MERGER AND LISTING PROSPECTUS 23 October 2020 The Boards of Directors of Altia Plc (“Altia”) and Arcus ASA (“Arcus”) have, on 29 September 2020, signed a combination agreement (the “Combination Agreement”) concerning the combination of their business...

Exhibit 1.18

| MERGER AND LISTING PROSPECTUS | 23 October 2020 |

|

|

|

The Boards of Directors of Altia Plc (“Altia”) and Arcus ASA (“Arcus”) have, on 29 September 2020, signed a combination agreement (the “Combination Agreement”) concerning the combination of their business operations and a merger plan (the “Merger Plan”), according to which Arcus shall be merged into Altia through a statutory cross-border absoprtion merger in such a manner that all assets and liabilities of Arcus shall be transferred without a liquidation procedure to Altia (the “Merger”). The Boards of Directors of Altia and ▇▇▇▇▇ have on 2 October 2020 proposed that the Extraordinary General Meetings of Altia and Arcus, convened to be held on 12 November 2020, would resolve upon the Merger as set forth in the Merger Plan. The completion of the Merger is subject to, inter alia, approval by the Extraordinary General Meetings of Altia and Arcus, obtaining of necessary regulatory approvals, including merger control approvals by the relevant competition authorities, fulfillment of other conditions to completion set forth in the Combination Agreement and the Merger Plan or waiver of such conditions. Furthermore, it is required for the completion of the Merger that the Combination Agreement has not been terminated in accordance with its provisions, and that the execution of the Merger is registered with the trade register maintained by the Finnish Patent and Registration Office (the “Finnish Trade Register”). Information on the conditions for the completion of the Merger included in the Combination Agreement and the Merger Plan is being presented in the section “Merger of Altia and Arcus – Combination Agreement – Conditions to the Completion of the Merger” and in the Merger Plan, which is attached to this Merger and Listing Prospectus (the “Merger Prospectus”) as Annex D. The Merger shall be completed on the date of registration of the execution of the Merger with the Finnish Trade Register (the “Effective Date”). The planned Effective Date is 1 April 2021 (effective registration time approximately at 00:01:01). The planned Effective Date is not binding and the actual Effective Date may be earlier or later than above date. Arcus shall automatically dissolve on the Effective Date.

The Merger is based on an exchange ratio reflecting a relative value of Altia and ▇▇▇▇▇ of 53.5:46.5. The shareholders of Arcus shall receive as merger consideration 0.4618 new shares in Altia (the “Merger Consideration Shares”) for each share owned by them in Arcus (the “Merger Consideration”). As the primary alternative, ▇▇▇▇▇ expects to deliver the Merger Consideration Shares through a depository interest arrangement in the Norwegian Verdipapirsentralen (“VPS”). Alternatively, as a secondary alternative the Merger Consideration Shares may be delivered as depository receipts registered in VPS or as directly held shares in the Combined Company in the book-entry securities system maintained by Euroclear Finland Oy (“Euroclear Finland”). The allocation of the Merger Consideration will be based on the shareholding in Arcus at a record date to be set in connection with the completion of the Merger. No Merger Consideration will be distributed to shares in Arcus held by Arcus itself or by Altia. On the date of this Merger Prospectus, the total number of the Merger Consideration Shares to be issued is expected to be approximately 31,409,930 shares and the total number of shares in the Combined Company would thus be 67,550,415 (each a “Share” and collectively the “Shares”). The Merger Consideration Shares shall be registered on the book-entry accounts of the shareholders of Arcus on or about the Effective Date or as soon as possible thereafter in accordance with the practices followed by Euroclear Finland and the VPS. See “Merger of Altia and Arcus – Merger Plan – Merger Consideration”.

▇▇▇▇▇ has prepared and published this Merger Prospectus in order to issue Merger Consideration Shares to the shareholders of Arcus. Altia intends to apply for the Merger Consideration Shares to be listed on the official list of Nasdaq Helsinki Ltd (“Nasdaq Helsinki”) (the “Listing”). Altia and Arcus will seek to ensure that primarily, the Combined Company’s Shares through a depository interest arrangement, or secondarily, the depository receipts or directly-held Shares in the Combined Company will be subject to a secondary listing on the Oslo Børs in connection with the completion of the Merger or as soon as possible thereafter, for a transitional period of four (4) months from the first day of the secondary listing on the Oslo Børs (the “Secondary Listing”). The trading in the shares of Arcus on Oslo Børs is expected to end at the end of the last trading day preceding the Effective Date and the shares in Arcus are expected to cease to be listed on Oslo Børs as of the Effective Date, at the latest. Information on Altia’s obligation to supplement this Merger Prospectus has been presented in the section “Important Information”. The application for the Listing shall be done prior to the Effective Date. The trading in the Merger Consideration Shares on the official list of Nasdaq Helsinki is expected to begin approximately on the Effective Date or as soon as possible thereafter.

NOT FOR PUBLICATION OR DISTRIBUTION, IN WHOLE OR IN PART, DIRECTLY OR INDIRECTLY, IN OR INTO AUSTRALIA, CANADA, HONG KONG, JAPAN, SOUTH AFRICA OR ANY OTHER JURISDICTION WHERE SUCH PUBLICATION OR DISTRIBUTION WOULD VIOLATE APPLICABLE LAWS OR RULES OR WOULD REQUIRE ADDITIONAL DOCUMENTS TO BE COMPLETED OR REGISTERED OR REQUIRE ANY MEASURE TO BE UNDERTAKEN IN ADDITION TO THE REQUIREMENTS UNDER FINNISH LAW. SEE “IMPORTANT INFORMATION” ON PAGE ii AND “CERTAIN MATTERS” ON PAGES 54–55 BELOW.

Investing in the Combined Company involves a number of risks, see “Risk Factors.”

|

|

|

IMPORTANT INFORMATION

Altia has prepared and published this Merger Prospectus in order to issue Merger Consideration Shares to the shareholders of Arcus and carry out the Listing and the Secondary Listing. The Merger Prospectus has been prepared in accordance with the following regulations: the Finnish Securities Market Act (764/2012, as amended) (the “Finnish Securities Markets Act”), Regulation (EU) 2017/1129 of the European Parliament and of the Council of 14 June 2017, as amended (the “Prospectus Regulation”), Commission Delegated Regulation (EU) 2019/979 of 14 March 2019, supplementing Regulation (EU) 2017/1129 of the European Parliament and of the Council with regard to regulatory technical standards on key financial information in the summary of a prospectus, the publication and classification of prospectuses, advertisements for securities, supplements to a prospectus, and the notification portal, and repealing Commission Delegated Regulation (EU) No 382/2014 and Commission Delegated Regulation (EU) 2016/301, Commission Delegated Regulation (EU) 2019/980 of 14 March 2019 (Annexes 3, 12 and 20) supplementing Regulation (EU) 2017/1129 of the European Parliament and of the Council as regards the format, content, scrutiny and approval of the prospectus to be published when securities are offered to the public or admitted to trading on a regulated market, and repealing Commission Regulation (EC) No 809/2004 (together, the “Delegated Prospectus Regulation”), and the regulations and guidelines issued by the Finnish Financial Supervisory Authority (the “FIN-FSA”). The Merger Prospectus also includes a summary, which has been translated into Finnish. The FIN-FSA has approved the Merger Prospectus as competent authority under the Prospectus Regulation. The Merger Prospectus has been prepared in English and has been approved by the FIN-FSA as the competent authority under the Prospectus Regulation. The FIN-FSA only approves the Merger Prospectus as meeting the standards of completeness, comprehensibility, and consistency imposed by the Prospectus Regulation. Such approval should not be considered an endorsement of the issuer that is the subject of the Merger Prospectus. The Merger Prospectus has been drawn up as a simplified prospectus in accordance with Article 14 of the Prospectus Regulation. The record number of the FIN-FSA’s approval decision concerning the Merger Prospectus is FIVA 49/02.05.04/2020. The Merger Prospectus will be notified to the Financial Supervisory Authority in Norway in accordance with the Prospectus Regulation. This Merger Prospectus will expire after the Listing and the Secondary Listing have taken place or on 22 October 2021, at the latest.

In the Merger Prospectus, prior to the Effective Date, any reference to “Altia” or “Altia Group” means Altia Plc and its subsidiaries on a consolidated basis, except where it is clear from the context that the term means Altia Plc or a particular subsidiary or business group only. Prior to the Effective Date, any reference to “Arcus” or “Arcus Group” means Arcus ASA and its subsidiaries on a consolidated basis, except where it is clear from the context that the term means Arcus ASA or a particular subsidiary or business group only. However, references to the shares, share capital and corporate governance of Altia or Arcus refer to the shares, share capital and corporate governance of Altia Plc or Arcus ASA. The term “Combined Company” shall refer to Altia as of the Effective Date, once Arcus has merged into Altia.

Shareholders and investors should rely solely on the information contained in the Merger Prospectus as well as in the stock exchange releases published by Altia or Arcus. No person has been authorised to provide any information or give any statements other than those provided in the Merger Prospectus. Delivery of the Merger Prospectus shall not, under any circumstances, indicate that the information presented in the Merger Prospectus is correct on any day other than on the date of the Merger Prospectus, or that there would not have been any adverse changes or events after the date of the Merger Prospectus, which could have an adverse effect on Altia’s, Arcus’ or the Combined Company’s business, financial position or results of operations. If a significant new factor, material mistake or material inaccuracy relating to the information included in the Merger Prospectus which may affect the assessment of the securities arises or is noted prior to the Listing, this Merger Prospectus will be supplemented in accordance with the Prospectus Regulation. The obligation to supplement the Merger Prospectus under the Prospectus Regulation will end when the Merger Prospectus expires. Information given in the Merger Prospectus is not a guarantee or grant for future events by Altia or Arcus and shall not be considered as such. Unless otherwise stated, any estimates with respect to market development relating to Altia or Arcus or their industry are based upon reasonable estimates of the management of the respective company that such information concerns.

In a number of jurisdictions, in particular in Australia, Canada, Hong Kong, Japan and South Africa, the distribution of this Merger Prospectus may be subject to restrictions imposed by law (such as registration, admission, qualification and other regulations). No Merger Consideration Shares have been, or will be, registered under the United States Securities Act of 1933, as amended (the “U.S. Securities Act”) or the securities laws of any state of the United States (as such term is defined in Regulation S under the U.S. Securities Act) and may not be offered, sold or delivered, directly or indirectly, in or into the United States absent registration, except pursuant to an exemption from, or in a transaction not subject to, the registration requirements of the U.S. Securities Act and in compliance with any applicable state and other securities laws of the United States. This Merger Prospectus does not constitute an offer to sell or solicitation of an offer to buy any of the shares in the United States. In addition to Finland, Norway and the United States, no action has been or will be taken by Altia or Arcus to permit the possession or distribution of the Merger Prospectus (or any other offering or publicity materials or application form(s) relating to the Merger) in any jurisdiction where such distribution may otherwise lead to a breach of any law or regulatory requirement. Altia advises persons into whose possession this Merger Prospectus comes to inform themselves of and observe all possible applicable restrictions. The Merger Consideration Shares will be offered and sold in the United States in connection with the Merger in reliance upon the exemption from the registration requirements of the U.S. Securities Act provided by Rule 802 thereunder, see “Certain Matters – Notice to Shareholders in the United States” on pages 54–55 below.

