives rise, in accordance with the provisions set out below.

21

ENGLISH LANGUAGE TRANSLATION

FOR INFORMATION PURPOSES ONLY

| 16.2 | Retroactive effect |

The Merger will take effect from a tax and accounting point of view on the first day of the then current financial year of MPI on the Final Completion Date.

The Parties acknowledge that the retroactive effect of the Merger will have full effect from a tax point of view and undertake to bear the resulting consequences.

| 16.3 | Corporate income tax |

As provided for above, the Merger will take effect for tax and accounting purposes on the first day of the then current financial year of MPI on the Final Completion Date. All tax credits and losses arising after such date out of the business of MPI will thus be incorporated into the taxable income of MAUREL & PROM for the financial year in progress on the Final Completion Date.

The representatives of MAUREL & PROM and MPI represent that on the Final Completion Date: (i) XXXXXX & PROM and MPI are both submitted to corporate income tax and have their registered offices in France; (ii) the Merger will be submitted to the preferential tax rules set forth in article 210 A of the French Tax Code (Code Général des Impôts).

Accordingly, XXXXXX & PROM expressly undertake to comply with all of the commitments set forth in article 210 A of the French Tax Code and in particular, as applicable, to:

| (i) | incorporate into its liabilities all MPI provisions subject to deferred taxation that will not be rendered ineffective by the Merger, including any regulated provisions; |

| (ii) | assume the obligations of MPI with respect to adding back any profits/losses carried forward for tax purposes; |

| (iii) | calculate the capital gains generated on the sale of any non-depreciable non-current assets received as part of the Merger, pursuant to article 210 A of the French Tax Code, based on the value of these assets, from a tax point of view, recorded in MPI financial statements on the Final Completion Date; |

| (iv) | add back to its income liable to corporate income tax, under the conditions set forth in article 210 A of the French Tax Code, any capital gains generated by the Merger as a result of the transfer of depreciable assets, and to include to the result of the financial year of the sale any untaxed portion of the capital gains on assets sold prior to the expiry of the add back period as part of its profits or losses for the year; |

| (v) | record, in its balance sheet, those assets transferred to it, excluding non-current and equivalent assets as provided for in article 210 A(6) of the French Tax Code, at the value of said assets, from a tax point of view, in the financial statements of MPI or, failing this, record the profit corresponding to the difference between the new value of these assets and their previous value, from a tax point of view, in the financial statements of MPI as part of the income for the financial year; |

| (vi) | comply with the tax reporting obligations set forth in article 54 septies I and II of the French Tax Code, i.e.: |

| • | append to the tax returns of the Parties a statement of the capital gains on the transferred assets containing the information required by article 38 quindecies of Appendix III to the French Tax Code, |

| • | with respect to MAUREL & PROM, keep a special register of capital gains on non-depreciable assets, to be retained until the end of the third year following that in which the last asset entered into the register is no longer recorded as an asset of MPI, under the conditions set forth in article L.102 B of the French Code of Tax Procedures (Livre des procédures fiscales); this register must be disclosed in the event of a tax audit. |

22

ENGLISH LANGUAGE TRANSLATION

FOR INFORMATION PURPOSES ONLY

Pursuant to the provisions of article 145 of the French Tax Code, for any investment securities transferred under the preferential rules set forth in article 210 A of the French Tax Code, the retention period applicable to MAUREL & PROM will be deemed to have commenced on the date of subscription or acquisition of the securities by MPI;

| (vii) | in general, assume the profits and/or charges from all tax-related commitments arising out of any and all assets and liabilities transferred as part of the Merger as may have been taken out or over by MPI as part of any previous transactions to which preferential tax rules were applied with respect to registration and/or corporate income tax or other revenue-related tax. |

| 16.4 | Value Added Tax (VAT) |

In so far as the Merger constitutes a transfer of all assets and liabilities of MPI and as MAUREL & PROM and MPI are liable to VAT, article 257 bis of the French Tax Code and the principles set forth in BOFIP BOI-TVA-CHAMP-10-10-50-10-20121001 will apply:

| (i) | all deliveries of goods and services carried out between parties liable to VAT as part of a universal transfer of assets and liabilities (transmission universelle de patrimoine) are exempt from VAT. This exemption applies to all goods and services concerned by the transfer, regardless of the nature thereof; |

| (ii) | XXXXXX & PROM will assume all rights and obligations of MPI, including with respect to adjustments of the tax deducted by MPI: |

| • | as applicable, MAUREL & PROM must make all adjustments of the tax deduction rights provided for in article 207 to Appendix II to the French Tax Code, which MPI would have had to make had it continued to use the assets in question; |