Neither the Merger Prospectus, any notification nor any other merger material may be distributed or published in any jurisdiction except under circumstances that will result in compliance with any applicable laws and regulations. ▇▇▇▇▇▇▇ ▇▇▇▇▇, ▇▇▇▇▇ nor financial advisors of Altia and ▇▇▇▇▇ accept any legal responsibility for persons who have obtained the Merger Prospectus in violation of these restrictions, irrespective of whether these persons are prospective recipients of the Merger Consideration Shares. No actions have been taken to register or qualify the Merger Consideration Shares for public offer in any jurisdiction other than Finland, Norway and the United States.

Any disputes arising in connection with this Merger Prospectus will be settled exclusively by a court of competent jurisdiction in Finland. Investors must not construe the contents of this Merger Prospectus as legal, investment or tax advice. Each investor should consult such investor’s own counsel, accountant or business advisor as to legal, investment and tax advice and related matters pertaining to the Merger.

Nordea Bank Abp is acting exclusively for Altia in connection with the Merger and for no one else and will not be responsible to anyone other than Altia for providing the protections afforded to its clients or for providing advice in relation to the Merger. ABG Sundal ▇▇▇▇▇▇▇ ▇▇▇ is acting exclusively for Arcus in connection with the Merger and for no one else and will not be responsible to anyone other than Arcus for providing the protections afforded to its clients or for providing advice in relation to the Merger.

ii

TABLE OF CONTENT

| IMPORTANT INFORMATION | ii |

| TABLE OF CONTENT | iii |

| SUMMARY | 1 |

| TIIVISTELMÄ | 10 |

| RISK FACTORS | 19 |

| Risks Related to the Merger | 19 |

| Risks Related to the Combined Company’s Operating Environment | 23 |

| Risks Related to the Highly Regulated Nordic Alcohol Market | 26 |

| Risks Related to the Combined Company’s Business | 29 |

| Risks Related to Financial Position and Financing | 41 |

| Risks Related to the Shares in the Combined Company | 45 |

| Risks Related to the Delivery of the Merger Consideration Shares and the Listing on Oslo Børs | 46 |

| COMPANIES, BOARD OF DIRECTORS, AUDITORS AND ADVISERS | 49 |

| CERTAIN MATTERS | 51 |

| CERTAIN IMPORTANT DATES | 56 |

| EXCHANGE RATES | 57 |

| MERGER OF ALTIA AND ARCUS | 58 |

| INFORMATION ON THE COMBINED COMPANY | 70 |

| ALTIA’S CAPITALISATION AND INDEBTEDNESS | 74 |

| SELECTED CONSOLIDATED FINANCIAL INFORMATION | 76 |

| UNAUDITED PRO FORMA FINANCIAL INFORMATION | 90 |

| INFORMATION ON ALTIA | 102 |

| Business of Altia | 102 |

| Overview of the Business | 102 |

| Business Strategy | 104 |

| Financial Targets | 104 |

| History | 105 |

| Altia’s Business Operations | 105 |

| Business segments | 110 |

| Investments | 112 |

| Property, Plant and Equipment | 112 |

| Intellectual Property | 112 |

| Sustainability | 112 |

| Organisation and Personnel | 114 |

| Material Agreements | 115 |

| Insurance | 116 |

| Legal Proceedings | 116 |

| Outlook and Trend Information | 117 |

| Overview of Disclosed Information over the Last 12 Months Relevant as at the Date of This Merger Prospectus | 122 |

| Altia’s Board of Directors, Management and Auditors | 122 |

| ▇▇▇▇▇’s Shares and Share Capital | 129 |

| Altia’s Ownership Structure | 130 |

| Altia’s Related Party Transactions | 130 |

| INFORMATION ON ARCUS | 132 |

| Business of Arcus | 132 |

iii

| Overview of the Business | 132 |

| Business strategy | 133 |

| Financial Targets | 134 |

| History | 135 |

| Business Areas | 135 |

| Investments | 137 |

| Properties, Plant and Equipment | 137 |

| Intellectual Property | 138 |

| Corporate Social Responsibility | 138 |

| Organisation and Personnel | 139 |

| Material Agreements | 140 |

| Insurance | 141 |

| Legal Proceedings | 141 |

| Outlook and Trend Information | 142 |

| Overview of Disclosed Information over the Last 12 Months Relevant as at the Date of This Merger Prospectus | 145 |

| Arcus’ Board of Directors, Management and Auditors | 145 |

| Arcus’ Shares and Share Capital | 150 |

| Arcus’ Ownership Structure | 151 |

| Arcus’ Related Party Transactions | 153 |

| SHAREHOLDER RIGHTS | 154 |

| THE FINNISH SECURITIES MARKETS | 158 |

| TAXATION | 162 |

| DOCUMENTS ON DISPLAY | 170 |

| DOCUMENTS INCORPORATED BY REFERENCE INTO THIS MERGER PROSPECTUS | 171 |

| ANNEX A – THE ARTICLES OF ASSOCIATION OF ALTIA | A-1 |

| ANNEX B – THE ARTICLES OF ASSOCIATION OF ARCUS | B-1 |

| ANNEX C – INDEPENDENT AUDITOR’S ASSURANCE REPORT ON THE COMPILATION OF PRO FORMA FINANCIAL INFORMATION INCLUDED IN THIS MERGER PROSPECTUS | C-1 |

| ANNEX D – MERGER PLAN | D-1 |

iv

SUMMARY

Introduction

This summary should be considered as an introduction to this Merger and Listing Prospectus (the “Merger Prospectus”). Any decision by an investor to invest in the securities issued by Altia Plc should be based on consideration of this Merger Prospectus as a whole. An investor could lose all or part of the invested capital. Where a claim relating to the information contained in this Merger Prospectus is brought before a court, the plaintiff investor might, under the national legislation of the member states, have to bear the costs of translating this Merger Prospectus before the legal proceedings are initiated. Civil liability attaches only to those persons who have tabled the summary including any translation thereof, but only if the summary is misleading, inaccurate, or inconsistent when read together with the other parts of this Merger Prospectus or where it does not provide, when read together with the other parts of this Merger Prospectus, key information in order to aid investors when considering whether to invest in the securities issued by Altia Plc.

The identity and contact details of the issuer are:

| Company | Altia Plc |

| Business identity code | 1505555-7 |

| Legal entity identifier (“LEI”) | 52990007AXNSS4PNX352 |

| Domicile | Helsinki, Finland |

| Registered office | ▇▇▇▇▇▇▇▇▇▇▇▇ ▇, ▇▇-▇▇▇▇▇ ▇▇▇▇▇▇▇▇, ▇▇▇▇▇▇▇ |

Altia’s shares are subject to trading on Nasdaq Helsinki Ltd (“Nasdaq Helsinki”) under the trading code “Altia” (ISIN code: FI4000292438).

The identity and contact details of the merging company are:

| Company | Arcus ASA |

| Business identity code | 987 470 569 |

| LEI | 213800Z4X87YPAKKS645 |

| Domicile | Nittedal, Norway |

| Registered office | ▇▇▇▇▇▇▇▇▇▇▇▇▇▇▇ ▇▇, ▇▇▇▇ ▇▇▇▇▇, ▇▇▇▇▇▇ |

Arcus’ shares are subject to trading on Oslo Børs under the ticker code “ARCUS” (ISIN code: NO0010776875).

Hereinafter, the term “Combined Company” refers to ▇▇▇▇▇ as of the date of registration of the execution of the merger of Altia and Arcus (the “Effective Date”).

The FIN-FSA has, in its capacity as competent authority under the Prospectus Regulation, approved the Merger Prospectus on 23 October 2020. The record number of the FIN-FSA’s approval of the Merger Prospectus is FIVA 49/02.05.04/2020. The FIN-FSA’s address is P.O. Box 103, FI-00101 Helsinki, Finland, its telephone number is ▇▇▇▇ ▇ ▇▇▇ ▇▇ and its email address is ▇▇▇▇▇▇▇▇@▇▇▇▇▇▇▇▇▇▇▇▇▇▇▇▇.▇▇.

Key Information on Altia and Arcus

Who is the Issuer of the Securities?

The issuer’s legal and commercial name is Altia Oyj in Finnish, Altia Abp in Swedish and Altia Plc in English. Altia is a Finnish public limited liability company organised under the laws of Finland and domiciled in Helsinki, Finland, and its LEI is 52990007AXNSS4PNX352.

Principal Activities

Altia is a leading Nordic alcoholic beverage company that operates in the wine and spirits markets in the Nordic countries, and has an existing presence in Estonia and Latvia.1 Altia also has production in Cognac, France. Altia produces, imports, markets, sells and distributes both own and partner brand beverages and exports alcoholic beverages to approximately 30 countries, most of which are in Europe, Asia and North America. Altia comprises three business segments: Finland & Exports, Scandinavia and Altia Industrial. The Finland & Exports and Scandinavia segments comprise importing, sale and marketing of wine, spirits and other beverage product categories. Within the Finland & Exports segment Altia operates in

_________________________

1 The Company has a leading position in the combined Nordic wine and spirits sector as well as in Finland measured in volume.

1

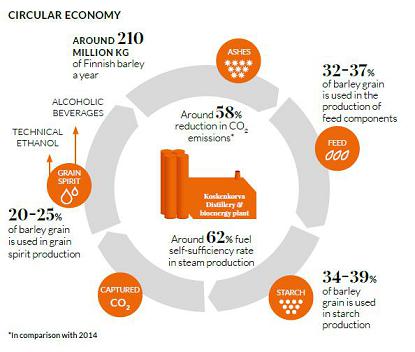

Finland, the Baltics and travel retail channels and conducts exports. Within the Scandinavia segment Altia operates in Sweden, Norway and Denmark. The Altia Industrial segment comprises Altia’s production of grain spirit and technical ethanol, starch and feed component, logistics, procurement and manufacturing operations as well as contract services.

Major Shareholders

The following table sets forth the ten largest shareholders of Altia that appear in the shareholder register maintained by Euroclear Finland Oy (“Euroclear Finland”) as at 21 October 2020:

| Shareholder | Number of Shares | Percent of shares and votes | ||||||

| Valtion Kehitysyhtiö Vake Oy1) | 13,097,481 | 36.24 | ||||||

| Ilmarinen Mutual Pension Insurance Company | 1,113,300 | 3.08 | ||||||

| Varma Mutual Pension Insurance Company | 1,050,000 | 2.91 | ||||||

| WestStar Oy | 655,566 | 1.81 | ||||||

| Veritas Pension Insurance Company Ltd. | 420,000 | 1.16 | ||||||

| FIM ▇▇▇▇▇ Sijoitusrahasto | 151,025 | 0.42 | ||||||

| Säästöpankki Kotimaa | 150,000 | 0.42 | ||||||

| ▇▇▇▇▇▇ and ▇▇▇▇▇▇ ▇▇▇▇▇▇▇▇▇´s Foundation | 140,200 | 0.39 | ||||||

| Mandatum Life Insurance Company Limited | 138,798 | 0.38 | ||||||

| Sijoitusrahasto Visio Allocator | 123,012 | 0.34 | ||||||

| Other shareholders including nominee-registered shareholders | 19,101,103 | 52.85 | ||||||

| Total Shares in the Company | 36,140,485 | 100.00 | ||||||

________

1) The State Business Development Company Vake Oy is wholly-owned by the State of Finland.

To the extent known to Altia, Altia is not, directly or indirectly, owned or controlled by any one person. ▇▇▇▇▇ is not aware of any arrangements that may lead to a change of control in Altia.

Chief Executive Officer and Executive Management Team

The following table sets forth the members of ▇▇▇▇▇’s Executive Management Team as at the date of this Merger Prospectus:

Name |

Year of birth | Position | Appointed |

| ▇▇▇▇▇ ▇▇▇▇▇▇▇ | 1969 | CEO | 2014 |

| ▇▇▇▇▇ ▇▇▇▇▇▇▇▇▇ | 1970 | Senior Vice President, Scandinavia | 2017 (member of the Executive Management Team since 2015) |

| ▇▇▇▇ ▇▇▇▇▇▇▇▇ | 1963 | Senior Vice President, Finland & Exports | 2017 |

| ▇▇▇▇▇ ▇▇▇▇▇▇▇ | 1963 | Senior Vice President, HR | 2016 |

| ▇▇▇▇▇ ▇▇▇▇▇▇▇ | 1970 | Senior Vice President, Marketing | 2016 |

| ▇▇▇▇▇ ▇▇▇▇▇▇▇▇ | 1958 | Senior Vice President, Altia Industrial | 2009 (member of the Executive Management Team since 2008) |

Statutory Auditor

Altia’s statutory auditor is PricewaterhouseCoopers Oy, Authorised Public Accountants, with Authorised Public Accountant ▇▇▇▇ ▇▇▇▇▇▇▇▇ as the auditor with principal responsibility. ▇▇▇▇ ▇▇▇▇▇▇▇▇ is registered in the register of auditors referred in Section 9 of Chapter 6 of the Auditing Act (1141/2015, as amended).

What Is the Key Financial Information Regarding the Issuer?

The following tables present selected consolidated financial information of Altia as at and for the six months period ended 30 June 2020, and 30 June 2019, and as at and for the financial year ended 31 December 2019. The selected consolidated financial information presented below has been derived from ▇▇▇▇▇’s unaudited consolidated half-year financial report as at and for the six months ended 30 June 2020 prepared in accordance with “IAS 34 – Interim Financial Reporting”, including the unaudited comparative financial information for the six months ended 30 June 2019, and ▇▇▇▇▇’s audited consolidated financial statements as at and for the year ended 31 December 2019, prepared in accordance with IFRS as adopted by the EU, all of which are incorporated by reference into this Merger Prospectus.

2

The following tables set forth a summary of ▇▇▇▇▇’s key financial information as at the dates and for the periods indicated:

|

As at and for the six months ended 30 June |

As at and for the year ended 31 December | ||

| In EUR million, unless otherwise indicated |

2020 |

2019 |

2019 |

| (unaudited) | (audited, unless otherwise indicated) | ||

| Income statement and statement of comprehensive income | |||

| Net sales | 149.3 | 165.0 | 359.6 |

| Operating result | 9.2 | 4.5 | 25.1 |

| Comparable EBITDA | 18.8 | 13.7 | 44.8 |

| Comparable EBITDA margin, % | 12.6 | 8.3 | 12.41) |

| Result for the period | 7.5 | 4.0 | 18.4 |

| Earnings per share (basic and diluted), EUR | 0.21 | 0.11 | 0.51 |

| Balance sheet | |||

| Total assets | 428.9 | 387.7 | 400.2 |

| Total equity | 149.5 | 137.6 | 151.2 |

| Net debt | 29.9 | 81.3 | 28.91) |

| Statement of cash flows | |||

| Net cash flow from operating activities | 10.3 | -4.0 | 52.6 |

| Net cash flow from investing activities | -1.3 | -2.2 | -6.0 |

| Net cash flow from financing activities | 29.9 | -7.4 | -23.9 |

| ________________ | |||

| 1) Unaudited. | |||

There are no qualifications in the audit report relating to ▇▇▇▇▇’s audited consolidated financial statement as at and for the year ended 31 December 2019.

Who is the Merging Company?

The merging company's legal and commercial name is Arcus ASA. Arcus is a Norwegian public limited liability company organised under the laws of Norway and domiciled in Nittedal, Norway, and its LEI is 213800Z4X87YPAKKS645.

Principal Activities

▇▇▇▇▇ is a leading Nordic player in the production, import, sale and distribution of wine and spirits2. Arcus is represented in all Nordic countries, with subsidiary companies in Norway, Sweden, Denmark and Finland, as well as in Germany. Arcus has further exports of spirits to markets outside the Nordic region and Germany, most importantly to the United States. Arcus has three business segments, Wine, Spirits and Logistics. Within the business segment Wine, Arcus offers wines in all price brackets. The majority of the wine portfolio is comprised of a wide variety of partner brands supplied by a large number of international producers, and a limited, but growing, share of the portfolio are Arcus’ own brands that have been developed in-house, specifically customised to target local market preferences in each individual market. Within the business segment Spirits, Arcus’ portfolio consists of iconic Arcus brands with long histories and heritage, as well partner brands. The Spirits business segment is managed from Norway, with the exception of certain Danish brands (Aalborg and ▇▇▇▇▇▇ Dansk) which are managed locally but with support from Norway and other countries. The business segment Logistics, operating externally under the Vectura name, is Arcus’ logistics service provider in the Norwegian market.

Major Shareholders

Shareholders owning 5 percent or more of the shares in Arcus have an interest in Arcus’ share capital which is notifiable pursuant to the Norwegian Securities Trading Act. The following table sets forth shareholders owning 5 percent or more of the shares in Arcus, as registered in the Norwegian Central Securities Depositary as of 21 October 2020.

| Shareholder | Number of shares | Percent of shares and votes | ||||||

| Canica AS | 30,093,077 | 44.2 | % | |||||

| Geveran Trading Co Ltd | 6,750,000 | 9.9 | % | |||||

| Other shareholders including nominee-registered shareholders | 31,180,178 | 45.8 | % | |||||

| Total Shares in the Company | 68,023,255 | 100.0 | % | |||||

__________________________

2 Based on sales data from Vinmonopolet (Norway), Systembolaget (Sweden), Alko (Finland) and Nielsen (Denmark).

3

To the extent known to Arcus, Arcus is not, directly or indirectly, owned or controlled by any one person. ▇▇▇▇▇ is not aware of any arrangements that may lead to a change of control in Arcus

Chief Executive Officer and Management Team

The following table sets forth the members of Arcus’ Group Management Team as at the date of this Merger Prospectus:

Name |

Position | Appointed |

| ▇▇▇▇▇▇▇ ▇▇▇▇▇▇ | Group CEO | 2015 |

| ▇▇▇▇▇▇▇ ▇▇▇▇ | Group CFO | 2016 |

| ▇▇▇▇▇▇ ▇▇▇▇▇▇▇▇▇▇ | Group Director Spirits | 2016 |

| ▇▇▇▇▇ ▇▇▇▇▇▇▇▇ | Group Director Wine, Managing Director Vingruppen AS (Wine Norway) | 2018 |

| ▇▇▇▇▇▇ ▇▇▇▇▇▇▇ | Managing Director Vingruppen i ▇▇▇▇▇▇ ▇▇ (Wine Sweden) | 2018 |

| ▇▇▇▇▇ ▇▇▇▇▇▇ | Managing Director Vingruppen Oy (Wine Finland) | 2020 |

| ▇▇▇▇▇ ▇▇▇▇▇▇▇▇ | Group Director Production | 2020 |

| ▇▇▇▇ ▇▇▇▇ | Group Director CSR, Group Technical Services | 2018 |

| ▇▇▇-▇▇▇▇ ▇▇▇▇▇▇ | Group Director HR | 2019 |

| ▇▇▇ ▇▇▇▇▇▇▇ | Group Director IR and Communications | 2013 |

| ▇▇▇▇ ▇▇▇▇▇▇▇ | Managing Director Vectura AS | 2019 |

Statutory Auditor

Arcus’ statutory auditor is ▇▇▇▇▇ & ▇▇▇▇▇ AS with Authorised Public Accountant ▇▇▇▇▇▇ ▇▇▇▇▇▇▇ as the auditor with principal responsibility. ▇▇▇▇▇ & Young AS is a member of the Norwegian Institute of Public Accountants.

What Is the Key Financial Information Regarding the Merging Company?

The following tables present selected consolidated financial information of Arcus as at and for the six months period ended 30 June 2020 and 30 June 2019, and as at and for the financial year ended 31 December 2019. The selected consolidated financial information presented below has been derived from Arcus’ unaudited consolidated half-year financial report as at and for the six months ended 30 June 2020 prepared in accordance with “IAS 34 – Interim Financial Reporting”, including the unaudited comparative financial information for the six months ended 30 June 2019, and ▇▇▇▇▇’ audited consolidated financial statements as at and for the year ended 31 December 2019, prepared in accordance with IFRS as adopted by the EU, all of which are incorporated by reference into this Merger Prospectus.