| • | MAUREL & PROM and MPI will enter the total amount before tax of the value of the goods transferred as part of the Merger on their VAT returns for the period during which the Merger is to take place. This amount should be entered under “Autres opérations non imposables” (BOI-TVA-DECLA-20-30-20-20120912 § 20); |

| (iii) | with respect to VAT credits, pursuant to the principles set out in BOFIP BOI-TVA-DED-50-20-20-20140513 no.130, MPI will automatically transfer all VAT credits available to it to MAUREL & PROM, if any, on the Final Completion Date: |

| • | MPI will send two copies of the appropriate tax form reporting the transfer of its VAT credit to MAUREL & PROM to its allocated tax office; |

| • | MAUREL & PROM must notify its allocated tax office of the amount of any credits transferred to it, citing the Merger with MPI as a reference; |

| • | MAUREL & PROM will provide any and all accounting documentation to the tax office to justify the amount of the deduction rights included in the credit; |

| (iv) | transfers of immovable property liable to VAT on property will be “reported as non-existent” for the purposes of article 257-7 of the French Tax Code. |

23

ENGLISH LANGUAGE TRANSLATION

FOR INFORMATION PURPOSES ONLY

| 16.5 | Registration tax |

The Parties represent that the Merger falls within the scope of the special rules set forth in article 816 of the French Tax Code in so far as it is to be carried out under conditions that comply with the provisions of articles 301-B and 301-F of Appendix II to the French Tax Code.

Accordingly, the Merger will be subject to a single fixed-rate registration tax of EUR 500.

| 16.6 | Other taxes |

| (i) | Contribution Economique Territoriale (“CET”) |

CET is payable by the taxpayer carrying on the applicable business on 1 January. In so far as the retroactive effect of the Merger has no bearing on CET, MPI will remain liable for the payment of this tax on the business in 2015. However, by operation of the Merger, XXXXXX & PROM will assume the obligations of MPI for the payment of CET 2015.

| (ii) | Miscellaneous tax provisions |

In general, XXXXXX & PROM will automatically be subrogated to the rights and obligations of MPI with respect to all taxes and other tax obligations to which it may be subject and the benefits of any surplus or credit.

For the avoidance of doubt, XXXXXX & PROM undertakes to bear all payments of the taxe d’apprentissage and participation au financement de la formation professionnelle continue employment contributions to which MPI may be liable starting from the first day of its financial year that is in progress on the Final Completion Date.

Pursuant to the provisions of article 163 of Appendix II to the French Tax Code, XXXXXX & PROM undertakes to bear all obligations relating to the participation des employeurs à l’effort de construction employment contribution to which MPI will continue to be liable on the Final Completion Date for all salaries paid by MPI starting from the first day of its financial year that is in progress on the Final Completion Date.

| ARTICLE 17. | MISCELLANEOUS PROVISIONS |

| 17.1 | Costs |

Each Party will bear all costs and expenses it may incur for the negotiation and performance of the Agreement, it being specified that should the Merger take place, all costs, taxes and fees resulting therefrom and from all consequences thereof will be borne in full by XXXXXX & PROM.

| 17.2 | Delivery of documents |

All titles of ownership, securities, contracts, archives, exhibits, accounting books and other documents relating to the transferred assets will be delivered by MPI to MAUREL & PROM on the Final Completion Date.

24

ENGLISH LANGUAGE TRANSLATION

FOR INFORMATION PURPOSES ONLY

| 17.3 | Governing law and jurisdiction |

Any issues pertaining to the validity, interpretation and performance of the Agreement will be governed by French law.

Any disputes arising out of or in connection to the Agreement or its schedules that cannot be settled out of court will be submitted, where permitted by law, to the exclusive jurisdiction of the Paris Commercial Court.

| 17.4 | Notifications |

For the purposes of the Agreement and any subsequent agreements and for all service of documents and notices, the addresses for service of the Parties will be their respective registered offices.

| 17.5 | Validity |

If any provision of the Agreement is or becomes invalid, this will not affect the validity of the other provisions of the Agreement, which will remain in full force and effect.

In the above circumstances, the Parties will cooperate to draft a replacement clause which, to the greatest extent possible, achieves the intended result of the invalid provision.

| 17.6 | Amendments and waivers |

The Parties agree that this Agreement may only be amended by written amendment signed by all the Parties. However, each Party may individually waive a right conferred by this Agreement or a condition stipulated in its benefit, subject to notification in writing of such waiver to the other Party.

| 17.7 | Formalities |

XXXXXX & PROM will carry out all necessary formalities relating to the filing and publication of the Merger.