The following tables set forth a summary of Arcus key financial information as at the dates and for the periods indicated:

4

|

As at and for the six months ended 30 June |

As at and for the year ended 31 December | ||

| In NOK million, unless otherwise indicated |

2020 |

2019 |

2019 |

| (unaudited) | (audited) | ||

| Income statement | |||

| Total operating revenue | 1,378 | 1,250 | 2,763 |

| Adjusted EBITDA | 186 | 129 | 397 |

| Adjusted EBITDA margin % | 13.5% | 10.3% | 14.4% |

| Adjusted operating result (EBIT) | 123 | 75 | 277 |

| Adjusted operating margin % | 8.9% | 6.0% | 10.0% |

| Result for the period | 82 | 8 | 133 |

| Earnings per share (NOK) | 1.19 | 0.11 | 1.94 |

| Diluted earnings per share (NOK) | 1.12 | 0.11 | 1.85 |

| Balance sheet | |||

| Total assets | 6,011 | 4,991 | 5,590 |

| Total equity | 1,741 | 1,521 | 1,662 |

| Total liabilities | 4,270 | 3,470 | 3,928 |

| Statement of cash flows | |||

| Net cash flow from operating activities | 519 | -131 | 292 |

| Net cash flow from investing activities | -24 | -7 | -71 |

| Net cash flow from financing activities | -84 | -198 | -284 |

Unaudited Pro Forma Financial Information

The unaudited pro forma financial information (“Pro Forma Information”) is presented to illustrate the effect to the Merger of Altia and Arcus to Altia’s financial information as if the Merger had been undertaken at an earlier date. The Pro Forma Information has been presented for illustrative purposes only and, therefore, the hypothetical financial position and results of operations therein may differ from the Combined Company’s actual financial position and results of operations. In addition, the unaudited pro forma financial information does not reflect any cost savings, synergy benefits or future integration costs that are expected to be generated or may be incurred as a result of the Merger. The unaudited pro forma income statements for the six months ended 30 June 2020 and for the year ended 31 December 2019 give effect to the Merger as if it had occurred on 1 January 2019. The unaudited pro forma balance sheet as at 30 June 2020 gives effect to the Merger as if it had occurred on that date.

The Pro Forma Information has been compiled in accordance with the Annex 20 to the Commission Delegated Regulation (EU) 2019/980 and on a basis consistent with the accounting principles applied by Altia in its consolidated financial statements prepared in accordance with IFRS. The Merger will be accounted for as a business combination at consolidation using the acquisition method of accounting under the provisions of IFRS with Altia determined as the acquirer of Arcus.

The Pro Forma Information reflects adjustments to historical financial information to give pro forma effect to events that are directly attributable to the Merger and which are factually supportable. The pro forma adjustments include certain assumptions related to the fair value of purchase consideration, the purchase price allocation, accounting policy alignments and other adjustments, which are considered to be reasonable under the circumstances. Considering the ongoing regulatory approval processes which restricts ▇▇▇▇▇’s access to detailed data of Arcus, the pro forma adjustments presented are preliminary and based on information available at this time, thus subject to change among others due to that the final fair value of the purchase consideration will be determined based on the share price as at the Effective Date, the final purchase price allocation will be based on the fair values of Arcus’ assets acquired and liabilities assumed on the Effective Date and detailed review of Arcus’ accounting policies and financial statements presentation differences can only be done after the Effective Date.

There can be no assurance that the assumptions used in the preparation of the Pro Forma Information will prove to be correct and the final impact of the Merger to the financial information of Altia may materially differ from the pro forma adjustments reflected in the Pro Forma Information. Further, the accounting policies to be applied by the Combined Company in the future may differ from the accounting policies applied in the Pro Forma Information.

The following table set forth a summary of key figures relating to Pro Forma Information as at the dates and for the periods indicated:

5

| As at and for the six months ended 30 June 2020 | For the year ended 31 December 2019 | |||||||||||||||||||||||||||||||

| In EUR million, unless otherwise indicated | Altia historical | Arcus reclassified | Merger | Combined Company pro forma | Altia historical | Arcus reclassified | Merger | Combined Company pro forma | ||||||||||||||||||||||||

| Net sales | 149.3 | 127.2 | — | 276.5 | 359.6 | 280.4 | — | 640.0 | ||||||||||||||||||||||||

| Comparable EBITDA | 18.8 | 17.4 | — | 36.1 | 44.8 | 39.9 | — | 84.7 | ||||||||||||||||||||||||

| EBITDA | 18.0 | 15.7 | 1.1 | 34.8 | 43.1 | 37.9 | -25.4 | 55.6 | ||||||||||||||||||||||||

| Operating result | 9.2 | 9.9 | -0.5 | 18.6 | 25.1 | 25.8 | -29.1 | 21.8 | ||||||||||||||||||||||||

| Result for the period | 7.5 | 7.6 | -0.1 | 14.9 | 18.4 | 13.5 | -24.7 | 7.2 | ||||||||||||||||||||||||

| Earnings per share – basic, EUR | 0.22 | 0.10 | ||||||||||||||||||||||||||||||

| Total assets | 428.9 | 550.9 | 95.8 | 1,075.6 | ||||||||||||||||||||||||||||

| Total equity | 149.5 | 159.6 | 106.0 | 415.1 | ||||||||||||||||||||||||||||

| Net debt | 211.2 | |||||||||||||||||||||||||||||||

| Gearing, % | 50.9 | |||||||||||||||||||||||||||||||

Equity ratio, % | 38.6 | |||||||||||||||||||||||||||||||

What are the Key Risks that Are Specific to the Combined Company?

| · | There is no certainty that the Merger will be completed, or the completion may be delayed; |

| · | the Merger may not necessarily be completed in the manner currently contemplated, which could have a material adverse effect on the estimated benefits of the Merger or the market price of the shares in Altia and/or Arcus; |

| · | uncertain global economic, political and financial market conditions could have a material adverse effect on the Combined Company’s business, financial condition and results of operations; |

| · | the Combined Company operates in a very competitive industry and intensifying competition could have a material adverse effect on the Combined Company’s business; |

| · | changes to legislation regarding state-owned retail monopolies in the Combined Company’s core markets could have a negative impact on the Combined Company’s business; |

| · | increases in taxes, particularly increases to excise taxes, could adversely affect demand for the Combined Company’s products; |

| · | the Combined Company may be unsuccessful in fulfilling its strategy or the strategy itself may be unsuccessful, which may lead to the Combined Company not being able to achieve its financial targets and the actual results of operations may differ materially from the financial targets included in this Merger Prospectus; |

| · | the Combined Company is dependent on the supply of high-quality Finnish grain and Norwegian potato spirits, and changes in the prices or availability of grain and potato spirits or other raw materials, wine, eau-de-vie, supplies and finished products could have an adverse effect on the Combined Company’s business; |

| · | loss of agreements, unfavourable agreement terms or weakening of the relationships between the Combined Company and the key partners, customers, suppliers and distributors could affect the Combined Company’s business negatively; |

| · | failures in tender processes, in fulfilling requirements to maintain a product ranking or other requirements related to assortments could affect the Combined Company’s business adversely; |

| · | the Combined Company’s business may be adversely affected by disruptions and damage in its production and storage plants; and |

| · | difficulties in accessing additional financing or complying with financial covenants included in the Combined Company’s credit facilities as well as increases in costs of financing could have an adverse effect on the Combined Company’s financial condition and results of operations. |

6

Key Information on the Securities

What Are the Main Features of the Securities?

As at the date of this Merger Prospectus, ▇▇▇▇▇’s registered share capital is EUR 60,480,378.36 and the number of shares issued is 36,140,485. Altia’s shares have no nominal value, are denominated in euro and all shares issued have been paid in full and issued in accordance with Finnish laws. Altia has one class of shares, the ISIN code of which is FI4000292438.

The shareholders of Arcus shall receive as merger consideration 0.4618 new shares in Altia (the “Merger Consideration Shares”) for each share owned by them in Arcus (the “Merger Consideration”). The Merger Consideration Shares correspond to the existing share class in Altia. Each Merger Consideration Share entitles to one vote at the General Meetings of Altia and all Merger Consideration Shares provide equal rights to dividend and other distributable funds of Altia, including the distribution of Altia’s assets in dissolution. There are no voting restrictions related to the Merger Consideration Shares and they are freely transferrable.

The rights attached to the Merger Consideration Shares are determined by the Finnish Companies Act (624/2006, as amended) (the “Companies Act”) and other applicable Finnish regulation and include, among other things, a pre-emptive right to subscribe for new shares in the Combined Company, right to attend and vote at the General Meetings of the Combined Company, right to dividend and other distributions of equity, and other rights under the Companies Act.

The dividends paid and other unrestricted equity distributed by Altia or Arcus for previous financial years are not an indication of the dividends to be paid by the Combined Company in the future, if any. There can be no assurance that the Combined Company will distribute any dividends or unrestricted equity in the future. The Combined Company will determine its dividend policy after the Effective Date and annually assess the preconditions for distributing dividend or other unrestricted equity.

Where Will the Securities Be Traded?

Altia shall apply for the listing of the Merger Consideration Shares to be issued by Altia to public trading on Nasdaq Helsinki. The listing of and trading in the Merger Consideration Shares shall begin on the Effective Date or as soon as reasonably possible thereafter.

Altia and Arcus will seek to ensure that primarily, the Combined Company’s Shares through a depository interest arrangement, or secondarily, the depository receipts or directly-held Shares in the Combined Company will be subject to a secondary listing on the Oslo Børs in connection with the completion of the Merger or as soon as possible thereafter, for a transitional period of four (4) months from the first day of the secondary listing on the Oslo Børs, after which the Combined Company’s Shares through a depository interest arrangement or depository receipts or directly-held Shares in the Combined Company shall be delisted from the Oslo Børs. The Board of Directors of the Combined Company is instructed to implement the delisting by separate application to the Oslo Børs. The trading in the shares of Arcus on Oslo Børs is expected to end at the end of the last trading day preceding the Effective Date and the shares in Arcus are expected to cease to be listed on Oslo Børs as of the Effective Date, at the latest.

What Are the Key Risks that Are Specific to the Securities?

· The market price of the Shares may fluctuate considerably, which may result in investors losing all or part of their invested capital;

| · | The listing on the Oslo Børs may not succeed as expected or the listing may not take place at all; and |

| · | The Merger Consideration Shares are expected to be delivered through a depository interest arrangement, which means that the Arcus shareholders receiving the Merger Consideration Shares will be considered nominee-registered shareholders, and may also involve additional bureaucratic burden and costs as well as risks relating to the trading in the Merger Consideration Shares. |

7

Key Information on the Offer of Securities to the Public and the Admission to Trading on a Regulated Market

Why Is This Merger Prospectus Being Produced?

This Merger Prospectus has been prepared and published by Altia for the purposes of offering Merger Consideration Shares to the shareholders of Arcus and applying for the Listing and the temporary secondary listing on the Oslo Børs as described above in “Key Information on the Securities – Where Will the Securities Be Traded?”.

The Combined Company will be named Anora Group Oyj in Finnish (in Swedish Anora Group Abp, and in English Anora Group Plc). The Combined Company’s preliminary aggregated annual revenue is EUR 640 million and it will employ approximately 1,100 professionals around the Nordics and Baltics. With corporate and management functions across the Nordics, the Combined Company will have its legal domicile in Helsinki, Finland and headquarters in Helsinki.

The Combined Company will offer a unique portfolio of iconic local, regional, and global brands and have a strong foothold in the Nordic markets making it an attractive partner with its superior pan-Nordic route-to-market. With a solid combined cash flow, the Combined Company is well positioned for stronger international expansion. The Combined Company will continue Altia’s and ▇▇▇▇▇’ targeted work to improve sustainable production, and to develop a modern and responsible drinking culture.

The Merger will form a wine and spirits brand house with a leading presence across the Nordics with existing presence also in the Baltics. The Combined Company will have a unique portfolio of iconic local, regional and global wine and spirits brands. This, combined with deep consumer insights and strong innovation capabilities will enable the Combined Company to achieve growth and meet changing consumer needs even better. The Combined Company will offer a one-stop shop for customers both in on- and off-trade. Further, its wide distribution presence in the complex Nordic markets and enhanced sales excellence, will make the Combined Company an even more attractive partner.

The Merger will allow the Combined Company to strive for growth and more powerful product launches both in and outside the Nordics. The Combined Company’s attractive brand portfolio has significant export potential. With a strong combined cash flow, the Combined Company will be a competitive Northern European player able to seek further growth also through targeted M&A.

There will be no proceeds accruing from the issuance of the Merger Consideration Shares to the Combined Company.

ABG Sundal ▇▇▇▇▇▇▇ ▇▇▇ and Nordea Bank Abp acting as the financial advisers, as well as other entities within the same groups, have provided to Altia and Arcus, and may provide to the Combined Company in the future, investment or other banking services in the ordinary course of their business.

The total costs estimated to be incurred by Altia and Arcus in connection with the Merger primarily comprise financial, legal and advisory costs and amount to approximately EUR 21.8 million (excluding financing transaction costs). Certain members of management of Altia and Arcus are, in accordance with customary practice, entitled to remuneration, which shall be paid due to the Merger (a part of which is to be paid only upon a successful completion of the Merger), amounting to approximately EUR 7.3 million in aggregate and which is included in the aforementioned total costs incurred in connection with the Merger. No expenses are charged by ▇▇▇▇▇ or ▇▇▇▇▇ from their respective shareholders in relation to the Merger.

Under which Conditions and Timetable can I Invest in this Security?

The Boards of Directors of Altia and Arcus have, on 29 September 2020, signed a combination agreement (the “Combination Agreement”) concerning the combination of their business operations and a merger plan (the “Merger Plan”), according to which Arcus shall be merged into Altia through a statutory cross-border absorption merger in such a manner that all assets and liabilities of Arcus shall be transferred without a liquidation procedure to Altia (the “Merger”). The Boards of Directors of Altia and ▇▇▇▇▇ have on 2 October 2020 proposed that the Extraordinary General Meetings of Altia and Arcus, convened to be held on 12 November 2020, would resolve upon the Merger as set forth in the Merger Plan. The completion of the Merger is subject to, inter alia, approval by the Extraordinary General Meetings of Altia and Arcus, obtaining of necessary regulatory approvals, including merger control approvals by the relevant competition authorities, fulfilment of other conditions to completion set forth in the Combination Agreement and the Merger Plan or waiver of such conditions. Furthermore, it is required for the completion of the Merger that the Combination Agreement has not been terminated in accordance with its provisions, and that the execution of the Merger is registered with the trade register maintained by the Finnish Patent and Registration Office (the “Finnish Trade Register”). The Merger shall be completed on the date of registration of the execution of the Merger with the Finnish Trade Register (i.e. the Effective Date). The planned Effective Date is 1 April 2021 (effective registration time approximately at 00:01:01). The planned

8

Effective Date is not binding and the actual Effective Date may be earlier or later than above date. Arcus shall automatically dissolve on the Effective Date.

The Merger is based on an exchange ratio reflecting a relative value of Altia and ▇▇▇▇▇ of 53.5:46.5 (the “Exchange Ratio”). The shareholders of Arcus shall receive as Merger Consideration 0.4618 Merger Consideration Shares for each share owned in Arcus per each individual book-entry account. The Merger Consideration Shares shall be issued to the shareholders of Arcus in proportion to their shareholding in Arcus at a record date to be set in connection with completion of the Merger. No Consideration Shares will be issued with respect to shares in Arcus held by Arcus itself or by Altia.

On the date of this Merger Prospectus, the number of issued and outstanding shares in Arcus is 68,023,255, which includes 6,948 treasury shares. Based on the situation on the date of this Merger Prospectus and the agreed Exchange Ratio, the total number of shares in Altia to be issued as Merger Consideration would therefore be 31,409,930 shares. The final number of shares to be issued as Merger Consideration may be affected by, among others, any change concerning the number of shares issued by and outstanding in Arcus or held by Arcus as treasury shares, e.g., Arcus transferring existing treasury shares in accordance with existing share-based incentive plans, prior to the Effective Date.

In case the number of shares received by a shareholder of Arcus per each individual book-entry account as Merger Consideration is a fractional number, the fractions shall be rounded down to the nearest whole share for the purpose of determining the number of Merger Consideration Shares to be received by the relevant shareholder. Fractional entitlements to new shares of the Combined Company shall be aggregated and sold in public trading on Nasdaq Helsinki or the Oslo Børs and the proceeds shall be distributed to shareholders of Arcus entitled to receive such fractional entitlements in proportion to holding of such fractional entitlements. Any costs related to the sale and distribution of fractional entitlements shall be borne by Altia. With the exception of proceeds from the sale of possible fractional entitlements, no other cash consideration will be paid in connection with the Merger.

The Merger Consideration shall be distributed to the shareholders of Arcus on the Effective Date or as soon as reasonably possible thereafter. As the primary alternative, ▇▇▇▇▇ expects to deliver the Merger Consideration Shares through a depository interest arrangement in the VPS. As secondary alternatives the Merger Consideration Shares could be delivered as depository receipts registered in the VPS or as directly held Shares in the Combined Company in the book-entry securities system maintained by Euroclear Finland.

Altia and Arcus will seek a temporary secondary listing of the Combined Company on the Oslo Børs for a transitional period of four (4) months from the first day of the secondary listing on the Oslo Børs, and in case of such a listing the Combined Company shall facilitate the holding and trading of Shares by current shareholders of Arcus primarily through a depository interest arrangement in the VPS, secondarily as VPS-registered depository receipts or, if possible, direct registration of the Combined Company’s Shares in the VPS, which is currently not envisaged to be possible. In the event that depositary interest arrangements registered in the VPS, depositary receipts registered in the VPS or the Combined Company's Shares are not temporarily listed on the Oslo Børs, the Combined Company shall facilitate and cover the cost of any shareholders of Arcus who wish, within (3) months from the Effective Date to switch to holding shares registered in Euroclear Finland, whether through a nominee structure or other structure generally suitable for the current shareholder base.

9

TIIVISTELMÄ

Johdanto

Tätä tiivistelmää on pidettävä tämän sulautumis- ja listalleottoesitteen (”Sulautumisesite”) johdantona. Mahdollisten sijoittajien tulisi perustaa Altia Oyj:n arvopapereita koskevat sijoituspäätöksensä tähän Sulautumisesitteeseen kokonaisuutena. Sijoittaja voi menettää sijoittamansa pääoman kokonaan tai osittain. ▇▇▇ tuomioistuimessa pannaan vireille tähän Sulautumisesitteeseen sisältyviä tietoja koskeva ▇▇▇▇▇, kantajana toimiva sijoittaja voi jäsenvaltioiden kansallisen lainsäädännön mukaan joutua ▇▇▇▇▇ oikeudenkäynnin vireillepanoa vastaamaan tämän Sulautumisesitteen käännöskustannuksista. Siviilioikeudellista vastuuta sovelletaan henkilöihin, jotka ovat jättäneet tämän tiivistelmän, sen käännös mukaan luettuna, mutta vain ▇▇▇ tiivistelmä on harhaanjohtava, epätarkka tai epäjohdonmukainen suhteessa tämän Sulautumisesitteen muihin osiin ▇▇▇ ▇▇▇ siinä ei ▇▇▇▇▇▇ yhdessä tämän Sulautumisesitteen muiden osien kanssa keskeisiä tietoja sijoittajien auttamiseksi, kun he harkitsevat Altia Oyj:n arvopapereihin sijoittamista.

Liikkeeseenlaskija ▇▇ ▇▇▇ yhteystiedot:

| Yhtiö | Altia Oyj |

| Y-tunnus | 1505555-7 |

| Oikeushenkilötunnus (”LEI”) | 52990007AXNSS4PNX352 |

| Kotipaikka | Helsinki, Suomi |

| Rekisteröity toimipaikka | Kaapeliaukio 1, 00180 Helsinki, Suomi |

Altian osakkeet ovat julkisen kaupankäynnin kohteena Nasdaq Helsinki Oy:ssä (”Nasdaq Helsinki”) kaupankäyntitunnuksella ”ALTIA” (ISIN-koodi: FI4000292438).

Sulautuva yhtiö ▇▇ ▇▇▇ yhteystiedot:

| Yhtiö | Arcus ASA |

| Y-tunnus | 987 470 569 |

| LEI | 213800Z4X87YPAKKS645 |

| Kotipaikka | Nittedal, Norja |

| Rekisteröity toimipaikka | Destilleriveien 11, 1481 ▇▇▇▇▇, ▇▇▇▇▇ |

Arcuksen osakkeet ovat julkisen kaupankäynnin kohteena Oslo Børsissä kaupankäyntitunnuksella ”ARCUS” (ISIN-koodi: NO0010776875).

Jäljempänä termillä ”Yhdistynyt Yhtiö” viitataan Altiaan Altian ja ▇▇▇▇▇▇▇▇ sulautumisen täytäntöönpanon rekisteröinnin päivämäärästä eteenpäin (”Täytäntöönpanopäivä”).

Finanssivalvonta on Esiteasetuksen tarkoittamana toimivaltaisena viranomaisena hyväksynyt Sulautumisesitteen 23.10.2020. Finanssivalvonnan tämän Sulautumisesitteen hyväksymispäätöksen diaarinumero on FIVA 49/02.05.04/2020. Finanssivalvonnan osoite on ▇▇ ▇▇▇, ▇▇▇▇▇ ▇▇▇▇▇▇▇▇, ▇▇▇▇▇, puhelinnumero ▇▇▇▇ ▇ ▇▇▇ ▇▇ ja sähköpostiosoite ▇▇▇▇▇▇▇▇@▇▇▇▇▇▇▇▇▇▇▇▇▇▇▇▇.▇▇.