XXXXXX & PROM will assume personal responsibility for all necessary declarations and formalities with respect to all appropriate authorities to transfer the assets into its name.

In general, XXXXXX & PROM will complete all necessary formalities to render the transfer of assets and rights enforceable against third parties.

The Parties will file a copy of the Agreement with the registry of the Paris Commercial Court and will comply with all publication obligations set forth in the provisions of articles L.236-6, R.236-3 (or, as applicable, R.236-3-1) and R.236-2-1 of the French Commercial Code.

Pursuant to the provisions of article R.236-2-1 of the French Commercial Code, MAUREL & PROM and MPI will publish the Agreement and the merger notice on their respective websites for a continuous period of thirty (30) days before the Final Completion Date and under conditions that guarantee the security and authenticity of these documents.

| 17.8 | Powers |

All powers are hereby expressly granted to:

| • | the undersigned, in their official capacity as the representatives of the companies concerned by the Merger, acting individually or collectively, to take all necessary actions by way of all additional or supplementary agreements; |

| • | to the bearers of an original, copy or official copy (expédition) of the Agreement or a certified excerpt therefrom to carry out all formalities and make all declarations, serve all notices, make all filings, registrations and publications and, in general, to meet all necessary legal formalities. |

* *

*

25

ENGLISH LANGUAGE TRANSLATION

FOR INFORMATION PURPOSES ONLY

| Executed in Paris, as at the date hereof, | ||

| In seven original counterparts, | ||

|

| ||

| ETABLISSEMENTS | ||

| XXXXXX & PROM S.A. | ||

| By: |

| |

| Position: |

| |

|

| ||

| MPI S.A. | ||

| By: |

| |

| Position: |

| |

26

ENGLISH LANGUAGE TRANSLATION

FOR INFORMATION PURPOSES ONLY

LIST OF SCHEDULES

| SCHEDULE 4.1 | Annual financial statements of MPI as at 31 December 2014 | |

| SCHEDULE 4.2 | Annual financial statements of MAUREL & PROM as at 31 December 2014 | |

| SCHEDULE 5 | Multi-criteria method for the calculation of the actual value of the transferred assets | |

| SCHEDULE 7 | List of MPI employees to be transferred to MAUREL & PROM | |

| SCHEDULE 9 | Calculation of the exchange ratio | |

27

ENGLISH LANGUAGE TRANSLATION

FOR INFORMATION PURPOSES ONLY

SCHEDULE 4.1

Annual financial statements of MPI as at 31 December 2014

28

ENGLISH LANGUAGE TRANSLATION

FOR INFORMATION PURPOSES ONLY

SCHEDULE 4.2

Annual financial statements of MAUREL & PROM as at 31 December 2014

29

ENGLISH LANGUAGE TRANSLATION

FOR INFORMATION PURPOSES ONLY

SCHEDULE 5

Multi-criteria method for the determination of the actual value of the transferred assets

| • | Determination of the actual value of the stake in Seplat |

The determination of an actual value for MPI’s stake in Seplat is EUR 140 million. It is based on the average share price at 1 month, 2 months, 3 months and 4 months prior to 8 October 2015 (date on which the figures have been calculated for the boards of directors of MAUREL & PROM and MPI dated 15 October 2015 and having approved the Agreement), i.e. EUR 1.16 per Seplat share (or GBP 0.8440 at an average EUR/GBP exchange rate over the same period of 0.725).

The averages were taken from market data provided by BNPP.

Seplat market valuation

| Nombre de titres Seplat (en millions) |

553,310 | |||

| MPI’s stake in Seplat |

21,76 | % |

| Seplat share price (£) |

Seplat share price (€) |

Seplat market cap (€m) |

MPI stake in Seplat (€m) |

|||||||||||||

| spot (8/10/2015) |

0,780 | 1,06 | 585 | 127 | ||||||||||||

| 1m average |

0,802 | 1,09 | 605 | 132 | ||||||||||||

| 2m average |

0,803 | 1,10 | 610 | 133 | ||||||||||||

| 3m average |

0,880 | 1,22 | 676 | 147 | ||||||||||||

| 4m average |

0,891 | 1,24 | 686 | 149 | ||||||||||||

| 6m average |

1,052 | 1,46 | 808 | 176 | ||||||||||||

| 9m average |

1,175 | 1,62 | 895 | 195 | ||||||||||||

| 12m average |

1,272 | 1,71 | 948 | 206 | ||||||||||||

| moyenne 1m, 2m, 3m et 4m |

0,844 | 1,16 | 1 | 140 | ||||||||||||

| • | Determination of the actual value of the stake in Saint-Xxxxx Energie |

The determination of an actual value for MPI’s stake in Saint-Xxxxx Energie is based on MPI’s share (two-thirds) in past costs, in keeping with the oil sector practice when valuing assets for farm-out agreements.