Keskeiset tiedot Altiasta ja Arcuksesta

▇▇▇▇▇▇▇▇▇ on arvopaperien liikkeeseenlaskija?

Liikkeeseenlaskijan virallinen nimi ja liiketoiminnassa käytettävä toiminimi on suomeksi Altia Oyj, ruotsiksi Altia Abp ja englanniksi Altia Plc. Altia on suomalainen Suomen lainsäädännön mukaan perustettu julkinen osakeyhtiö, jonka kotipaikka on Helsinki ▇▇ ▇▇▇ on 52990007AXNSS4PNX352.

Päätoimialat

Altia on johtava pohjoismainen alkoholijuomayhtiö, joka toimii viinien ja väkevien alkoholijuomien markkinoilla Pohjoismaissa, ▇▇ ▇▇▇▇▇ on olemassa oleva asema myös ▇▇▇▇▇ ▇▇ Latvian markkinoilla.3 Altialla on tuotantoa myös Cognacissa, Ranskassa. Altia valmistaa, maahantuo, markkinoi, myy ja jakelee omia brändejä ▇▇▇▇ päämiestuotteita ja vie alkoholijuomia noin 30 maahan, jotka sijaitsevat pääosin Euroopassa, Aasiassa ja Pohjois-Amerikassa. Altialla on kolme liiketoimintasegmenttiä: Finland & Exports, Scandinavia ja Altia Industrial. Finland & Exports ja Scandinavia -segmentit

___________________________

3 Yhtiöllä on johtava asema viinien ja väkevien alkoholijuomien yhteenlasketulla Pohjoismaisella sektorilla ▇▇▇▇ Suomessa volyymeissä mitattuna.

10

käsittävät viinien, väkevien alkoholijuomien ja muiden juomatuotteiden maahantuonnin, myynnin ja markkinoinnin. Altian Finland & Exports -segmentti toimii Suomessa, Baltian ▇▇▇▇▇▇ ▇▇ matkustajamyynnissä ▇▇▇▇ harjoittaa vientiä. Altian Scandinavia-segmentti toimii Ruotsissa, Norjassa ja Tanskassa. Altia Industrial -segmentti vastaa Altian viljaviinan, teknisen etanolin, tärkkelyksen ja rehuraaka-aineen tuotannosta, logistiikasta, hankinnasta ja valmistustoiminnasta ▇▇▇▇ sopimuspalveluista.

Suurimmat osakkeenomistajat

Seuraavassa taulukossa esitetään Altian kymmenen suurinta Euroclear Finland Oy:n (”Euroclear Finland”) ylläpitämään osakasluetteloon 21.10.2020 rekisteröityä osakkeenomistajaa:

| Osakkeenomistajat | Osakkeiden lukumäärä | Prosenttia osakkeista ja äänistä | ||||

| Valtion Kehitysyhtiö Vake Oy1) | 13 097 481 | 36,24 | ||||

| Keskinäinen Eläkevakuutusyhtiö Ilmarinen | 1 113 300 | 3,08 | ||||

| Keskinäinen työeläkevakuutusyhtiö Varma | 1 050 000 | 2,91 | ||||

| WestStar Oy | 655 566 | 1,81 | ||||

| Eläkevakuutusosakeyhtiö Veritas | 420 000 | 1,16 | ||||

| FIM ▇▇▇▇▇ Sijoitusrahasto | 151 025 | 0,42 | ||||

| Säästöpankki Kotimaa | 150 000 | 0,42 | ||||

| ▇▇▇▇▇▇ ▇▇ ▇▇▇▇▇▇ ▇▇▇▇▇▇▇▇▇▇▇ ▇▇▇▇▇▇ | 140 200 | 0,39 | ||||

| Mandatum Henkivakuutusosakeyhtiö | 138 798 | 0,38 | ||||

| Sijoitusrahasto Visio Allocator | 123 012 | 0,34 | ||||

| Muut osakkeenomistajat, mukaan lukien hallintarekisteröityjen osakkeiden omistajat | 19 101 103 | 52,85 | ||||

| Yhtiön osakkeet yhteensä | 36 140 485 | 100,00 | ||||

1) Valtion Kehitysyhtiö Vake Oy on Suomen valtion kokonaan omistama.

▇▇▇▇▇ ▇▇▇▇ kuin Altia on tietoinen, Altia ei ole suoraan tai välillisesti kenenkään yhden henkilön omistuksessa tai määräysvallassa. Altian tiedossa ei ole järjestelyjä, jotka voisivat johtaa määräysvallan siirtymiseen Altiassa.

Toimitusjohtaja ja johtoryhmä

Seuraavassa taulukossa esitetään Altian johtoryhmän jäsenet tämän Sulautumisesitteen päivämääränä:

Nimi |

Syntymävuosi | Asema | Nimitetty |

| ▇▇▇▇▇ ▇▇▇▇▇▇▇ | 1969 | Toimitusjohtaja | 2014 |

| ▇▇▇▇▇ ▇▇▇▇▇▇▇▇▇ | 1970 | Senior Vice President, Scandinavia | 2017 (johtoryhmän ▇▇▇▇▇ vuodesta 2015) |

| ▇▇▇▇ ▇▇▇▇▇▇▇▇ | 1963 | Senior Vice President, Finland & Exports | 2017 |

| ▇▇▇▇▇ ▇▇▇▇▇▇▇ | 1963 | Senior Vice President, HR | 2016 |

| ▇▇▇▇▇ ▇▇▇▇▇▇▇ | 1970 | Senior Vice President, Marketing | 2016 |

| ▇▇▇▇▇ ▇▇▇▇▇▇▇▇ | 1958 | Senior Vice President, Altia Industrial | 2009 (johtoryhmän ▇▇▇▇▇ vuodesta 2008) |

Lakisääteinen tilintarkastaja

Altian lakisääteinen tilintarkastaja on tilintarkastusyhteisö PricewaterhouseCoopers Oy, ja päävastuullisena tilintarkastajana on KHT ▇▇▇▇ ▇▇▇▇▇▇▇▇. ▇▇▇▇ ▇▇▇▇▇▇▇▇ on rekisteröity tilintarkastuslain (1141/2015, muutoksineen) 6 luvun 9 §:n tarkoittamaan tilintarkastajarekisteriin.

Mitkä ovat liikkeeseenlaskijan keskeiset taloudelliset tiedot?

Seuraavissa taulukoissa esitetään Altian valikoituja konsernitilinpäätöstietoja 30.6.2020 ja 30.6.2019 päättyneiltä kuuden kuukauden jaksoilta ▇▇▇▇ 31.12.2019 päättyneeltä tilikaudelta. Alla esitettävät valikoidut konsernitilinpäätöstiedot ovat peräisin ”IAS 34 – Osavuosikatsaukset” -standardin mukaisesti 30.6.2020 päättyneeltä kuuden kuukauden jaksolta laaditusta Altian tilintarkastamattomasta puolivuosikatsauksesta, ja niihin sisältyy vertailutietoina esitetyt tilintarkastamattomat konsernin taloudelliset tiedot 30.6.2019 päättyneeltä kuuden kuukauden jaksolta ja EU:n käyttöön ottamien IFRS-standardien mukaisesti 31.12.2019 päättyneeltä tilikaudelta laadittu Altian tilintarkastettu konsernitilinpäätös, jotka on sisällytetty tähän Sulautumisesitteeseen viittaamalla.

11

Seuraavissa taulukoissa esitetään yhteenveto Altian keskeisistä taloudellisista tiedoista ilmoitettuina ajankohtina ja ajanjaksoina:

|

1.1.–30.6. ja 30.6. |

1.1.–31.12. ja 31.12. | ||

| Milj. euroa, ellei toisin ilmoitettu |

2020 |

2019 |

2019 |

| (tilintarkastamaton) | (tilintarkastettu, ellei toisin ole ilmoitettu) | ||

| Tuloslaskelma ▇▇ ▇▇▇▇▇ tuloslaskelma | |||

| Liikevaihto | 149,3 | 165,0 | 359,6 |

| Liiketulos | 9,2 | 4,5 | 25,1 |

| Vertailukelpoinen käyttökate | 18,8 | 13,7 | 44,8 |

| Vertailukelpoinen käyttökateprosentti | 12,6 | 8,3 | 12,41) |

| Kauden tulos | 7,5 | 4,0 | 18,4 |

| Osakekohtainen tulos (laimentamaton ja laimennusvaikutuksella oikaistu), euroa | 0,21 | 0,11 | 0,51 |

| Tase | |||

| Varat yhteensä | 428,9 | 387,7 | 400,2 |

| Oma pääoma yhteensä | 149,5 | 137,6 | 151,2 |

| Nettovelka | 29,9 | 81,3 | 28,91) |

| Rahavirtalaskelma | |||

| Liiketoiminnan nettorahavirta | 10,3 | -4,0 | 52,6 |

| Investointien nettorahavirta | -1,3 | -2,2 | -6,0 |

| Rahoituksen nettorahavirta | 29,9 | -7,4 | -23,9 |

| ____________________________________ | |||

| 1) Tilintarkastamaton. | |||

Tilintarkastuskertomuksessa ei ole Altian 31.12.2019 päättyneen tilikauden tilintarkastettuun konsernitilinpäätökseen liittyviä muistutuksia.

▇▇▇▇▇▇▇▇▇ on Sulautuva Yhtiö?

Sulautuvan yhtiön virallinen nimi ja liiketoiminnassa käytettävä toiminimi on Arcus ASA. Arcus on norjalainen Norjan lainsäädännön mukaan perustettu julkinen osakeyhtiö, jonka kotipaikka on Nittedal, Norja ▇▇ ▇▇▇ on 213800Z4X87YPAKKS645.

Päätoimialat

Arcus on johtava pohjoismainen toimija viinin ja väkevien alkoholijuomien tuotannossa, maahantuonnissa, myynnissä ja jakelussa4. Arcus toimii kaikissa Pohjoismaissa, ▇▇ ▇▇▇▇▇ on tytäryhtiöt Norjassa, Ruotsissa, Tanskassa, Suomessa ja Saksassa. ▇▇▇▇▇ vie väkeviä alkoholijuomia myös pohjoismaisten ja saksalaisten markkinoiden ulkopuolelle, pääasiassa Yhdysvaltoihin. Arcuksella on kolme liiketoimintasegmenttiä, Wine, Spirits, ja Logistics. Wine-liiketoimintasegmentissä Arcus tarjoaa kaikkien hintaluokkien viinejä. Valtaosa viinivalikoimasta koostuu laajasta valikoimasta lukuisten kansainvälisten tuottajien päämiesbrändejä ja rajattu mutta kasvava osa valikoimasta koostuu ▇▇▇▇▇▇▇▇ omista brändeistä, jotka se on itse kehittänyt erityisesti vastaamaan paikallisia mieltymyksiä kullakin yksittäisellä markkinalla. Spirits-liiketoimintasegmentissä Arcuksen valikoima koostuu ikonisista Arcus-brändeistä, joilla on pitkät historiat ja perinteet, ▇▇▇▇ päämiesbrändeistä. Spirits-liiketoimintasegmenttiä hallinnoidaan Norjasta, poikkeuksena tietyt tanskalaiset brändit (Aalborg ▇▇ ▇▇▇▇▇▇ Dansk), joita hallinnoidaan paikallisesti Norjan ja muiden maiden tukemana. Logistics-liiketoimintasegmentti joka toimii ulkoisesti Vectura-toiminimen alla, toimii Arcuksen logistiikkapalveluiden toimittajana ▇▇▇▇▇▇ ▇▇▇▇▇▇▇▇▇▇▇▇.

Suurimmat osakkeenomistajat

Viisi prosenttia tai enemmän Arcuksen osakkeista omistavien osakkeenomistajien tulee ilmoittaa omistuksensa Norjan arvopaperikauppalain mukaisesti. Seuraavassa taulukossa esitetään Norjan Verdipapirsentraleniin (VPS) 21.10.2020 rekisteröidyt osakkeenomistajat, jotka omistavat Arcuksen osakkeista viisi prosenttia tai enemmän:

__________________________

4 Perustuu Vinmonopoletilta (Norja), Systembolagetilta (Ruotsi), Alkolta (Suomi) ja Nielseniltä (Tanska) saatuihin myyntitilastoihin.

12

| Osakkeenomistaja | Osakkeiden lukumäärä | Prosenttia osakkeista ja äänistä | ||

| Canica AS | 30 093 077 | 44,2 | ||

| Geveran Trading Co Ltd | 6 750 000 | 9,9 | ||

| Muut osakkeenomistajat, mukaan lukien hallintarekisteröityjen osakkeiden omistajat | 31 180 178 | 45,8 | ||

| Yhtiön osakkeet yhteensä | 68 023 255 | 100,00 |

▇▇▇▇▇ ▇▇▇▇ kuin Arcus on tietoinen, Arcus ei ole suoraan tai välillisesti kenenkään yhden henkilön omistuksessa tai määräysvallassa. ▇▇▇▇▇▇▇▇ tiedossa ei ole järjestelyjä, jotka voisivat johtaa määräysvallan siirtymiseen Arcuksessa.

Toimitusjohtaja ja johtoryhmä

Seuraavassa taulukossa esitetään ▇▇▇▇▇▇▇▇ johtoryhmän jäsenet tämän Sulautumisesitteen päivämääränä:

▇▇▇▇ |

▇▇▇▇▇ | ▇▇▇▇▇▇▇▇▇ |

| ▇▇▇▇▇▇▇ ▇▇▇▇▇▇ | ▇▇▇▇▇▇▇▇▇ toimitusjohtaja | 2015 |

| ▇▇▇▇▇▇▇ ▇▇▇▇ | ▇▇▇▇▇▇▇▇▇ talousjohtaja | 2016 |

| ▇▇▇▇▇▇ ▇▇▇▇▇▇▇▇▇▇ | Group Director Spirits | 2016 |

| ▇▇▇▇▇ ▇▇▇▇▇▇▇▇ | Group Director Wine, Managing Director Vingruppen AS (Wine Norway) | 2018 |

| ▇▇▇▇▇▇ ▇▇▇▇▇▇▇ | Managing Director Vingruppen i ▇▇▇▇▇▇ ▇▇ (Wine Sweden) | 2018 |

| ▇▇▇▇▇ ▇▇▇▇▇▇ | Managing Director Vingruppen Oy (Wine Finland) | 2020 |

| ▇▇▇▇▇ ▇▇▇▇▇▇▇▇ | Group Director Production | 2020 |

| ▇▇▇▇ ▇▇▇▇ | Group Director CSR, Group Technical Services | 2018 |

| ▇▇▇-▇▇▇▇ ▇▇▇▇▇▇ | Group Director HR | 2019 |

| ▇▇▇ ▇▇▇▇▇▇▇ | Group Director IR and Communications | 2013 |

| ▇▇▇▇ ▇▇▇▇▇▇▇ | Managing Director Vectura AS | 2019 |

Lakisääteinen tilintarkastaja

Arcuksen lakisääteinen tilintarkastaja on Ernst & ▇▇▇▇▇ AS, ja päävastuullisena tilintarkastajana on hyväksytty tilintarkastaja ▇▇▇▇▇▇ ▇▇▇▇▇▇▇. ▇▇▇▇▇ & ▇▇▇▇▇ AS on Norjan tilintarkastajien järjestön ▇▇▇▇▇.

Mitkä ovat Sulautuvan Yhtiön keskeiset taloudelliset tiedot?

Seuraavissa taulukoissa esitetään ▇▇▇▇▇▇▇▇ valikoituja konsernitilinpäätöstietoja 30.6.2020 ja 30.6.2019 päättyneiltä kuuden kuukauden jaksoilta ▇▇▇▇ 31.12.2019 päättyneeltä tilikaudelta. Alla esitettävät valikoidut konsernitilinpäätöstiedot ovat peräisin ”IAS 34 – Osavuosikatsaukset” -standardin mukaisesti 30.6.2020 päättyneeltä kuuden kuukauden jaksolta laaditusta Arcuksen tilintarkastamattomasta puolivuosikatsauksesta, ja niihin sisältyy vertailutietoina esitetyt tilintarkastamattomat konsernin taloudelliset tiedot 30.6.2019 päättyneeltä kuuden kuukauden jaksolta ja EU:n käyttöön ottamien IFRS-standardien mukaisesti 31.12.2019 päättyneeltä tilikaudelta laadittu Arcuksen tilintarkastettu konsernitilinpäätös, jotka on sisällytetty tähän Sulautumisesitteeseen viittaamalla.

Seuraavissa taulukoissa esitetään yhteenveto Arcuksen keskeisistä taloudellisista tiedoista ilmoitettuina ajankohtina ja ajanjaksoina:

13

|

1.1.–30.6. ja 30.6. |

1.1.–31.12. ja 31.12. | ||

| Milj. Norjan kruunua, ellei toisin ilmoitettu |

2020 |

2019 |

2019 |

| (tilintarkastamaton) | (tilintarkastettu) | ||

| Tuloslaskelma | |||

| Liikevaihto …………………………………………….. | 1 378 | 1 250 | 2 763 |

| Oikaistu käyttökate | 186 | 129 | 397 |

| Oikaistu käyttökatemarginaali, % | 13,5% | 10,3% | 14,4% |

| Oikaistu liiketulos (EBIT) | 123 | 75 | 277 |

| Oikaistu liiketulosmarginaali, % | 8,9 % | 6,0 % | 10,0 % |

| Kauden tulos | 82 | 8 | 133 |

| Osakekohtainen tulos (NOK) | 1,19 | 0,11 | 1,94 |

| Laimennusvaikutuksella oikaistu osakekohtainen tulos (NOK) | 1,12 | 0,11 | 1,85 |

| Tase | |||

| Varat yhteensä | 6 011 | 4 991 | 5 590 |

| Oma pääoma yhteensä | 1 741 | 1 521 | 1 662 |

| Velat yhteensä | 4 270 | 3 470 | 3 928 |

| Rahavirtalaskelma | |||

| Liiketoiminnan nettorahavirta | 519 | -131 | 292 |

| Investointien nettorahavirta | -24 | -7 | -71 |

| Rahoituksen nettorahavirta | -84 | -198 | -284 |

| ____________________________________ | |||

Tilintarkastamattomat pro forma -taloudelliset tiedot

Tilintarkastamattomat pro forma -taloudelliset tiedot (“Pro forma -tiedot”) on esitetty tarkoituksena havainnollistaa Altian ja Arcuksen Sulautumisen vaikutuksia Altian taloudellisiin tietoihin ikään kuin Sulautuminen olisi tapahtunut aikaisempana ajankohtana. Pro forma -tiedot on esitetty yksinomaan havainnollistamistarkoituksessa, ▇▇ ▇▇▇ vuoksi niihin sisältyvä hypoteettinen taloudellinen asema ja liiketoiminnan tulos saattavat poiketa Yhdistyneen Yhtiön todellisesta taloudellisesta asemasta ja liiketoiminnan tuloksesta. Tilintarkastamattomat pro forma -taloudelliset tiedot eivät myöskään kuvaa mitään kustannussäästöjä, synergiaetuja tai tulevaisuudessa syntyviä integraatiokuluja, joita odotetaan muodostuvan ▇▇▇ ▇▇▇▇▇ saattaa syntyä Sulautumisen seurauksena. Tilintarkastamattomat pro forma -tuloslaskelmat 30.6.2020 päättyneeltä kuuden kuukauden jaksolta ja 31.12.2019 päättyneeltä tilikaudelta esittävät Sulautumisen vaikutukset ikään kuin Sulautuminen olisi tapahtunut 1.1.2019. Tilintarkastamattomassa pro forma -taseessa 30.6.2020 Sulautumisen vaikutukset esitetään ikään kuin Sulautuminen olisi toteutunut kyseisenä päivänä.

Pro forma -tiedot on laadittu komission delegoidun asetuksen (EU) 2019/980 liitteen 20 mukaisesti ▇▇▇▇ Altian IFRS:n mukaisessa konsernitilinpäätöksessään soveltamien laatimisperiaatteiden mukaisesti. Sulautuminen käsitellään liiketoimintojen yhdistämisenä IFRS:n mukaista hankintamenetelmää käyttäen, ja Altia on määritetty Arcuksen hankkivaksi osapuoleksi.