Past costs amount to EUR 78,097,000. They are determined on the basis of the following elements taken from the audited financial statements of Saint-Xxxxx Energie as at 31 December 2014:

| • | securities held by Saint Xxxxx Energie in its subsidiaries (excluding Maurel & Prom Irak): EUR 114,000; |

| • | shareholder loans granted by Saint-Xxxxx Energie to its subsidiaries (excluding Maurel & Prom Irak) including restated accrued interest on corresponding unrealised foreign exchange gains: EUR 77,768,000; |

| • | free cash flow: EUR 215,000. |

| • | Determination of the actual value of other receivables, debts and free cash flows |

Other receivables, debts and free cash flows will be transferred at their net book value as stated in MPI’s audited financial statements as at 31 December 2014.

The value of the Cardinal securities recorded as an asset has been set off against the debt on the investment.

Treasury shares will be transferred at a value of zero as they are to be cancelled.

30

ENGLISH LANGUAGE TRANSLATION

FOR INFORMATION PURPOSES ONLY

Unrealised foreign exchange losses and the related provision for foreign exchange losses have been set off.

The unrealised foreign exchange gains on the loans granted to Saint-Xxxxx Energie will not be transferred as they have been included in the actual value of Saint Xxxxx Energie, as explained above.

31

ENGLISH LANGUAGE TRANSLATION

FOR INFORMATION PURPOSES ONLY

SCHEDULE 7

List of MPI employees to be transferred to MAUREL & PROM

| • | Xxxx xx Xxxxxxxx |

| • | Xxxxxxxxxx Xxxxxxxxx |

| • | Xxxxxxx Xxxxxxxxxx |

| • | Xxxxxxx Xxxxxxx |

32

ENGLISH LANGUAGE TRANSLATION

FOR INFORMATION PURPOSES ONLY

SCHEDULE 9

Calculation of the exchange ratio

The consideration for the transfers and the method of calculation of the exchange ratio were jointly determined by the MAUREL & PROM and MPI boards of directors.

| 1. | Criteria used to compare the companies |

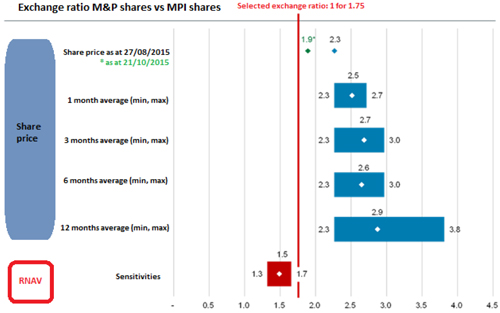

The proposed exchange ratio of 1 MAUREL & PROM share for 1.75 MPI shares (corresponding to an exchange ratio of 4 MAUREL & PROM shares for 7 MPI shares), post-Exceptional Distribution, was determined using a multi-criteria approach relying on the usual and appropriate valuation methods for the Merger, taking into account the specific characteristics of the oil and gas exploration and production industry.

The following were applied:

| • | an analysis of the MAUREL & XXXX and MPI historical share prices; and |

| • | a comparison of the valuations obtained for MAUREL & PROM and for MPI using the revalued net asset value (RNAV) method, based mainly on the value of the principal assets of the two companies using the discounted cash flow (DCF) method. |

In light of the above, the exchange ratio was determined as the ratio between the values of the equity of MAUREL & PROM and of MPI after taking into account the Exceptional Distribution.

| 2. | Criteria not used to compare the companies |

The following methods were not applied:

Financial analysts’ forecasts of share prices

This method was not selected given the lack of regular coverage of MPI by financial analysts and the limited coverage of MAUREL & PROM.

Comparable peers

This method was not selected given (i) the lack of listed exploration and production companies that are truly comparable to MAUREL & PROM or to MPI, particularly in terms of geographical exposure, the gas/oil mix of reserves and the exploration/production mix and (ii) MPI’s unique position as an oil and gas exploration and production company and a holding company.

Comparable transactions

This method was not selected given the lack of comparable past transactions (in terms of oil and gas prices, geographical exposure and business mix) of which the terms are publicly available.

Net asset value