Pro forma -tietoja laadittaessa historiallisiin taloudellisiin tietoihin on tehty oikaisuja, jotka koskevat välittömästi Sulautumisesta johtuvien tapahtumien pro forma -vaikutusta ▇▇ ▇▇▇▇▇ ovat perusteltavissa tosiseikoin. Pro forma -oikaisut sisältävät tiettyjä oletuksia hankintavastikkeen käypään arvoon, hankintavastikkeen kohdistamiseen, tilinpäätöksen laatimisperiaatteiden yhdenmukaistamiseen ja muihin oikaisuihin liittyen, joiden uskotaan olevan kohtuullisia vallitsevissa olosuhteissa. Ottaen huomioon meneillään olevat viranomaisten hyväksyntäprosessit, jotka rajoittavat Altian pääsyä Arcuksen yksityiskohtaisiin tietoihin, esitettävät pro forma -oikaisut ovat alustavia ja perustuvat tällä hetkellä saatavilla oleviin tietoihin, ja esitetyt tiedot tulevat muuttumaan. Lopullinen hankintavastikkeen käypä arvo määritetään Täytäntöönpanopäivän osakekurssiin perustuen, hankintavastikkeen lopullinen kohdistaminen perustuu ▇▇▇▇▇▇▇▇ hankittujen varojen ja vastattavaksi otettujen velkojen käypiin arvoihin Täytäntöönpanopäivänä ja yksityiskohtainen läpikäynti Arcuksen tilinpäätöksen laatimisperiaatteista ja tilinpäätöksen esittämistavasta voidaan tehdä ▇▇▇▇▇ Täytäntöönpanopäivän jälkeen.

Ei voi olla mitään varmuutta siitä, ▇▇▇▇ Pro forma -tietoja laadittaessa käytetyt oletukset osoittautuvat oikeiksi, ja Sulautumisen lopullinen vaikutus Altian taloudellisiin tietoihin saattaa poiketa olennaisesti Pro forma -tiedoissa esitettävistä pro forma -oikaisuista. Lisäksi Yhdistyneen Yhtiön tulevaisuudessa soveltamat tilinpäätöksen laatimisperiaatteet saattavat poiketa Pro forma -tiedoissa sovelletuista laatimisperiaatteista.

Seuraavassa taulukossa esitetään yhteenveto Pro forma -tietoihin liittyvistä tunnusluvuista ilmoitettuina ajankohtina ja ajanjaksoina:

14

| 1.1.–30.6.2020 ja 30.6.2020 | 1.1.–31.12.2019 | |||||||||||||||||||||||||||||||

| Milj. euroa, ellei toisin ilmoitettu | Altia historial-linen | Arcus uudelleen-luokiteltu | Sulautu-minen | Yhdistynyt Yhtiö pro forma | Altia historial-linen | Arcus uudelleen-luokiteltu | Sulautu-minen | Yhdistynyt Yhtiö pro forma | ||||||||||||||||||||||||

| Liikevaihto | 149,3 | 127,2 | — | 276,5 | 359,6 | 280,4 | — | 640,0 | ||||||||||||||||||||||||

| Vertailukelpoinen käyttökate | 18,8 | 17,4 | — | 36,1 | 44,8 | 39,9 | — | 84,7 | ||||||||||||||||||||||||

| Käyttökate | 18,0 | 15,7 | 1,1 | 34,8 | 43,1 | 37,9 | -25,4 | 55,6 | ||||||||||||||||||||||||

| Liiketulos | 9,2 | 9,9 | -0,5 | 18,6 | 25,1 | 25,8 | -29,1 | 21,8 | ||||||||||||||||||||||||

| Kauden tulos | 7,5 | 7,6 | -0,1 | 14,9 | 18,4 | 13,5 | -24,7 | 7,2 | ||||||||||||||||||||||||

| Osakekohtainen tulos (laimentamaton), euroa | 0,22 | 0,10 | ||||||||||||||||||||||||||||||

| Varat yhteensä | 428,9 | 550,9 | 95,8 | 1 075,6 | ||||||||||||||||||||||||||||

| Oma pääoma yhteensä | 149,5 | 159,6 | 106,0 | 415,1 | ||||||||||||||||||||||||||||

| Nettovelka | 211,2 | |||||||||||||||||||||||||||||||

| Nettovelkaantumisaste, % | 50,9 | |||||||||||||||||||||||||||||||

| Omavaraisuusaste, % | 38,6 | |||||||||||||||||||||||||||||||

Mitkä ovat keskeiset Yhdistyneeseen Yhtiöön liittyvät riskit?

| · | Ei ole varmuutta siitä, ▇▇▇▇ Sulautuminen pannaan täytäntöön, tai täytäntöönpano voi viivästyä. |

| · | Sulautumista ei välttämättä panna täytäntöön tällä hetkellä suunnitellulla tavalla, millä voi olla olennaisen haitallinen vaikutus Sulautumisesta odotettaviin hyötyihin tai Altian ja/tai Arcuksen osakkeiden markkinahintaan. |

| · | Maailmantalouden, politiikan ja rahoitusmarkkinoiden epävarmoilla olosuhteilla voi olla olennaisen haitallinen vaikutus Yhdistyneen Yhtiön liiketoimintaan, taloudelliseen asemaan ja liiketoiminnan tulokseen. |

| · | Yhdistynyt Yhtiö toimii erittäin kilpaillulla markkinalla, ja kiristyvä kilpailu voi vaikuttaa Yhdistyneen Yhtiön liiketoimintaan olennaisen haitallisesti. |

| · | Valtionomisteisia vähittäismyyntimonopoleja koskevan lainsäädännön muuttuminen Yhdistyneen Yhtiön keskeisillä markkina-alueilla voi vaikuttaa negatiivisesti Yhdistyneen Yhtiön liiketoimintaan. |

| · | Verojen, erityisesti valmisteverojen, korotukset voivat vaikuttaa haitallisesti Yhdistyneen Yhtiön tuotteiden kysyntään. |

| · | Yhdistynyt Yhtiö voi epäonnistua sen strategian toimeenpanossa tai sen strategia voi itsessään olla epäonnistunut, minkä vuoksi Yhdistynyt Yhtiö ei välttämättä pysty saavuttamaan taloudellisia tavoitteitaan ja todellinen liiketoiminnan tulos voi poiketa olennaisesti Sulautumisesitteessä kuvatuista taloudellisista tavoitteista. |

| · | Yhdistynyt Yhtiö on riippuvainen korkealaatuisen suomalaisen viljan ja norjalaisen perunaväkiviinan saatavuudesta, ja muutoksilla viljan ja perunaväkiviinan tai muiden raaka-aineiden, viinien, eau-▇▇-▇▇▇▇, tarvikkeiden ja valmiiden tuotteiden saatavuudessa tai hinnoissa voi olla haitallinen vaikutus Yhdistyneen Yhtiön liiketoimintaan. |

| · | Yhdistyneen Yhtiön ja keskeisten päämiesten, asiakkaiden, toimittajien ja jakelijoiden välisten suhteiden heikentyminen ▇▇▇▇ näiden tahojen kanssa tehtyjen sopimusten menettäminen tai epäsuotuisat sopimusehdot voivat vaikuttaa haitallisesti Yhdistyneen Yhtiön liiketoimintaan. |

| · | Epäonnistuminen tarjousmenettelyissä, vaatimusten täyttämisessä ranking-sijoituksen ylläpitämiseksi tai muiden tuotevalikoimaa koskevien edellytysten täyttämisessä voi vaikuttaa haitallisesti Yhdistyneen Yhtiön liiketoimintaan. |

| · | Häiriöt ja vahingot tuotanto- ja varastolaitoksissa voivat vaikuttaa haitallisesti Yhdistyneen Yhtiön liiketoimintaan. |

15

| · | Vaikeudet lisärahoituksen saannissa tai Yhdistyneen Yhtiön lainoihin sisältyvien kovenanttiehtojen täyttämisessä ▇▇▇▇ rahoituskustannusten nousu voivat vaikuttaa haitallisesti Yhdistyneen Yhtiön taloudelliseen asemaan ja tulokseen. |

Keskeiset tiedot arvopapereista

Mitkä ovat arvopaperien tärkeimmät ominaisuudet?

Tämän Sulautumisesitteen päivämääränä Altian osakepääoma on 60 480 378,36 euroa ja liikkeeseen laskettujen osakkeiden lukumäärä on 36 140 485 osaketta. Altian osakkeilla ei ole nimellisarvoa, ne ovat euromääräisiä ja kaikki liikkeeseen lasketut osakkeet on maksettu täysimääräisesti ja laskettu liikkeeseen Suomen lakien mukaisesti. Altialla on yksi osakesarja, jonka ISIN-koodi on FI4000292438.

Arcuksen osakkeenomistajat saavat sulautumisvastikkeena 0,4618 uutta Altian osaketta (”Sulautumisvastikeosakkeet”) kutakin omistamaansa Arcuksen osaketta kohden (”Sulautumisvastike”). Sulautumisvastikeosakkeet vastaavat Altian olemassa olevaa osakesarjaa. Kukin Sulautumisvastikeosake oikeuttaa yhteen ääneen Altian yhtiökokouksissa, ja kaikki Sulautumisvastikeosakkeet tuottavat yhtäläiset oikeudet osinkoon ja muihin Altian jakokelpoisiin varoihin, mukaan lukien Altian varojen jakoon purkautumistilanteessa. Sulautumisvastikeosakkeisiin ei liity äänestysrajoituksia, ja ne ovat vapaasti luovutettavissa.

Sulautumisvastikeosakkeisiin liittyvät oikeudet määritellään Suomen osakeyhtiölaissa (624/2006, muutoksineen) (”Osakeyhtiölaki”) ja muussa soveltuvassa suomalaisessa lainsäädännössä, ja niihin kuuluu muun muassa etuoikeus merkitä Yhdistyneen Yhtiön uusia osakkeita, oikeus osallistua Yhdistyneen Yhtiön yhtiökokouksiin ja käyttää äänioikeutta, oikeus osinkoon ja muuhun oman pääoman jakamiseen ▇▇▇▇ muut Osakeyhtiölain mukaiset oikeudet.

Altian tai ▇▇▇▇▇▇▇▇ aikaisemmilta tilikausilta maksama osinko tai muun vapaan oman pääoman jakaminen ei ▇▇▇▇ viitteitä Yhdistyneen Yhtiön tulevilta tilikausilta mahdollisesti maksamista osingoista. Ei voi olla varmuutta siitä, ▇▇▇▇ Yhdistynyt Yhtiö jakaa tulevaisuudessa osinkoa tai vapaata omaa pääomaa. Yhdistynyt Yhtiö määrittää osinkokäytäntönsä Täytäntöönpanopäivän jälkeen ja arvioi vuosittain osingon tai muun vapaan oman pääoman jakamisen edellytyksiä.

Missä arvopapereilla käydään kauppaa?

Altia hakee liikkeeseen laskettavien Sulautumisvastikeosakkeiden ottamista julkisen kaupankäynnin kohteeksi Nasdaq Helsingissä. Sulautumisvastikeosakkeiden ottaminen kaupankäynnin kohteeksi tapahtuu ja kaupankäynti Sulautumisvastikeosakkeilla alkaa Täytäntöönpanopäivänä tai mahdollisimman pian sen jälkeen.